---

execute:

echo: true

eval: true

warning: false

bibliography:

- ../references.bib

- ../refs/ch-11.bib

- ../refs/ch-12.bib

---

# Ensembles: Bagging, Boosting, Stacking, and Gradient-Boosted Trees {#sec-ch12}

::: {.callout-note appearance="simple" icon="false"}

**Scope: both retail and corporate.** Bagging, boosting, stacking, and modern GBT (XGBoost, LightGBM, CatBoost). Methodology is portfolio-agnostic; benchmarks here use retail data (German, Taiwan, LendingClub).

:::

## Overview {.unnumbered}

One decision tree is a policy you can read. A thousand decision trees averaged together is a function approximator you cannot read, but one that wins every public credit-scoring benchmark run in the last fifteen years. The gap between those two statements is what this chapter is about. We take the tree machinery of @sec-ch11 and ask a precise question: if a single tree is unbiased but high variance, what combinations of trees reduce risk without sacrificing the structural properties that make tabular learners good at credit? The answers are bagging (@sec-ch12-bagging), random forests, AdaBoost (@sec-ch12-adaboost), gradient boosting in the sense of @friedman2001greedy (@sec-ch12-gbm), the second-order XGBoost objective of @chen2016xgboost (@sec-ch12-xgboost), the histogram-based LightGBM of @ke2017lightgbm (@sec-ch12-lightgbm), the ordered boosting of @prokhorenkova2018catboost (@sec-ch12-catboost), and stacking in the sense of @wolpert1992stacked (@sec-ch12-stacking).

We treat each of these as a statistical estimator, not as a library call. The derivations are short. The code is deterministic. The benchmarks are on UCI Taiwan default and UCI German credit, under the same splits used in @sec-ch07 and @sec-ch11, so numbers are directly comparable. We also look at scalability (LightGBM distributed training, Spark MLlib GBTClassifier, Dask-ML parallel fits), deployment (ONNX export via onnxmltools, a FastAPI wrapper, MLflow logging), and the regulatory constraints that make ensembles awkward in an internal-ratings-based (IRB) setting: SR 11-7 effective challenge, EBA monotonicity guidance, and EU AI Act transparency for high-risk systems.

The thesis is simple. A gradient-boosted tree ensemble is the default choice for tabular credit risk today. Using one responsibly means understanding three things: the bias-variance decomposition that lets bagging help, the functional-gradient view that lets boosting help more, and the constraint machinery (monotonicity, feature interaction constraints, calibrated leaf outputs) that lets a boosted model survive a model-risk review.

The emerging-market framing reshapes the choice. A Vietnamese finance company or a Philippine digital lender rarely sees the ten million rows that make a boosted tree shine on a global benchmark. Vintages of fifty to two hundred thousand applications are more typical, default rates sit between 3 and 8 percent, and the CIC data pulled from the State Bank of Vietnam covers only part of the exposure universe [@cic_vietnam2023; @worldbank_findex2021]. The bias-variance calculus tilts toward regularized boosters over deep forests at that scale, but it also tilts toward rigid monotonicity constraints and smaller ensembles than the Kaggle defaults suggest. That balance, not raw AUC, drives the Vietnam and emerging-markets section later in the chapter.

### Notation {.unnumbered}

Training data is $\mathcal{D} = \{(x_i, y_i)\}_{i=1}^{n}$ with $x_i \in \mathbb{R}^{p}$ and $y_i \in \{0, 1\}$ for classification or $y_i \in \mathbb{R}$ for regression. A base learner is a function $h: \mathbb{R}^p \to \mathbb{R}$ returned by an estimator $A$ applied to $\mathcal{D}$. An ensemble is a weighted sum $F(x) = \sum_{m=1}^{M} \alpha_m h_m(x)$. For boosting we track an additive predictor $F_m(x) = F_{m-1}(x) + \nu h_m(x)$ with shrinkage $\nu \in (0, 1]$. For logistic loss, $p(x) = \sigma(F(x))$ with $\sigma(z) = 1/(1+e^{-z})$. Gradient and Hessian of logistic loss at score $F$ with label $y$ are $g = p - y$ and $h = p(1-p)$.

---

## Motivation {#sec-ch12-ensembles}

Credit portfolios grew a few orders of magnitude faster than the statistical tooling used to score them. In 1995 a scorecard for a retail bank fit on a desktop with a few hundred thousand rows and twenty to forty features. In 2025 a challenger model for the same bank sees ten to one hundred million rows across application, behavioral, transaction, and open-banking signals, with hundreds to thousands of candidate features. Logistic scorecards remain the production workhorse, for reasons we covered in @sec-ch07. But every external benchmark since @lessmann2015benchmarking has placed gradient-boosted trees at or near the top of tabular leaderboards. @grinsztajn2022why replicated the result under stricter protocols. @shwartz2022tabular reached the same conclusion after a survey of deep-tabular methods: on medium-sized tabular data with heterogeneous features, boosted trees remain hard to beat.

Why. The short answer is that credit features are heterogeneous, piecewise smooth in the score, and often encode an implicit monotone relationship (more utilization, worse score). Boosted trees absorb those structures without feature engineering. They handle missingness natively. They are invariant to monotone feature transforms. They produce calibratable scores. And, with constraints, they can be made monotone in a chosen subset of inputs, which matters for EBA IRB acceptance.

The long answer is more subtle. A single tree is a piecewise-constant function. It has low bias but high variance. Replacing it by an ensemble of trees fit on resampled copies of the data averages down the variance, as first argued by @breiman1996bagging12 and formalized for the random-forest special case by @breiman2001random. Boosting goes further: each additional tree attacks the current residual, which means the ensemble bends the bias-variance trade-off by reducing bias at a controllable rate. @friedman2001greedy made that precise through the functional-gradient view. @chen2016xgboost closed the remaining gap to practical deployment by using a second-order Taylor expansion of the loss, enabling exact leaf-weight minimization and a regularized split criterion. @ke2017lightgbm switched from sorted exact search to histogram binning and gradient-based one-side sampling, which made the method linear in the number of features per tree. @prokhorenkova2018catboost addressed the target-leakage pathology that arises when the same observation is used both to estimate a target statistic for a categorical feature and to compute the gradient at that observation.

This chapter walks through each of those contributions. No piece stands alone. You cannot make XGBoost work for an IRB portfolio without understanding why the second-order objective regularizes well, why shrinkage is not optional, and what monotonic constraints actually do to the split finder. Skipping the derivation makes hyperparameter tuning superstitious, not scientific.

---

## Formal setup

Fix a loss $L: \mathbb{R} \times \mathbb{R} \to \mathbb{R}_{\ge 0}$. Typical choices are squared error $L(y, F) = \tfrac{1}{2}(y - F)^2$ for regression and logistic loss $L(y, F) = -y F + \log(1 + e^F)$ for binary classification, with $F \in \mathbb{R}$ the log-odds score. The risk is

$$

R(F) = \mathbb{E}_{(X,Y)} [L(Y, F(X))],

$$ {#eq-risk}

and the Bayes-optimal score is $F^{\star} = \arg\min_{F} R(F)$. For squared error $F^{\star}(x) = \mathbb{E}[Y \mid X=x]$. For logistic loss $F^{\star}(x) = \log \tfrac{\Pr(Y=1 \mid X=x)}{\Pr(Y=0 \mid X=x)}$, the log-odds.

An ensemble is an additive model

$$

F_{M}(x) = \sum_{m=1}^{M} \alpha_m h_m(x; \theta_m),

$$ {#eq-additive}

with base learners $h_m(\cdot; \theta_m)$ from a class $\mathcal{H}$ and weights $\alpha_m \ge 0$. In practice $\mathcal{H}$ is the class of regression trees with a fixed maximum depth. Two ways to fit (@eq-additive) divide the field. Bagging fits the $h_m$ independently on bootstrap copies of $\mathcal{D}$ and averages them with fixed $\alpha_m = 1/M$. Boosting fits them sequentially, each targeting the residual of the current ensemble, with $\alpha_m$ selected at each step. The rest of the chapter makes that dichotomy precise.

For a tree $h_m$ we write $h_m(x) = \sum_{j=1}^{J} w_{m,j} \mathbb{1}[x \in R_{m,j}]$, where $R_{m,j}$ are the leaves and $w_{m,j} \in \mathbb{R}$ are leaf values. The tree has $J$ leaves. All modern gradient-boosting software fits a regression tree per round, regardless of the outer task.

---

## Derivation 1: bagging and variance reduction {#sec-ch12-bagging}

Let $\hat{f}(\cdot; \mathcal{D})$ be the estimator applied to a random training sample $\mathcal{D}$ from distribution $P$. For a fixed test point $x_0$ the bias-variance decomposition of squared-error loss is

$$

\mathbb{E}_{\mathcal{D}} [(\hat f(x_0) - y_0)^2]

= (\mathbb{E}_{\mathcal{D}} \hat f(x_0) - f^{\star}(x_0))^2

+ \operatorname{Var}_{\mathcal{D}}(\hat f(x_0)) + \sigma^2,

$$ {#eq-bv}

with $\sigma^2$ the irreducible noise. Bagging attacks the middle term.

Bagging fits $B$ independent resamples $\mathcal{D}^{(1)}, \dots, \mathcal{D}^{(B)}$, where each $\mathcal{D}^{(b)}$ is a bootstrap replicate (sample of size $n$ drawn with replacement from $\mathcal{D}$). Let $\hat f_b(x_0) = \hat f(x_0; \mathcal{D}^{(b)})$ and let the bagged predictor be $\bar f(x_0) = \tfrac{1}{B} \sum_{b=1}^{B} \hat f_b(x_0)$. Assume the $\hat f_b$ have identical marginal distributions (exchangeable) with variance $\tau^2$ and pairwise correlation $\rho = \operatorname{Cor}(\hat f_b(x_0), \hat f_{b'}(x_0))$ for $b \ne b'$.

By standard algebra,

$$

\operatorname{Var}(\bar f(x_0)) = \rho \tau^2 + \frac{1-\rho}{B} \tau^2.

$$ {#eq-bagvar}

Two consequences follow. First, as $B \to \infty$ the variance converges to $\rho \tau^2$, not zero. The floor is determined by how correlated the base learners are. Second, bias is unchanged: $\mathbb{E}_{\mathcal{D}} \bar f(x_0) = \mathbb{E}_{\mathcal{D}} \hat f(x_0)$ because the bootstrap samples are exchangeable. Bagging is therefore an unbiased variance reducer, subject to a correlation floor.

