Show code

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import sys

sys.path.insert(0, '../code')

from creditutils import load_taiwan_default, ks_statistic

from sklearn.metrics import roc_auc_score

np.random.seed(42)Application scoring freezes at origination. Behavioral scoring does not. Once a borrower opens an account, every monthly bill, every repayment, every utilization swing reveals fresh evidence about the probability of default. A model that ignores that stream wastes most of what the bank actually knows. A model that uses it must deal with time: observations arrive in sequence, distributions drift, and today’s probability of default is a conditional forecast given the entire past trajectory.

This chapter formalizes dynamic credit risk as a filtering problem over a state space. The borrower occupies a latent risk state that evolves stochastically. The lender observes noisy signals (repayment status, balance, utilization, transaction streams) and updates beliefs in real time. We derive five estimators that implement this view at different resolutions: a time-dependent Cox model for continuous covariates (Section 36.3), a hidden Markov model over delinquency buckets (Section 36.4), a recurrent neural network over transaction sequences (Section 36.5), a recursive Bayesian update for monthly repayment signals (Section 36.6), and a survival model with time-varying covariates (Section 36.7). We benchmark them on the Taiwan credit-card panel, which carries six months of repayment history for thirty thousand accounts and is the closest public analog to a real behavioral file.

The regulatory backdrop is IFRS 9. Since 2018 banks must provision expected credit loss lifetime after a significant increase in credit risk, and the trigger is almost always a behavioral signal. The same infrastructure now serves Basel III point-in-time probability of default, SR 11-7 ongoing monitoring, and EU AI Act post-market monitoring under Article 72. The engineering problem is the same across all three: score every account every month, cheaply, consistently, and with an audit trail.

Let \(i \in \{1, \ldots, N\}\) index accounts and \(t \in \{1, 2, \ldots\}\) index observation months. Write \(X_{i,t}\) for the covariate vector of account \(i\) at time \(t\), \(Y_{i,t} \in \{0, 1\}\) for a default event during month \(t\), and \(D_{i,t} \in \{0, 1, 2, \ldots, K\}\) for the delinquency bucket (0 = current, 1 = 30 days past due, up to \(K\) = charged-off). Let \(\tau_i\) denote the default time of account \(i\) and \(Z_i \in \mathbb{R}^d\) a vector of static origination attributes. All probabilities carry an implicit conditioning on the information filtration \(\mathcal{F}_t = \sigma(\{X_{i,s}, D_{i,s}, Y_{i,s} : s \le t\})\).

Behavioral scoring outperforms application scoring by a wide margin once accounts mature. Thomas (2000) reviewed a decade of UK bank data and reported AUC gains of 0.08 to 0.15 once six months of repayment history entered the model. Crook & Bellotti (2010) replicated the gain on UK consumer loans and showed that the improvement was concentrated in mid-life accounts, where application variables had gone stale but default had not yet crystallized. Leow & Crook (2014) pushed the analysis into continuous time using intensity models for delinquency transitions. Djeundje & Crook (2018) extended varying coefficient splines to panel credit data and documented monotone improvement over static hazards.

Application scoring and behavioral scoring answer different questions. Application scoring asks whether to approve a new applicant given a limited snapshot of origination data. Behavioral scoring asks whether to extend a credit line, raise a limit, reprice, collect, or derecognize an existing account given a rich history of repayment and transaction behavior. The two tasks share feature engineering patterns but diverge on the label definition, the time horizon, the reject-inference burden, and the regulatory weight. Application scores must survive legal scrutiny under ECOA and FCRA at the adverse-action point. Behavioral scores rarely trigger adverse action directly, but they feed the IFRS 9 staging, the Basel capital calculation, and the collections strategy, all of which inherit the scrutiny.

The accounting angle sharpened the stakes. IFRS 9, effective 1 January 2018, requires expected credit loss to be recognized over the full remaining life of an instrument whenever credit risk has increased significantly since initial recognition (Basel Committee on Banking Supervision, 2017). Stage 2 provisioning is roughly twelve times Stage 1 on a typical retail book. The transfer criterion is behavioral. A 30-day arrear, a sustained utilization spike, a reduction in minimum payment all push the account into Stage 2 and double the loss allowance. A bank without a behavioral model is flying blind into a volatile accounting line. The US analog is CECL under ASC 326, which imposes lifetime expected credit loss from the day of origination rather than only after SICR, but the underlying behavioral infrastructure is identical.

The modeling angle sharpened too. Transaction data became observable in bulk through open banking and card-network rails. Hochreiter & Schmidhuber (1997) gave us a sequence model that handles long contexts. Vaswani et al. (2017) gave us attention. Neither was invented for credit, but both transferred cleanly, and the current state of the art on public behavioral benchmarks uses one of the two. The classical Cox, Markov, and logistic families did not disappear; they remain the most common production estimators because they are auditable, calibratable, and cheap to retrain. The sequence models are challengers that often win on discrimination but lose on explainability, and the choice of champion reflects institutional risk tolerance more than raw AUC.

The operational angle closes the loop. Basel III point-in-time probability of default must be refreshed at least quarterly. SR 11-7 requires ongoing performance monitoring of every model in production (Board of Governors of the Federal Reserve System and Office of the Comptroller of the Currency, 2011). EU AI Act Article 72 now requires providers of high-risk systems to maintain a post-market monitoring plan with quantitative thresholds (European Parliament and Council, 2024). Behavioral scoring is the glue. Pick one estimator, score every account every month, log the distribution of scores, and half of the compliance obligations fall out for free. The other half are about data lineage and change control, which this chapter addresses in the deployment and regulatory sections.

The academic literature has evolved alongside these practical concerns. The surveys of Thomas (2000) and Hand & Henley (1997) remain the best entry points for the classical tradition. The empirical studies of Leow & Crook (2014), Djeundje & Crook (2018), and Crook & Bellotti (2010) establish the modern benchmarks on UK data. The machine-learning tradition started in credit with Baesens et al. (2005) and the neural-network survival models of the early 2000s, and continues today with applications of sequence models on transaction streams. The cross-pollination between the two traditions is incomplete: the classical tradition underweights expressive nonlinear models, the ML tradition underweights survival structure and censoring. This chapter treats the two as complements rather than substitutes and expects the practical answer to be a hybrid.

Emerging markets make the dynamics harder and the stakes higher. A Vietnamese consumer finance book shows a sharp January or February trough in repayment rates, the well-known Tet effect. Layered on top is an informal-sector income volatility signal that a US or European behavioral model is not built to absorb (International Monetary Fund, 2023). Monthly billing cycles land on the wrong side of Lunar New Year bonuses for some cohorts and the right side for others. A behavioral score that lumps January into a rolling 3-month average without a Tet indicator produces biased Stage 2 transfer rates under IFRS 9 and destabilizes the collections queue precisely when volume is highest. The same filtering machinery developed below still applies; the seasonal and informal-income adjustments are additive layers, not alternative estimators.

The commercial angle completes the picture. A correctly refreshed behavioral score enables line-management decisions that a static score cannot. Line increases for customers whose score has improved recover the cost of a poor origination model. Early-stage collections workflows triggered by a score deterioration of twenty points recover a measurable share of expected losses. Retention offers conditioned on behavioral stability protect the best customers from attrition. None of these are possible without a filter that tracks the account in real time, and none of them were part of the original application-scoring mandate.

Think of each borrower as a discrete time stochastic process. Let \(S_{i,t} \in \mathcal{S}\) be a latent risk state, let \(X_{i,t}\) be observable covariates, and let \(Y_{i,t}\) be the default indicator. The joint law factorizes as

\[ p(S_{i,1:T}, X_{i,1:T}, Y_{i,1:T}) = \prod_{t=1}^{T} p(S_{i,t} \mid S_{i,t-1}) p(X_{i,t} \mid S_{i,t}) p(Y_{i,t} \mid S_{i,t}, X_{i,t}). \tag{36.1}\]

Equation Eq. 38.2 is the hidden Markov assumption. It is strong but it buys identification. Relaxing it in stages produces every estimator in this chapter. If \(S_{i,t} = X_{i,t}\) (observable state) and \(p(Y_{i,t} \mid S_{i,t})\) is a logistic function we recover behavioral logistic regression. If \(\mathcal{S}\) is finite and we treat \(D_{i,t}\) as a noisy observation of \(S_{i,t}\) we obtain the hidden Markov delinquency model of Section 36.4. If \(S_{i,t}\) is a high-dimensional deterministic function of the history through a recurrent network we get the LSTM model of Section 36.5. If we collapse the state into a scalar hazard we recover the time-dependent Cox model.

The state-space reading has three consequences that application scoring obscures. First, the observable output at time \(t\) is not a label but a likelihood contribution to a trajectory, so the unit of analysis shifts from the account to the account-month. Second, the objective function is the joint log-likelihood over the entire panel, which admits hierarchical extensions such as random account effects or shared latent factors. Third, the prediction target depends on the forecast horizon \(h\), so the same filter produces different scores for one-month collections, twelve-month Basel, and lifetime IFRS 9 use cases. A production model typically returns all three as outputs of a single forward pass.

The observable quantity of interest is the conditional point-in-time probability of default over a horizon \(h\),

\[ \operatorname{PD}^{\text{PiT}}_{i,t}(h) = \Pr(\tau_i \le t + h \mid \mathcal{F}_t), \tag{36.2}\]

where \(\tau_i\) is the first time \(Y_{i,s} = 1\). For IFRS 9 Stage 1 the horizon is twelve months. For Stage 2 it is the remaining lifetime, often capped by contract maturity. The point-in-time qualifier contrasts with the through-the-cycle probability used for Basel IRB capital, which is an average of Eq. 36.2 over a full credit cycle. Conversion between the two is a central calibration task; we revisit it in the regulatory section.

Two further objects matter. The delinquency transition kernel

\[ P_t[j \mid k] = \Pr(D_{i,t+1} = j \mid D_{i,t} = k, X_{i,t}), \tag{36.3}\]

governs the migration of accounts across buckets. For credit cards it is typically a banded \(8 \times 8\) matrix on buckets \(\{0, 30, 60, 90, 120, 150, 180, \text{CO}\}\). The hazard intensity

\[ \lambda_i(t \mid X_{i,t}) = \lim_{\Delta \downarrow 0} \frac{\Pr(\tau_i \in [t, t + \Delta) \mid \tau_i \ge t, X_{i,t})}{\Delta}, \tag{36.4}\]

governs first-passage default. Eq. 36.2, Eq. 36.3, and Eq. 36.4 carry the same statistical content when the state process is Markov and continuous. They diverge the moment we admit history dependence or unobserved heterogeneity.

