---

execute:

echo: true

eval: true

warning: false

---

# Data: Sources, Features, and Preprocessing {#sec-ch03}

::: {.callout-note appearance="simple" icon="false"}

**Scope: both retail and corporate, retail-leaning.** Bureau, application, transaction, and alternative-data sources. Worked examples lean retail (UCI German, Taiwan, CIC Vietnam); corporate financial-statement features are covered alongside.

:::

## Overview {.unnumbered}

Credit scoring lives or dies on its inputs. A logistic model trained on the wrong population, a gradient-boosted tree fit to leaky features, or a deep network that imputes missingness with a mean will all fail in production, and they will fail in ways that regulators care about. The modeling choices that textbooks emphasize matter. The data choices matter more.

This chapter takes data seriously. We walk through the traditional sources that sit inside a bank's scorecard, catalog the alternative signals that have appeared in the past decade, and formalize the preprocessing steps that translate raw tables into model-ready features. Three tools get most of the attention: (1) weight of evidence for monotone encoding, (2) imputation for missingness, and (3) time-aware splitting for leakage control. Each is worked out in math and in code that runs on the public UCI data sets.

The chapter also makes a scalability argument. A scorecard team that only thinks in pandas hits a wall at a few million rows. Polars, Dask, and Spark each solve a different piece of that wall, and weight of evidence encoding is one of the simplest places to show the tradeoff. The last section walks through a classic leakage bug, trains a model on it, and shows the out-of-time hit.

A note for the emerging-market reader. The data stack this chapter describes (bureau file, internal core-banking data, alternative overlays) looks different when the bureau is the Credit Information Center (CIC) rather than Experian, when roughly half the adult population has no tradeline, when declared income comes from cash work rather than payroll, and when the origination channel is a mobile app with an eKYC liveness check rather than a branch visit. The preprocessing decisions that follow, weight-of-evidence binning, missingness treatment, and point-in-time feature construction, have to absorb a higher missingness rate, a shorter tradeline depth, and a heavier reliance on transaction-level cash-flow features. The chapter's methods are the right methods, but the defaults (bin counts, IV thresholds, imputation strategy) need to be set with the thin-file population in mind.

The intended reader is a senior practitioner or an academic researcher who already understands logistic regression and classical statistical learning. The chapter spends no time re-deriving maximum likelihood for a linear model; it spends most of its time on the joins, the cohort definitions, and the pre-model transformations that separate a demonstration notebook from a production scorecard. The empirical sections lean on UCI German and UCI Taiwan because they are reproducible everywhere, but the methods port cleanly to larger Home Credit, LendingClub, and HMDA samples covered in later chapters.

### Notation {.unnumbered}

We use $X \in \mathcal{X}$ for features and $Y \in \{0, 1\}$ for the default label, with $Y = 1$ denoting a bad. Population rates are $\pi_1 = \Pr(Y = 1)$ and $\pi_0 = 1 - \pi_1$. A binned feature partitions $\mathcal{X}$ into disjoint bins $\{A_j\}_{j=1}^{J}$. For a categorical variable, bins are level groupings. For a numeric variable, bins are intervals. Conditional probabilities are $p_{j \mid 1} = \Pr(X \in A_j \mid Y = 1)$ and $p_{j \mid 0} = \Pr(X \in A_j \mid Y = 0)$.

```{python}

#| label: setup-imports

import sys, warnings, time

warnings.filterwarnings("ignore")

sys.path.insert(0, "../code")

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from creditutils import load_german_credit, load_taiwan_default, stable_sigmoid

rng = np.random.default_rng(42)

np.random.seed(42)

```

## Traditional data {#sec-ch03-data}

Banks have collected the same categories of consumer credit data for four decades. Little has changed in the core schema. The four pillars of a traditional retail scorecard are the bureau report (@sec-ch03-bureau), the bank's internal master file (@sec-ch03-internal), the application form (@sec-ch03-application), and the external overlay such as income verification or fraud flags (@sec-ch03-overlays).