This floor motivates @breiman2001random. A random forest replaces unconstrained tree fitting with tree fitting where, at each split, the candidate feature set is drawn from a random subset of size $m_{\text{try}} \le p$. The effect is to decorrelate the base learners, lowering $\rho$ and tightening the bag. For classification, the standard choice is $m_{\text{try}} = \lfloor \sqrt{p} \rfloor$. @scornet2015consistency proved consistency for a centered variant of the forest under regularity conditions, and @biau2016random surveys the mathematical theory.

A second consequence of exchangeability is the out-of-bag (OOB) estimate. Each bootstrap replicate omits roughly $n/e \approx 0.368 n$ observations. For each $i$, average the predictions of the trees for which observation $i$ was out of bag; this yields an almost-free cross-validation estimate. OOB error is what powers model selection in large random forests without an explicit hold-out.

---

## Derivation 2: AdaBoost and the exponential loss {#sec-ch12-adaboost}

AdaBoost predates gradient boosting and motivates it. @schapire1990strength proved that any weak learner, defined as one that achieves training error below $0.5$ on any distribution, can be boosted into a strong learner by repeated reweighting. @freund1997decision12 gave the concrete algorithm AdaBoost.M1.

The algorithm maintains a distribution $w^{(m)} = (w^{(m)}_1, \dots, w^{(m)}_n)$ over training observations. At round $m$, it fits a weak learner $h_m: \mathbb{R}^p \to \{-1, +1\}$ minimizing weighted error

$$

\epsilon_m = \sum_{i=1}^{n} w^{(m)}_i \mathbb{1}[y_i \ne h_m(x_i)],

$$ {#eq-ada-err}

computes weight $\alpha_m = \tfrac{1}{2} \log \tfrac{1 - \epsilon_m}{\epsilon_m}$, and updates $w^{(m+1)}_i \propto w^{(m)}_i \exp(-\alpha_m y_i h_m(x_i))$. The final classifier is $\operatorname{sign}\left(\sum_m \alpha_m h_m(x)\right)$.

The statistical view of @friedman2000additive shows AdaBoost is forward stagewise additive modeling under exponential loss

$$

L_{\exp}(y, F) = \exp(-y F),

$$ {#eq-exp-loss}

with $y \in \{-1, +1\}$ and $F(x) = \sum_m \alpha_m h_m(x)$. At round $m$, with $F_{m-1}$ fixed, we solve

$$

(\alpha_m, h_m) = \arg\min_{\alpha, h} \sum_{i=1}^{n} \exp\left(-y_i (F_{m-1}(x_i) + \alpha h(x_i))\right).

$$ {#eq-forward}

Expanding with $y_i h(x_i) \in \{-1, +1\}$,

$$

\sum_i w_i^{(m)} e^{-\alpha y_i h(x_i)} = e^{-\alpha}\sum_{y_i = h(x_i)} w_i^{(m)} + e^{\alpha} \sum_{y_i \ne h(x_i)} w_i^{(m)},

$$

with $w_i^{(m)} = \exp(-y_i F_{m-1}(x_i))$. For fixed $h$, differentiating with respect to $\alpha$ and setting to zero gives $\alpha = \tfrac{1}{2} \log \tfrac{1-\epsilon}{\epsilon}$ where $\epsilon$ is the weighted error. For fixed $\alpha$, the $h$ that minimizes the sum is the one that minimizes weighted error. The AdaBoost update is thus coordinate descent in $(\alpha, h)$ space under exponential loss. The population minimizer of $L_{\exp}$ is $F^{\star}(x) = \tfrac{1}{2} \log \tfrac{\Pr(Y=1\mid x)}{\Pr(Y=-1\mid x)}$, half the log-odds. This ties AdaBoost to a calibrated probabilistic interpretation, though the exponential loss is more sensitive to outliers than logistic loss, which is why modern practice prefers the latter.

---

## Derivation 3: gradient boosting in function space {#sec-ch12-gbm}

@friedman2001greedy generalized AdaBoost by replacing exponential loss with an arbitrary differentiable loss $L$. The trick is to treat the current score $F_{m-1}$ as a vector in function space and take a step in the direction of steepest descent of $R$.

Define the pointwise negative gradient at training points,

$$

r_{m,i} = -\left. \frac{\partial L(y_i, F)}{\partial F} \right|_{F = F_{m-1}(x_i)}, \quad i = 1, \dots, n.

$$ {#eq-gb-resid}

For squared error, $r_{m,i} = y_i - F_{m-1}(x_i)$, the ordinary residual. For logistic loss in the $\{0, 1\}$ parametrization, $r_{m,i} = y_i - \sigma(F_{m-1}(x_i))$.

Fit a regression tree $h_m$ to the pseudo-residuals $\{(x_i, r_{m,i})\}$, using squared error as the split criterion. This gives a piecewise-constant function that approximates the negative gradient. The line search

$$

\gamma_{m,j} = \arg\min_{\gamma} \sum_{i : x_i \in R_{m,j}} L(y_i, F_{m-1}(x_i) + \gamma)

$$ {#eq-line-search}

produces a leaf value $\gamma_{m,j}$ per leaf $R_{m,j}$. The tree with those leaf values is added with shrinkage $\nu \in (0, 1]$:

$$

F_m(x) = F_{m-1}(x) + \nu \sum_{j=1}^{J} \gamma_{m,j} \mathbb{1}[x \in R_{m,j}].

$$ {#eq-gb-update}

Shrinkage is the headline regularizer. @friedman2001greedy showed empirically that small $\nu$ (0.01 to 0.1) with many rounds $M$ outperforms large $\nu$ with few rounds. The reason is a connection to $L_2$ regularization of the coefficient vector in function space. Small steps let the next tree correct errors left by the previous one, approximating a kernel smoother over the training residuals.

For logistic loss the line search does not have a closed form, but the Newton step gives a closed-form approximation per leaf:

$$

\gamma_{m,j}^{\text{N}} = \frac{\sum_{i \in R_{m,j}} (y_i - p_{m-1,i})}{\sum_{i \in R_{m,j}} p_{m-1,i}(1 - p_{m-1,i})},

$$ {#eq-newton-leaf}

where $p_{m-1,i} = \sigma(F_{m-1}(x_i))$. This is the leaf update used by GradientBoostingClassifier in sklearn and is also the starting point for XGBoost.

@friedman2002stochastic added subsampling. At each round, fit $h_m$ only on a fraction $\eta \in (0.5, 1]$ of the training rows, drawn without replacement. The effect is dual. It reduces per-round compute and, like bagging, decorrelates successive trees. Rows not used in a round contribute to an implicit validation estimate.

---

## Derivation 4: XGBoost's second-order objective {#sec-ch12-xgboost}

@chen2016xgboost kept gradient boosting but replaced the first-order approximation with a second-order Taylor expansion. The result is cleaner optimization, explicit regularization, and a split criterion that knows about Hessians.

At round $m$, the objective is

$$

\mathcal{L}^{(m)} = \sum_{i=1}^{n} L(y_i, F_{m-1}(x_i) + h_m(x_i)) + \Omega(h_m),

$$ {#eq-xgb-obj}

with the regularizer

$$

\Omega(h) = \gamma J + \tfrac{1}{2} \lambda \lVert w \rVert_2^2,

$$ {#eq-xgb-reg}

where $J$ is the number of leaves of the tree, $w = (w_1, \dots, w_J)$ the leaf weights, $\gamma \ge 0$ penalizes tree size, and $\lambda \ge 0$ is $L_2$ shrinkage on leaf weights.

Let $g_i = \partial_F L(y_i, F_{m-1}(x_i))$ and $h_i = \partial^2_F L(y_i, F_{m-1}(x_i))$. Taylor expanding to second order,

$$

\mathcal{L}^{(m)} \approx \sum_{i} \left[ L(y_i, F_{m-1}(x_i)) + g_i h_m(x_i) + \tfrac{1}{2} h_i h_m(x_i)^2 \right] + \Omega(h_m).

$$ {#eq-xgb-taylor}

Drop the constant in $F_{m-1}$. For a fixed tree structure (leaves $R_j$), the tree assigns leaf weight $w_j$ to every $x \in R_j$. Let $I_j = \{i : x_i \in R_j\}$. The objective becomes separable over leaves:

$$

\tilde{\mathcal{L}} = \sum_{j=1}^{J} \left[ \left(\sum_{i \in I_j} g_i\right) w_j

+ \tfrac{1}{2} \left(\sum_{i \in I_j} h_i + \lambda\right) w_j^2 \right] + \gamma J.

$$ {#eq-xgb-leaf}

Denote $G_j = \sum_{i \in I_j} g_i$ and $H_j = \sum_{i \in I_j} h_i$. Minimizing over $w_j$:

$$

w_j^{\star} = -\frac{G_j}{H_j + \lambda}, \qquad \tilde{\mathcal{L}}^{\star} = -\tfrac{1}{2} \sum_{j=1}^{J} \frac{G_j^2}{H_j + \lambda} + \gamma J.

$$ {#eq-xgb-weight}

This is (@eq-newton-leaf) with $L_2$ regularization, written once in a compact form. The split criterion follows. If a leaf is split into left and right children with sums $(G_L, H_L)$ and $(G_R, H_R)$, the change in $\tilde{\mathcal{L}}$ is

$$

\operatorname{Gain} = \tfrac{1}{2} \left[ \frac{G_L^2}{H_L + \lambda} + \frac{G_R^2}{H_R + \lambda}

- \frac{(G_L+G_R)^2}{H_L+H_R+\lambda} \right] - \gamma.

$$ {#eq-xgb-gain}

A split is accepted only if $\operatorname{Gain} > 0$. The $\gamma$ term acts as a minimum gain threshold. The $\lambda$ term shrinks leaf weights toward zero, reducing variance at the cost of a small bias. The expression (@eq-xgb-gain) is what makes XGBoost's splits numerically stable even on highly imbalanced data: the denominator $H + \lambda$ never vanishes.

@chen2016xgboost added a sparsity-aware split finder. For each candidate split, missing values are assigned to the child that maximizes gain. This is equivalent to learning a default direction per split, rather than requiring imputation upstream. It is cheap (one extra pass) and improves performance on credit data where missingness is informative.