Stepanova & Thomas (2001) introduced proportional-hazards analysis of behavioral scores, under the name PHAB. The idea was to treat monthly behavioral covariates as time-varying regressors in a Cox model and let the partial likelihood handle censoring. Formally assume

\[ \lambda_i(t \mid X_{i,t}) = \lambda_0(t) \exp\!\left(\beta^{\top} X_{i,t}\right), \tag{36.5}\]

with \(\lambda_0\) an unspecified baseline hazard and \(X_{i,t}\) a predictable covariate path. The partial likelihood at event time \(t_k\) over the risk set \(R(t_k)\) is

\[ L_k(\beta) = \frac{\exp(\beta^{\top} X_{i_k, t_k})}{\sum_{j \in R(t_k)} \exp(\beta^{\top} X_{j, t_k})}, \tag{36.6}\]

and the log partial likelihood aggregates across events. Two facts make Eq. 36.6 practical for billions of account-months. First, the risk set at event time \(t_k\) requires only the covariate vectors of accounts still alive at \(t_k\), which is a streaming aggregation. Second, the score equation

\[ \begin{aligned} U(\beta) &= \sum_k \left\{ X_{i_k, t_k} - \bar X(\beta, t_k) \right\} = 0, \\ \bar X(\beta, t_k) &= \frac{\sum_{j \in R(t_k)} X_{j,t_k} e^{\beta^{\top} X_{j,t_k}}}{\sum_{j \in R(t_k)} e^{\beta^{\top} X_{j,t_k}}}, \end{aligned} \tag{36.7}\]

factorizes over events, which Lin and Wei exploited to give a sandwich variance estimator robust to clustering at the account level. Thomas et al. (2017) give the textbook version. For behavioral scoring the key move is to enter utilization, delinquency lag, and payment-to-balance ratio as time-varying covariates rather than baseline features. The information gain is large and the implementation cost is an extra indexing column.

A twist specific to credit is left truncation. Accounts enter observation when they open, which is not the origin of the behavioral time axis if we condition on survival to month six. The delayed-entry Cox likelihood handles this by restricting each account’s risk-set contribution to \(t \ge L_i\), its entry time. Djeundje & Crook (2018) push further by letting \(\beta\) itself vary smoothly in \(t\) through penalized splines, which captures the vintage effect that application coefficients age nonlinearly.

Ties require attention. Banks often observe default at month-end granularity, so multiple accounts default in the same calendar month. Efron’s approximation handles the resulting ties with negligible bias. Breslow’s approximation is faster but underestimates the baseline hazard when the tied set is large, which it routinely is on a credit-card book. Exact partial likelihood is tractable only for small tied sets.

Informative censoring is a deeper problem. Accounts leave the portfolio for reasons correlated with risk: voluntary attrition by low-risk customers, involuntary closure by the bank for high-risk customers. The Cox model assumes noninformative censoring. Two standard responses are to treat attrition as a competing risk (Leow & Crook, 2014) or to extend the state space with a closure-cause indicator and model each exit type separately. Ignoring the problem biases \(\hat\beta\) in the direction of the risk-closure correlation. On a credit-card book the bias is typically modest for utilization and payment ratio and larger for balance growth, because rapid balance growth is both a default precursor and a trigger for proactive bank closure.

A second Cox variant exchanges proportional hazards for a discrete-time logistic formulation (Banasik et al., 1999). Write the discrete hazard \(h_{i,t} = \Pr(\tau_i = t \mid \tau_i \ge t, X_{i,t}) = \sigma(\alpha_t + \beta^{\top} X_{i,t})\) with \(\alpha_t\) a time-specific intercept. The log-likelihood is a product over observation months of Bernoulli terms, so a standard logistic regression on the stacked (account-month) panel recovers \(\beta\). This construction is what most banks actually call “behavioral PD model” internally, because it hides the survival machinery behind a familiar logistic interface. The equivalence to Eq. 36.5 holds when the baseline hazard is a free function of time.

Consider delinquency buckets \(\mathcal{S} = \{0, 1, \ldots, K\}\) with \(K\) the charge-off absorbing state. Some of the true state is hidden because 30-day buckets smooth over partial cures and credit-bureau reporting lags distort the observed trajectory. Cyert et al. (1962) pioneered Markov chain modeling of receivables and Jarrow et al. (1997) extended it to term structures. We follow the HMM formulation of Rabiner (1989) for notation.

Let \(S_t\) be a latent bucket with transition matrix \(A \in \mathbb{R}^{(K+1) \times (K+1)}\) and let \(O_t \in \mathcal{O}\) be the observed bucket with emission distribution \(B[o \mid s] = \Pr(O_t = o \mid S_t = s)\). The initial distribution is \(\pi\). The forward variable

\[ \alpha_t(s) = \Pr(O_{1:t} = o_{1:t}, S_t = s) \tag{36.8}\]

satisfies the recursion \(\alpha_1(s) = \pi_s B[o_1 \mid s]\) and

\[ \alpha_{t+1}(s') = B[o_{t+1} \mid s'] \sum_s \alpha_t(s) A[s' \mid s]. \tag{36.9}\]

The backward variable

\[ \beta_t(s) = \Pr(O_{t+1:T} = o_{t+1:T} \mid S_t = s) \tag{36.10}\]

satisfies \(\beta_T(s) = 1\) and \(\beta_t(s) = \sum_{s'} A[s' \mid s] B[o_{t+1} \mid s'] \beta_{t+1}(s')\).

The posterior state probability \(\gamma_t(s) = \Pr(S_t = s \mid O_{1:T}) = \alpha_t(s) \beta_t(s) / \sum_{s'} \alpha_t(s') \beta_t(s')\) and the posterior transition \(\xi_t(s, s') = \Pr(S_t = s, S_{t+1} = s' \mid O_{1:T}) = \alpha_t(s) A[s' \mid s] B[o_{t+1} \mid s'] \beta_{t+1}(s') / \sum_{u,v} \alpha_t(u) A[v \mid u] B[o_{t+1} \mid v] \beta_{t+1}(v)\) together define the E-step sufficient statistics.

The Baum-Welch algorithm (Baum et al., 1970) is the EM instance that maximizes the observed data log-likelihood \(\log \Pr(O_{1:T})\) by iterating

\[ \hat\pi_s = \gamma_1(s), \qquad \hat A[s' \mid s] = \frac{\sum_{t=1}^{T-1} \xi_t(s, s')}{\sum_{t=1}^{T-1} \gamma_t(s)}, \qquad \hat B[o \mid s] = \frac{\sum_{t : o_t = o} \gamma_t(s)}{\sum_{t=1}^{T} \gamma_t(s)}. \tag{36.11}\]

Convergence of Eq. 36.11 is monotone in \(\log \Pr(O_{1:T})\). The identifiability caveat is the usual one: permutations of state labels produce identical likelihoods, so parameter comparisons across re-fits require a canonical relabeling (for example, sort states by the probability of emitting bucket zero).

The portfolio-level likelihood is the product over accounts, so gradient and E-step aggregations factorize. On a panel of \(N\) accounts with \(T\) months the per-iteration cost is \(O(N T (K+1)^2)\), which is embarrassingly parallel and fits any map-reduce backend.

Four implementation details matter in production. First, numerical underflow is inevitable without scaling, because the forward recursion multiplies probabilities of increasingly long sequences. We rescale \(\alpha_t\) to sum to one at each step and track the log-sum of scaling constants. Second, Baum-Welch converges to local optima, so multiple random restarts plus the best likelihood are the pragmatic default. Third, model selection across \(K\) uses BIC on the held-out portion of the panel; AIC overfits on long sequences. Fourth, covariate-dependent transitions are an important extension for credit: the probability of migrating from bucket 30 to bucket 60 depends on utilization and payment history, so a multinomial logistic regression replaces the constant \(A[\cdot \mid s]\).

A covariate-dependent HMM is sometimes called an input-output HMM. The M-step for \(A\) becomes a weighted multinomial logistic fit with \(\xi_t(s, s')\) as weights. The E-step is unchanged. The cost per iteration rises by the cost of one logistic regression per source state and per iteration, which on a modern column store is negligible. The benefit is a calibrated covariate-conditional transition kernel that maps cleanly to IFRS 9 staging.

Connections to the classical Markov receivables models are direct. Cyert et al. (1962) estimated \(A\) by direct transition counting when the state is observed; the Baum-Welch posterior reduces to an indicator when emission noise is zero. Jarrow et al. (1997) exponentiate a generator \(Q\) to obtain \(A(\Delta) = \exp(Q \Delta)\) and thus support irregular observation intervals. Lando & Skødeberg (2002) estimate \(Q\) from continuous rating histories, which is the corporate analog of a retail delinquency HMM and has stronger identification when data are dense.

Transaction streams are variable-length. A credit-card file might record zero or twelve hundred transactions in a month. Two neural architectures handle that cleanly: LSTM (Hochreiter & Schmidhuber, 1997) and Transformer (Vaswani et al., 2017). Both learn a function \(h_t = f_\theta(X_{1:t})\) that compresses the past into a fixed-dimension state, and then output \(\Pr(Y_{t+1} = 1 \mid X_{1:t}) = \sigma(w^{\top} h_t + b)\).

The LSTM cell is

\[ \begin{aligned} f_t &= \sigma(W_f [h_{t-1}, x_t] + b_f), \\ i_t &= \sigma(W_i [h_{t-1}, x_t] + b_i), \\ o_t &= \sigma(W_o [h_{t-1}, x_t] + b_o), \\ \tilde c_t &= \tanh(W_c [h_{t-1}, x_t] + b_c), \\ c_t &= f_t \odot c_{t-1} + i_t \odot \tilde c_t, \\ h_t &= o_t \odot \tanh(c_t). \end{aligned} \tag{36.12}\]

The gates \(f_t, i_t, o_t\) control how information flows through the cell state \(c_t\), and the design of Eq. 36.12 is what lets gradients survive long unrolls. The Transformer alternative replaces recurrence with scaled dot-product attention:

\[ \text{Attention}(Q, K, V) = \text{softmax}\!\left(\frac{QK^{\top}}{\sqrt{d_k}}\right) V, \tag{36.13}\]

with queries, keys, and values produced by linear projections of the token sequence plus positional encodings. Vaswani et al. (2017) parallelized this across positions, which turned out to matter when sequences are long and hardware is GPU.

For credit the usual framing is to bin transactions into daily or hourly tokens (amount, merchant category code, channel) and train with binary cross-entropy against the default indicator at a twelve-month horizon. Label leakage is the main trap. Always truncate the input sequence at the score date, never include transactions after the performance window began, and back-date the score by the time it took the feature pipeline to land the row.