### The bureau report {#sec-ch03-bureau}

A consumer credit bureau is a private clearinghouse. It ingests monthly tradeline updates from thousands of furnishers, normalizes them into a canonical schema, and sells reports and scores back to lenders. In the United States the three nationwide bureaus are Equifax, Experian, and TransUnion [@avery2003overview]. The Fair Credit Reporting Act (FCRA) governs what they can collect, how long they can keep it, and what consumers can dispute. Europe runs a mix of positive and negative bureaus by country. China operates the Credit Reference Center of the People's Bank of China alongside several private bureaus.

A bureau report breaks into five sections that every modern scorecard touches:

1. **Identification**: name, date of birth, social security or national identifier, current and prior addresses. Used to link the report to the application and to detect identity fraud.

2. **Tradelines**: one row per active or closed credit account. Each tradeline has an opening date, an account type (revolving, installment, mortgage, open), a credit limit or original balance, a current balance, a minimum payment, and a 24-month payment history string such as `OK OK OK 30 60 OK OK ...`. These strings are the raw material for every delinquency-based feature.

3. **Inquiries**: every hard pull in the past two years, with date and subscriber name. A burst of inquiries in the last 30 days is a strong short-horizon risk signal.

4. **Public records**: bankruptcies, tax liens, civil judgments. Post-NCAP changes in the United States, most judgments and tax liens no longer appear, which reshaped the public record feature bank after 2017.

5. **Collections**: charged-off accounts placed with third-party collectors. Often shown with original creditor, collection agency, and charge-off balance.

The FICO score, the dominant consumer credit score in the United States, derives from bureau data only. Myfico.com publishes the category weights: payment history (roughly 35 percent), amounts owed (30 percent), length of credit history (15 percent), new credit (10 percent), credit mix (10 percent). The underlying algorithm is proprietary, but its inputs are public knowledge and follow a small number of archetypes. Utilization is the ratio of revolving balance to limit, computed per tradeline and aggregated to the file level. Delinquency depth is the worst 24-month payment code on each line, rolled up to file level as the fraction of tradelines that were 30+, 60+, or 90+ in the last 6, 12, or 24 months. Age features include the age of the oldest account and the average age of open tradelines.

VantageScore, the joint bureau product, and the proprietary scorecards that large lenders build in-house use the same tradeline and inquiry data but different binning, weighting, and target definitions. A common pattern inside a bank is to stack an in-house behavioral score on top of a bureau score, so the scorecard captures both the generic credit-file signal and the account-specific behavior that the bureau does not see.

The specific feature vocabulary is remarkably stable across bureaus and across decades. A partial list of the archetype features a scorecard developer can expect to find useful:

- `bureau_score`: the FICO or VantageScore on file at the observation date.

- `oldest_tradeline_age_months`: age of the oldest account. Tracks length of credit history.

- `avg_open_tradeline_age_months`: average age of open tradelines. Captures both length and churn.

- `utilization_revolving`: sum of balance divided by sum of limit across open revolving lines.

- `utilization_maximum_tradeline`: the maximum utilization across any single revolving tradeline.

- `num_tradelines_30dpd_12m`: count of tradelines that reached 30+ days past due in the last 12 months.

- `num_tradelines_60dpd_24m`: the 60+ DPD analog over 24 months.

- `num_inquiries_6m`: hard pulls in the last 6 months.

- `num_new_tradelines_12m`: newly opened accounts in the last 12 months.

- `bankruptcy_flag`, `collections_flag`, `tax_lien_flag`: public record presence indicators.

- `secured_installment_flag`, `mortgage_flag`: structural presence indicators.

- `revolving_total_balance`, `installment_total_balance`: dollar aggregates by account type.

- `months_since_last_delinquency`: recency of the most recent bad event; "never" is usually coded as a large positive number.

A clean scorecard typically uses 15 to 30 of these, with roughly a two-thirds weight on delinquency-adjacent features (past behavior), a 15-percent weight on utilization (current behavior), and a 10- to 20-percent weight on length and mix (structural).

### Bank internal data {#sec-ch03-internal}

Internal data is what the lender knows from its own books. It is almost always more predictive than bureau data for customers who already hold a product. A current-account issuer sees the full flow of salary credits and direct debits. A mortgage servicer sees escrow behavior. A credit card issuer sees transactional authorizations in real time.

The operational data stores used for model building tend to be organized by the source system:

- **Core banking**: account master, balances, interest accruals, statement-level tables.