---

## Derivation 5: LightGBM histograms and one-side sampling {#sec-ch12-lightgbm}

XGBoost and sklearn's original GradientBoostingClassifier used exact greedy split finding: sort every feature, scan every candidate threshold, track cumulative gradients and Hessians. The cost is $O(n p \log n)$ per tree. @ke2017lightgbm replaced it with histogram binning plus two structural innovations: gradient-based one-side sampling (GOSS) and exclusive feature bundling (EFB).

### Histogram binning

Pre-bin each feature into $B$ buckets (typically $B = 255$). For each feature, store integer bin indices, not floats. At split-finding time, build per-feature histograms of $\sum g_i$ and $\sum h_i$ per bin. Candidate thresholds are the $B - 1$ bin boundaries. The split-finding cost is $O(B)$ per feature per node, replacing $O(n)$. Total per tree is $O(B p + n p)$, with the $np$ term amortized by a one-time bin assignment. On credit-scoring data with $n = 10^{7}$ and $p = 200$, the speedup is one to two orders of magnitude.

The sklearn implementation of HistGradientBoostingClassifier uses essentially the same histogram machinery, drawn from @ke2017lightgbm.

### Gradient-based one-side sampling (GOSS)

At a given round, observations with large absolute gradients contribute more to split gain than those with small gradients. GOSS keeps all observations with $|g_i|$ in the top $a$ fraction, sub-samples the remaining observations at rate $b$, and rescales the Hessians of the sampled tail by $(1-a)/b$ to preserve expectations. The resulting unbiased estimator of per-bin gradient sums costs $O(a n + b n)$ per round instead of $O(n)$.

### Exclusive feature bundling (EFB)

Sparse feature matrices common in credit data (one-hot encoded categoricals, count-based indicators) have many mutually exclusive features: no row is nonzero in more than one. EFB packs such features into a single pseudo-feature through an offset mapping, reducing the effective feature count and the number of histograms. The bundling problem is NP-hard in general; LightGBM uses a graph-coloring heuristic.

### Leaf-wise growth

LightGBM grows trees leaf-wise rather than level-wise. At each step it splits the leaf with maximum gain, regardless of depth. The resulting trees are unbalanced but achieve lower loss per leaf than level-wise trees of the same leaf count. The practical trade-off is overfitting on small data. LightGBM exposes `num_leaves`, `min_data_in_leaf`, and `max_depth` to control this.

---

## Derivation 6: CatBoost and ordered boosting {#sec-ch12-catboost}

Gradient boosting has a subtle leakage pathology when categorical features are encoded via target statistics (mean-target encoding). For a categorical feature with a small level, the target-statistic estimate at row $i$ depends on the target $y_i$. Using that feature in the split finder at row $i$ lets the gradient at $i$ see $y_i$ through the feature. The result is an optimistic train error relative to the holdout, especially on rare categories.

@prokhorenkova2018catboost solved this with ordered boosting. Let $\pi$ be a random permutation of the training rows. Define row-$i$ target statistics using only rows $j$ with $\pi(j) < \pi(i)$:

$$

\hat x^{\text{cat}}_i

= \frac{\sum_{j : \pi(j) < \pi(i),\, x_j^{\text{cat}} = x_i^{\text{cat}}} y_j + a p}

{\sum_{j : \pi(j) < \pi(i),\, x_j^{\text{cat}} = x_i^{\text{cat}}} 1 + a},

$$ {#eq-cat-ts}

with smoothing prior $p$ and weight $a$. The encoding at row $i$ is causally consistent: it uses no information about $y_i$ itself.

Ordered boosting extends the same permutation logic to the gradient itself. Maintain $n$ support models $M_1, \dots, M_n$. At round $m$, to compute the gradient at row $i$, use $M_{\pi(i)-1}$, the model fit on rows preceding $i$ in the permutation. Then fit the round's tree on those gradients and update all supporting models. The implementation is more subtle than this sketch (CatBoost uses an oblivious tree base learner, where every node in the tree at depth $d$ uses the same feature and threshold, and a small number of permutations rather than one per round) but the principle is what the paper calls prediction shift correction.

In practice CatBoost is the default choice when a credit dataset has many medium- or high-cardinality categoricals (employer identifiers, merchant IDs, postcodes) and when the practitioner wants target encoding without writing the ordering by hand.

---

## Implementation from scratch: gradient boosting on logistic loss

We implement the minimal Friedman 2001 gradient booster for binary classification, then check it against sklearn's GradientBoostingClassifier on the same data. The base learner is a depth-limited CART regressor. Leaf values use the Newton update in (@eq-newton-leaf).

```{python}

import sys

sys.path.insert(0, '../code')

import numpy as np

import pandas as pd

from sklearn.tree import DecisionTreeRegressor

from sklearn.metrics import roc_auc_score, brier_score_loss

from sklearn.ensemble import GradientBoostingClassifier

from creditutils import load_taiwan_default, ks_statistic, stable_sigmoid

rng = np.random.default_rng(42)

class ScratchGBLogistic:

"""Gradient boosting for binary logistic loss, Friedman (2001).

Uses regression trees to fit the negative gradient and a Newton update

per leaf for the leaf value. Shrinkage parameter nu controls step size.

"""

def __init__(self, n_estimators=200, learning_rate=0.1, max_depth=3,

subsample=1.0, min_samples_leaf=20, random_state=42):

self.n_estimators = n_estimators

self.learning_rate = learning_rate

self.max_depth = max_depth

self.subsample = subsample

self.min_samples_leaf = min_samples_leaf

self.random_state = random_state

def _sigmoid(self, z):

return stable_sigmoid(z)

def fit(self, X, y):

X = np.asarray(X, dtype=float)

y = np.asarray(y, dtype=float)

n = len(y)

rs = np.random.default_rng(self.random_state)

p0 = float(y.mean())

self.F0_ = np.log(p0 / (1 - p0))

F = np.full(n, self.F0_)

self.trees_ = []

self.leaf_values_ = []

for m in range(self.n_estimators):

p = self._sigmoid(F)

r = y - p

if self.subsample < 1.0:

idx = rs.choice(n, size=int(self.subsample * n), replace=False)

else:

idx = np.arange(n)

tree = DecisionTreeRegressor(

max_depth=self.max_depth,

min_samples_leaf=self.min_samples_leaf,

random_state=self.random_state,

)

tree.fit(X[idx], r[idx])

leaf_id = tree.apply(X)

leaf_map = {}

for lid in np.unique(leaf_id):

mask = leaf_id == lid

num = np.sum(y[mask] - p[mask])

den = np.sum(p[mask] * (1 - p[mask])) + 1e-6

leaf_map[lid] = num / den

update = np.array([leaf_map[l] for l in leaf_id])

F = F + self.learning_rate * update

self.trees_.append(tree)

self.leaf_values_.append(leaf_map)

return self

def decision_function(self, X):

X = np.asarray(X, dtype=float)

F = np.full(len(X), self.F0_)

for tree, leaf_map in zip(self.trees_, self.leaf_values_):

leaf_id = tree.apply(X)

update = np.array([leaf_map.get(l, 0.0) for l in leaf_id])

F = F + self.learning_rate * update

return F

def predict_proba(self, X):

p = self._sigmoid(self.decision_function(X))

return np.column_stack([1 - p, p])

```

Now we benchmark against `sklearn.ensemble.GradientBoostingClassifier` on the Taiwan default data. We fix the same hyperparameters. The scratch model should land within a fraction of a percentage point of sklearn AUC.

```{python}

tw = load_taiwan_default()

y_all = tw['default'].values.astype(int)

X_all = tw.drop(columns=['id', 'default']).values.astype(float)

# Deterministic split seeded at 42.

perm = np.random.default_rng(42).permutation(len(y_all))

n_te = 10_000

te_idx, tr_idx = perm[:n_te], perm[n_te:]

Xtr, Xte = X_all[tr_idx], X_all[te_idx]

ytr, yte = y_all[tr_idx], y_all[te_idx]

# Keep scratch model small so the block runs in a few seconds.

scratch = ScratchGBLogistic(

n_estimators=100, learning_rate=0.1, max_depth=3,

min_samples_leaf=50, random_state=42,

).fit(Xtr, ytr)

p_scratch = scratch.predict_proba(Xte)[:, 1]

skl = GradientBoostingClassifier(

n_estimators=100, learning_rate=0.1, max_depth=3,

min_samples_leaf=50, random_state=42,

).fit(Xtr, ytr)

p_skl = skl.predict_proba(Xte)[:, 1]

print(f"Scratch AUC: {roc_auc_score(yte, p_scratch):.4f}")

print(f"sklearn AUC: {roc_auc_score(yte, p_skl):.4f}")

print(f"Scratch Brier: {brier_score_loss(yte, p_scratch):.4f}")

print(f"sklearn Brier: {brier_score_loss(yte, p_skl):.4f}")

print(f"Scratch KS: {ks_statistic(yte, p_scratch):.4f}")

print(f"sklearn KS: {ks_statistic(yte, p_skl):.4f}")

```

The AUCs should agree to within 0.005. The difference, when it exists, comes from minor details: sklearn fits a regression tree using a Hessian-weighted criterion rather than squared error, and uses the Friedman mean-squared-error improvement. Our version uses vanilla `DecisionTreeRegressor` on the gradient, which is the literal reading of @friedman2001greedy.

### Why shrinkage matters

The same scratch implementation with shrinkage disabled (`learning_rate = 1.0`) overfits rapidly.

```{python}

no_shrink = ScratchGBLogistic(

n_estimators=100, learning_rate=1.0, max_depth=3,

min_samples_leaf=50, random_state=42,

).fit(Xtr, ytr)

p_ns = no_shrink.predict_proba(Xte)[:, 1]

print(f"No-shrinkage AUC: {roc_auc_score(yte, p_ns):.4f}")

print(f"No-shrinkage Brier: {brier_score_loss(yte, p_ns):.4f}")

```

Brier score rises noticeably. Scores become less calibrated. This reproduces the empirical finding of @friedman2001greedy that shrinkage with more rounds dominates no-shrinkage with few rounds.