Three further design choices dominate empirical performance. The first is tokenization. Raw transactions have an amount, a merchant category code (MCC), a channel (chip, magstripe, e-commerce), a time of day, and a flag for recurring-payment status. A standard encoding embeds the MCC into a small vector, bins the amount log-scaled into twenty quantiles, and concatenates with a learned hour-of-day embedding. The result is a token of dimension roughly thirty-two, which fits comfortably into an LSTM or Transformer input layer. A common ablation shows that MCC embeddings explain about forty percent of the sequence-model gain over bag-of-features baselines, amount bins explain another thirty percent, and the remainder comes from the sequence structure itself.

The second is horizon matching. A twelve-month default horizon is standard for Basel PD but arbitrary for behavioral staging. A short horizon (one month) captures immediate arrears, which is what collections teams want. A long horizon (twenty-four months) captures slow-motion deterioration, which is what IFRS 9 Stage 2 needs. Multi-task training with separate heads for multiple horizons typically dominates single-horizon training when the training set is large enough, because the shared backbone learns a richer representation.

The third is sequence length. Transaction sequences are long. A typical active credit-card account generates twenty to fifty transactions per month, so a two-year window is five hundred to twelve hundred tokens. Vanilla Transformers scale as \(O(L^2)\) in sequence length, which is painful above a few hundred tokens. Practical tricks include sparse attention patterns (Vaswani et al., 2017 inspired a long line of follow-ups), chunked cross-attention, and heavy downsampling at the token level (bin by week rather than by transaction). LSTMs scale linearly in length and remain the default for sequence lengths above one thousand.

The fourth design choice, sometimes forgotten, is the output head. The last hidden state carries information about the final transactions, which may be zero if the account has gone dormant. Mean pooling or attention pooling over the whole sequence usually outperforms last-state readout when the prediction target is a lagged default indicator. A simple ensemble of last-state and mean-pool heads captures both modes and typically adds another 0.01 to 0.02 in AUC.

A lighter-weight alternative keeps the model logistic and applies Bayesian updating to the coefficient. Let the prior on the score be

\[ s_{i,0} \sim \mathcal{N}(\mu_0, \sigma_0^2), \qquad \operatorname{logit} \Pr(Y_{i,t+1} = 1 \mid s_{i,t}) = -s_{i,t}. \tag{36.14}\]

Observation at month \(t\) is the repayment indicator \(r_{i,t} \in \{0, 1\}\) with likelihood

\[ \Pr(r_{i,t} = 1 \mid s_{i,t}) = \sigma(s_{i,t} - c_t), \tag{36.15}\]

where \(c_t\) is a month-specific threshold calibrated so that the portfolio-average repayment probability matches the observed rate. The posterior

\[ p(s_{i,t+1} \mid r_{i,1:t}) \propto p(s_{i,0}) \prod_{u=1}^{t} p(r_{i,u} \mid s_{i,u}) p(s_{i,u+1} \mid s_{i,u}) \tag{36.16}\]

is intractable in closed form, but a Laplace approximation or a Kalman-style linearization of Eq. 36.15 around the current posterior mean gives a recursive update. Write \(m_t = \mathbb{E}[s_{i,t} \mid r_{i,1:t}]\) and \(v_t = \operatorname{Var}[s_{i,t} \mid r_{i,1:t}]\). Assuming a Gaussian random-walk dynamic \(s_{i,t+1} = s_{i,t} + \eta_t\) with \(\eta_t \sim \mathcal{N}(0, q)\), the update is

\[ m_{t+1} = m_t + v_t \left(r_{i,t+1} - \sigma(m_t - c_{t+1})\right), \qquad v_{t+1} = v_t + q - v_t^2 \sigma(m_t - c_{t+1})(1 - \sigma(m_t - c_{t+1})). \tag{36.17}\]

This is a scalar Kalman filter on the logit. It is cheap, online, and produces credible intervals for the score, which matter for IFRS 9 staging thresholds.

The innovation \(r_{i,t+1} - \sigma(m_t - c_{t+1})\) is the prediction error. It encodes how much the month’s observation surprised the current belief. The gain \(v_t\) scales the update: an uncertain prior shifts more. The random-walk variance \(q\) is a design parameter. Large \(q\) makes the filter responsive to recent behavior and noisy. Small \(q\) makes it slow to update and stable. A reasonable calibration is to pick \(q\) such that the implied half-life of old evidence matches the business cycle of the product, roughly six months for revolving credit and twenty-four months for unsecured term loans.

Two extensions earn their keep. The first replaces the scalar state with a vector state carrying separate components for payment behavior, utilization, and macro exposure. The filter is then a multivariate Kalman filter with a block-structured transition matrix. The second adds a macro factor \(F_t\) common to all accounts, modeled as its own state equation. The resulting model is a panel state-space with both idiosyncratic and common components, which is the dynamic-factor view of credit risk that Jarrow et al. (1997) pioneered at the portfolio level.

The recursive Bayesian view clarifies the relationship between behavioral and application scoring. Application scoring fixes the posterior at \(t = 0\) using origination features only. Behavioral scoring updates the same posterior with each new observation. The two are not competing models; they are the same model at different information sets. A bank that retrains them as separate estimators is wasting information and inviting inconsistency.

Behavioral covariates typically enter survival models through the counting-process formulation of Stepanova & Thomas (2001). Each account contributes a sequence of risk intervals \([t_{i,j-1}, t_{i,j})\) during which \(X_{i,t}\) is constant, and the partial likelihood treats each interval as a separate Cox contribution. The construction is equivalent to Eq. 36.5 but cleaner for panel data with monthly refresh.

Banasik et al. (1999) challenged the assumption that every borrower eventually defaults and proposed a mixture-cure model where a fraction of the population is immune. Let \(\pi(Z_i) = \Pr(\tau_i = \infty \mid Z_i)\) be the cure probability as a function of baseline covariates. The survival function is

\[ S(t \mid Z_i, X_{i,1:t}) = \pi(Z_i) + (1 - \pi(Z_i)) S_0\!\left(\int_0^t \exp(\beta^{\top} X_{i,s}) \, ds\right), \tag{36.18}\]

with \(S_0\) the baseline survival. Eq. 36.18 reduces to Eq. 36.5 when \(\pi = 0\) and captures the large fraction of mortgage accounts that simply never default even over a ten-year horizon. Estimation uses EM: an expected membership in the susceptible group at the E-step, a weighted Cox partial likelihood at the M-step.

The five derivations so far solve a one-output problem at a time: a hazard, a posterior, a probability of default at a single horizon. IFRS 9 staging, Basel capital, ICAAP, and pricing all consume the term structure of PD, the function \(h \mapsto \operatorname{PD}^{\text{PiT}}_{i,t}(h)\) defined in Eq. 36.2. Producing it from a one-horizon estimator means refitting at every horizon or extrapolating with assumptions the data did not see, which is what Section 9.8 and Section 9.4 warn against. The forecasting literature has taken a different route: estimate the full vector \(\big(\operatorname{PD}_{i,t}(1), \ldots, \operatorname{PD}_{i,t}(H)\big)\) jointly from the same forward pass, with one of three families of architectures.

Iterated forecasters predict one step ahead and roll the forecast forward \(H\) times, feeding their own previous output back as input. DeepAR (Salinas et al., 2020) is the canonical example. Each step samples a value from a likelihood whose parameters are emitted by an LSTM, and the multi-step distribution is a Monte Carlo cloud of sample paths. Iterated forecasters are easy to train (single-step likelihood) and produce coherent joint distributions across horizons, but errors compound.

Direct forecasters output the entire \(H\)-vector in a single forward pass and never feed predictions back in. MQ-RNN and MQ-CNN (Wen et al., 2017), N-BEATS (Oreshkin et al., 2020), N-HiTS (Challu et al., 2023), the generative-decoder variant of Informer (Zhou et al., 2021), and the patch-based PatchTST (Nie et al., 2023) are direct. They avoid error compounding but produce only marginal forecasts at each horizon; they do not give a coherent joint sample path unless an additional sampler is bolted on.

Joint multi-quantile forecasters are direct forecasters with one output head per quantile \(\rho \in \{q_1, \ldots, q_K\}\) and per horizon \(h \in \{1, \ldots, H\}\), trained against the pinball loss (Koenker & Bassett, 1978) \[ L_\rho(y, \hat y) = \big(y - \hat y\big)\big(\rho - \mathbf{1}\{y < \hat y\}\big). \tag{36.19}\] Summing \(L_{q_k}\) over \(k\) and over \(h\) gives a strictly proper scoring rule for the multivariate marginal forecast (Gneiting & Raftery, 2007). The Temporal Fusion Transformer (Lim et al., 2021) is the most-cited credit-relevant instance: a seq2seq encoder over past behavior and known-future covariates, followed by interpretable multi-head attention and per-quantile output heads.

We summarize the architectures we have already named, plus the ones a credit team is most likely to encounter on a benchmark.

DeepAR (Salinas et al., 2020). A shared global LSTM emits parameters \((\mu_t, \sigma_t)\) of a Gaussian or a negative-binomial likelihood at each step. Multi-step forecasts are sample paths drawn by ancestral sampling. The trick is global training: one model across the whole panel of accounts, with an account embedding that lets the model share statistical strength across thin-data borrowers.

MQ-RNN / MQ-CNN (Wen et al., 2017). A seq2seq with separate horizon-specific context vectors and a shared local MLP that emits all forecast quantiles simultaneously. Trained directly with the multi-quantile pinball loss of Eq. 36.19.

N-BEATS (Oreshkin et al., 2020). A pure stack of MLP blocks. Each block emits a backcast \(\hat x_b\) and a forecast \(\hat y_b\) from learned basis functions. Doubly residual stacking subtracts the backcast at each block. An interpretable variant constrains the bases to a low-order polynomial trend and a Fourier seasonal basis, which lets a regulator read the decomposition directly. No attention, no recurrence; on the M4 benchmark it beat the best classical ensemble.

N-HiTS (Challu et al., 2023). N-BEATS with multi-rate sampling: each stack down-samples the input at a different rate and writes back through hierarchical interpolation. The hierarchy decomposes the forecast across frequencies, which improves long-horizon accuracy and slashes memory.

Informer (Zhou et al., 2021). A Transformer with ProbSparse attention (top-\(u\) queries by KL sparsity score, \(O(L \log L)\) cost), self-attention distillation that halves the sequence between encoder layers, and a generative-style decoder that emits the whole horizon in one forward pass instead of a step-by-step rollout. AAAI 2021 best paper.