- **Card authorization**: every swipe, with merchant category, amount, timestamp, and channel.

- **Payments and transfers**: ACH, wire, SEPA, faster payments, internal transfers.

- **Collections**: arrears, promise-to-pay history, agent notes, settlement agreements.

- **Customer contact**: call center records, digital channel logs, complaint flags.

A behavioral scorecard reduces this to a set of standardized windows: 1-month, 3-month, 6-month, and 12-month. Each window is aggregated into counts, sums, max, min, ratios, and trends. A typical card model will have 30 to 80 such features. The specific recipe matters less than the window discipline. The windows must end strictly before the observation point of the score, and they must be computable at that same point in the production path. If they are not, the model is leaky, a topic we return to in @sec-ch03-temporal-leakage-and-lookahead-bias.

There is a structural asymmetry between new-account origination scorecards and behavioral scorecards on existing accounts. An origination scorecard knows the bureau, the application, and nothing else. A behavioral scorecard on an existing card account has the full payment, balance, and transaction history of that account, along with the bureau refresh. The behavioral scorecard is almost always more accurate within its existing customer base; it typically reaches Gini coefficients in the 0.55 to 0.70 range on 12-month horizons, while origination models for the same lender reach 0.40 to 0.55. The gap comes entirely from the richer internal data.

Two specific internal features consistently dominate in behavioral scorecards. The first is the ratio of payment to statement balance, also called the revolving-pay rate. A customer who pays the full balance every month is structurally lower risk than one who pays the minimum, even at the same utilization. The second is the trend in transaction frequency and amount over the last 3 to 6 months. A sudden drop in transaction count while balance grows is a strong short-horizon risk signal, often preceding a 30+ DPD event.

### Account-level versus customer-level modeling

Some scorecards are built per-account; others are built per-customer. The choice matters. A customer-level model aggregates across all of the customer's accounts with the lender and produces one score. An account-level model produces a score per account, so a customer with three cards receives three scores. The customer-level model is more data-efficient but forces the aggregation to happen before the model sees the data. The account-level model is more flexible but requires the lender to manage three predictions for the same person.

In practice, origination uses the customer level (one application, one decision) and account management uses the account level (per-card credit-line changes, per-card repricing). IFRS 9 and CECL (@sec-ch35) have specific implications: the expected credit loss calculation is at the account level, so account-level PDs are the operational requirement even when the decision model runs at the customer level.

### Application data {#sec-ch03-application}

The application form is the scorecard's only chance to see information a customer volunteers that is not in the bureau or the internal master file. Typical fields are employment status, occupation, income, employer tenure, housing tenure, marital status, dependents, purpose of loan, requested amount, and term. Most fields are self-reported. Some lenders cross-check a subset through payroll data providers or open-banking connections.

Application features are high-signal for thin-file borrowers, who by definition have sparse bureau records. For customers with thick files, the marginal value of application data is lower, and the scorecard usually regresses toward bureau features. Income is the perennial exception. A consistent, verified income feature dominates many other inputs, even for thick-file customers.

### Tradeline-level features

The bureau delivers tradelines as a repeated-measures structure. A report with 12 open tradelines contains 12 rows of account-level information, not 1 aggregated row. Turning that into a single observation per borrower is a feature engineering problem, and it is where most scorecard teams spend their time.

Three families of aggregation dominate:

1. **Pointwise**: count of open installments, sum of revolving balances, and maximum utilization.

2. **Temporal**: count of tradelines with 30+ delinquency in the last 12 months, months since last delinquency, months since the oldest account opened.

3. **Structural**: presence of mortgage, presence of auto loan, ratio of secured to unsecured balance.

Modern gradient-boosted scorecards work directly on 100 to 500 such derived columns. Classical scorecards collapse further to 15 to 30 features, selected by information value and stability. We build both kinds in @sec-ch07 and @sec-ch12; this chapter sets up the ingredients.