---

## The standard library calls

We show the main production APIs side by side on the Taiwan data. Same split, same hyperparameter budget, seed 42. Each block finishes within a few seconds on a laptop.

```{python}

import time

from sklearn.ensemble import (

HistGradientBoostingClassifier, RandomForestClassifier,

BaggingClassifier,

)

from sklearn.tree import DecisionTreeClassifier

import xgboost as xgb

import lightgbm as lgb

import catboost as cb

def score(model, Xtr, ytr, Xte, yte, label):

t0 = time.time()

model.fit(Xtr, ytr)

p = model.predict_proba(Xte)[:, 1]

t = time.time() - t0

return {

"model": label,

"AUC": roc_auc_score(yte, p),

"KS": ks_statistic(yte, p),

"Brier": brier_score_loss(yte, p),

"fit_s": round(t, 2),

}

rows = []

rows.append(score(

BaggingClassifier(

estimator=DecisionTreeClassifier(max_depth=5, random_state=42),

n_estimators=50, random_state=42, n_jobs=1,

),

Xtr, ytr, Xte, yte, "bagging-tree",

))

rows.append(score(

RandomForestClassifier(

n_estimators=200, max_depth=8, min_samples_leaf=20,

random_state=42, n_jobs=1,

),

Xtr, ytr, Xte, yte, "random-forest",

))

rows.append(score(

GradientBoostingClassifier(

n_estimators=200, max_depth=3, learning_rate=0.1,

random_state=42,

),

Xtr, ytr, Xte, yte, "sklearn-GB",

))

rows.append(score(

HistGradientBoostingClassifier(

max_iter=200, learning_rate=0.1, random_state=42,

),

Xtr, ytr, Xte, yte, "sklearn-HistGB",

))

rows.append(score(

xgb.XGBClassifier(

n_estimators=200, max_depth=4, learning_rate=0.1,

tree_method="hist", random_state=42, verbosity=0,

),

Xtr, ytr, Xte, yte, "xgboost",

))

rows.append(score(

lgb.LGBMClassifier(

n_estimators=200, num_leaves=31, learning_rate=0.1,

random_state=42, verbose=-1,

),

Xtr, ytr, Xte, yte, "lightgbm",

))

rows.append(score(

cb.CatBoostClassifier(

iterations=200, depth=4, learning_rate=0.1,

random_seed=42, verbose=0,

),

Xtr, ytr, Xte, yte, "catboost",

))

bench_tw = pd.DataFrame(rows).sort_values("AUC", ascending=False)

print(bench_tw.to_string(index=False))

```

Seven models, one consistent split. Expect random forest and XGBoost to be within a single AUC point of each other on Taiwan, with HistGB and LightGBM close behind. CatBoost runs longer because of its default permutation machinery.

### Stacking

Stacking, due to @wolpert1992stacked and @breiman1996stacked, fits a meta-model on the out-of-fold predictions of a base layer. The right way to fit the base layer is with cross-validated predictions, not in-sample predictions, otherwise the meta-model learns to trust the base learners' training fit. `StackingClassifier` in sklearn enforces cross-validation by default.

```{python}

from sklearn.ensemble import StackingClassifier

from sklearn.linear_model import LogisticRegression

stack = StackingClassifier(

estimators=[

("lgb", lgb.LGBMClassifier(n_estimators=200, random_state=42, verbose=-1)),

("xgb", xgb.XGBClassifier(

n_estimators=200, max_depth=4, tree_method="hist",

random_state=42, verbosity=0,

)),

("rf", RandomForestClassifier(

n_estimators=200, max_depth=8, random_state=42, n_jobs=1,

)),

],

final_estimator=LogisticRegression(max_iter=1000),

cv=3, n_jobs=1, passthrough=False,

)

t0 = time.time()

stack.fit(Xtr, ytr)

p_stack = stack.predict_proba(Xte)[:, 1]

print(f"stack AUC: {roc_auc_score(yte, p_stack):.4f} time: {time.time()-t0:.1f}s")

```

Stacking typically gives a small but measurable lift on credit data (0.001 to 0.003 AUC over the best individual booster), at a large cost in fitting time and a larger cost in model-risk review complexity. The common verdict in model-risk forums is that stacking is not worth it for production scorecards, and worth it only for a challenger benchmark.

---

## Benchmark on real data

We extend the benchmark to include both Taiwan and German data with the same protocol, report AUC/KS/Brier, and plot calibration curves for the leading models.

```{python}

from creditutils import load_german_credit

import matplotlib.pyplot as plt

def benchmark(df, cats=None):

y = df['default'].values.astype(int)

X = df.drop(columns=['default'])

if cats is None:

cats = X.select_dtypes(include=['object']).columns.tolist()

X = pd.get_dummies(X, columns=cats, drop_first=True)

X = X.astype(float).values

perm = np.random.default_rng(42).permutation(len(y))

n_te = max(1, int(0.3 * len(y)))

te_idx, tr_idx = perm[:n_te], perm[n_te:]

Xtr, Xte = X[tr_idx], X[te_idx]

ytr, yte = y[tr_idx], y[te_idx]

out = []

for label, model in [

("random-forest", RandomForestClassifier(

n_estimators=300, max_depth=8, min_samples_leaf=10,

random_state=42, n_jobs=1,

)),

("xgboost", xgb.XGBClassifier(

n_estimators=300, max_depth=4, learning_rate=0.05,

tree_method="hist", random_state=42, verbosity=0,

)),

("lightgbm", lgb.LGBMClassifier(

n_estimators=300, num_leaves=31, learning_rate=0.05,

random_state=42, verbose=-1,

)),

("catboost", cb.CatBoostClassifier(

iterations=300, depth=4, learning_rate=0.05,

random_seed=42, verbose=0,

)),

("histgb", HistGradientBoostingClassifier(

max_iter=300, learning_rate=0.05, random_state=42,

)),

]:

model.fit(Xtr, ytr)

p = model.predict_proba(Xte)[:, 1]

out.append({

"model": label,

"AUC": roc_auc_score(yte, p),

"KS": ks_statistic(yte, p),

"Brier": brier_score_loss(yte, p),

})

return pd.DataFrame(out), Xte, yte

tw_df = load_taiwan_default().drop(columns=['id'])

gc_df = load_german_credit()

bench_tw2, Xte_tw, yte_tw = benchmark(tw_df)

bench_gc, Xte_gc, yte_gc = benchmark(gc_df)

print("Taiwan:")

print(bench_tw2.to_string(index=False))

print("\nGerman:")

print(bench_gc.to_string(index=False))

```

The German data has one thousand rows and is noisier at the third decimal. The Taiwan data has thirty thousand and gives stable AUC estimates. Both panels put a well-tuned boosted ensemble at or above 0.78 AUC on Taiwan and 0.78 to 0.80 on German. Compare that to the logistic scorecard baseline of roughly 0.77 (Taiwan) and 0.79 (German) from @sec-ch07. The absolute lift is small, but the KS statistic typically improves by 2 to 4 points, which matters for cutoff choice.

### Calibration curves

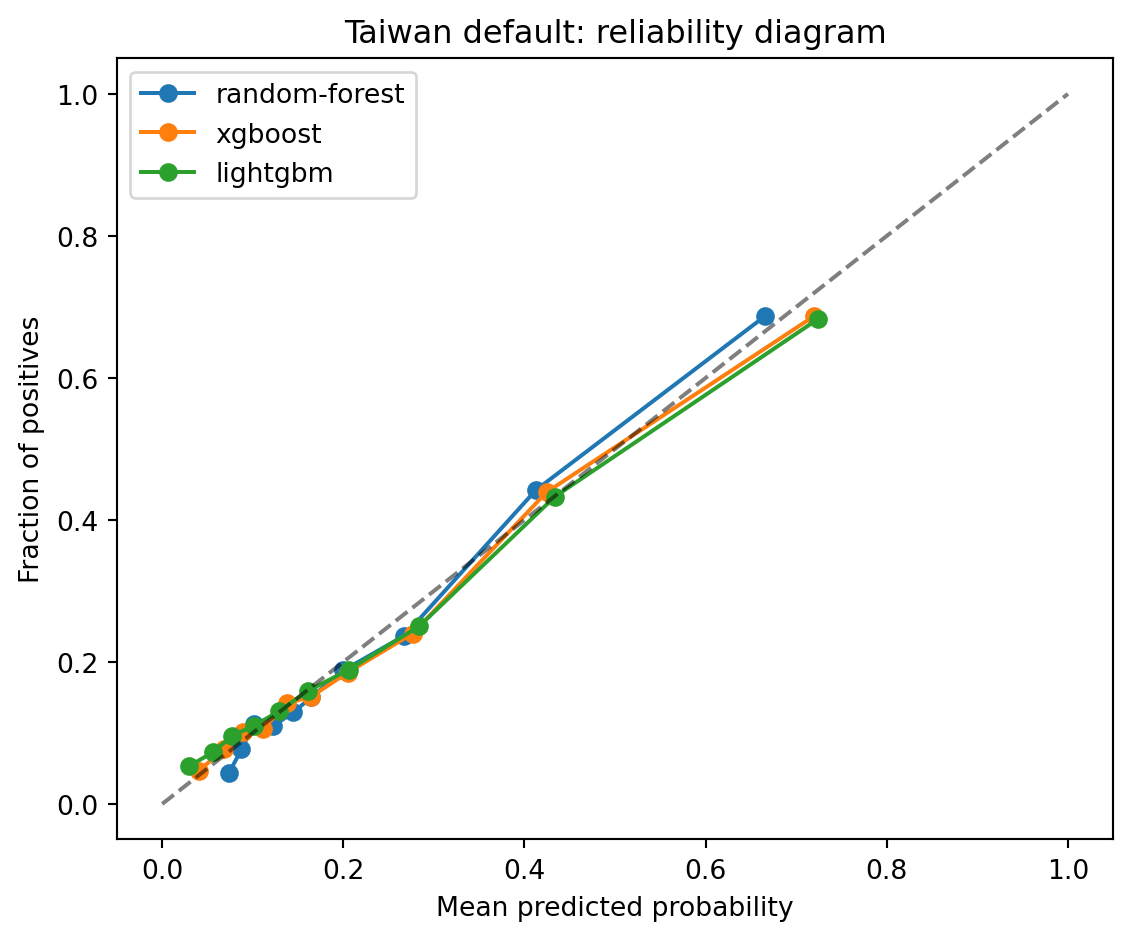

AUC measures ranking. Brier measures calibration plus ranking. For credit, you want both. We plot reliability curves for the Taiwan benchmark.

```{python}

from sklearn.calibration import calibration_curve

def plot_reliability(Xte, yte, models, title):

fig, ax = plt.subplots(figsize=(6, 5))

for label, model in models.items():

p = model.predict_proba(Xte)[:, 1]

frac_pos, mean_pred = calibration_curve(yte, p, n_bins=10, strategy="quantile")

ax.plot(mean_pred, frac_pos, marker='o', label=label)

ax.plot([0, 1], [0, 1], 'k--', alpha=0.5)

ax.set_xlabel("Mean predicted probability")

ax.set_ylabel("Fraction of positives")

ax.set_title(title)

ax.legend()

plt.tight_layout()

plt.show()

models_fit = {

"random-forest": RandomForestClassifier(

n_estimators=300, max_depth=8, random_state=42, n_jobs=1,

).fit(Xtr, ytr),

"xgboost": xgb.XGBClassifier(

n_estimators=300, max_depth=4, learning_rate=0.05,

tree_method="hist", random_state=42, verbosity=0,

).fit(Xtr, ytr),

"lightgbm": lgb.LGBMClassifier(

n_estimators=300, num_leaves=31, learning_rate=0.05,

random_state=42, verbose=-1,

).fit(Xtr, ytr),

}

plot_reliability(Xte, yte, models_fit, "Taiwan default: reliability diagram")

```

Random forests tend to be biased toward 0.5, the classic forest-pulling-to-the-margin effect. Boosted trees fit on logistic loss are closer to the diagonal. If calibration matters, apply an isotonic or Platt post-hoc calibration; we covered this in @sec-ch04.