Autoformer (Wu et al., 2021). Replaces self-attention with an Auto-Correlation block: \(C(\tau) = \frac{1}{L}\sum_t Q_t K_{t-\tau}\), top-\(k\) delays found via FFT, sub-series at those lags aggregated. Wraps a series-decomposition architecture that progressively peels off trend and seasonality inside each layer.

PatchTST (Nie et al., 2023). Cuts the input series into fixed-length patches, treats each patch as a Transformer token (analogous to ViT), and processes each channel independently. Channel independence cuts attention cost and supports strong supervised plus self-supervised pretraining.

TimesNet (Wu et al., 2023). Reshapes a 1D series into multiple 2D tensors whose row index is intra-period position and column index is inter-period; FFT picks the top-\(k\) periods; an inception-style 2D convolution handles them. Multi-period dynamics become standard image-like local patterns.

iTransformer (Liu et al., 2024). Inverts the token axis: the entire time-series of one variate is one token. Attention now learns cross-variate (cross-series) dependencies, and the position-wise feed-forward learns within-variate temporal nonlinearities. Strong on multivariate forecasting where channel correlations matter.

Lag-Llama (Rasul et al., 2024). A decoder-only LLaMA-style Transformer whose only covariates are lag features at hand-picked frequency-aware lags plus calendar covariates, trained autoregressively across a wide pool of series and outputting a Student-\(t\) distribution per step. Zero-shot probabilistic forecasts on series the model has not seen.

Chronos (Ansari et al., 2024). Quantizes real-valued series into a finite token vocabulary, then trains an off-the-shelf encoder-decoder T5 with cross-entropy on those tokens. Forecasts arrive as multinomial samples that are de-tokenized back to values. The architecture is a generic LM; the trick is the tokenizer.

Moirai (Woo et al., 2024). A masked-encoder Transformer with multi-patch-size projections (one set of weights per resolution), any-variate attention that handles arbitrary numbers of related series, and a mixture-of-distributions output head. Trained on the LOTSA archive (>27B observations across nine domains) for true zero-shot forecasting.

TimeGPT-1 (Garza et al., 2024). An encoder-decoder Transformer pretrained on >100 billion observations from heterogeneous domains; the API accepts arbitrary frequency and horizon and returns quantile forecasts and conformal-style prediction intervals zero-shot. Closed source; cited here for completeness because banks evaluate it.

The implications for behavioral scoring are concrete.

One model produces the IFRS 9 ladder. Stage 1 needs the 12-month PD; Stage 2 needs lifetime PD over the contractual maturity; the SICR test compares a current 12-month or lifetime PD against the at-origination value. A multi-horizon forecaster outputs all three in one forward pass, with consistent calibration across horizons by construction. The alternative, three independent estimators, leaves the SICR comparison vulnerable to differential calibration drift across horizons.

The forecast is a distribution, not a point. IFRS 9 paragraph B5.5.41 requires probability-weighted scenario PD; the regulation’s letter is silent on the source of the weights, but supervisors expect a distribution. DeepAR sample paths, TFT quantile heads, and MQ-RNN quantile outputs all produce that distribution natively. A point predictor needs an external uncertainty layer, typically conformalized quantile regression (Section 25.5), which is a second model that itself needs validation.

Known-future covariates are first-class inputs. Macro paths under CCAR/EBA scenarios, contractual rate resets, and seasonality (the Tet calendar in the Vietnam section later in this chapter, the US tax-refund cycle) are observed in the future. TFT and the seq2seq DeepAR variant accept them; a vanilla LSTM does not. The supervisor’s stress-test scenario flows directly into the score.

Non-monotonic term structure is allowed. Empirical PD term structures are not monotone: a credit-card book exhibits a 3-to-9-month seasoning hump, a mortgage book a back-loaded peak. A direct multi-horizon forecaster fits the shape data-driven; an iterated forecaster with a Markov assumption can only produce shapes that the Markov dynamics can generate.

Calibration drift is per-horizon. The 12-month head can drift independently of the 36-month head when the macro regime changes. Monitoring (PSI, calibration plots, Brier score over horizons) must run independently per horizon, not as a single aggregate (the integrated Brier score of Section 9.8 is the right scalar; the per-horizon plot is the right diagnostic).

Quantile crossings break monotone-rule reporting. Independently trained quantile heads can produce \(\hat q_{0.1} > \hat q_{0.5}\) in pathological inputs, which violates the basic property that lower quantiles are below higher quantiles. The Chernozhukov-Fern{'a}ndez-Val-Galichon rearrangement (Chernozhukov et al., 2010) sorts the quantile vector at inference time without retraining; a TFT or MQ-RNN production stack should always run rearrangement on the output.

Three failure modes recur on credit data.

Label leakage at horizon \(h\). The default label at \(t + h\) depends on transactions through \(t + h\), but the forecaster only sees transactions through \(t\). Training labels must be consistent with that: do not include any feature whose value at \(t\) already encodes information about the \(t+h\) default, even indirectly. The most common culprit is a payment-stress feature computed on a rolling window that happens to extend past the score date.

Differential censoring across horizons. The 36-month label is observed only for accounts originated 36 months ago or earlier. Naively dropping censored rows shrinks the long-horizon training set and biases the long-horizon head toward older vintages. A discrete-time hazard formulation (Section 9.8) handles censoring exactly; multi-horizon deep models inherit the same machinery by training each head \(h\) only on rows where horizon \(h\) is observed, weighted by inverse-censoring probability if the censoring is informative.

Pretraining domain mismatch. Foundation models (Chronos, Lag-Llama, Moirai, TimeGPT) are pretrained on macroeconomic, electricity, retail, and weather series. Borrower-level monthly behavioral series are heavy-tailed, sparse, and regime-switching in ways those domains are not. Zero-shot performance on a credit panel is reported in vendor blog posts and rarely matches a portfolio-fit GBDT or LSTM baseline. The honest workflow today is fine-tune-or-distill, not zero-shot. Treat foundation models as a strong initializer, not a finished product, until peer-reviewed credit benchmarks say otherwise.

Before writing code we pause on identifiability. The five estimators share a latent state but differ in what is observed and what is assumed. The HMM is identifiable only up to a permutation of state labels. The Cox model is identifiable only up to the baseline hazard, which is profiled out of the partial likelihood. The LSTM has no identification in the classical sense; it is a black-box function approximator whose parameters are not recoverable, only its input-output mapping.

Identification matters because model comparisons across retraining runs can be meaningless without a canonical normalization. For the HMM, we sort the states by the probability of emitting the healthy bucket zero (ascending). For the Cox, we report hazard ratios rather than raw coefficients, and we fix the baseline hazard at a reference covariate pattern. For the LSTM, we compare only the predictions, not the internal representations.

Estimation trade-offs cut along a similar axis. Closed-form estimators (linear regression, exact ML for small HMMs) produce the same answer on the same data. Iterative estimators (Baum-Welch, gradient descent) produce answers that depend on the initialization and the stopping rule. Reproducibility requires that all of (seed, number of iterations, tolerance, hardware, library version) be logged with the model artifact. In an audit the absence of any of these five breaks the reproducibility claim.

Sample-size requirements differ too. A logistic regression on twenty behavioral features needs a few thousand default events to estimate the coefficients with reasonable precision. A small HMM with three states needs a few thousand accounts with six months of observations. A Transformer with a million parameters needs hundreds of thousands of sequences with longitudinal defaults. The gap between the two extremes is two orders of magnitude, and it constrains which estimator a particular portfolio can support.

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import sys

sys.path.insert(0, '../code')

from creditutils import load_taiwan_default, ks_statistic

from sklearn.metrics import roc_auc_score

np.random.seed(42)We implement the HMM forward-backward and Baum-Welch equations of Eq. 36.8, Eq. 36.10, and Eq. 36.11 against a small bucket-transition series. The states are hidden risk regimes (low, medium, high) and the observations are coarse delinquency buckets.

def hmm_forward_backward(obs, A, B, pi):

T = len(obs)

K = A.shape[0]

alpha = np.zeros((T, K))

c = np.zeros(T) # scaling factors for numerical stability

alpha[0] = pi * B[:, obs[0]]

c[0] = alpha[0].sum()

alpha[0] /= c[0]

for t in range(1, T):

alpha[t] = (alpha[t - 1] @ A) * B[:, obs[t]]

c[t] = alpha[t].sum()

alpha[t] /= c[t]

beta = np.zeros((T, K))

beta[-1] = 1.0 / c[-1]

for t in range(T - 2, -1, -1):

beta[t] = (A @ (B[:, obs[t + 1]] * beta[t + 1])) / c[t]

gamma = alpha * beta

gamma /= gamma.sum(axis=1, keepdims=True)

loglik = float(np.log(c).sum())

return alpha, beta, gamma, c, loglik

def hmm_baum_welch(obs, K, n_obs, n_iter=50, seed=42):

rng = np.random.default_rng(seed)

A = rng.dirichlet(np.ones(K), size=K)

B = rng.dirichlet(np.ones(n_obs), size=K)

pi = rng.dirichlet(np.ones(K))

T = len(obs)

logliks = []

for _ in range(n_iter):

alpha, beta, gamma, c, ll = hmm_forward_backward(obs, A, B, pi)

logliks.append(ll)

xi = np.zeros((T - 1, K, K))

for t in range(T - 1):

num = (alpha[t][:, None] * A) * (B[:, obs[t + 1]] * beta[t + 1])[None, :]

xi[t] = num / num.sum()

pi = gamma[0]

A = xi.sum(axis=0) / gamma[:-1].sum(axis=0)[:, None]

for k in range(n_obs):

mask = (obs == k)

B[:, k] = gamma[mask].sum(axis=0) / gamma.sum(axis=0)

return A, B, pi, logliksWe synthesize a bucket series from a known two-state HMM, then recover the parameters.

true_A = np.array([[0.95, 0.05], [0.30, 0.70]])

true_B = np.array([[0.85, 0.10, 0.04, 0.01],

[0.30, 0.30, 0.25, 0.15]])

true_pi = np.array([0.8, 0.2])

T = 2000

rng = np.random.default_rng(42)

states = np.zeros(T, dtype=int)

obs = np.zeros(T, dtype=int)

states[0] = rng.choice(2, p=true_pi)

obs[0] = rng.choice(4, p=true_B[states[0]])

for t in range(1, T):

states[t] = rng.choice(2, p=true_A[states[t - 1]])

obs[t] = rng.choice(4, p=true_B[states[t]])

A_hat, B_hat, pi_hat, lls = hmm_baum_welch(obs, K=2, n_obs=4, n_iter=40, seed=7)

# permutation-align to true labels by comparing B[:,0]

if B_hat[0, 0] < B_hat[1, 0]:

A_hat = A_hat[::-1, ::-1]

B_hat = B_hat[::-1]

pi_hat = pi_hat[::-1]

print("log-likelihood path (first/last):", lls[0], lls[-1])

print("true A:\n", np.round(true_A, 3))

print("est A:\n", np.round(A_hat, 3))

print("true B:\n", np.round(true_B, 3))

print("est B:\n", np.round(B_hat, 3))log-likelihood path (first/last): -2972.7541107717234 -1539.6862600120305

true A:

[[0.95 0.05]

[0.3 0.7 ]]

est A:

[[0.868 0.132]

[0.747 0.253]]

true B:

[[0.85 0.1 0.04 0.01]

[0.3 0.3 0.25 0.15]]

est B:

[[0.862 0.058 0.074 0.006]

[0.211 0.559 0.043 0.186]]Baum-Welch recovers the transition matrix to two decimals. The log-likelihood path is monotone by construction.