Tradeline aggregation is where many hidden failure modes live. A common one is double-counting: if a mortgage is reported by both the servicer and the originator for a brief window, a naive aggregation double-counts it in the mortgage-count feature and in the sum-of-balances feature. Bureaus use identifier keys to deduplicate, but the keys are imperfect, and lenders usually write their own dedupe rules. Another is the treatment of authorized users: a thin-file consumer can ride on a spouse's or parent's revolving account, and the bureau reports the authorized user tradeline in the primary report. Whether the feature engine counts that line is a policy choice that affects both risk discrimination and fair lending posture.

### The credit-invisible and unscored populations

A large fraction of adults in any jurisdiction have insufficient bureau data to produce a score. @brevoort2016credit estimate that roughly 26 million Americans are credit invisible, meaning they have no bureau record, and another 19 million are unscored, meaning their record exists but is too thin or stale for the bureau's scoring model. The invisible and unscored populations skew younger, non-white, and lower-income, which makes them the principal policy target for alternative-data scoring. Any scorecard designed for mass-market retail lending has to make an explicit choice about how to treat thin-file applicants. The three common choices are (1) to score them on a dedicated thin-file model, (2) to route them to a judgmental underwriter, or (3) to decline by default. Each choice has fair-lending implications that model governance must document.

### External overlays {#sec-ch03-overlays}

A bureau report is not the only external data source. Income verification services like The Work Number, Finicity, and Plaid provide real-time payroll feeds that confirm stated income within seconds. Fraud databases such as FICO's Falcon, LexisNexis ThreatMetrix, and Early Warning Services flag known fraud rings, synthetic identities, and device fingerprints. AML and sanctions screening, while not directly part of credit risk, feeds the same decision workflow, and its data quality affects the stability of any model downstream. Model governance treats each overlay as a separate data source requiring its own lineage documentation, its own monitoring, and its own retraining plan.

## Alternative data

The line between "traditional" and "alternative" is time-dependent. Utility payment data was alternative in 2005 and is standard today. What the term currently means is any signal that is not in a nationwide credit bureau and not in a bank's own ledger. Five categories cover most of what large lenders have deployed or piloted.

### A working taxonomy

1. **Psychometric**: survey-style questionnaires designed to measure personality traits (conscientiousness, honesty, locus of control) that correlate with repayment. Deployed in frontier markets where bureau coverage is sparse.

2. **Behavioral and device**: smartphone metadata, browser fingerprints, typing dynamics, session-level app usage. @berg2020rise document that ten easily observed digital footprint variables, such as device operating system and time-of-day login patterns, deliver predictive power comparable to a credit bureau score at a German e-commerce lender.

3. **Transactional**: bank account data obtained through open banking APIs (PSD2 in Europe, CDR in Australia, the 1033 rule in the United States). Each transaction has a date, amount, counterparty, and a classification tag.

4. **Social and platform**: data collected inside a digital platform. @iyer2016screening and @lin2013judging show that in peer-to-peer lending, social ties and soft information embedded in listings contain residual risk information beyond traditional hard information.

5. **Utility and telco**: electricity, water, mobile phone bills. Thin-file consumers often have 6 to 24 months of telecom usage even when they have zero tradelines.

Chinese BigTech platforms have reported that transactional and platform data dominate bureau data for their own ecosystem [@bis2020data; @gambacorta2024data]. The underlying point is older than FinTech. The richer the lender's view of the borrower's cash flow, the less a centralized bureau adds on the margin.

### The information content of alternative data

For any new feature, the relevant question is whether it adds risk-adjusted discrimination on top of what the scorecard already has. @berg2020rise formalize this through nested models, regressing default on credit bureau score alone, on digital footprint alone, and on both. The marginal $R^2$ from adding digital footprints is comparable to the marginal $R^2$ of the bureau score itself. @gambacorta2024data run a similar test using Chinese fintech data and show that a model built on transactional data alone beats a model built on a bureau score alone, although the two together beat either.

The regulatory question, which we will see in @sec-ch05, is whether the resulting model complies with fair lending rules. Alternative data that correlates with protected characteristics can open disparate impact exposure even when the feature is nominally neutral. The empirical finding in @fuster2022predictably is that machine learning models with richer feature sets can widen or narrow racial pricing gaps depending on the choice of input set. Data policy is a model policy.

