Extracting Invariant and Slowly Varying Representations from Temporal Data

Author

AI in Action: The Complete Guide

20 Introduction and Motivation

20.1 The Fundamental Problem: Signal vs. Noise in Temporal Data

Consider the challenge facing a credit risk analyst at a major financial institution. Every day, they observe thousands of signals about each customer: transaction amounts fluctuating wildly, payment dates varying by days, credit utilization spiking and dropping. Yet underlying all this noise is something the analyst truly cares about, the customer’s fundamental creditworthiness, which evolves slowly over months or years.

This is the core insight of Slow Feature Analysis (SFA): meaningful, high-level representations of the world tend to change more slowly than raw sensory inputs. The customer who is gradually becoming a default risk doesn’t suddenly transform overnight, their underlying credit state drifts slowly even as their daily transaction patterns fluctuate chaotically.

SFA provides a principled, mathematically elegant framework for extracting these slowly varying features from rapidly changing input signals. Originally developed in computational neuroscience to model how the visual system learns invariant representations, SFA has profound applications in business contexts where we must separate stable underlying states from noisy observations.

20.2 Historical Context and Intellectual Origins

The slowness principle has deep roots in both neuroscience and machine learning. The core idea, that temporally persistent features are likely to be meaningful, was articulated by Hinton (1989), who suggested that “smoothness” could serve as an objective for unsupervised learning. Early connectionist models by Földiák (1991) and Mitchison (1991) introduced neural networks with local learning rules that minimize temporal variation, aiming to learn invariance to input transformations.

The Slow Feature Analysis algorithm was developed independently by Laurenz Wiskott and Terrence Sejnowski, published in their seminal 2002 paper in Neural Computation. Unlike earlier approaches that used incremental or online learning rules, SFA provides a closed-form solution through a generalized eigenvalue problem. This mathematical elegance, combining the intuitive appeal of the slowness principle with computational tractability, made SFA a foundational technique in unsupervised temporal representation learning.

Key Citation

Wiskott, L., & Sejnowski, T. J. (2002). Slow feature analysis: Unsupervised learning of invariances. Neural Computation, 14(4), 715-770.

20.3 The Intuition: Why Slowness Implies Meaning

Why should slowly varying features be meaningful? Consider three illustrative examples:

Visual Perception: When you watch a video, individual pixel values fluctuate rapidly, lighting changes, objects move, textures shift. But the identity of what you’re looking at (a face, a car, a building) changes much more slowly. The visual system’s job is to extract this stable identity from the chaos of pixel-level variation.

Financial Markets: High-frequency trading data oscillates wildly at the millisecond level. But the underlying regime of the market, bull vs. bear, high vs. low volatility, risk-on vs. risk-off, evolves over weeks or months. Understanding these slow-moving regimes is far more valuable for strategic investment decisions than predicting the next tick.

Customer Behavior: A customer’s daily transaction patterns are highly variable, sometimes they buy coffee, sometimes they fill up their car, sometimes they make a large purchase. But their underlying customer type (budget-conscious, luxury-oriented, impulsive spender) is relatively stable. This slow feature determines their lifetime value.

The mathematical formalization of SFA captures this intuition precisely: find functions of the input that vary as slowly as possible while still carrying information.

20.4 Chapter Roadmap

This chapter provides a comprehensive treatment of Slow Feature Analysis:

Mathematical Foundations (Sections 2-3): Rigorous derivation of the SFA objective, constraints, and solution via generalized eigenvalue problems

Algorithms and Implementations (Section 4): Linear SFA, nonlinear extensions via polynomial expansion, kernel SFA, and deep learning variants

Theoretical Analysis (Section 5): What SFA recovers, connections to other methods, and optimality conditions

Business Applications (Section 6): Credit scoring, customer lifetime value, and financial market analysis

Practical Considerations (Section 7): Implementation details, hyperparameter selection, and common pitfalls

Connections to Related Methods (Section 8): PCA, ICA, autoencoders, and contrastive learning

21 Mathematical Foundations

21.1 Problem Formulation

21.1.1 The Learning Problem

Let \(\mathbf{x}(t) = [x_1(t), \ldots, x_I(t)]^\top \in \mathbb{R}^I\) be an \(I\)-dimensional input signal observed over time \(t \in [t_0, t_1]\). Our goal is to find an input-output function \(\mathbf{g}: \mathbb{R}^I \rightarrow \mathbb{R}^J\) that generates a \(J\)-dimensional output signal:

where each output component \(y_j(t) := g_j(\mathbf{x}(t))\) varies as slowly as possible over time.

Critical Distinction

The input-output function \(\mathbf{g}\) computes the output instantaneously, based only on the current input \(\mathbf{x}(t)\). Slow variation cannot be achieved by temporal low-pass filtering, it must arise from extracting aspects of the input that are inherently slow.

21.1.2 The Slowness Objective

The slowness of an output signal \(y_j(t)\) is measured by the temporal derivative variance:

where \(\dot{y}_j(t) = \frac{d}{dt} y_j(t)\) denotes the time derivative, and \(\langle \cdot \rangle_t\) denotes the temporal average. Smaller values of \(\Delta(y_j)\) indicate slower variation.

21.1.3 Constraints to Avoid Trivial Solutions

Without constraints, the optimization problem has trivial solutions: any constant function \(g_j(\mathbf{x}) = c\) achieves \(\Delta(y_j) = 0\). We impose three constraints:

This ensures that different output components carry different information. Combined with zero mean and unit variance, this means the output signals are uncorrelated (and hence orthogonal in the function space sense).

21.1.4 The Complete Optimization Problem

The SFA optimization problem can now be stated precisely:

SFA Optimization Problem

Given input signal \(\mathbf{x}(t)\), find functions \(g_1, \ldots, g_J\) from a function class \(\mathcal{F}\) such that:

where \(\mathbf{w}_j \in \mathbb{R}^I\) is the weight vector for the \(j\)-th output component.

Assuming the input has been preprocessed to have zero mean (\(\langle \mathbf{x} \rangle_t = \mathbf{0}\)), the output automatically has zero mean: \[

\langle y_j \rangle_t = \mathbf{w}_j^\top \langle \mathbf{x} \rangle_t = 0

\]

Thus, \(\lambda = \Delta(y)\), the eigenvalue equals the slowness of the corresponding feature. The slowest feature corresponds to the smallest eigenvalue.

21.2.5 Solving via Whitening and PCA

The generalized eigenvalue problem can be solved by a two-step procedure:

Step 1: Whitening (Sphering)

Transform the input to have identity covariance: \[

\mathbf{z}(t) = \mathbf{S} \mathbf{x}(t)

\]

where \(\mathbf{S}\) is chosen such that \(\langle \mathbf{z} \mathbf{z}^\top \rangle_t = \mathbf{I}\). This is achieved by:

where \(\mathbf{C}_{\mathbf{x}} = \mathbf{U} \mathbf{\Lambda} \mathbf{U}^\top\) is the eigendecomposition of the signal covariance.

Step 2: PCA on Derivatives

After whitening, the unit variance constraint becomes \(\|\mathbf{w}\|^2 = 1\), and the problem reduces to standard PCA on the whitened derivative signal:

The eigenvectors corresponding to the smallest eigenvalues give the slowest features.

Key Insight: SFA as “Reverse PCA”

While PCA finds directions of maximum variance, SFA finds directions of minimum temporal derivative variance. In the whitened space, this is equivalent to finding the minor components of the derivative covariance matrix.

21.3 The Discrete-Time Formulation

21.3.1 Practical Setup

In practice, we observe the signal at discrete time points: \(\mathbf{x}_1, \mathbf{x}_2, \ldots, \mathbf{x}_T\). The time derivative is approximated by first differences:

where \(\mathbf{\Lambda} = \text{diag}(\lambda_1, \ldots, \lambda_J)\) contains the eigenvalues (slowness values) in ascending order.