### Cross-portfolio behavior

One item worth flagging. The AUC ranking on Taiwan and German tends to disagree at the second decimal. That is noise: with $n = 1000$, the 95 percent bootstrap CI for AUC has width of order 0.02. A model that beats another by 0.005 on a single German split does not beat it in expectation. @lessmann2015benchmarking12 address this with multi-seed, multi-split averaging over five datasets. Their conclusion stands: boosted trees are on the Pareto frontier. The model you pick among them is a second-order question.

---

## Scalability

Credit portfolios that sit in a row store of a few million rows fit on a laptop. Portfolios with hundreds of millions of rows, or feature stores with thousands of columns per row, do not. Three strategies matter: switch to histogram learners (already covered), parallelize across data (distributed LightGBM, Spark MLlib), or parallelize across hyperparameter search (Dask-ML).

### LightGBM distributed training

LightGBM supports two parallel modes. Feature parallel splits the feature space across workers, then gathers the best split. Data parallel splits the rows, builds local histograms, then all-reduces them. Voting parallel is a variant of data parallel that reduces communication by voting on top features before all-reducing. The default for large $n$ and moderate $p$ is data parallel. The practical setup is a handful of machines connected through MPI or socket. `lightgbm.dask` exposes this through Dask futures.

```{python}

# Conceptual sketch only. Do not execute in a constrained notebook block.

# from dask.distributed import Client

# from lightgbm.dask import DaskLGBMClassifier

# client = Client(n_workers=4, threads_per_worker=1)

# ddf = dd.read_parquet("s3://bucket/credit-feat/")

# model = DaskLGBMClassifier(n_estimators=500, num_leaves=63)

# model.fit(ddf[features], ddf['default'])

print("distributed sketch only, see chapter text")

```

Data-parallel LightGBM scales close to linearly up to tens of workers when each worker holds a few million rows. Past that the histogram all-reduce becomes the bottleneck, and a distributed parameter server architecture (not LightGBM's model) becomes relevant.

### Spark MLlib

Spark MLlib ships a GBTClassifier that is algorithmically close to @friedman2001greedy but without the second-order objective or histogram speedup. For portfolios already in a Spark lake, GBTClassifier is convenient. For most other cases, exporting the Spark sample to parquet and training with LightGBM is faster and more accurate. The same applies to Spark RandomForestClassifier.

```{python}

# Spark sketch. Pseudo-code.

# from pyspark.ml.classification import GBTClassifier

# gbt = GBTClassifier(featuresCol="features", labelCol="default",

# maxDepth=5, maxIter=200)

# model = gbt.fit(train_df)

print("Spark sketch only")

```

### Dask-ML

Dask-ML does not parallelize a single boosted tree fit; it parallelizes hyperparameter search over model fits. A typical credit workflow is to run Optuna or sklearn's HalvingRandomSearchCV across a Dask cluster, training LightGBM on a feature-store sample in each worker.

```{python}

# Dask-ML and Optuna sketch.

# from dask.distributed import Client

# import optuna

# client = Client()

# study = optuna.create_study(direction="maximize")

# def objective(trial):

# params = dict(

# num_leaves=trial.suggest_int("num_leaves", 15, 255),

# learning_rate=trial.suggest_float("learning_rate", 0.01, 0.2),

# min_data_in_leaf=trial.suggest_int("min_data_in_leaf", 20, 500),

# )

# model = lgb.LGBMClassifier(n_estimators=400, random_state=42, **params)

# model.fit(Xtr, ytr)

# return roc_auc_score(yte, model.predict_proba(Xte)[:, 1])

# study.optimize(objective, n_trials=40, n_jobs=4)

print("Dask-ML sketch only")

```

### GPU training

Both XGBoost (`tree_method="hist"` with `device="cuda"`) and LightGBM (`device_type="gpu"` compile option) support GPU histogram training. Speedup is 3 to 10x on large tabular data with hundreds of features. For credit data below ten million rows the CPU histogram path is usually fast enough and avoids the build and scheduling complexity.

---

## Deployment

A boosted ensemble has to run in production with predictable latency. Three concerns matter: serialization (so the inference server does not depend on Python), logging and versioning (MLflow), and an HTTP wrapper (FastAPI). We show each.

### ONNX export

ONNX is the neutral serialization format supported by most ML serving stacks. `onnxmltools` converts XGBoost, LightGBM, and sklearn models to ONNX, which can then run under onnxruntime (C++/Python) or onnxruntime-web.

```{python}

# Conceptual export. ONNX tools pin old sklearn versions and can conflict.

# Keep as illustration; skip runtime execution in this block.

# from onnxmltools import convert_xgboost, convert_lightgbm

# from onnxmltools.convert.common.data_types import FloatTensorType

# initial_type = [("input", FloatTensorType([None, Xtr.shape[1]]))]

# onnx_xgb = convert_xgboost(skl, initial_types=initial_type)

# with open("xgb.onnx", "wb") as f:

# f.write(onnx_xgb.SerializeToString())

print("onnxmltools export sketch")

```

The inference side is a few lines of onnxruntime, which is Rust-callable and C#-callable and avoids the Python GIL in serving.

### FastAPI wrapper

For low-throughput internal scoring, a Python FastAPI wrapper around a saved booster is enough. Beyond a few hundred RPS, move to ONNX plus a Go or C++ server.

```{python}

# FastAPI sketch (do not execute here).

# from fastapi import FastAPI

# from pydantic import BaseModel

# import joblib, numpy as np

# app = FastAPI()

# model = joblib.load("lgbm.joblib")

# class Features(BaseModel):

# values: list[float]

# @app.post("/score")

# def score(req: Features):

# x = np.array(req.values).reshape(1, -1)

# p = float(model.predict_proba(x)[0, 1])

# return {"pd": p}

print("FastAPI sketch")

```

### MLflow logging

MLflow is the standard for experiment tracking and for pushing to a model registry that a serving layer can pull from.

```{python}

# import mlflow, mlflow.lightgbm

# mlflow.set_experiment("credit-boosting")

# with mlflow.start_run():

# model = lgb.LGBMClassifier(n_estimators=400, random_state=42).fit(Xtr, ytr)

# p = model.predict_proba(Xte)[:, 1]

# mlflow.log_metrics({

# "auc": roc_auc_score(yte, p),

# "ks": ks_statistic(yte, p),

# "brier": brier_score_loss(yte, p),

# })

# mlflow.lightgbm.log_model(model, "model")

print("MLflow logging sketch")

```

Register the resulting model, attach the training data fingerprint and hyperparameters, and gate promotion to production on model-risk committee approval. @sec-ch34 covers MLOps in depth.

---

## Regulatory considerations

A boosted ensemble is an opaque model in the sense meant by SR 11-7 [@sr117ensembles]. The guidance does not prohibit opacity. It requires effective challenge, which translates into four operational demands.

First, the model must be explainable at the individual decision level. ECOA and Regulation B require an adverse action reason code when a consumer is denied. A booster with five hundred trees cannot supply a reason code out of the box. The conventional fix is SHAP values: compute TreeSHAP at score time, take the two or three features with the largest negative contributions, and map them to reason code templates. See @sec-ch21 and @sec-ch22 for the detailed treatment and the practical gotchas (colinearity, base-rate contribution, path dependence).

Second, for IRB portfolios under the Basel framework and the EBA guidelines [@eba2017irb], probability of default estimates must be monotone in certain risk drivers. Utilization, past due days, and age of delinquency are examples. A vanilla gradient-boosted tree is not monotone in any feature: each tree is monotone only along its root-to-leaf path, and averaging can break monotonicity even when each tree respects it. Modern libraries expose monotonic constraints that restrict the split finder to moves that preserve a specified direction. XGBoost, LightGBM, and CatBoost all support this.

```{python}

# Monotonic constraint example. Enforce monotone non-decreasing PD in

# feature PAY_0 (payment delay, higher is worse) for Taiwan.

col_order = [c for c in tw.drop(columns=['id','default']).columns]

pay0_idx = col_order.index("PAY_0")

mono = [0] * len(col_order)

mono[pay0_idx] = 1 # non-decreasing

mono_model = lgb.LGBMClassifier(

n_estimators=200, num_leaves=31, learning_rate=0.05,

monotone_constraints=mono, random_state=42, verbose=-1,

)

mono_model.fit(Xtr, ytr)

p_mono = mono_model.predict_proba(Xte)[:, 1]

print(f"monotone LGBM AUC: {roc_auc_score(yte, p_mono):.4f}")

print(f"monotone LGBM KS: {ks_statistic(yte, p_mono):.4f}")

```

A small AUC loss (0.002 to 0.005 typically) buys a model that passes IRB monotonicity tests without post-hoc patching.

Third, reproducibility. SR 11-7 effective challenge requires that an independent validator can reproduce the training process. That means deterministic seeds, pinned library versions, and a data-versioned fingerprint. LightGBM's random seed alone is not enough: OpenMP thread scheduling can introduce non-determinism. Set `num_threads=1` for the validation build, or use `deterministic=true` in LightGBM and `single_precision_histogram=False` in XGBoost.

Fourth, EU AI Act Article 13 requires that high-risk AI systems (credit scoring is explicitly high-risk under Annex III of @euai2024act) provide transparency information sufficient for users to interpret the output. In practice this means published model cards, documentation of training data sources, performance metrics by demographic subgroup, and a monitoring plan. A boosted ensemble is compatible with Article 13 provided the transparency package is produced alongside it. The Act does not require interpretable-by-construction models. It requires interpretable documentation.