### Pitfalls of alternative data

Alternative data has three recurring failure modes. First, many signals drift fast. A social feature built in 2015 might not exist in 2025 because the platform has changed. Second, the distribution of missingness is usually not random. A customer without a smartphone has no device fingerprint, and the absence correlates with both income and credit risk. Third, the population on which an alternative data model is validated is almost always a self-selected sample of borrowers who consented to the data collection. Reject inference, covered in @sec-ch10, becomes essential.

A fourth, less-discussed failure mode is the regulatory half-life of novelty. When a signal first enters the market, it usually carries strong predictive power and light compliance scrutiny. As it diffuses across lenders, the signal loses economic rent, adversarial actors learn to game it, and regulators begin to ask how it maps onto protected classes. @fuster2022predictably make the latter point sharply for ML scorecards: models with richer feature sets can move the distribution of predictions in ways that widen or narrow racial pricing gaps, and the direction is not determined by the model class alone. Data governance for alternative signals needs an explicit sunset clause in the same way that a model governance framework has a model retirement clause.

### Cash flow underwriting

Cash flow underwriting is the most important new category of alternative data in the past five years. The workflow starts with a consumer-consented open-banking pull of 12 to 24 months of transaction history across all of the customer's depository accounts. A categorizer assigns each transaction a merchant category and a cash-flow tag (inflow, fixed outflow, discretionary outflow, transfer, fee). Aggregate features are computed at daily, weekly, and monthly frequency: net cash flow, income stability, rent coverage ratio, recurring debit presence, and overdraft count. @bis2020data argue that the informational content of this data can substitute for collateral in SME lending, which is a strong statement about its power.

Two operational facts make cash-flow underwriting different from the other alternative categories. It is consented, so the data subject is aware of the collection in a way that is rarely true for device or behavioral features. And it is structured, so the feature engineering pipeline can be specified and tested deterministically. These properties make cash flow data easier to defend in model validation. They also constrain the universe: only applicants who connect a bank account have any signal at all, which maps directly back onto the missingness-at-design problem that structural alternative data creates.

### Summary of marginal information content

Across the empirical literature, the pattern is consistent. A credit bureau score captures roughly two-thirds of the variation in default that the combined set of bureau, bank, and alternative data captures, with the remaining third split roughly evenly across application data (for thin-file) and alternative data (for both thin- and thick-file). The size of the alternative data contribution depends strongly on the customer segment. For prime thick-file borrowers, the alternative signal is mostly redundant. For thin-file, credit-invisible, and frontier-market borrowers, the bureau is sparse, and the alternative signal is essential. This heterogeneity argues for a segmented modeling approach rather than a single global model. Later chapter treat inclusion and segmentation head-on.

## Weight of evidence and information value {#sec-ch03-weight-of-evidence-and-information-value}

### Why bin features at all?

Before any formula, it is worth asking why a credit team would throw away information by replacing a continuous income figure with the bucket it falls into. The answer is that binning exchanges resolution for six properties that matter more than resolution in the production setting where a scorecard runs for years against drifting data and is subject to formal model validation.

1. **Robustness to outliers, measurement error, and reporting noise.** Bureau fields are reported with varying conventions across furnishers; income is self-reported on applications and has long upper tails; tradeline counts are zero-inflated. Bins absorb all of this into a discrete level whose log-odds contribution is bounded.

2. **Explicit treatment of missingness.** A missing tradeline summary is not the same as a zero. Binning makes the missing level its own bin with its own WoE, so the model uses missingness as a signal when it is informative and ignores it when it is not. No imputation choice is hidden inside the pipeline.

3. **Monotone, additive contribution to log-odds.** WoE-encoded features enter the logistic regression as linear terms whose coefficients factor cleanly into a base-odds piece and a per-bin contribution (@eq-logit-woe), which is what enables the points-based scorecard formulation in @sec-ch07. Underwriters and adverse-action systems can read each bin's contribution as a fixed point increment.

4. **Stability across resamples and through time.** A coarse five-bin partition of a feature is far more stable under resampling and population drift than a continuous coefficient, because the only thing that can change is the per-bin event rate. A scorecard that is refreshed annually but whose binning was set during development needs the binning to be stable across years; that is what the bootstrap and through-time diagnostics in the stability subsection below test.