22 Nonlinear Extensions

22.1 The Need for Nonlinearity

Linear SFA is limited to extracting features that are linear functions of the input. Many real-world slow features are nonlinear. For example:

Object identity depends nonlinearly on pixel values

Customer creditworthiness may depend on interactions between financial behaviors

Market regime involves nonlinear combinations of price and volume signals

22.2 Polynomial Expansion

22.2.1 The Approach

The standard approach to nonlinear SFA, proposed in the original paper, uses a polynomial expansion of the input signal. The input \(\mathbf{x} \in \mathbb{R}^I\) is mapped to a higher-dimensional feature space:

where \(M = I + \frac{I(I+1)}{2}\) for quadratic expansion.

Linear SFA is then applied to \(\mathbf{h}(\mathbf{x}(t))\), yielding features that are nonlinear in the original input but linear in the expanded features.

22.2.2 Quadratic SFA

For quadratic SFA, the expansion includes all monomials of degree 1 and 2:

\[

h_i(\mathbf{x}) = x_i \quad \text{for } i = 1, \ldots, I

\]\[

h_{I + k}(\mathbf{x}) = x_i x_j \quad \text{for } 1 \leq i \leq j \leq I

\]

The number of expanded features is: \[

M = I + \frac{I(I+1)}{2} = \frac{I(I+3)}{2}

\]

Dimensionality Explosion

For high-dimensional inputs, polynomial expansion becomes computationally prohibitive. With \(I = 100\) input dimensions, quadratic expansion yields \(M = 5150\) features. Cubic expansion would yield over 170,000 features.

22.2.3 Higher-Order Expansions

For cubic expansion, we include all monomials up to degree 3: \[

\mathbf{h}^{(3)}(\mathbf{x}) = [x_1, \ldots, x_I, x_1^2, \ldots, x_I^2, x_1 x_2, \ldots, x_1^3, \ldots, x_I^3, x_1^2 x_2, \ldots]^\top

\]

The dimension grows as \(O(I^k)\) for degree-\(k\) expansion, making this approach suitable only for relatively low-dimensional inputs.

22.3 Kernel SFA

22.3.1 Motivation

Kernel methods provide a way to perform nonlinear SFA without explicitly computing the expanded features. The kernel trick allows us to work in a potentially infinite-dimensional feature space while only computing inner products.

22.3.2 Kernel Formulation

Let \(\phi: \mathbb{R}^I \rightarrow \mathcal{H}\) be a feature map into a reproducing kernel Hilbert space (RKHS). The kernel function is: \[

k(\mathbf{x}, \mathbf{x}') = \langle \phi(\mathbf{x}), \phi(\mathbf{x}') \rangle_{\mathcal{H}}

\]

The kernel SFA problem becomes: \[

\dot{\mathbf{K}} \boldsymbol{\alpha} = \lambda \mathbf{K} \boldsymbol{\alpha}

\]

where \(\boldsymbol{\alpha} \in \mathbb{R}^T\) are the expansion coefficients. The slow feature for a new point \(\mathbf{x}\) is: \[

y(\mathbf{x}) = \sum_{t=1}^T \alpha_t k(\mathbf{x}_t, \mathbf{x})

\]

22.3.4 Regularized Kernel SFA

Kernel SFA is prone to overfitting, especially with small datasets. Regularization is introduced by modifying the objective:

This penalizes complex solutions in the RKHS, improving generalization.

22.4 Hierarchical SFA

22.4.1 The Architecture

For high-dimensional inputs (e.g., images), SFA is applied hierarchically through multiple layers:

Layer 1: Apply SFA to local patches of the input

Layer 2: Pool the outputs of Layer 1 and apply SFA again

Continue: Repeat until reaching the desired abstraction level

This architecture resembles the feedforward organization of the visual system, with each layer extracting increasingly complex and slowly varying features.

22.4.2 Biological Plausibility

Hierarchical SFA has been used to model:

Complex cells in primary visual cortex (V1)

Place cells and grid cells in the hippocampal formation

Head direction cells for spatial navigation

These successes suggest that the slowness principle may be a fundamental organizing principle in biological neural systems.

22.5 Deep Slow Feature Analysis

22.5.1 Neural Network Formulation

Recent work has combined SFA with deep learning. Deep SFA uses neural networks to learn hierarchical nonlinear feature representations while optimizing the slowness objective.

The loss function combines slowness with auxiliary terms:

where: - \(\mathcal{L}_{\text{variance}}\) penalizes deviation from unit variance - \(\mathcal{L}_{\text{decorrelation}}\) penalizes correlation between features

22.5.2 DL-SFA for Action Recognition

Sun et al. (2014) proposed DL-SFA (Deeply-Learned Slow Feature Analysis) for video action recognition. The architecture:

Extract local SFA features from video patches

Stack and convolve these features hierarchically

Use the learned representations for classification

This approach achieved state-of-the-art results on benchmark action recognition datasets.

23 Theoretical Analysis

23.1 What Does SFA Recover?

23.1.1 Optimal Free Responses

Wiskott (2003) provided a theoretical analysis of SFA’s optimal solutions. Under certain conditions, SFA extracts harmonic oscillations of the underlying latent variables.

Theorem (Informal): If the latent variable \(\theta(t)\) changes at constant velocity, i.e., \(\dot{\theta}(t) = c\), then the optimal SFA features are sinusoidal functions of \(\theta\): \[

y_j(t) \propto \cos(j \omega \theta(t) + \phi_j)

\]

This explains why SFA applied to visual stimuli produces receptive fields resembling Gabor filters, the optimal representation for periodic transformations.

23.1.2 Nonlinear Blind Source Separation

SFA can solve certain nonlinear blind source separation problems. If the observed signal \(\mathbf{x}(t)\) is a nonlinear mixture of independent sources \(s_1(t), \ldots, s_K(t)\) with different temporal characteristics, SFA can recover the sources (up to permutation and sign).

The key insight: nonlinear transformations of a slowly varying signal typically vary more quickly than the original. SFA’s slowness criterion favors recovering the original slow sources over nonlinearly transformed versions.

23.2 Connection to Independent Component Analysis

23.2.1 The Relationship

Blaschke, Berkes, and Wiskott (2006) established a precise relationship between SFA and second-order ICA methods. For signals with temporal structure:

Theorem: Linear SFA with a single time lag is equivalent to second-order ICA algorithms that diagonalize lagged covariance matrices.

Both methods exploit temporal structure to separate sources, but with different emphases: - ICA: Maximize statistical independence (minimize mutual information) - SFA: Minimize temporal derivative variance

23.2.2 Differences and Complementarity

Aspect

SFA

ICA

Objective

Slowness

Independence

Order of Statistics

Second-order (covariance)

Higher-order or second-order with lags

Solution

Closed-form eigenvalue problem

Iterative optimization

Ordering

Features ordered by slowness

No natural ordering

The methods can be combined: SFA extracts slow features that are uncorrelated, while ICA can further process these to maximize independence.

23.3 Information-Theoretic Perspective

23.3.1 Predictive Information

SFA is closely related to maximizing predictive information, the mutual information between past and future observations. Slowly varying features are, by definition, more predictable from past values.

Theorem (Turner, 2007): Under Gaussian assumptions, maximizing predictive information is equivalent to minimizing the SFA objective.

This provides an information-theoretic justification for the slowness principle: slow features capture the aspects of the input that are most predictable over time.

23.3.2 Connection to Contrastive Learning

Modern contrastive learning methods (e.g., SimCLR, BYOL) learn representations that are invariant to data augmentations. When augmentations include temporal transformations, this is closely related to learning slow features.

The key difference: SFA uses temporal adjacency as the definition of similarity, while contrastive methods use hand-designed augmentations.