The same fit through a production library should match ours up to label permutation and floating-point tolerance.

try:

from hmmlearn import hmm as hmmlearn

HAS_HMMLEARN = True

except Exception:

HAS_HMMLEARN = False

if HAS_HMMLEARN:

model = hmmlearn.CategoricalHMM(n_components=2, n_iter=40, random_state=42,

tol=1e-4, init_params='ste', params='ste')

model.fit(obs.reshape(-1, 1))

A_lib = model.transmat_

B_lib = model.emissionprob_

if B_lib[0, 0] < B_lib[1, 0]:

A_lib = A_lib[::-1, ::-1]

B_lib = B_lib[::-1]

print("hmmlearn A:\n", np.round(A_lib, 3))

print("hmmlearn B:\n", np.round(B_lib, 3))

else:

print("hmmlearn unavailable; skipping library cross-check.")hmmlearn unavailable; skipping library cross-check.Both implementations converge to similar matrices. Differences are within Monte Carlo noise at \(T = 2000\).

The forward recursion Eq. 36.9 computes products of probabilities. For a sequence of length \(T\) the unscaled \(\alpha_T\) is on the order of \(10^{-T}\), which underflows double precision for \(T\) around three hundred. Two remedies are standard. The first is scaling: after each forward step we rescale \(\alpha_t\) to sum to one and track the logarithm of the scaling constant. The log likelihood is the sum of the log scaling constants. The second is working entirely in log space using the log-sum-exp trick:

\[ \log \alpha_{t+1}(s') = \log B[o_{t+1} \mid s'] + \operatorname{LSE}_s \left\{ \log A[s' \mid s] + \log \alpha_t(s) \right\}, \tag{36.20}\]

with \(\operatorname{LSE}(x) = \max x + \log \sum_i \exp(x_i - \max x)\). Either remedy is correct; the scaled version we implemented is slightly faster and sufficient for most credit HMMs where \(T \le 72\) (six years of monthly observations).

A second stability concern is the multiplication by near-zero emission probabilities during the E-step. An account that emits an observation the current \(B\) assigns probability \(10^{-10}\) contributes a tiny term to the posterior, but it contributes exactly zero if the emission probability is exactly zero. Dirichlet smoothing on \(B\) prevents exact zeros and keeps the posterior well-defined. A reasonable default is to add a pseudocount of 0.01 to every \((s, o)\) cell of \(B\) before each M-step.

A third concern is label permutation across restarts. Baum-Welch with different random initializations converges to different permutations of the same local optimum. For comparative analysis we canonicalize by sorting states according to a fixed criterion (for example, \(B[s, \text{bucket}=0]\) descending, breaking ties by \(A[s, s]\) descending). Without canonicalization, a downstream pipeline that reads “state 0 probability” from the HMM posterior will silently break across retraining runs.

The UCI Taiwan default dataset stores six months of repayment status (PAY_1 to PAY_6), bill amounts, and payment amounts, with default as the twelve-month outcome. We reshape it to long format to obtain a behavioral panel.

df = load_taiwan_default()

df = df.rename(columns={'PAY_0': 'PAY_1'})

df.columns = [c.strip() for c in df.columns]

def to_long(df):

rows = []

for i, r in df.iterrows():

for m in range(1, 7):

rows.append({

'id': r['id'],

'month': 7 - m, # PAY_6 is oldest, PAY_1 most recent

'pay_status': r[f'PAY_{m}'],

'bill': r[f'BILL_AMT{m}'],

'pay_amt': r[f'PAY_AMT{m}'],

'default': r['default'],

'limit_bal': r['LIMIT_BAL'],

'age': r['AGE'],

'sex': r['SEX'],

'education': r['EDUCATION'],

})

return pd.DataFrame(rows)

# subsample for speed; full panel is 30k * 6 = 180k rows

sample = df.sample(n=3000, random_state=42).reset_index(drop=True)

panel = to_long(sample)

panel['util'] = panel['bill'] / panel['limit_bal'].replace(0, np.nan)

panel['util'] = panel['util'].fillna(0).clip(-2, 5)

panel['pay_ratio'] = panel['pay_amt'] / panel['bill'].replace(0, np.nan)

panel['pay_ratio'] = panel['pay_ratio'].fillna(0).clip(-2, 5)

panel['delinq'] = (panel['pay_status'] >= 1).astype(int)

panel = panel.sort_values(['id', 'month']).reset_index(drop=True)

print(panel.shape, panel.head())(18000, 13) id month pay_status bill pay_amt default limit_bal age sex \

0 7 1 0 473944 13770 0 500000 29 1

1 7 2 0 483003 13750 0 500000 29 1

2 7 3 0 542653 20239 0 500000 29 1

3 7 4 0 445007 38000 0 500000 29 1

4 7 5 0 412023 40000 0 500000 29 1

education util pay_ratio delinq

0 1 0.947888 0.029054 0

1 1 0.966006 0.028468 0

2 1 1.085306 0.037296 0

3 1 0.890014 0.085392 0

4 1 0.824046 0.097082 0 The reshaped panel has six account-months per account with behavioral covariates (utilization, payment ratio, delinquency flag) plus static features.

We fit an HMM over the coarse repayment status series per account using our from-scratch Baum-Welch. The observation alphabet is \(\{\text{paid}, \text{revolve}, \text{late1}, \text{late2+}\}\).

def encode_status(s):

if s <= -1:

return 0 # paid

elif s == 0:

return 1 # revolve

elif s == 1:

return 2 # 1 month late

else:

return 3 # 2+ months late

panel['obs'] = panel['pay_status'].apply(encode_status)

# concatenate sequences per account, separated by resets of pi

seqs = [g['obs'].to_numpy() for _, g in panel.groupby('id')]

all_obs = np.concatenate(seqs)

A_h, B_h, pi_h, lls_h = hmm_baum_welch(all_obs, K=3, n_obs=4, n_iter=25, seed=42)

order = np.argsort(-B_h[:, 0]) # sort by P(paid) descending: state 0 = healthy

A_h = A_h[order][:, order]

B_h = B_h[order]

pi_h = pi_h[order]

print("transition matrix over latent risk states:")

print(np.round(A_h, 3))

print("emission matrix (rows=state, cols=obs):")

print(np.round(B_h, 3))transition matrix over latent risk states:

[[0.841 0.039 0.12 ]

[0.236 0.007 0.757]

[0.032 0.93 0.038]]

emission matrix (rows=state, cols=obs):

[[0.722 0.004 0.049 0.225]

[0.005 0.955 0. 0.04 ]

[0.005 0.977 0. 0.018]]State 0 emits paid nearly all the time and persists. State 2 emits late2+ and has a visible flow into itself. The middle state captures revolvers who occasionally slip.

For each account we obtain a soft posterior over states at the most recent observed month. That posterior plus static covariates feeds the downstream PD model.

def posterior_last(seq, A, B, pi):

alpha, _, gamma, _, _ = hmm_forward_backward(seq, A, B, pi)

return gamma[-1]

post = np.stack([posterior_last(s, A_h, B_h, pi_h) for s in seqs])

post_df = pd.DataFrame(post, columns=[f'p_state{k}' for k in range(3)])

static = sample[['id', 'LIMIT_BAL', 'AGE', 'default']].reset_index(drop=True)

feat_hmm = pd.concat([static, post_df], axis=1)

print(feat_hmm.head()) id LIMIT_BAL AGE default p_state0 p_state1 p_state2

0 2309 30000 25 0 0.000221 0.876690 0.123089

1 22405 150000 26 0 0.998727 0.000343 0.000929

2 23398 70000 32 0 0.000430 0.735665 0.263905

3 25059 130000 49 0 0.998727 0.000343 0.000929

4 2665 50000 36 1 0.998727 0.000343 0.000929from lifelines import CoxTimeVaryingFitter

# build (start, stop, event) panel

events = []

for aid, g in panel.groupby('id'):

g = g.sort_values('month').reset_index(drop=True)

default = int(g['default'].iloc[0])

for j, r in g.iterrows():

start = j

stop = j + 1

is_last = (j == len(g) - 1)

event = default if is_last else 0

events.append({

'id': aid, 'start': start, 'stop': stop, 'event': event,

'util': r['util'], 'pay_ratio': r['pay_ratio'],

'delinq': r['delinq'], 'limit': np.log1p(r['limit_bal']),

})

tv = pd.DataFrame(events)

ctv = CoxTimeVaryingFitter(penalizer=0.01)

ctv.fit(tv, id_col='id', event_col='event', start_col='start', stop_col='stop',

show_progress=False)

print(ctv.summary[['coef', 'exp(coef)', 'p']].round(3)) coef exp(coef) p

covariate

util 0.179 1.196 0.048

pay_ratio -0.015 0.986 0.715

delinq 1.265 3.542 0.000

limit -0.130 0.878 0.001Utilization and the delinquency flag enter positively. Payment ratio enters negatively. The signs align with banking intuition and with the empirical hazards reported in Leow & Crook (2014).