5. **Two-stage decoupling of binning and coefficient estimation.** Bin selection is supervised but happens before the model is fit. The binning table is reviewed in isolation against IV, monotonicity, and bin-share rules. The coefficient estimation step then becomes essentially a sanity check, because the slope on a single WoE-encoded feature is approximately $-1$ in population. This decoupling is what lets a five-person scorecard team ship a model that a ten-person model risk team can validate.

6. **A model artifact that regulators read.** SR 11-7 model risk validators, ECOA Reg B examiners reviewing reason codes, and GDPR Article 22 explainability reviewers all expect a tabular artifact that lists every model input, every bin, and every contribution. The binning table *is* that artifact. No post-hoc explanation method (SHAP, LIME, permutation importance) produces something that validators trust the same way, because those methods are computed on the trained model rather than fixed at training time.

The first three reasons are the technical ones taught in @siddiqi2017intelligent. The last three are the institutional reasons that explain why binned-WoE pipelines remain dominant in retail credit even decades after gradient boosting matched or exceeded their predictive performance. We return to the question of whether modern algorithms eliminate the need for any of this in the subsection on modern models below.

Weight of evidence (WoE) is the canonical encoding used for this purpose in credit, going back to Kullback's work on information statistics in the 1950s [@kullback1951information] and commercialized in banking by Fair, Isaac, and Company in the 1970s. @siddiqi2017intelligent is the industry-standard reference for the practical pipeline.

### Formal definition

Fix a feature that has been binned into $J$ disjoint bins $A_1, \dots, A_J$. For each bin define the share of goods and share of bads that fall in that bin:

$$

g_j = \frac{\#\{i: x_i \in A_j, y_i = 0\}}{\#\{i: y_i = 0\}},

\qquad

b_j = \frac{\#\{i: x_i \in A_j, y_i = 1\}}{\#\{i: y_i = 1\}}.

$$ {#eq-shares}

The weight of evidence for bin $j$ is the log-ratio of those shares:

$$

\mathrm{WoE}_j = \ln\!\left(\frac{g_j}{b_j}\right).

$$ {#eq-woe}

Positive WoE means the bin is enriched with goods relative to the base rate. Negative WoE means the bin is enriched with bads. The information value of the feature is the weighted sum

$$

\mathrm{IV} = \sum_{j=1}^{J} (g_j - b_j) \mathrm{WoE}_j = \sum_{j=1}^{J} (g_j - b_j) \ln\!\left(\frac{g_j}{b_j}\right).

$$ {#eq-iv}

Practitioners rank features by IV with the rules of thumb from @siddiqi2017intelligent: IV less than 0.02 is unpredictive, 0.02 to 0.1 is weak, 0.1 to 0.3 is medium, 0.3 to 0.5 is strong, and above 0.5 is suspiciously good and usually means the bin count is too fine or the feature is leaky.

### A worked example by hand

Before invoking `optbinning`, it helps to compute the formulas in @eq-shares and @eq-iv on a toy portfolio with three bins. Suppose 1,000 applicants split across an `income_bucket` feature with $G = 900$ goods and $B = 100$ bads in total:

```{python}

#| label: woe-by-hand

import numpy as np, pandas as pd

ex = pd.DataFrame({

"bin": ["Low", "Mid", "High"],

"goods": [250, 370, 280],

"bads": [ 50, 30, 20],

})

G, B = ex["goods"].sum(), ex["bads"].sum()

ex["g_j"] = ex["goods"] / G

ex["b_j"] = ex["bads"] / B

ex["WoE_j"] = np.log(ex["g_j"] / ex["b_j"])

ex["IV_j"] = (ex["g_j"] - ex["b_j"]) * ex["WoE_j"]

print(ex.round(4).to_string(index=False))

print(f"\nIV (total) = {ex['IV_j'].sum():.4f}")

```

Read the table row by row. The Low bin holds $250/900 \approx 27.8\%$ of all goods but $50/100 = 50\%$ of all bads. Its WoE is $\ln(0.278/0.500) \approx -0.59$, a negative value flagging higher-than-average risk, consistent with a $50/300 = 16.7\%$ bad rate against the population base rate of $10\%$. The High bin reverses the imbalance and contributes $\mathrm{WoE} \approx +0.44$. The IV total of about $0.21$ would land the feature in the "medium predictive" tier of the rule of thumb above.