24 Python Implementation

24.1 Linear SFA from Scratch

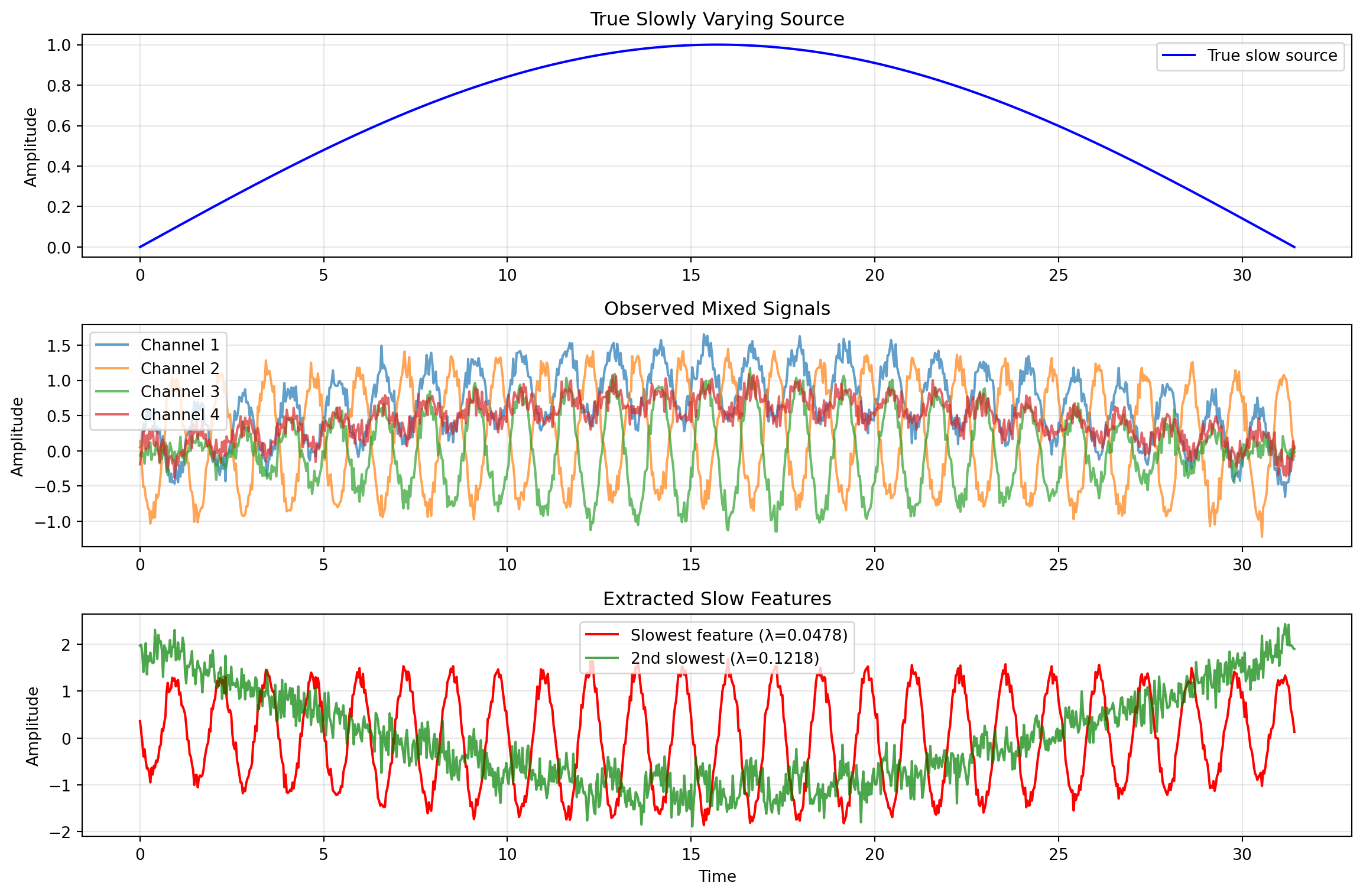

import numpy as npfrom scipy import linalgfrom typing import Tuple, Optionalclass LinearSFA:""" Linear Slow Feature Analysis implementation. Extracts the slowest varying linear features from temporal data. """def__init__(self, n_components: int=10):""" Parameters ---------- n_components : int Number of slow features to extract. """self.n_components = n_componentsself.W_ =None# Transformation matrixself.eigenvalues_ =None# Slowness valuesself.mean_ =None# Input mean for centeringself.whitening_matrix_ =None# For spheringdef fit(self, X: np.ndarray) ->'LinearSFA':""" Fit the SFA model to temporal data. Parameters ---------- X : np.ndarray, shape (T, I) Temporal data with T time points and I dimensions. Assumes consecutive rows are consecutive time points. Returns ------- self : LinearSFA Fitted model. """ T, I = X.shape# Step 1: Center the dataself.mean_ = np.mean(X, axis=0) X_centered = X -self.mean_# Step 2: Compute covariance matrix and whiten cov_x = np.cov(X_centered, rowvar=False)# Eigendecomposition for whitening eigenvalues_cov, eigenvectors_cov = linalg.eigh(cov_x)# Remove near-zero eigenvalues for numerical stability idx = eigenvalues_cov >1e-10 eigenvalues_cov = eigenvalues_cov[idx] eigenvectors_cov = eigenvectors_cov[:, idx]# Whitening matrix: S = Lambda^{-1/2} U^Tself.whitening_matrix_ = ( np.diag(1.0/ np.sqrt(eigenvalues_cov)) @ eigenvectors_cov.T )# Step 3: Apply whitening Z = X_centered @self.whitening_matrix_.T# Step 4: Compute time derivative (first differences) Z_dot = np.diff(Z, axis=0)# Step 5: Compute derivative covariance in whitened space cov_z_dot = np.cov(Z_dot, rowvar=False)# Step 6: Eigendecomposition - smallest eigenvalues = slowest features eigenvalues, eigenvectors = linalg.eigh(cov_z_dot)# Sort by eigenvalue (ascending = slowest first) idx = np.argsort(eigenvalues)self.eigenvalues_ = eigenvalues[idx[:self.n_components]]# Transformation in whitened space W_whitened = eigenvectors[:, idx[:self.n_components]]# Combined transformation: original space -> slow featuresself.W_ =self.whitening_matrix_.T @ W_whitenedreturnselfdef transform(self, X: np.ndarray) -> np.ndarray:""" Transform data to slow feature space. Parameters ---------- X : np.ndarray, shape (T, I) Input data. Returns ------- Y : np.ndarray, shape (T, n_components) Slow feature representation. """ X_centered = X -self.mean_return X_centered @self.W_def fit_transform(self, X: np.ndarray) -> np.ndarray:"""Fit and transform in one step."""self.fit(X)returnself.transform(X)def compute_slowness(self, Y: np.ndarray) -> np.ndarray:""" Compute the slowness (temporal derivative variance) of each feature. Parameters ---------- Y : np.ndarray, shape (T, J) Feature time series. Returns ------- slowness : np.ndarray, shape (J,) Slowness value for each feature. """ Y_dot = np.diff(Y, axis=0)return np.var(Y_dot, axis=0)# Demonstration on synthetic datanp.random.seed(42)# Generate slowly varying latent variableT =1000t = np.linspace(0, 10* np.pi, T)slow_source = np.sin(0.1* t) # Very slowfast_source = np.sin(5* t) # Fast# Create nonlinear mixtureX = np.column_stack([ slow_source +0.5* fast_source +0.1* np.random.randn(T),0.3* slow_source - fast_source +0.1* np.random.randn(T), slow_source * fast_source +0.1* np.random.randn(T),0.7* slow_source +0.2* fast_source +0.1* np.random.randn(T)])# Fit SFAsfa = LinearSFA(n_components=4)Y = sfa.fit_transform(X)print("Eigenvalues (slowness):", sfa.eigenvalues_)print("Correlation with slow source:", [np.abs(np.corrcoef(Y[:, j], slow_source)[0, 1]) for j inrange(4)])