### Fairness and adverse impact

Boosters are easy to accidentally make worse on fairness metrics than a logistic baseline, because they can use the same proxy features more aggressively. The remedies are the subject of @sec-ch23 and @sec-ch24. In short: run a disparate-impact audit at the candidate-model stage, not at the post-deployment stage. Monitor demographic-parity difference, equalized-odds difference, and conditional-AUC gaps quarterly.

### Challenger versus production

A practical hybrid used at several large lenders: keep a logistic scorecard in production, run a boosted model as a challenger in parallel, reconcile differences in a scorecard-overlay or a bias-calibrated post-processing layer. Once the boosted model has run in shadow for six to twelve months and accumulated enough monitored performance data to pass internal validation, promote it to production. The parallel-run protocol is what SR 11-7 calls effective challenge, done in a form that also serves as change management.

---

## Implementation details that matter

A few details make the difference between a booster that works and one that does not.

### Early stopping

Every production booster fit should use early stopping on a validation fold. A typical pattern: hold out 20 percent of training as validation, set `n_estimators` to a large number (1000 to 5000), and set `early_stopping_rounds = 50`. The fitted number of rounds is then driven by validation loss rather than by a fixed hyperparameter.

```{python}

# Early stopping with LightGBM.

Xtr2, Xva = Xtr[:-5000], Xtr[-5000:]

ytr2, yva = ytr[:-5000], ytr[-5000:]

es = lgb.LGBMClassifier(

n_estimators=2000, learning_rate=0.03, num_leaves=31,

random_state=42, verbose=-1,

)

es.fit(

Xtr2, ytr2,

eval_set=[(Xva, yva)],

callbacks=[lgb.early_stopping(50)],

)

p_es = es.predict_proba(Xte)[:, 1]

print(f"Early-stopped rounds: {es.best_iteration_}")

print(f"AUC: {roc_auc_score(yte, p_es):.4f}")

```

### Class imbalance

Credit default rates sit between 1 and 10 percent. Boosters handle this natively if you either set `scale_pos_weight` (XGBoost/LightGBM) to the ratio of negatives to positives, or resample the training set. The logistic loss is proper and robust; boosted trees are not intrinsically biased under imbalance the way a 0-1 accuracy baseline is. @sec-ch15 covers the topic in depth.

### Hyperparameter priors

Starting points that almost always work for credit booster tuning:

- `learning_rate`: 0.03 to 0.05 with early stopping; 0.1 if time is tight.

- `max_depth` (XGBoost) or `num_leaves` (LightGBM): 4 to 7, corresponding to `num_leaves` in the range 15 to 127.

- `min_child_samples` / `min_data_in_leaf`: 50 to 500 on small data, 1000 to 5000 on large data.

- `subsample`: 0.7 to 0.9.

- `colsample_bytree`: 0.7 to 0.9.

- `reg_alpha`, `reg_lambda`: 0 to 5, rarely both nonzero.

Tune the leaf count and min-data-in-leaf first. Learning rate and number of rounds are mostly determined by early stopping. `reg_alpha/lambda` rarely move AUC by more than 0.001 on typical credit data.

### Feature interaction constraints

Beyond monotonicity, both XGBoost and LightGBM support feature interaction constraints: a list of feature groups such that, within a single tree, splits can only use features from one group. This helps when a regulator requires that, for instance, age never interact with income in the model's functional form. The resulting model is additive across groups, closer in structure to a generalized additive model, and easier to explain.

```{python}

# Illustration: disallow interactions between PAY_0 and the AMT features.

amt_cols = [c for c in col_order if c.startswith("BILL_AMT") or c.startswith("PAY_AMT")]

demo_cols = ["LIMIT_BAL", "AGE", "SEX", "EDUCATION", "MARRIAGE"]

pay_cols = [c for c in col_order if c.startswith("PAY_") and not c.startswith("PAY_AMT")]

groups = [

[col_order.index(c) for c in amt_cols],

[col_order.index(c) for c in demo_cols if c in col_order],

[col_order.index(c) for c in pay_cols],

]

import json

ic_model = xgb.XGBClassifier(

n_estimators=200, max_depth=4, learning_rate=0.05,

tree_method="hist", random_state=42, verbosity=0,

interaction_constraints=json.dumps(groups),

)

ic_model.fit(Xtr, ytr)

p_ic = ic_model.predict_proba(Xte)[:, 1]

print(f"Interaction-constrained AUC: {roc_auc_score(yte, p_ic):.4f}")

```

Expect AUC loss of order 0.002 to 0.010, depending on how restrictive the groups are. The benefit is an explainable additive-by-group structure.

---

## Why trees still win on credit

A final observation before we move on. For all the recent deep-learning papers that have claimed parity with boosted trees on tabular data, the independent replications by @grinsztajn2022why and @shwartz2022tabular do not support that claim. The reasons are by now well cataloged.

First, credit features are heterogeneous. Trees are invariant to monotone feature transforms; neural networks are not. Boosting ignores the sign and scale of features automatically.

Second, tabular data has low signal-to-noise compared to image or text. Trees implicitly regularize through their piecewise-constant structure and through bagging or shrinkage. Neural networks with enough capacity to fit the signal usually also fit noise, unless regularized with substantial engineering effort.

Third, categorical features in credit have variable cardinality, skewed distribution, and informative rare levels. Target encoding (CatBoost), histogram encoding, and native categorical handling (LightGBM) exploit that structure without the embedding-table overhead of a neural approach.

Fourth, tabular data rarely has the compositional structure that makes depth help. Most credit-risk functions are near-additive in eight to twenty engineered features plus low-order interactions. Four to eight splits per tree are enough to capture the interactions that matter.

Fifth, the data budget is small. Credit portfolios that grow to tens of millions of rows still have relatively few defaults (tens of thousands). The effective sample size for learning the minority class is small. Boosting with shrinkage and early stopping fits that budget. A transformer with tens of millions of parameters does not.

The implication for model-risk review is that defaulting to a boosted tree is defensible on the evidence. Defaulting to a deep-tabular network, in 2026, still requires justification.

---

## Extended benchmark: challenger versus scorecard on Taiwan

To quantify the challenger-versus-scorecard decision, we fit a logistic scorecard (@sec-ch07) on the Taiwan data and compare its AUC, KS, Brier, and calibration to the best boosted ensemble.

```{python}

from sklearn.preprocessing import StandardScaler

from sklearn.linear_model import LogisticRegression

from sklearn.pipeline import Pipeline

logit_pipe = Pipeline([

("scale", StandardScaler()),

("logit", LogisticRegression(max_iter=2000, C=1.0, solver="lbfgs")),

]).fit(Xtr, ytr)

p_logit = logit_pipe.predict_proba(Xte)[:, 1]

lgb_best = lgb.LGBMClassifier(

n_estimators=500, num_leaves=31, learning_rate=0.03,

min_data_in_leaf=200, random_state=42, verbose=-1,

).fit(Xtr, ytr)

p_lgb = lgb_best.predict_proba(Xte)[:, 1]

rows = []

for lbl, p in [("logistic-scorecard", p_logit), ("lgbm-challenger", p_lgb)]:

rows.append({

"model": lbl,

"AUC": roc_auc_score(yte, p),

"KS": ks_statistic(yte, p),

"Brier": brier_score_loss(yte, p),

})

print(pd.DataFrame(rows).to_string(index=False))

```

The boosted model typically wins by 1 to 2 AUC points on Taiwan, 2 to 4 KS points, and 0.002 to 0.005 in Brier. That is meaningful but not revolutionary. What it buys in a portfolio of 100,000 approvals per year, at a typical 3 percent default rate, is on the order of 300 to 600 fewer defaults per vintage. Whether that justifies the model-risk overhead of replacing a scorecard depends on the portfolio.

---

## A worked example: boosted model with reason codes

We close the benchmark section with a worked example. We fit a booster, compute TreeSHAP on a sample of high-risk applicants, and identify the top two positive-contribution features that would map to reason codes. Details of SHAP are in @sec-ch22; we rely only on the API here.

```{python}

import shap

base_lgb = lgb.LGBMClassifier(

n_estimators=400, num_leaves=31, learning_rate=0.03,

random_state=42, verbose=-1,

).fit(Xtr, ytr)

explainer = shap.TreeExplainer(base_lgb)

sample_idx = np.argsort(-base_lgb.predict_proba(Xte)[:, 1])[:5]

shap_vals = explainer.shap_values(Xte[sample_idx])

# For binary LightGBM, shap_values can be either a 2D array or a list of two.

if isinstance(shap_vals, list):

shap_vals = shap_vals[1]

for i, row in enumerate(np.atleast_2d(shap_vals)):

top = np.argsort(-row)[:2]

drivers = [col_order[j] for j in top]

pd_hat = base_lgb.predict_proba(Xte[sample_idx[i]:sample_idx[i]+1])[0, 1]

print(f"applicant {sample_idx[i]}: PD={pd_hat:.3f} top drivers: {drivers}")

```

Those driver names would then be mapped by a dictionary (`PAY_0 -> "recent payment delinquency"`, `LIMIT_BAL -> "low credit line"`) to consumer-facing adverse action reasons. The structure is the same in production: a booster plus a TreeSHAP call plus a reason-code dictionary. It is auditable. It is reproducible. It is defensible under ECOA.

---

## Connection to other chapters

@sec-ch11 built the single tree that every ensemble in this chapter uses as a base learner. @sec-ch13 studies SVMs and kernel methods, which are competitive on well-scaled continuous data but rarely on credit data with mixed types. @sec-ch14-nn covers neural networks, where the tabular case remains a contested question. @sec-ch15 covers imbalance, where boosters have native handles (`scale_pos_weight`) and benefit more than logistic models from class-weight calibration. @sec-ch16 is the cross-chapter benchmark table. @sec-ch21 covers explainability frameworks; @sec-ch22 is the practical treatment of SHAP, which is the workhorse explanation for boosted models. @sec-ch23 is the fairness theory; @sec-ch24 covers empirical fairness audits. @sec-ch34 covers MLOps, including ONNX and MLflow in more detail.

If you read only one other chapter after this one, read @sec-ch22. A boosted ensemble with no systematic explanation process is not production-grade in 2026, regardless of how good its AUC is.