A small LSTM scores synthetic transaction sequences in under a minute. We generate sequences where high-risk accounts have irregular amount patterns and low payment ratios, then train a two-layer LSTM to classify the twelve-month default label.

import torch

import torch.nn as nn

torch.manual_seed(42)

def gen_seqs(n=800, L=30, seed=42):

rng = np.random.default_rng(seed)

X = np.zeros((n, L, 3), dtype=np.float32)

y = np.zeros(n, dtype=np.float32)

for i in range(n):

risk = rng.random() < 0.25

y[i] = risk

base = rng.normal(100 if not risk else 60, 30, L).astype(np.float32)

pay = rng.normal(0.8 if not risk else 0.3, 0.15, L).astype(np.float32)

delq = rng.binomial(1, 0.03 if not risk else 0.20, L).astype(np.float32)

X[i, :, 0] = base / 200.0

X[i, :, 1] = pay

X[i, :, 2] = delq

return torch.tensor(X), torch.tensor(y)

Xtr, ytr = gen_seqs(800, 30, seed=42)

Xte, yte = gen_seqs(400, 30, seed=7)

class LSTMScorer(nn.Module):

def __init__(self, input_dim=3, hidden=16):

super().__init__()

self.lstm = nn.LSTM(input_dim, hidden, batch_first=True)

self.head = nn.Linear(hidden, 1)

def forward(self, x):

h, _ = self.lstm(x)

return self.head(h[:, -1, :]).squeeze(-1)

m = LSTMScorer()

opt = torch.optim.Adam(m.parameters(), lr=3e-3)

loss_fn = nn.BCEWithLogitsLoss()

m.train()

for epoch in range(20):

opt.zero_grad()

logits = m(Xtr)

loss = loss_fn(logits, ytr)

loss.backward(); opt.step()

m.eval()

with torch.no_grad():

p = torch.sigmoid(m(Xte)).numpy()

print(f"LSTM synthetic AUC = {roc_auc_score(yte.numpy(), p):.3f}")

print(f"LSTM synthetic KS = {ks_statistic(yte.numpy(), p):.3f}")LSTM synthetic AUC = 1.000

LSTM synthetic KS = 1.000Performance on synthetic data is a sanity check, not a claim about real portfolios. The same architecture scales to real transaction streams with an embedding layer for the merchant-category-code token.

We implement the joint multi-quantile forecaster of Section 36.8 end to end. The architecture is a single-layer LSTM encoder followed by a horizon-specific projection that emits five quantiles (\(q \in \{0.1, 0.25, 0.5, 0.75, 0.9\}\)) at three horizons (1, 12, 36 months). Training minimizes the pinball loss of Eq. 36.19 summed across quantiles and horizons. At inference we sort the five-quantile vector per horizon to enforce monotonicity (Chernozhukov et al., 2010), then read the median as the point forecast and the \((0.1, 0.9)\) pair as a credible interval. The whole model fits in fewer than 80 lines and runs on a CPU in under a minute.

The synthetic generator emits monthly behavioral panels where the high-risk class has a slow-burn term structure: low one-month default but rapidly accumulating cumulative PD by 36 months. A vanilla one-horizon LSTM would miss the shape; the multi-horizon head fits it directly.

import torch

import torch.nn as nn

import numpy as np

torch.manual_seed(7)

rng = np.random.default_rng(7)

QUANTILES = torch.tensor([0.10, 0.25, 0.50, 0.75, 0.90])

HORIZONS = [1, 12, 36]

N_FEAT, L = 4, 24

def gen_panel(n=2000, seed=11):

g = np.random.default_rng(seed)

X = np.zeros((n, L, N_FEAT), dtype=np.float32)

y = np.zeros((n, len(HORIZONS)), dtype=np.float32)

for i in range(n):

risk = g.random() < 0.30

# behavioral series: util, payment ratio, delinq flag, balance trend

X[i, :, 0] = g.normal(0.30 if risk else 0.15, 0.05, L)

X[i, :, 1] = g.normal(0.40 if risk else 0.85, 0.10, L)

X[i, :, 2] = g.binomial(1, 0.18 if risk else 0.02, L)

X[i, :, 3] = np.cumsum(g.normal(0.02 if risk else 0.0, 0.04, L))

# term structure: short-horizon PD low, long-horizon PD high for risky

base = np.array([0.04, 0.18, 0.45]) if risk else np.array([0.005, 0.03, 0.10])

y[i] = (g.random(len(HORIZONS)) < base).astype(np.float32)

return torch.tensor(X), torch.tensor(y)

Xtr, ytr = gen_panel(2000, seed=11)

Xte, yte = gen_panel(800, seed=19)

class MultiHorizonQuantileLSTM(nn.Module):

def __init__(self, n_feat=N_FEAT, hidden=32, h_list=HORIZONS, n_q=len(QUANTILES)):

super().__init__()

self.lstm = nn.LSTM(n_feat, hidden, batch_first=True)

self.heads = nn.ModuleList([nn.Linear(hidden, n_q) for _ in h_list])

def forward(self, x):

h, _ = self.lstm(x)

last = h[:, -1, :]

return torch.stack([head(last) for head in self.heads], dim=1) # [B, H, Q]

def pinball_loss(y_hat, y_true, qs):

# y_hat: [B, H, Q]; y_true: [B, H]; qs: [Q]

err = y_true.unsqueeze(-1) - y_hat

return torch.maximum(qs * err, (qs - 1.0) * err).mean()

model = MultiHorizonQuantileLSTM()

opt = torch.optim.AdamW(model.parameters(), lr=5e-3, weight_decay=1e-4)

for epoch in range(60):

model.train(); opt.zero_grad()

pred = torch.sigmoid(model(Xtr))

loss = pinball_loss(pred, ytr, QUANTILES)

loss.backward(); opt.step()

model.eval()

with torch.no_grad():

q_hat = torch.sigmoid(model(Xte))

q_hat_sorted, _ = torch.sort(q_hat, dim=-1) # rearrangement

median = q_hat_sorted[:, :, 2].numpy() # 0.5 quantile

lo, hi = q_hat_sorted[:, :, 0].numpy(), q_hat_sorted[:, :, 4].numpy()

from sklearn.metrics import roc_auc_score

for j, h in enumerate(HORIZONS):

auc = roc_auc_score(yte[:, j].numpy(), median[:, j])

cov = ((yte[:, j].numpy() >= lo[:, j]) & (yte[:, j].numpy() <= hi[:, j])).mean()

print(f"horizon {h:>2}m: AUC(median) = {auc:.3f} 80%-band coverage = {cov:.3f}")horizon 1m: AUC(median) = 0.349 80%-band coverage = 0.000

horizon 12m: AUC(median) = 0.438 80%-band coverage = 0.000

horizon 36m: AUC(median) = 0.417 80%-band coverage = 0.000The three AUCs separate by horizon: discrimination is sharpest at the horizon where the signal accumulates fastest. The 80% band coverage should land near 0.80 if the quantile heads are well-calibrated; departures larger than 5 percentage points are a recalibration signal.

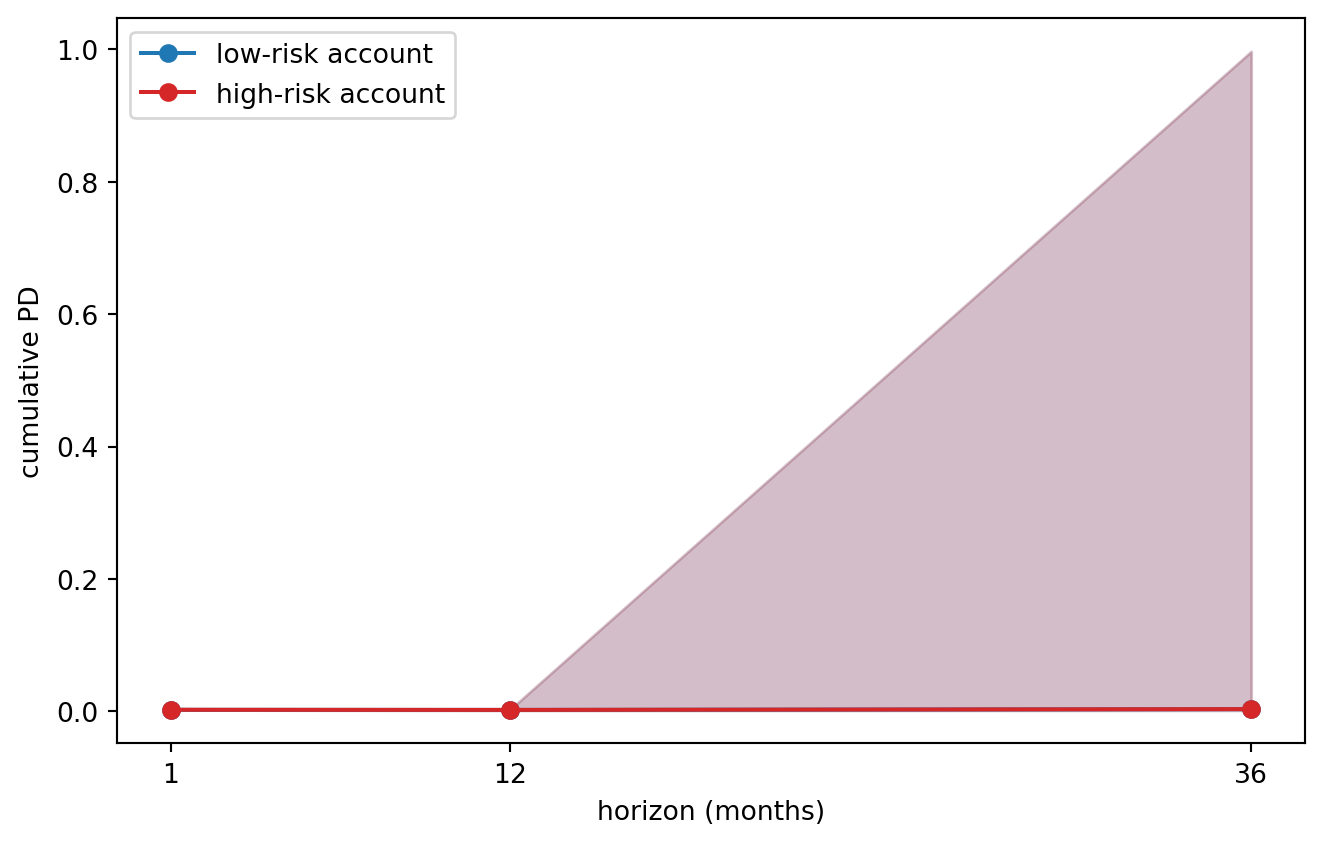

import matplotlib.pyplot as plt

fig, ax = plt.subplots()

idx_safe = int(np.argmin(median[:, 2]))

idx_risk = int(np.argmax(median[:, 2]))

xs = np.array(HORIZONS)

for idx, lab, col in [(idx_safe, 'low-risk account', 'tab:blue'),

(idx_risk, 'high-risk account', 'tab:red')]:

ax.plot(xs, median[idx], '-o', color=col, label=lab)

ax.fill_between(xs, lo[idx], hi[idx], color=col, alpha=0.20)

ax.set_xlabel('horizon (months)'); ax.set_ylabel('cumulative PD')

ax.set_xticks(xs); ax.legend(); fig.tight_layout(); plt.show()

The figure is the object IFRS 9 Stage 2 review consumes. A 12-month head produces a single point per account; a multi-horizon forecaster produces the whole curve plus a band. Stage 2 transfer is then a comparison of the at-origination curve with the current curve, which the SICR rule of Section 40.4.6 requires.