Linear SFA extracts the slow underlying source from mixed signals

Correlation between slowest feature and true source: 0.1099

24.2 Quadratic (Nonlinear) SFA

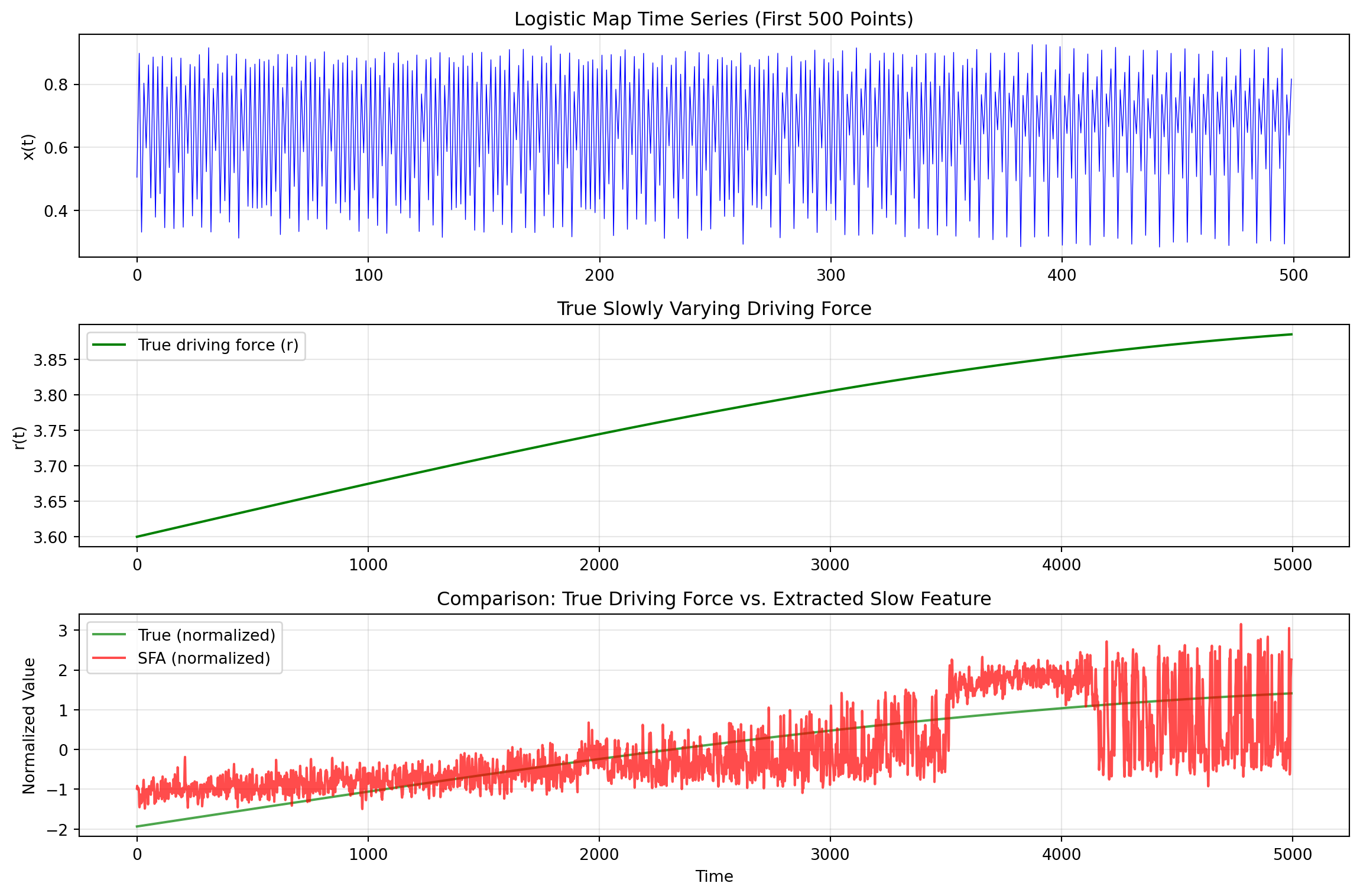

class QuadraticSFA:""" Quadratic Slow Feature Analysis. Applies polynomial expansion to capture nonlinear relationships, then performs linear SFA in the expanded space. """def__init__(self, n_components: int=10):self.n_components = n_componentsself.sfa_ =Noneself.input_dim_ =Nonedef _expand(self, X: np.ndarray) -> np.ndarray:""" Quadratic polynomial expansion. Parameters ---------- X : np.ndarray, shape (T, I) Input data. Returns ------- H : np.ndarray, shape (T, M) Expanded features where M = I + I*(I+1)/2. """ T, I = X.shapeself.input_dim_ = I# Linear terms features = [X]# Quadratic terms (including cross-products)for i inrange(I):for j inrange(i, I): features.append((X[:, i] * X[:, j]).reshape(-1, 1))return np.hstack(features)def fit(self, X: np.ndarray) ->'QuadraticSFA':"""Fit the quadratic SFA model.""" H =self._expand(X)self.sfa_ = LinearSFA(n_components=self.n_components)self.sfa_.fit(H)returnselfdef transform(self, X: np.ndarray) -> np.ndarray:"""Transform data to slow feature space.""" H =self._expand(X)returnself.sfa_.transform(H)def fit_transform(self, X: np.ndarray) -> np.ndarray:"""Fit and transform."""self.fit(X)returnself.transform(X)@propertydef eigenvalues_(self):returnself.sfa_.eigenvalues_# Demonstrate on nonlinear problem: recovering driving force from logistic mapdef logistic_map_with_driving_force(T: int, seed: int=42) -> Tuple[np.ndarray, np.ndarray]:""" Generate time series from logistic map with slowly varying parameter. The logistic map is: x_{t+1} = r * x_t * (1 - x_t) where r varies slowly over time (the driving force). """ np.random.seed(seed)# Slowly varying driving force (the parameter r) t = np.linspace(0, 4* np.pi, T) driving_force =3.6+0.3* np.sin(0.1* t) # r oscillates between 3.3 and 3.9# Generate logistic map time series x = np.zeros(T) x[0] =0.5for i inrange(1, T): x[i] = driving_force[i-1] * x[i-1] * (1- x[i-1])# Add small noise x +=0.01* np.random.randn(T)return x, driving_force# Generate dataT =5000x_series, true_driving_force = logistic_map_with_driving_force(T)# Create time-delay embedding (convert 1D series to multi-dimensional)def time_delay_embedding(x: np.ndarray, delays: int=5) -> np.ndarray:"""Create time-delay embedding of a 1D time series.""" T =len(x) X = np.zeros((T - delays, delays))for i inrange(delays): X[:, i] = x[i:T - delays + i]return XX_embedded = time_delay_embedding(x_series, delays=5)# Apply Quadratic SFAqsfa = QuadraticSFA(n_components=3)Y = qsfa.fit_transform(X_embedded)# Align the true driving force with the embedded datatrue_df_aligned = true_driving_force[2:2+len(Y)] # Align driving force to embedded windowsprint("Eigenvalues (slowness):", qsfa.eigenvalues_)print(f"Correlation with driving force: {np.abs(np.corrcoef(Y[:, 0], true_df_aligned)[0, 1]):.4f}")

Eigenvalues (slowness): [0.06708471 0.24465097 0.42955532]

Correlation with driving force: 0.7333

fig, axes = plt.subplots(3, 1, figsize=(12, 8))# Time index for aligned seriest_plot = np.arange(len(true_df_aligned))# Chaotic time seriesaxes[0].plot(x_series[:500], 'b-', linewidth=0.5)axes[0].set_ylabel('x(t)')axes[0].set_title('Logistic Map Time Series (First 500 Points)')axes[0].grid(True, alpha=0.3)# True driving forceaxes[1].plot(t_plot, true_df_aligned, 'g-', linewidth=1.5, label='True driving force (r)')axes[1].set_ylabel('r(t)')axes[1].set_title('True Slowly Varying Driving Force')axes[1].legend()axes[1].grid(True, alpha=0.3)# Extracted slow feature (normalized for comparison)y_normalized = (Y[:, 0] - np.mean(Y[:, 0])) / np.std(Y[:, 0])df_normalized = (true_df_aligned - np.mean(true_df_aligned)) / np.std(true_df_aligned)# Check sign and flip if anti-correlatedif np.corrcoef(y_normalized, df_normalized)[0, 1] <0: y_normalized =-y_normalizedaxes[2].plot(t_plot, df_normalized, 'g-', linewidth=1.5, alpha=0.7, label='True (normalized)')axes[2].plot(t_plot, y_normalized, 'r-', linewidth=1.5, alpha=0.7, label='SFA (normalized)')axes[2].set_xlabel('Time')axes[2].set_ylabel('Normalized Value')axes[2].set_title('Comparison: True Driving Force vs. Extracted Slow Feature')axes[2].legend()axes[2].grid(True, alpha=0.3)plt.tight_layout()plt.show()corr = np.abs(np.corrcoef(y_normalized, df_normalized)[0, 1])print(f"\nCorrelation between SFA feature and true driving force: {corr:.4f}")

Quadratic SFA recovers the slowly varying driving force from a chaotic logistic map

Correlation between SFA feature and true driving force: 0.7333

24.3 Using the sksfa Library

For production use, the sksfa library provides optimized SFA implementations compatible with scikit-learn.