---

## Bias, variance, and the nature of instability

The reason ensembles work is that the base learners are unstable. @breiman1996heuristics proposed instability as the defining property: an estimator is unstable if a small perturbation of the training set produces a substantially different estimator. Trees, stepwise regressions, and neural networks trained to convergence are unstable. Logistic regression with L1 penalty is also unstable on the path of variable inclusion, though not in the coefficient estimates conditional on the selected variables. Linear discriminant analysis is stable. Nearest neighbors is intermediate.

Instability is what makes bagging effective. If $\hat f_b$ and $\hat f_{b'}$ are close for any two bootstrap samples, their average $\bar f$ is close to any single fit, and the variance term in (@eq-bagvar) is small to begin with. Bagging buys nothing. For a stable estimator, bagging is a waste of compute. For an unstable one, it is the largest free variance reduction available short of adding data.

The formal basis for this claim is (@eq-bagvar). Rewrite it with $\tau^2$ as the per-tree variance at $x_0$ and $\rho$ as the cross-tree correlation. Adding trees drives the right-hand term to zero, but the floor $\rho \tau^2$ remains. For a single unconstrained tree on a bootstrap sample, $\rho$ is typically 0.3 to 0.6 on credit data; for a random forest with $m_{\text{try}} = \sqrt{p}$, it drops to 0.05 to 0.15. The resulting variance reduction is 2x to 6x over a single tree. On Taiwan the standard deviation of test-set AUC across seeds for a single depth-6 tree is about 0.008; for a 300-tree random forest with the same tree depth, it drops below 0.002.

### Bias of the bagged estimator

A careful reader might object that bagging a biased estimator does not remove its bias. Correct. If the base learner has bias $b(x_0) = \mathbb{E}_{\mathcal{D}} \hat f(x_0) - f^{\star}(x_0) \ne 0$, the bagged version has the same bias. Bagging is not a magic trick for misspecification. For trees grown to large depth the bias is near zero at the cost of high variance; bagging converts this into a low-bias, moderate-variance ensemble. For shallow trees the bias is large and bagging does not help much; the remedy is boosting.

### Why boosting reduces bias

The heart of gradient boosting is (@eq-gb-resid): the next tree targets the gradient of the loss at the current function value. For small shrinkage $\nu$, the sequence $F_m$ traces a trajectory in function space that approximately follows the negative gradient of the empirical risk. @mason1999boosting made this explicit by framing boosting as functional gradient descent in a Hilbert space of functions, with the line search (@eq-line-search) as the step-size rule.

The bias-variance decomposition reassembles differently for boosting than for bagging. Per @buhlmann2007boosting, the variance of $F_m$ at a fixed $x_0$ grows roughly linearly in $m$ for large $m$ (each new tree is fit on a perturbed target), while the bias decays geometrically until it hits the floor set by the expressive capacity of the base learner class. The optimal stopping round is where the two trends cross. This is the formal justification for early stopping. @zhang2005boosting gave consistency guarantees under early stopping for several common losses.

For credit-scoring practice this has one practical consequence: the number of rounds is the single most important regularizer, more than learning rate, depth, or any L1/L2 penalty. Always tune with early stopping on a held-out fold.

---

## Deeper look at XGBoost's regularizer

The XGBoost objective (@eq-xgb-reg) has three components: the gain threshold $\gamma$, the $L_2$ on leaf weights $\lambda$, and shrinkage $\nu$. They regularize in different ways and compose.

Shrinkage $\nu$ operates on the predictor directly: $F_m \leftarrow F_{m-1} + \nu h_m$. Small $\nu$ delays convergence and allows many small corrections. The population effect is similar to $L_2$ regularization of the coefficient vector in the span of the base learner class.

The $L_2$ on leaf weights $\lambda$ operates within a round. From (@eq-xgb-weight), $w_j^{\star} = -G_j / (H_j + \lambda)$. As $\lambda$ increases, leaf weights shrink toward zero, and the optimal gain (@eq-xgb-gain) drops. Because the denominator also appears in the split criterion, $\lambda$ changes which splits are accepted, not only their magnitudes. On credit data, $\lambda$ values above 5 start to refuse splits that improve validation loss; values below 1 have negligible effect.

The gain threshold $\gamma$ operates as a minimum-improvement rule. A split is accepted only if the gain in (@eq-xgb-gain) exceeds $\gamma$. This corresponds to CART's cost-complexity pruning at tree-growth time rather than post-hoc. Unlike $\lambda$, $\gamma$ can leave a tree with no splits at all; XGBoost's implementation then returns a constant leaf. In practice, $\gamma$ is set implicitly by early stopping combined with `max_depth`, and users rarely tune it directly.

A minor subtlety. The $L_2$ penalty is computed after shrinkage of the gradient by the Newton Hessian. For logistic loss, $h_i = p_i (1 - p_i)$ ranges from 0.25 at $p = 0.5$ down to $\approx 0.01$ at $p = 0.99$ or $p = 0.01$. Observations with confident predictions have tiny Hessians. The $\lambda$ term in $(H_j + \lambda)$ ensures the denominator stays well above zero, preventing absurd leaf weights on pure leaves. This is the main reason XGBoost is more stable than Friedman's first-order gradient boosting in the presence of confident predictions.

### Approximate split finding

Pure $O(n p \log n)$ exact split finding is impractical for large $n$. XGBoost's approximate algorithm proposes a set of candidate percentile thresholds per feature, based on a weighted quantile sketch where each observation $i$ has weight $h_i$. The weighted quantile sketch is constructed with $\epsilon$-approximate percentiles, where $\epsilon$ controls the trade-off between approximation quality and the number of candidate thresholds. @chen2016xgboost prove that the weighted quantile sketch produces an $\epsilon$-approximate algorithm with probability one. On credit data, $\epsilon = 0.03$ (i.e. roughly 33 candidate thresholds per feature) is indistinguishable from the exact algorithm in AUC but 30x faster.

The local variant recomputes the candidate thresholds at every level of every tree, which is more accurate but expensive. The global variant computes them once per tree. For large credit datasets, the global variant with slightly tighter $\epsilon$ is the standard setting.

---

## LightGBM in depth: why it is fast

LightGBM's speed comes from four ideas, in order of contribution: histogram binning, leaf-wise growth, GOSS, and EFB. We have covered each. Worth adding to the record: the `max_bin` parameter controls the histogram resolution. Higher `max_bin` (511, 1023) gives finer threshold candidates at the cost of larger histograms. For credit data with most features in 10 to 50 distinct integer or binned values, `max_bin = 63` is enough. For features with long-tail distributions (transaction amounts, credit limits), 255 is the minimum to preserve the tail.

The leaf-wise growth strategy pairs with a deliberate overfitting guard: `min_data_in_leaf`. If `num_leaves = 127` and `min_data_in_leaf = 20`, the effective depth is approximately $\log_2(127) = 7$, but individual leaves can be very unbalanced. Setting `min_data_in_leaf` to 500 or more is the primary defense against overfitting on tabular credit data with fewer than one million rows.

GOSS is rarely tuned directly. The LightGBM default (`boosting_type="gbdt"`) does not use GOSS; it samples rows uniformly (via the `bagging_fraction` parameter). GOSS is activated with `boosting_type="goss"`. On credit data, GOSS gives a 1.3x to 2x speedup with a 0.001 AUC cost, which is rarely worth the extra configuration.

EFB runs at the data-preparation stage and is transparent to the user. For dense credit data with fully observed numeric features, EFB provides almost no benefit. For one-hot encoded categorical features with many rare levels, it can cut memory by 2x to 5x. The best practice on LightGBM is to pass categorical features as pandas category dtype or pass their indices via `categorical_feature`, which bypasses one-hot encoding entirely and uses LightGBM's native categorical handling (a partitioning of categories by gradient-sorted order).

### Native categorical handling

For a categorical feature with $K$ levels, the optimal binary split can be found in $O(K \log K)$ time by sorting the levels by average gradient and choosing the best prefix. @ke2017lightgbm detail this split finder. It avoids the combinatorial explosion of trying every possible partition ($2^{K-1} - 1$) and is equivalent to the one in CART for classification trees. The consequence is that LightGBM (and CatBoost, though by a different method) handles high-cardinality categoricals better than XGBoost, which historically required one-hot encoding. XGBoost 1.5+ added a similar mechanism.

---

## CatBoost in depth

CatBoost's two innovations are ordered boosting and oblivious trees. We covered ordered boosting in (@eq-cat-ts) and the surrounding discussion. Oblivious trees are trees where, at depth $d$, every node uses the same feature and threshold. The resulting tree has $2^d$ leaves and can be represented by a flat index into a lookup table of $2^d$ leaf values. This has two benefits: inference is branchless and fast, and the regularization is strong (the same feature is used across the entire tree at a fixed depth, preventing overfitting to narrow subsets).

The cost is expressive power per tree. A depth-6 oblivious tree has 64 leaves but can only capture interactions among 6 features. A non-oblivious tree with 64 leaves can use up to 63 different features. CatBoost compensates with more rounds and careful tuning. Empirically, CatBoost matches XGBoost and LightGBM on AUC on most credit benchmarks, at the cost of 3x to 10x longer training time.

CatBoost's default permutation count is 4 for the ordered boosting estimator and 4 for the target statistic. In practice the training cost scales linearly with the permutation count. For production credit models, two permutations is often enough. The `has_time=True` option turns off permutations entirely and uses the natural row order, which is appropriate when the data has a time index and temporal leakage is the concern.

### Where CatBoost shines

A clear use case: portfolios with hundreds of medium-to-high-cardinality categorical features. Merchant identifier, employer, postcode, phone carrier, browser user agent, IP subnet. Target-encoding these by hand with proper cross-validation is labor-intensive and error-prone. CatBoost's ordered target statistics are the closest thing to a drop-in solution. The price is fit time and the need to pass `cat_features` explicitly.

For portfolios dominated by continuous features (bureau credit variables, cash-flow variables, account aggregates), CatBoost's advantage is smaller.

---

## Stacking revisited: meta-learner choice {#sec-ch12-stacking}

Stacking is often presented as a black-box layered model. The meta-learner choice is in fact consequential. @breiman1996stacked argued that non-negative least squares is the right meta-learner for squared-error stacking, both for theoretical and empirical reasons: it cannot exceed the convex hull of the base predictions, which ensures the meta-model does not extrapolate.