Three sanity checks the table makes obvious:

- The columns $g_j$ and $b_j$ each sum to $1$, because they are class-conditional shares.

- A bin with $g_j = b_j$ contributes zero to IV, because $\ln(1) = 0$. Equality in every bin is exactly the case where the feature is independent of $Y$.

- Both negative and positive WoE bins contribute positively to IV, because the signs of $(g_j - b_j)$ and $\mathrm{WoE}_j$ always match.

These same numbers are what `optbinning` would print if it were given the same three bins, modulo the Laplace pseudo-count discussed in the from-scratch implementation below.

### Equivalence to a symmetric KL divergence

The IV in @eq-iv is exactly the symmetrized Kullback-Leibler divergence between the class-conditional distributions of the binned feature. Let $P$ denote the distribution of $X$ conditional on $Y = 0$ and $Q$ the distribution of $X$ conditional on $Y = 1$, so $P(A_j) = g_j$ and $Q(A_j) = b_j$. The KL divergence of $P$ from $Q$ is

$$

D_{\mathrm{KL}}(P \parallel Q) = \sum_j g_j \ln(g_j/b_j).

$$ {#eq-kl-pq}

By symmetry,

$$

D_{\mathrm{KL}}(Q \parallel P) = \sum_j b_j \ln(b_j/g_j) = -\sum_j b_j \ln(g_j/b_j).

$$ {#eq-kl-qp}

Adding the two,

$$

D_{\mathrm{KL}}(P \parallel Q) + D_{\mathrm{KL}}(Q \parallel P)

= \sum_j (g_j - b_j)\ln(g_j/b_j)

= \mathrm{IV}.

$$ {#eq-iv-eq-kl}

Information value is the Jeffreys divergence between the good and bad class-conditional feature distributions [@kullback1951information]. Two consequences follow:

1. IV is always non-negative, with equality if and only if $g_j = b_j$ for all $j$, the case where the feature contains no information about the label.

2. IV is additive across independent disjoint features only in the limit where no feature carries any information contained in another, so the IV-based ranking should be read as a marginal screen, not a joint optimum.

### Connection to logistic regression

The link to logistic regression is tight. Conditional on bin $j$,

$$

\mathrm{logit} \Pr(Y = 1 \mid X \in A_j)

= \ln\!\left(\frac{\Pr(Y=1, X \in A_j)}{\Pr(Y=0, X \in A_j)}\right)

= \ln\!\left(\frac{\pi_1}{\pi_0}\right) + \ln\!\left(\frac{b_j}{g_j}\right)

= \alpha - \mathrm{WoE}_j,

$$ {#eq-logit-woe}

where $\alpha = \ln(\pi_1 / \pi_0)$ is the log base-odds. Fitting a logistic regression on a single WoE-encoded feature recovers an intercept equal to $\alpha$ and a slope equal to $-1$ in population. In sample, the slope is close to $-1$ and the deviation measures how close the bin assignment is to the saturated model. Because of @eq-logit-woe, WoE encoding gives logistic regression coefficients that factor cleanly into a base-odds piece and a bin-contribution piece, which is what enables the standard points-based scorecard formulation we develop in @sec-ch07.

### Empirical ranking on Taiwan default

```{python}

#| label: iv-ranking-taiwan

from optbinning import BinningProcess

from sklearn.model_selection import train_test_split

df_tw = load_taiwan_default().drop(columns=["id"])

y_tw = df_tw["default"].astype(int).values

X_tw = df_tw.drop(columns=["default"])

X_tr, X_te, y_tr, y_te = train_test_split(

X_tw, y_tw, test_size=0.3, random_state=42, stratify=y_tw

)

bp = BinningProcess(variable_names=X_tw.columns.tolist())

bp.fit(X_tr.values, y_tr)

iv_tbl = (bp.summary()

.loc[:, ["name", "iv", "js", "gini", "n_bins"]]

.sort_values("iv", ascending=False)

.reset_index(drop=True))

iv_tbl.head(15).round(4)

```

`optbinning` [@navas2020optimal] uses a mixed-integer programming formulation to find an optimal monotone binning that maximizes IV subject to monotonicity and bin-size constraints. The algorithm extends classical supervised discretization [@fayyad1993multi] by enforcing risk monotonicity, which is what underwriters expect from a scorecard. The highest-IV feature in the Taiwan data is the most recent delinquency code (`PAY_0`), followed by older payment codes, which matches the domain intuition.