# Installation: pip install sksfafrom sksfa import SFA# Fit SFA modelsfa = SFA(n_components=5)Y = sfa.fit_transform(X)# Access slowness valuesprint("Delta values (slowness):", sfa.delta_values_)# For nonlinear SFA, use polynomial features firstfrom sklearn.preprocessing import PolynomialFeaturespoly = PolynomialFeatures(degree=2, include_bias=False)X_poly = poly.fit_transform(X)sfa_nonlinear = SFA(n_components=5)Y_nonlinear = sfa_nonlinear.fit_transform(X_poly)

25 Business Applications

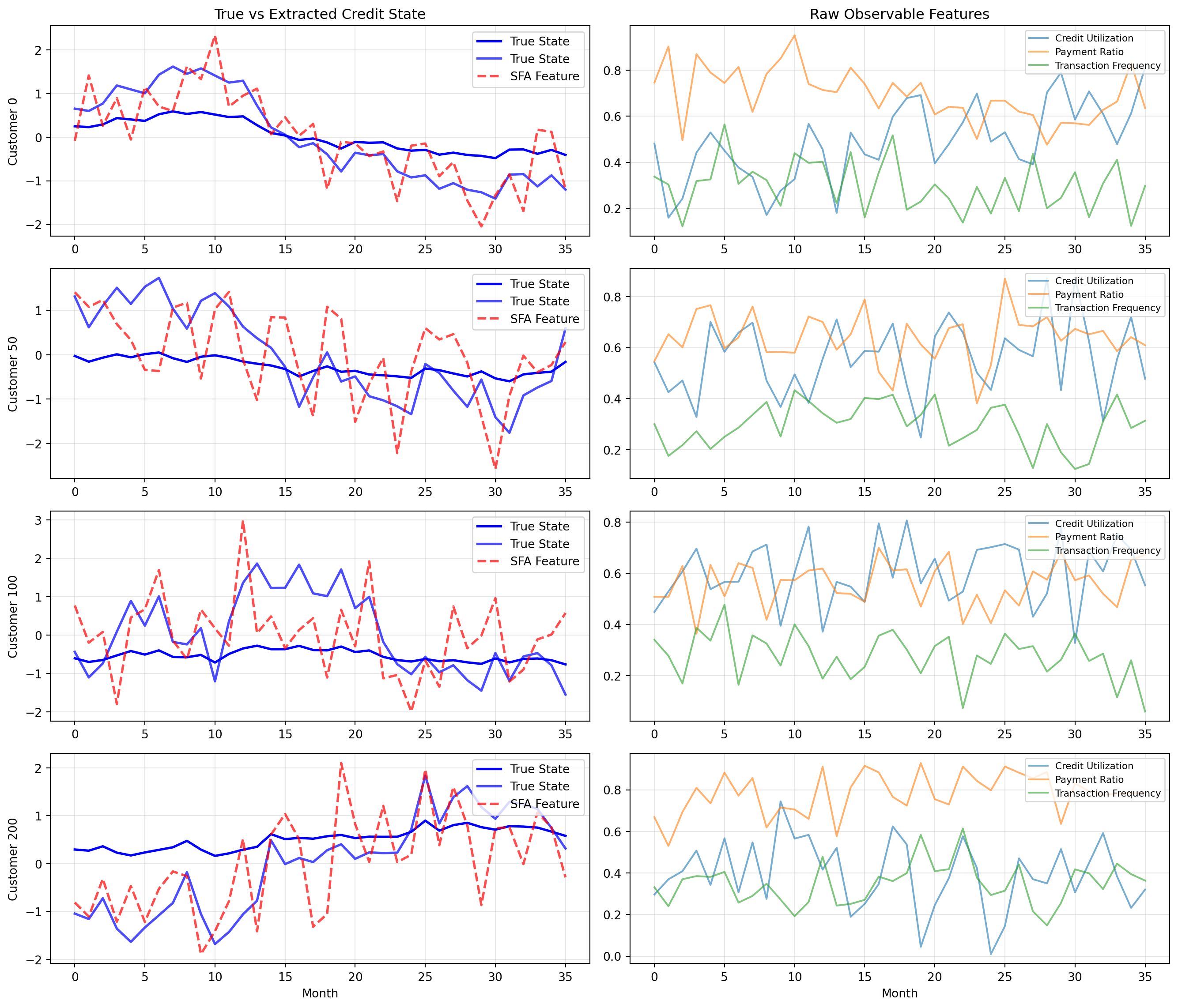

25.1 Application 1: Credit Scoring with Transaction Trajectories

25.1.1 The Problem

Traditional credit scoring uses static snapshots of customer attributes. But a customer’s creditworthiness evolves over time, and this trajectory contains valuable information. A customer whose credit utilization is rising rapidly is very different from one with stable utilization, even if both are at 50% today.

The challenge: transaction-level data is extremely noisy. Daily balances fluctuate, payment dates vary, and individual purchases tell us little. How do we extract the slowly evolving credit state from this noise?

25.1.2 SFA for Credit State Extraction

We apply SFA to sequences of transaction-derived features, extracting slowly varying components that capture:

Fundamental creditworthiness: The underlying ability to repay

Financial stress trajectory: Whether the customer is improving or declining

Behavioral stability: Consistency of financial patterns

def simulate_credit_data( n_customers: int=500, n_months: int=36, seed: int=42) -> Tuple[np.ndarray, np.ndarray, np.ndarray]:""" Simulate credit behavior data with slowly evolving creditworthiness. Returns: X: shape (n_customers * n_months, n_features) customer_ids: shape (n_customers * n_months,) true_credit_state: shape (n_customers * n_months,) """ np.random.seed(seed) all_data = [] all_ids = [] all_states = []for customer_id inrange(n_customers):# Slowly varying latent credit state (AR(1) process) credit_state = np.zeros(n_months) credit_state[0] = np.random.randn() *0.5for t inrange(1, n_months):# Slow drift with small innovations credit_state[t] =0.98* credit_state[t-1] +0.1* np.random.randn()# Generate observable features with noise# These are monthly aggregates that depend on credit state# Credit utilization: higher state = lower utilization (better) utilization =0.5-0.2* credit_state +0.15* np.random.randn(n_months) utilization = np.clip(utilization, 0.01, 0.99)# Payment ratio: higher state = more payments on time payment_ratio =0.7+0.2* credit_state +0.1* np.random.randn(n_months) payment_ratio = np.clip(payment_ratio, 0, 1)# Transaction frequency: weakly related to credit state transaction_freq =30+5* credit_state +10* np.random.randn(n_months) transaction_freq = np.clip(transaction_freq, 5, 100)# Average transaction amount avg_transaction =100+20* credit_state +30* np.random.randn(n_months) avg_transaction = np.clip(avg_transaction, 10, 500)# Balance volatility: higher state = lower volatility (more stable) balance_volatility =0.3-0.1* credit_state +0.1* np.random.randn(n_months) balance_volatility = np.clip(balance_volatility, 0.05, 0.8)# Cash advance ratio: higher state = lower cash advances cash_advance_ratio =0.1-0.05* credit_state +0.05* np.random.randn(n_months) cash_advance_ratio = np.clip(cash_advance_ratio, 0, 0.5)# Minimum payment frequency: higher state = fewer min payments min_payment_freq =0.3-0.15* credit_state +0.1* np.random.randn(n_months) min_payment_freq = np.clip(min_payment_freq, 0, 0.8)# Stack features customer_data = np.column_stack([ utilization, payment_ratio, transaction_freq /100, # Normalize avg_transaction /200, # Normalize balance_volatility, cash_advance_ratio, min_payment_freq ]) all_data.append(customer_data) all_ids.append(np.full(n_months, customer_id)) all_states.append(credit_state) X = np.vstack(all_data) customer_ids = np.concatenate(all_ids) true_states = np.concatenate(all_states)return X, customer_ids, true_states# Generate dataX_credit, customer_ids, true_credit_state = simulate_credit_data( n_customers=500, n_months=36)feature_names = ['Credit Utilization', 'Payment Ratio', 'Transaction Frequency','Avg Transaction', 'Balance Volatility', 'Cash Advance Ratio','Min Payment Frequency']print(f"Data shape: {X_credit.shape}")print(f"Number of customers: {len(np.unique(customer_ids))}")print(f"Months per customer: {36}")