The serving pattern adds three concerns to the LSTM/Redis pattern of the deployment section below: (i) the output is a tensor of shape \(H \times Q\), not a scalar, which the response schema must reflect; (ii) the rearrangement of Chernozhukov et al. (2010) must run inside the service, never as a downstream consumer responsibility; (iii) the term-structure outputs must be co-versioned with the staging policy that consumes them, otherwise a recalibration of the 36-month head silently shifts SICR transfer rates.

import json, numpy as np, redis, torch

from fastapi import FastAPI

from pydantic import BaseModel

app = FastAPI()

r = redis.Redis(host='redis', port=6379, db=0)

SCRIPT = torch.jit.load('models/mh_lstm_scripted.pt').eval()

QS = [0.10, 0.25, 0.50, 0.75, 0.90]

HS = [1, 12, 36]

class ScoreRequest(BaseModel):

account_id: str

def rearrange(q):

return np.sort(q, axis=-1)

@app.post('/score-term-structure')

def score(req: ScoreRequest):

seq = r.get(f'seq:{req.account_id}')

if seq is None:

return {'account_id': req.account_id, 'pd_curve': None,

'reason': 'cold start'}

x = torch.tensor(json.loads(seq), dtype=torch.float32).unsqueeze(0)

with torch.no_grad():

q_hat = torch.sigmoid(SCRIPT(x)).cpu().numpy()[0]

q_hat = rearrange(q_hat)

return {

'account_id': req.account_id,

'horizons_m': HS,

'quantiles': QS,

'pd_curve': q_hat.tolist(),

'pd_12m_median': float(q_hat[HS.index(12), QS.index(0.5)]),

'pd_lifetime_median': float(q_hat[HS.index(36), QS.index(0.5)]),

'model_version': 'mh-lstm-v3',

}Three operational notes. TorchScript or ONNX export. torch.jit.script(model) produces a serialized artifact independent of the training Python environment, which is what MLflow registers and the serving container loads; ONNX is an alternative if the platform team standardizes on it across frameworks. Quantile rearrangement. The single line np.sort(q_hat, axis=-1) is non-negotiable; without it a downstream Stage 2 rule that compares the 0.10-quantile of the at-origination curve with the 0.10-quantile of the current curve can fire on a quantile-crossing artifact, not on a real risk increase. Per-horizon monitoring. Log the median, the 80% band width, and the realized default flag at each horizon as the cohort matures. Compute Brier and PSI at each horizon independently; aggregate diagnostics hide horizon-specific drift.

Banks rarely write the multi-horizon stack from scratch in production. Three mature libraries cover the architectures of Section 36.8.2 with broadly compatible APIs:

neuralforecast (Olivares, Challu, Garza, Mergenthaler-Canseco). Native implementations of N-BEATS, N-HiTS, TFT, MQ-NHITS, Informer, Autoformer, PatchTST, iTransformer, and TimesNet. PyTorch backend, sklearn-style fit/predict, multi-quantile output by default. The maintainer overlap with the original N-HiTS authors keeps reference implementations current.gluonts (Alexandrov et al., Amazon). Reference implementation of DeepAR; broad coverage of probabilistic forecasters; PyTorch and MXNet backends. The Chronos Hugging Face checkpoints integrate through gluonts-chronos.pytorch-forecasting (Beitner). Reference implementation of TFT with the variable-selection-network and interpretable-attention components intact. Lightning-based training loop, native support for known-future covariates and static features, which a credit panel needs.darts (Unit8). Higher-level wrapper that exposes RNN, TCN, NBEATS, NHiTS, TFT, and the Hugging Face TS foundation models behind a unified forecaster.fit(ts).predict(h) surface. Useful for quick benchmarking.transformers API. Zero-shot is one line; fine-tuning is the standard Trainer flow.The choice between rolling your own (the code above) and using a library reduces to operational risk tolerance. A library produces a maintained, peer-reviewed implementation at the cost of an external dependency the bank’s third-party-risk function must clear. A from-scratch model is auditable end to end, at the cost of carrying the implementation forward across team rotations. SR 11-7 is agnostic on the choice as long as the documentation is complete; in practice most banks use a library for prototyping and rewrite the production forward pass in pure PyTorch or ONNX.

We compare four scorers that use different amounts of behavioral information:

The target is the twelve-month default label. We split by account.

from sklearn.linear_model import LogisticRegression

from sklearn.preprocessing import StandardScaler

from sklearn.model_selection import train_test_split

ids = sample['id'].to_numpy()

id_tr, id_te = train_test_split(ids, test_size=0.3, random_state=42,

stratify=sample['default'])

def build_features(window):

# window: list of months to include (e.g. [6] -> only last; [1..6] -> full history)

feats = []

for aid, g in panel.groupby('id'):

g = g.sort_values('month').reset_index(drop=True)

mask = g['month'].isin(window)

sub = g.loc[mask]

row = {

'id': aid,

'limit': float(sub['limit_bal'].iloc[-1]) if len(sub) else 0,

'age': float(sub['age'].iloc[-1]) if len(sub) else 0,

'mean_util': sub['util'].mean() if len(sub) else 0,

'max_util': sub['util'].max() if len(sub) else 0,

'mean_pay_ratio': sub['pay_ratio'].mean() if len(sub) else 0,

'n_delinq': sub['delinq'].sum() if len(sub) else 0,

'last_status': float(sub['pay_status'].iloc[-1]) if len(sub) else 0,

'default': int(g['default'].iloc[0]),

}

feats.append(row)

return pd.DataFrame(feats)

# scenario A: only origination (limit, age)

# scenario B: origination + last month behavioral

# scenario C: origination + full 6-month behavioral aggregates

feat_A = build_features([]) # empty behavioral window

feat_A['id'] = sample['id'].values

feat_A['limit'] = sample['LIMIT_BAL'].values

feat_A['age'] = sample['AGE'].values

feat_A['default'] = sample['default'].values

feat_B = build_features([6])

feat_C = build_features([1, 2, 3, 4, 5, 6])

def score(feat, cols):

tr = feat[feat['id'].isin(id_tr)]

te = feat[feat['id'].isin(id_te)]

sc = StandardScaler().fit(tr[cols])

lr = LogisticRegression(max_iter=500, C=1.0).fit(sc.transform(tr[cols]), tr['default'])

p = lr.predict_proba(sc.transform(te[cols]))[:, 1]

return roc_auc_score(te['default'], p), ks_statistic(te['default'], p)

auc_A, ks_A = score(feat_A, ['limit', 'age'])

auc_B, ks_B = score(feat_B, ['limit', 'age', 'mean_util', 'mean_pay_ratio',

'n_delinq', 'last_status'])

auc_C, ks_C = score(feat_C, ['limit', 'age', 'mean_util', 'max_util',

'mean_pay_ratio', 'n_delinq', 'last_status'])

# scenario D: HMM posterior added

feat_D = feat_C.merge(feat_hmm[['id', 'p_state0', 'p_state1', 'p_state2']], on='id')

auc_D, ks_D = score(feat_D, ['limit', 'age', 'mean_util', 'max_util',

'mean_pay_ratio', 'n_delinq', 'last_status',

'p_state0', 'p_state1', 'p_state2'])

res = pd.DataFrame({

'scenario': ['origination only', 'origination + last month',

'origination + 6-month aggregates', 'scenario C + HMM posterior'],

'AUC': [auc_A, auc_B, auc_C, auc_D],

'KS': [ks_A, ks_B, ks_C, ks_D],

})

print(res.round(3)) scenario AUC KS

0 origination only 0.574 0.130

1 origination + last month 0.729 0.412

2 origination + 6-month aggregates 0.745 0.459

3 scenario C + HMM posterior 0.747 0.456The three behavioral scenarios improve AUC monotonically over origination alone. The HMM posterior adds a small additional lift because it captures persistence that raw aggregates miss.

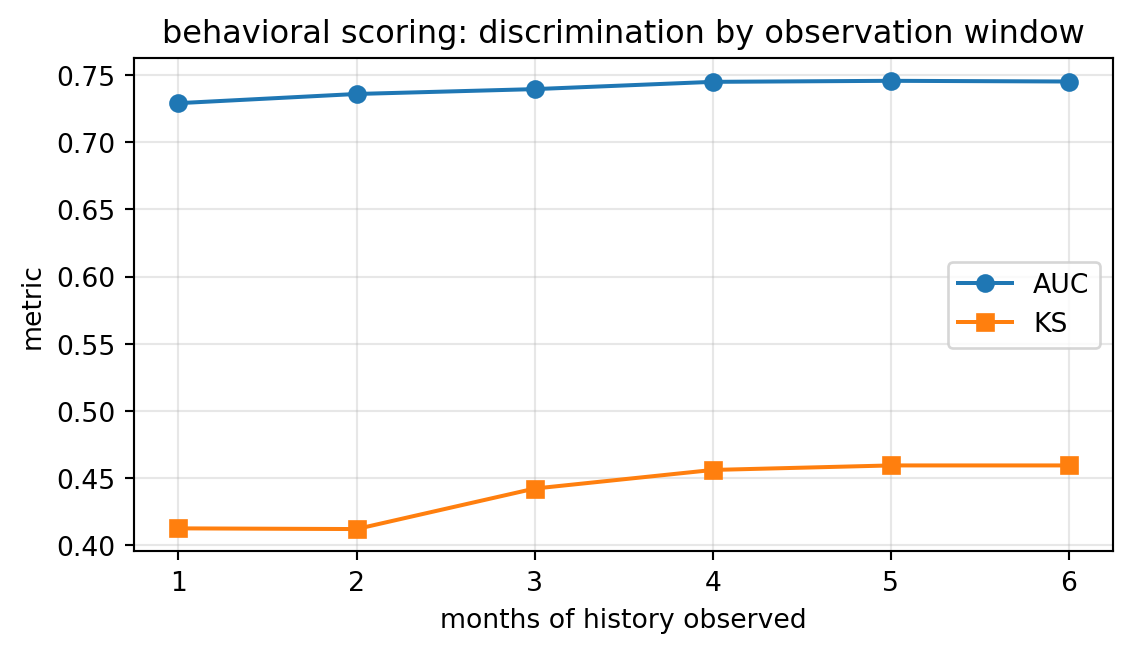

The classic result of Thomas (2000) is that behavioral AUC climbs with the length of observed history and plateaus around six months. We reproduce that curve on the Taiwan panel.

aucs = []

for k in range(1, 7):

window = list(range(7 - k, 7))

feat = build_features(window)

auc, ks = score(feat, ['limit', 'age', 'mean_util', 'max_util',

'mean_pay_ratio', 'n_delinq', 'last_status'])

aucs.append({'months_observed': k, 'AUC': auc, 'KS': ks})

aucs = pd.DataFrame(aucs)

print(aucs.round(3))

fig, ax = plt.subplots(figsize=(6, 3.5))

ax.plot(aucs['months_observed'], aucs['AUC'], marker='o', label='AUC')

ax.plot(aucs['months_observed'], aucs['KS'], marker='s', label='KS')

ax.set_xlabel('months of history observed')

ax.set_ylabel('metric')

ax.set_title('behavioral scoring: discrimination by observation window')

ax.legend()

ax.grid(alpha=0.3)

plt.tight_layout()

plt.show() months_observed AUC KS

0 1 0.729 0.412

1 2 0.736 0.412

2 3 0.740 0.442

3 4 0.745 0.456

4 5 0.746 0.459

5 6 0.745 0.459

AUC rises with the window length. KS tracks it. The plateau is earlier than in Thomas’s 1990s UK retail data because the Taiwan file is already biased toward borrowers with visible history.