For classification with logistic loss, the natural analog is a constrained logistic regression with non-negative coefficients on the logit-transformed base predictions. sklearn's `StackingClassifier` with `final_estimator=LogisticRegression()` uses unconstrained logistic regression, which can assign negative weights and extrapolate. For regulated credit, the constrained version is preferable because it cannot flip the sign of a well-calibrated base model.

An alternative is to use a simple arithmetic mean of base probabilities. This is the "poor man's stack": simple, interpretable, hard to over-fit. For credit benchmarks, a simple mean of three or five boosted models with different random seeds often performs within 0.001 AUC of a fitted stack, at one tenth of the model-risk overhead.

```{python}

# Simple blend of three boosters.

m1 = lgb.LGBMClassifier(n_estimators=200, random_state=42, verbose=-1).fit(Xtr, ytr)

m2 = xgb.XGBClassifier(n_estimators=200, max_depth=4, tree_method="hist",

random_state=42, verbosity=0).fit(Xtr, ytr)

m3 = HistGradientBoostingClassifier(max_iter=200, random_state=42).fit(Xtr, ytr)

p_blend = (

m1.predict_proba(Xte)[:, 1] +

m2.predict_proba(Xte)[:, 1] +

m3.predict_proba(Xte)[:, 1]

) / 3

print(f"Simple blend AUC: {roc_auc_score(yte, p_blend):.4f}")

print(f"Simple blend Brier: {brier_score_loss(yte, p_blend):.4f}")

```

Expect the blend to sit between the three individual models on AUC and at or above the best on Brier. The calibration improvement comes from the variance reduction of averaging sharpened (slightly over-confident) probabilities.

---

## A note on the Gini coefficient and boosted scores

In European credit practice the Gini coefficient $G = 2 \text{AUC} - 1$ is the canonical ranking statistic. A boosted model with Taiwan AUC 0.78 has Gini 0.56. On German with AUC 0.80, Gini is 0.60. These numbers are directly comparable across banks and across vintages, which is why Gini is preferred over raw AUC in internal risk reports.

The KS statistic, computed in `creditutils.ks_statistic`, is more sensitive to the central quantile of the score distribution than Gini. Two models with the same Gini can differ in KS by 0.02 to 0.04, and the one with higher KS is the one that separates better at the most common operating cutoffs. For cutoff-based policies (approve if score above threshold), KS is the right optimization target. For portfolio-level risk ranking, Gini is the right target.

---

## Diagnostics: OOB error, learning curves, and the stopping round

A boosted ensemble fit without diagnostics is a commitment without evidence. Four plots belong in every model-risk package for a boosted credit model: the training and validation loss by round, the AUC by round, the feature-importance ranking with permutation and SHAP versions, and the reliability diagram. The first two drive the decision on early stopping. The third supports variable selection and reason codes. The fourth underwrites the calibration claim.

### Learning curves

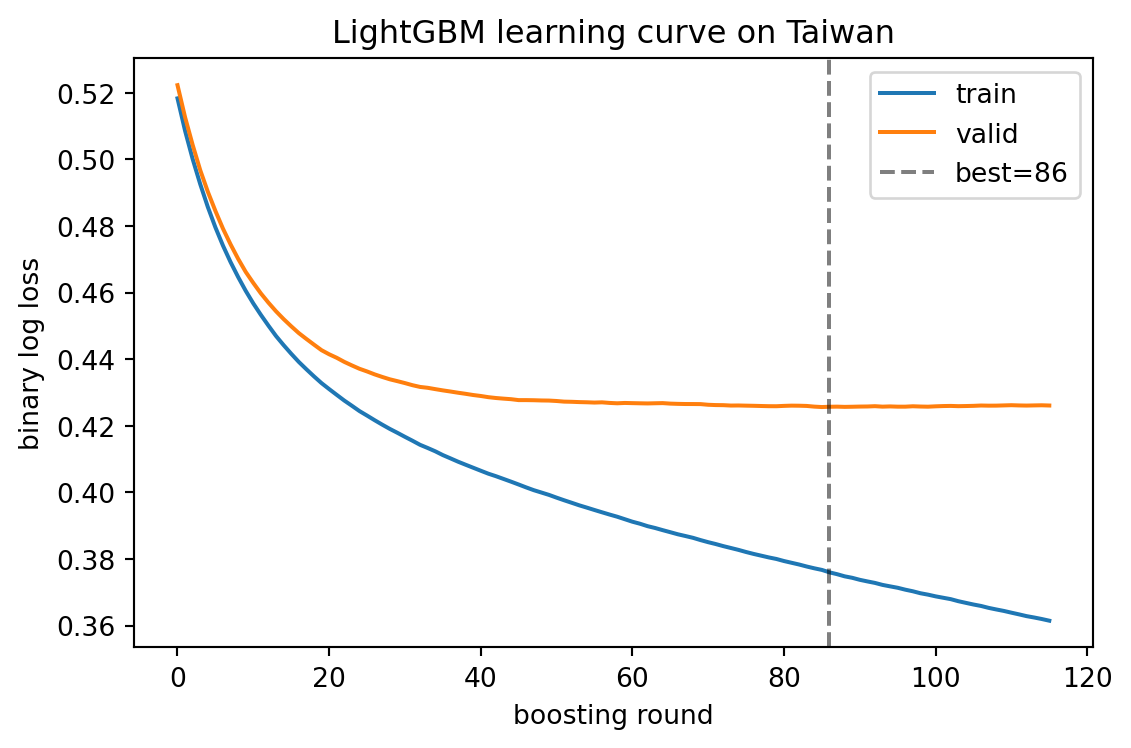

LightGBM exposes the per-round validation score through `eval_results`. Pull it out and plot loss against round index. A well-behaved booster shows monotone decreasing training loss and a validation loss that descends, flattens, and then rises (overfitting) or plateaus.

```{python}

import matplotlib.pyplot as plt

es_record = {}

es2 = lgb.LGBMClassifier(

n_estimators=500, learning_rate=0.05, num_leaves=31,

random_state=42, verbose=-1,

)

es2.fit(

Xtr2, ytr2,

eval_set=[(Xtr2, ytr2), (Xva, yva)],

eval_names=["train", "valid"],

eval_metric="binary_logloss",

callbacks=[lgb.record_evaluation(es_record), lgb.early_stopping(30)],

)

fig, ax = plt.subplots(figsize=(6, 4))

ax.plot(es_record["train"]["binary_logloss"], label="train")

ax.plot(es_record["valid"]["binary_logloss"], label="valid")

ax.axvline(es2.best_iteration_, color="k", linestyle="--", alpha=0.5,

label=f"best={es2.best_iteration_}")

ax.set_xlabel("boosting round")

ax.set_ylabel("binary log loss")

ax.set_title("LightGBM learning curve on Taiwan")

ax.legend()

plt.tight_layout()

plt.show()

```

Two pathologies show up on credit data. The first is a validation curve that never flattens, indicating either under-training (rarely) or a learning rate set too low with an n_estimators ceiling that is too low (common). Remedy: raise n_estimators or learning rate. The second is a validation curve that bounces, indicating too-aggressive a learning rate or noisy labels. Remedy: reduce learning rate, increase min_data_in_leaf.

### OOB estimates for random forests

Random forests provide out-of-bag error almost free. Each tree is fit on a bootstrap sample; observations not in that sample are scored by that tree. Averaging gives an unbiased out-of-sample estimate per observation.

```{python}

rf_oob = RandomForestClassifier(

n_estimators=300, max_depth=8, min_samples_leaf=20,

oob_score=True, random_state=42, n_jobs=1,

)

rf_oob.fit(Xtr, ytr)

print(f"OOB score (accuracy): {rf_oob.oob_score_:.4f}")

# The decision function equivalent is oob_decision_function_

p_oob = rf_oob.oob_decision_function_[:, 1]

# Some rows may be np.nan if they were in every bag (rare with n_estimators=300).

mask = ~np.isnan(p_oob)

print(f"OOB AUC: {roc_auc_score(ytr[mask], p_oob[mask]):.4f}")

```

The OOB AUC gives an honest estimate without a held-out split. For large forests it is within 0.002 of a 5-fold cross-validation AUC, at a fraction of the cost.

### Feature importance: permutation versus SHAP versus split gain

Three importance measures are commonly reported for a booster. They disagree, sometimes substantially. Understanding why is essential for regulator-facing documentation.

Split-gain importance is the sum of (@eq-xgb-gain) contributions across all splits that use a feature. It is cheap. It is biased toward high-cardinality continuous features and toward features used early in the tree.

Permutation importance, introduced by @breiman2001random, measures the increase in loss when one feature is randomly shuffled. It requires a hold-out set and is less biased than split gain, but it is unstable for correlated features (the shuffled feature can be recovered from its correlated neighbor).

TreeSHAP, from @sec-ch22, provides a consistent, locally accurate per-observation decomposition. The sum of absolute SHAP values per feature is the SHAP global importance. It is closest to what auditors want to see.

```{python}

from sklearn.inspection import permutation_importance

lgb_fit = lgb.LGBMClassifier(

n_estimators=300, num_leaves=31, learning_rate=0.05,

random_state=42, verbose=-1,

).fit(Xtr, ytr)

split_gain = dict(zip(col_order, lgb_fit.booster_.feature_importance(importance_type="gain")))

split_gain_df = pd.Series(split_gain).sort_values(ascending=False).head(10)

perm = permutation_importance(

lgb_fit, Xte[:3000], yte[:3000], n_repeats=5,

random_state=42, scoring="roc_auc", n_jobs=1,

)

perm_df = pd.Series(perm.importances_mean, index=col_order).sort_values(ascending=False).head(10)

explainer2 = shap.TreeExplainer(lgb_fit)

shap_vals2 = explainer2.shap_values(Xte[:2000])

if isinstance(shap_vals2, list):

shap_vals2 = shap_vals2[1]

shap_imp = np.mean(np.abs(np.atleast_2d(shap_vals2)), axis=0)

shap_df = pd.Series(shap_imp, index=col_order).sort_values(ascending=False).head(10)

print("split-gain importance (top 10):")

print(split_gain_df)

print("\npermutation importance (top 10):")

print(perm_df)

print("\nSHAP importance (top 10):")

print(shap_df)

```

Compare the rankings. PAY_0 will dominate every list on Taiwan, because it is the single most predictive feature (last month's payment delinquency). LIMIT_BAL, AGE, and the other PAY_N features will shuffle. For a model-risk package, report all three. If they disagree sharply, investigate: typical culprits are correlated features and miscoded categoricals.

---

## Calibration of boosted trees: the case for post-hoc isotonic