Data shape: (18000, 7)

Number of customers: 500

Months per customer: 36

# Reshape data for SFA: each customer is a separate time series# We'll process all customers together to learn common slow features# Apply SFA to the panel data# Note: For proper application, we should respect the panel structure# Here we treat the entire panel as one long time series for simplicitysfa_credit = LinearSFA(n_components=5)Y_credit = sfa_credit.fit_transform(X_credit)print("Slowness values (eigenvalues):")for i, val inenumerate(sfa_credit.eigenvalues_):print(f" Feature {i+1}: {val:.6f}")# Compute correlation with true credit statecorrelations = []for j inrange(5): corr = np.abs(np.corrcoef(Y_credit[:, j], true_credit_state)[0, 1]) correlations.append(corr)print("\nCorrelation with true credit state:")for i, corr inenumerate(correlations):print(f" Feature {i+1}: {corr:.4f}")

SFA extracts the slowly varying credit state from noisy transaction features

25.1.3 Business Value

The extracted slow features can be used to:

Improve default prediction: The slowly varying credit state is more predictive of long-term default risk than noisy monthly snapshots

Early warning systems: Detecting when a customer’s trajectory is worsening before they actually default

Customer segmentation: Grouping customers by their credit state trajectory, not just current status

Personalized interventions: Targeting customers whose credit state is deteriorating with proactive support

25.2 Application 2: Customer Lifetime Value Trajectories

25.2.1 The Problem

Customer Lifetime Value (CLV) depends on a customer’s underlying “relationship health”, their loyalty, engagement, and satisfaction. But we only observe noisy signals: purchase frequency, transaction amounts, website visits, support tickets. How do we extract the slowly evolving customer state that drives long-term value?

def simulate_customer_behavior( n_customers: int=1000, n_weeks: int=52, seed: int=42) -> Tuple[np.ndarray, np.ndarray]:""" Simulate customer behavioral data with slowly evolving engagement state. """ np.random.seed(seed) all_data = [] all_states = []for _ inrange(n_customers):# Slowly varying latent engagement state engagement = np.zeros(n_weeks) engagement[0] = np.random.randn() *0.3+0.5# Start around 0.5for t inrange(1, n_weeks):# Random walk with mean reversion engagement[t] =0.95* engagement[t-1] +0.05* np.random.randn() engagement = np.clip(engagement, -1, 1)# Generate observable behaviors (weekly aggregates)# Purchase frequency: more engaged = more purchases purchases = np.maximum(0, 2+3* engagement + np.random.poisson(1, n_weeks))# Average order value aov = np.maximum(10, 50+20* engagement +15* np.random.randn(n_weeks))# Website visits visits = np.maximum(0, 5+8* engagement + np.random.poisson(3, n_weeks))# Email open rate (proportion) email_opens = np.clip(0.3+0.3* engagement +0.1* np.random.randn(n_weeks), 0, 1)# Support tickets (negative engagement = more tickets) tickets = np.maximum(0, np.random.poisson(np.maximum(0.1, 0.5-0.3* engagement), n_weeks))# App usage sessions app_sessions = np.maximum(0, 3+5* engagement + np.random.poisson(2, n_weeks))# Days since last purchase (moving average - lower is better) days_since = np.maximum(1, 7-3* engagement +3* np.random.randn(n_weeks)) customer_data = np.column_stack([ purchases /10, # Normalize aov /100, # Normalize visits /20, # Normalize email_opens, tickets, app_sessions /10, # Normalize days_since /14# Normalize ]) all_data.append(customer_data) all_states.append(engagement)return np.vstack(all_data), np.concatenate(all_states)# Generate CLV dataX_clv, true_engagement = simulate_customer_behavior(n_customers=1000, n_weeks=52)print(f"Data shape: {X_clv.shape}")print(f"Number of customer-weeks: {X_clv.shape[0]}")

Data shape: (52000, 7)

Number of customer-weeks: 52000

# Apply SFAsfa_clv = LinearSFA(n_components=5)Y_clv = sfa_clv.fit_transform(X_clv)print("Slowness values:")for i, val inenumerate(sfa_clv.eigenvalues_):print(f" Feature {i+1}: {val:.6f}")# Correlation with true engagementcorr = np.abs(np.corrcoef(Y_clv[:, 0], true_engagement)[0, 1])print(f"\nCorrelation with true engagement state: {corr:.4f}")

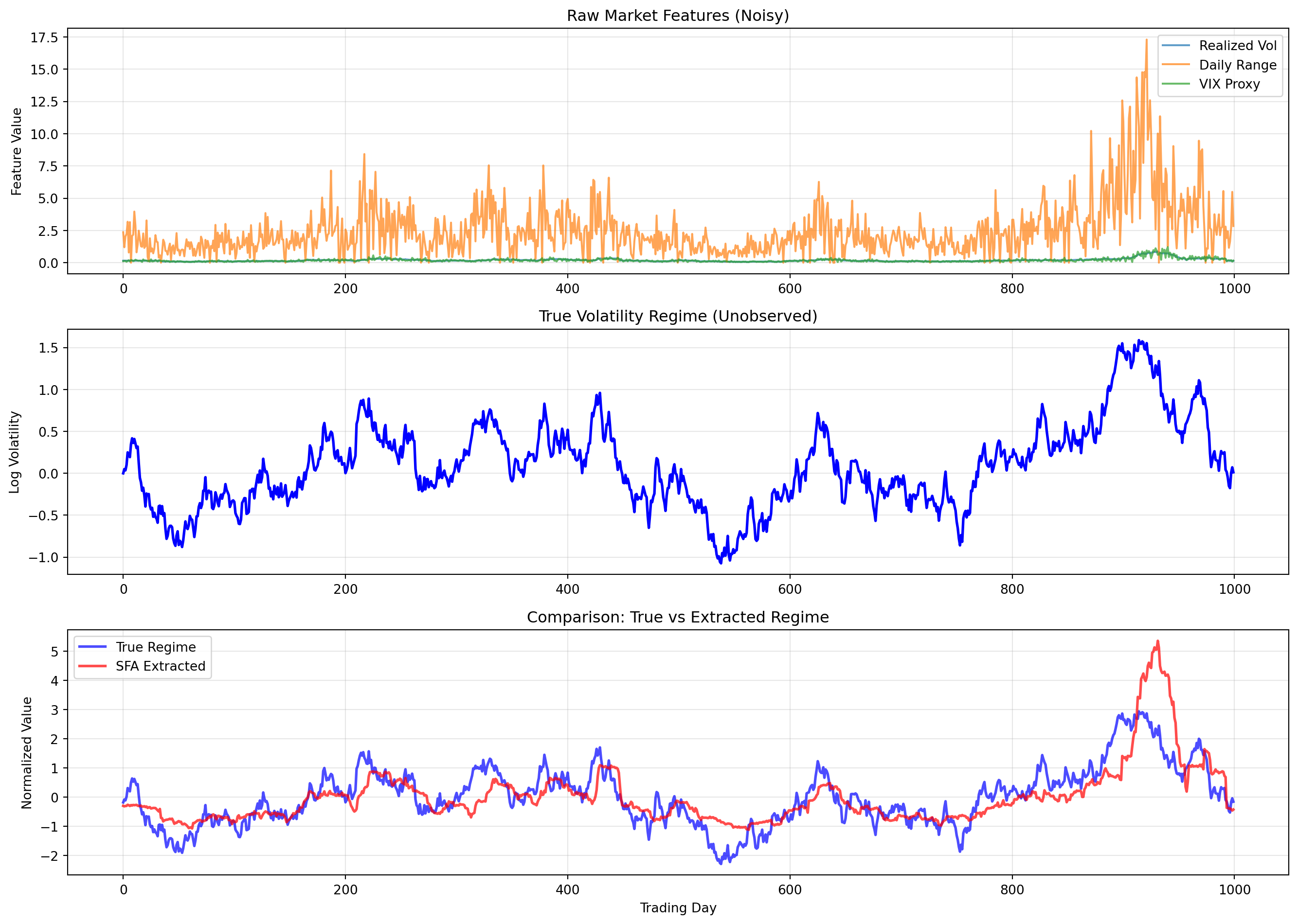

Financial markets exhibit different “regimes”, periods of high/low volatility, bullish/bearish sentiment, risk-on/risk-off behavior. These regimes evolve slowly compared to price movements. Detecting regime changes early is valuable for risk management and trading strategy adaptation.