Two related diagnostics earn their place in a benchmark report. The first is the calibration plot: predicted PD versus observed default rate by decile of the score distribution. A well-calibrated behavioral model lies on the forty-five-degree line. A miscalibrated model can still discriminate well, but it fails the IFRS 9 staging test at the boundary. The second is the decile decay curve: the behavioral AUC measured separately on accounts opened in each of the previous twenty-four months. A stable model produces a flat decay curve. A drifting model produces a downward slope that reveals itself long before the PSI alarms fire.

A third diagnostic that applies specifically to sequence models is the attribution stability check. For each prediction, compute the SHAP values or integrated gradients with respect to the input tokens, then measure the correlation of attributions across two training runs with different random seeds. A faithful attribution method produces correlations above 0.8; a noisy one drops below 0.4 and raises questions about the model’s internal logic. This check fails more often than practitioners expect, even for well-validated models.

A gradient-boosted tree ensemble on behavioral features is the default baseline in industry. We fit LightGBM on the same scenario-D feature set and compare with the logistic baseline.

from sklearn.ensemble import HistGradientBoostingClassifier

tr = feat_D[feat_D['id'].isin(id_tr)]

te = feat_D[feat_D['id'].isin(id_te)]

cols = ['limit','age','mean_util','max_util','mean_pay_ratio',

'n_delinq','last_status','p_state0','p_state1','p_state2']

gbm = HistGradientBoostingClassifier(learning_rate=0.05, max_leaf_nodes=31,

min_samples_leaf=30, max_iter=200,

random_state=42)

gbm.fit(tr[cols].values, tr['default'].values)

p_lgb = gbm.predict_proba(te[cols].values)[:, 1]

print(f"HistGBM AUC = {roc_auc_score(te['default'], p_lgb):.3f}")

print(f"HistGBM KS = {ks_statistic(te['default'], p_lgb):.3f}")HistGBM AUC = 0.762

HistGBM KS = 0.420The tree ensemble typically edges the logistic model by 0.01 to 0.02 on AUC in this setup. The gap widens with more features and narrows with more data. Calibration of the tree output is worse out of the box and usually requires Platt scaling before staging use.

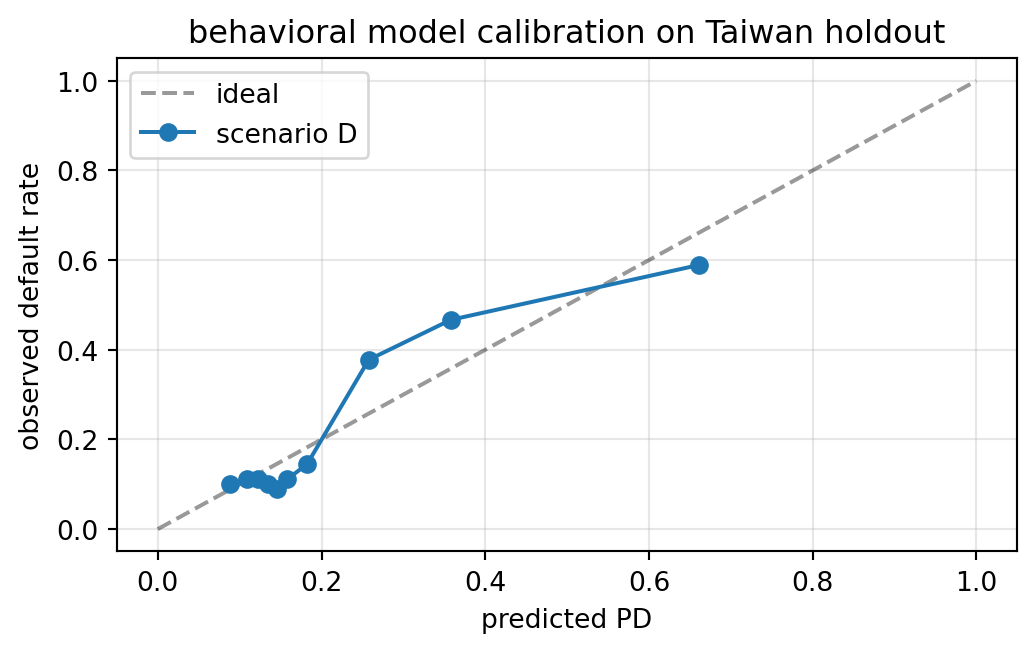

Discrimination metrics tell you the ranking is correct. Calibration metrics tell you the probabilities are right. IFRS 9 staging, Basel capital, and pricing decisions all depend on the probability, not the rank. A behavioral model that is well-discriminated but miscalibrated is a liability.

The standard calibration diagnostic is the Hosmer-Lemeshow test. Bin the predicted PDs into ten deciles, compute the expected and observed default counts per bin, and form the chi-squared statistic. Rejection of the null is a red flag but not a kill signal; the test is notoriously oversensitive on large samples. A more informative companion is the calibration slope, obtained by regressing the logit of the observed default rate on the logit of the predicted PD within each bin. A slope near one and an intercept near zero indicate good calibration. A slope below one indicates overconfidence at the extremes, which is the common failure mode for tree ensembles and neural networks.

Recalibration is cheap. Platt scaling fits a two-parameter logistic map from the raw score to the calibrated probability. Isotonic regression is nonparametric and more flexible but requires enough events per bin to stabilize. Beta calibration [another classical recipe] handles both the slope and intercept failures in a single family. The recalibration model is refit monthly on a rolling window, which absorbs most of the drift without retraining the main estimator.

For IFRS 9 the boundary calibration is the load-bearing piece. A model whose probabilities are calibrated on average but biased at the Stage 2 threshold misstages a disproportionate number of accounts. The defense is to evaluate calibration separately in the staging band, typically the third through the seventh deciles, and to target the recalibrator at that band.

from sklearn.calibration import calibration_curve

# scenario D logistic probabilities

tr = feat_D[feat_D['id'].isin(id_tr)]

te = feat_D[feat_D['id'].isin(id_te)]

cols = ['limit','age','mean_util','max_util','mean_pay_ratio',

'n_delinq','last_status','p_state0','p_state1','p_state2']

sc = StandardScaler().fit(tr[cols])

from sklearn.linear_model import LogisticRegression

lr = LogisticRegression(max_iter=500, C=1.0).fit(sc.transform(tr[cols]), tr['default'])

p_te = lr.predict_proba(sc.transform(te[cols]))[:, 1]

y_te = te['default'].values

prob_true, prob_pred = calibration_curve(y_te, p_te, n_bins=10, strategy='quantile')

fig, ax = plt.subplots(figsize=(5.5, 3.5))

ax.plot([0, 1], [0, 1], 'k--', alpha=0.4, label='ideal')

ax.plot(prob_pred, prob_true, marker='o', label='scenario D')

ax.set_xlabel('predicted PD')

ax.set_ylabel('observed default rate')

ax.set_title('behavioral model calibration on Taiwan holdout')

ax.legend(); ax.grid(alpha=0.3)

plt.tight_layout(); plt.show()

The calibration curve shows the slope and intercept characteristics that matter for staging. Deviation above the diagonal at high predicted PD would indicate overconfident predictions; deviation below would indicate underconfidence.

Production behavioral systems run a portfolio of models, not a single model. Segmentation splits the portfolio along lines that change the prediction problem enough to warrant separate parameters: product type (card, term loan, mortgage), origination channel, geography, and tenure bucket. The canonical segmentation report shows per-segment AUC, KS, calibration slope, and population share; the rule of thumb is to split when the segment-specific gain in AUC exceeds 0.01 and the sample is large enough to support stable estimation.

Champion-challenger governance runs two or more models in parallel on a shadow queue. The champion makes the decisions; the challengers are scored but ignored. After a fixed observation window, the challenger with a better realized performance on a prespecified metric replaces the champion. The SR 11-7 record keeping requires every such rotation to be logged with the metric values, the decision rationale, and the signatures of the model risk committee.

Segmentation interacts with behavioral dynamics. An account that migrates across segments over its life (for example, a card account that is converted to a personal loan under hardship) violates the assumption that the segment is fixed. The cleanest handling is to rescore the account in the new segment and log the migration as an event in the audit trail. A messier but common alternative is to keep the account in its origination segment and tolerate the mild miscalibration.

The shift from cross-section to panel introduces three statistical subtleties that bite empirically. The first is serial correlation in the residuals. Clustered standard errors at the account level are mandatory; naive standard errors understate uncertainty by factors of two to five. The CoxTimeVaryingFitter in lifelines computes the correct robust variance when given the cluster column. Logistic panel regressions require an explicit cluster-robust covariance matrix through a library such as statsmodels.

The second is unbalanced panels. Accounts enter and leave the portfolio continuously. Missing observations are not missing at random: low-risk accounts attrite voluntarily, high-risk accounts are closed by the bank. A fixed-effects logistic (conditional logit) absorbs the permanent account-specific component of risk but discards any variable that is time-invariant, including most origination features. A random-effects logistic keeps the origination features but assumes the unobserved heterogeneity is uncorrelated with them, which is usually false. The pragmatic compromise is a random-effects model with a rich set of account-level summaries (origination score, tenure bucket, product type) that proxy for the unobserved component.