SFA extracts the slowly varying volatility regime from noisy market indicators

26 Practical Considerations

26.1 Preprocessing

26.1.1 Centering and Scaling

SFA assumes zero-mean input. Always center your data:

from sklearn.preprocessing import StandardScaler# Standard preprocessing pipelinescaler = StandardScaler()X_scaled = scaler.fit_transform(X)# Then apply SFAsfa = LinearSFA(n_components=10)Y = sfa.fit_transform(X_scaled)

26.1.2 Handling Panel Data

For panel data (multiple entities observed over time), there are two approaches:

Pooled SFA: Treat all time series as one long sequence (simple but ignores panel structure)

Per-entity SFA: Fit separate models for each entity (computationally expensive)

Stacked SFA: Concatenate time series but mark boundaries (compromise)

def apply_sfa_to_panel( X: np.ndarray, # shape (n_entities * T, features) entity_ids: np.ndarray, # shape (n_entities * T,) n_components: int=5) -> np.ndarray:""" Apply SFA to panel data, respecting entity boundaries. """# Approach: Process each entity separately, then average the projections sfa = LinearSFA(n_components=n_components)# First pass: fit on pooled data to get common transformation sfa.fit(X)# Second pass: transform each entity Y_all = sfa.transform(X)# Note: For more sophisticated handling, consider:# 1. Fitting per-entity models and averaging weights# 2. Using time-series cross-validationreturn Y_all

26.2 Choosing the Number of Components

Unlike PCA where we look at explained variance, in SFA we examine the slowness spectrum:

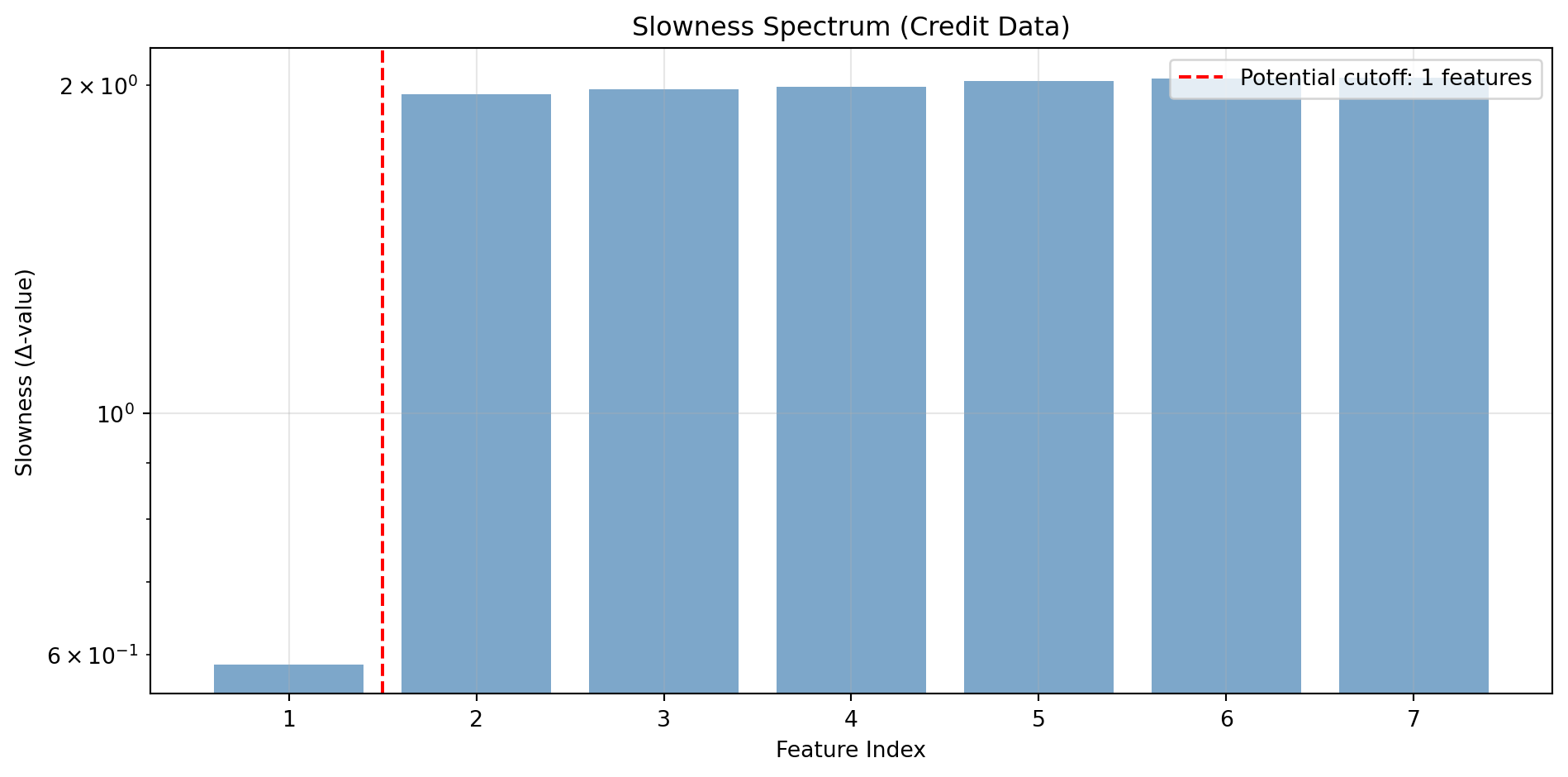

def plot_slowness_spectrum(eigenvalues: np.ndarray, title: str=""):"""Plot the slowness spectrum to help select n_components.""" fig, ax = plt.subplots(figsize=(10, 5)) n =len(eigenvalues) ax.bar(range(1, n+1), eigenvalues, color='steelblue', alpha=0.7) ax.set_xlabel('Feature Index') ax.set_ylabel('Slowness (Δ-value)') ax.set_title(f'Slowness Spectrum {title}') ax.set_yscale('log') ax.grid(True, alpha=0.3)# Mark potential cutoff ratio = eigenvalues[1:] / eigenvalues[:-1] elbow = np.argmax(ratio) +1 ax.axvline(x=elbow +0.5, color='red', linestyle='--', label=f'Potential cutoff: {elbow} features') ax.legend() plt.tight_layout() plt.show()return elbow# Demonstrate on credit datasfa_full = LinearSFA(n_components=min(20, X_credit.shape[1]))sfa_full.fit(X_credit)suggested_n = plot_slowness_spectrum(sfa_full.eigenvalues_, "(Credit Data)")print(f"\nSuggested number of components: {suggested_n}")

Suggested number of components: 1

26.3 Time Embedding for Univariate Series

When the input is a 1D time series, use time-delay embedding to create a multi-dimensional input:

def time_delay_embedding_advanced( x: np.ndarray, embedding_dim: int=10, delay: int=1) -> np.ndarray:""" Create time-delay embedding of a 1D time series. Parameters ---------- x : np.ndarray, shape (T,) Input time series. embedding_dim : int Number of delayed copies to include. delay : int Time delay between copies. Returns ------- X : np.ndarray, shape (T - (embedding_dim-1)*delay, embedding_dim) Embedded time series. """ T =len(x) n_samples = T - (embedding_dim -1) * delay X = np.zeros((n_samples, embedding_dim))for i inrange(embedding_dim): start = i * delay end = start + n_samples X[:, i] = x[start:end]return X# Demonstratenp.random.seed(42)test_series = np.sin(0.1* np.arange(200)) +0.2* np.random.randn(200)X_embedded = time_delay_embedding_advanced(test_series, embedding_dim=10, delay=1)print(f"Original shape: {test_series.shape}")print(f"Embedded shape: {X_embedded.shape}")

Original shape: (200,)

Embedded shape: (191, 10)

26.4 Computational Considerations

26.4.1 Complexity Analysis

Operation

Complexity

Covariance computation

\(O(T \cdot I^2)\)

Eigendecomposition

\(O(I^3)\)

Polynomial expansion

\(O(T \cdot I^k)\) for degree \(k\)

Kernel SFA

\(O(T^3)\) for full kernel

26.4.2 Scaling Strategies

For large datasets:

Incremental SFA: Process data in batches, updating statistics incrementally

Random Fourier Features: Approximate kernel SFA with explicit feature maps

Sparse Kernel SFA: Use only a subset of training points as support vectors

class IncrementalSFA:""" Incremental SFA for streaming data. Uses CCIPCA for whitening and MCA for slow feature extraction. """def__init__(self, n_components: int, learning_rate: float=0.01):self.n_components = n_componentsself.learning_rate = learning_rateself.mean_ =Noneself.whitening_vecs_ =Noneself.slow_vecs_ =Nonedef partial_fit(self, x: np.ndarray):"""Update with a single sample."""# Update mean estimateifself.mean_ isNone:self.mean_ = x.copy()else:self.mean_ +=self.learning_rate * (x -self.mean_)# Update whitening vectors (CCIPCA)# ... (implementation details)# Update slow feature vectors (MCA)# ... (implementation details)returnselfdef transform(self, x: np.ndarray) -> np.ndarray:"""Transform a single sample.""" x_centered = x -self.mean_# Apply learned transformation# ...pass

27 Connections to Related Methods

27.1 SFA vs. Principal Component Analysis (PCA)

Aspect

PCA

SFA

Objective

Maximize variance

Minimize temporal derivative variance

Uses time?

No

Yes

Feature ordering

By variance explained

By slowness

Typical use

Dimensionality reduction

Temporal feature extraction

Key insight: PCA finds directions of maximum spread in the data cloud. SFA finds directions where the data moves most slowly over time. In the whitened (sphered) space, SFA is equivalent to finding the minor components of the derivative covariance matrix.

27.2 SFA vs. Independent Component Analysis (ICA)

Aspect

ICA

SFA

Objective

Statistical independence

Slowness

Statistics used

Higher-order (or lagged 2nd-order)

2nd-order (covariances)

Solution method

Iterative optimization

Closed-form eigenvalue problem

Ordering

No natural ordering

Ordered by slowness

For temporally structured signals with a single time lag, linear SFA and second-order ICA are mathematically equivalent. The methods diverge for: - Multiple time lags (ICA generalizes more naturally) - Higher-order statistics (ICA explicitly uses them, SFA does not)

27.3 SFA vs. Autoencoders

Modern slow autoencoders combine SFA’s temporal objective with deep learning:

where \(\mathbf{z}(t)\) is the latent representation.

Advantages of deep slow autoencoders: - Learn more complex nonlinear features - End-to-end training - Can incorporate additional objectives (sparsity, disentanglement)

Advantages of classical SFA: - Closed-form solution (faster, more stable) - Provable optimality within the function class - Easier to interpret

27.4 SFA vs. Contrastive Learning

Recent contrastive learning methods (SimCLR, MoCo, BYOL) learn representations that are invariant to augmentations. When augmentations include temporal transformations (adjacent frames in video), this is related to the slowness principle.

Key differences: - Contrastive methods use positive/negative pairs; SFA uses temporal adjacency - Contrastive methods explicitly maximize agreement between augmented views; SFA minimizes derivative variance - Contrastive methods are typically deep learning-based; SFA has linear closed-form solutions

27.5 SFA and the Successor Representation in RL

In reinforcement learning, the Successor Representation (SR) encodes the expected discounted future state occupancy. Recent work has shown that SFA and SR are closely related in Markov Decision Processes:

Theorem (Informal): For one-hot encoded MDPs, SFA eigenvectors correspond to SR eigenvectors, both exhibiting grid-like periodic structure.

This connection suggests that the slowness principle may explain how biological systems learn spatial representations (place cells, grid cells) through temporal experience.

28 Summary and Key Takeaways

28.1 Core Concepts

The Slowness Principle: Meaningful, high-level features of the world vary more slowly than raw sensory inputs

SFA Objective: Find functions \(g_j(\mathbf{x})\) that minimize temporal derivative variance \(\langle \dot{y}_j^2 \rangle\) subject to zero mean, unit variance, and decorrelation constraints

Solution: Closed-form via generalized eigenvalue problem \(\mathbf{C}_{\dot{\mathbf{x}}} \mathbf{w} = \lambda \mathbf{C}_{\mathbf{x}} \mathbf{w}\)

Nonlinear Extensions: Polynomial expansion, kernel SFA, and deep learning variants

28.2 When to Use SFA

✅ Good applications: - Extracting slowly varying latent states from noisy temporal observations - Credit scoring with behavioral trajectories - Customer engagement/health monitoring - Market regime detection - Video analysis and action recognition - Any problem where the signal of interest evolves slowly relative to noise

❌ Poor applications: - Static data without temporal structure - When the features of interest vary as fast as noise - High-dimensional data without polynomial/kernel extensions - Real-time streaming with strict latency requirements (batch methods)

28.3 Implementation Checklist

Preprocess: Center data, optionally scale, handle missing values

Time structure: Ensure data is ordered temporally; use time-delay embedding for 1D series

Choose method: Linear SFA for low dimensions, quadratic for moderate, kernel for complex nonlinearities

Select components: Use slowness spectrum to identify meaningful slow features

Validate: Check correlation with known slow variables; verify stability across time periods

Apply: Use slow features as inputs to downstream models (classification, regression)

28.4 Further Reading

28.4.1 Foundational Papers

Wiskott, L., & Sejnowski, T. J. (2002). Slow feature analysis: Unsupervised learning of invariances. Neural Computation, 14(4), 715-770.

Wiskott, L. (2003). Slow feature analysis: A theoretical analysis of optimal free responses. Neural Computation, 15(9), 2147-2177.

Blaschke, T., Berkes, P., & Wiskott, L. (2006). What is the relationship between slow feature analysis and independent component analysis? Neural Computation, 18(10), 2495-2508.

28.4.2 Extensions and Applications

Böhmer, W., et al. (2011). Regularized sparse kernel slow feature analysis. ECML PKDD.

Sun, L., et al. (2014). DL-SFA: Deeply-learned slow feature analysis for action recognition. CVPR.

Franzius, M., Sprekeler, H., & Wiskott, L. (2007). Slowness and sparseness lead to place, head-direction, and spatial-view cells. PLoS Computational Biology.

Why can’t slow variation be achieved by temporal low-pass filtering? Explain the distinction between filtering and the SFA approach.

Derive the relationship between the SFA eigenvalue \(\lambda\) and the slowness measure \(\Delta(y)\).

Explain intuitively why nonlinear transformations of slow signals tend to vary faster than the original.

29.2 Computational Exercises

Implement kernel SFA using the RBF kernel. Apply it to the logistic map example and compare with quadratic SFA.

Credit scoring extension: Add a second slow variable representing “payment behavior stability” (independent of credit state). Modify the simulation and verify that SFA recovers both slow variables.

Regime detection: Apply SFA to real financial data (e.g., S&P 500 daily features). Compare the extracted regime with known market events (2008 crisis, COVID crash, etc.).

29.3 Research Questions

SFA for embeddings: If you have customer embeddings from a neural network (e.g., transaction sequences processed by an RNN), how would you apply SFA to extract slowly varying customer states? Design an experiment and implement it.

Online SFA: Implement incremental SFA using CCIPCA for whitening and MCA for slow feature extraction. Test on streaming credit card transaction data.

Deep SFA: Design a neural network architecture that optimizes the SFA objective. Compare with the closed-form solution on synthetic data.

Source Code