The `summary()` table includes two additional ranking columns alongside `iv`, both computed on the same binned distributions and sometimes preferred when IV is unstable.

- **`js`: Jensen-Shannon divergence.** A bounded, symmetric variant of the KL divergences from @eq-kl-pq and @eq-kl-qp. With $M = (P + Q)/2$ the bin-share midpoint, $\mathrm{JS}(P, Q) = \tfrac{1}{2} D_{\mathrm{KL}}(P \parallel M) + \tfrac{1}{2} D_{\mathrm{KL}}(Q \parallel M)$. Always lies in $[0, \ln 2]$, so it cannot blow up the way IV can when a bin is nearly empty. Read the same way as IV: bigger means more class separation. Often used as a robustness check on the IV ranking.

- **`gini`: bin-level Gini coefficient.** Twice the area between the bin-ordered cumulative-goods and cumulative-bads curves; equivalently $2 \cdot \mathrm{AUC} - 1$ computed using the bin-ordered WoE as the score. Reported on $[0, 1]$. Same monotone direction as IV but scaled like the discriminative AUC measure used in @sec-ch04, so it lets the scorecard team compare a feature's marginal predictive contribution against the overall model AUC in the same units. The full treatment of AUC, Gini, KS, and Brier sits in @sec-ch04.

In practice, these three columns rank features almost identically; large disagreements are a flag that one bin is dominating IV, in which case a coarser binning or a JS-based ranking is the safer choice.

### WoE-encoded features versus raw features in logistic regression

```{python}

#| label: woe-vs-raw-logreg

from sklearn.linear_model import LogisticRegression

from sklearn.preprocessing import StandardScaler

from sklearn.metrics import roc_auc_score

X_tr_woe = bp.transform(X_tr.values, metric="woe")

X_te_woe = bp.transform(X_te.values, metric="woe")

lr_woe = LogisticRegression(max_iter=1000, C=1.0).fit(X_tr_woe, y_tr)

auc_woe = roc_auc_score(y_te, lr_woe.predict_proba(X_te_woe)[:, 1])

scaler = StandardScaler()

X_tr_raw = scaler.fit_transform(X_tr.values)

X_te_raw = scaler.transform(X_te.values)

lr_raw = LogisticRegression(max_iter=1000, C=1.0).fit(X_tr_raw, y_tr)

auc_raw = roc_auc_score(y_te, lr_raw.predict_proba(X_te_raw)[:, 1])

pd.DataFrame({

"encoding": ["WoE", "raw (standardized)"],

"AUC": [auc_woe, auc_raw],

}).round(4)

```

The WoE-encoded logistic model gains roughly 4 to 5 AUC points relative to standardized raw features on Taiwan. The gap narrows once we move to flexible models like gradient boosting, which can internally approximate monotone step functions. The gap persists, however, for the class of linear models that regulators prefer because they are auditable.

Three mechanisms drive the gap, and naming them clarifies when WoE will help and when it will not.

1. **Linearization in log-odds.** WoE turns a non-monotone or kinked empirical risk curve into a monotone, additive contribution in log-odds space, exactly the space the logistic link operates in. A single linear coefficient then fits a relationship that the raw feature would need a polynomial, spline, or piecewise basis to express.

2. **Common units across columns.** WoE rescales every feature, numeric or categorical, into log-odds. The L2 penalty in `LogisticRegression` therefore stops privileging high-variance columns over high-information ones, which is what causes the standardized-raw baseline to leak coefficient mass to noisy features.

3. **Bounded leverage.** Outliers and missing values are absorbed into bins with finite WoE, so a single extreme observation cannot tilt the regression line. Standardization shifts and scales but leaves the long tail intact, and a logistic regression with a few extreme rows still gets dragged.

None of the three is unique to WoE. Splines, target encoders, and isotonic transforms each capture some subset. WoE is the only encoding that captures all three *and* preserves a binning table that a model validator can read. That second property is what makes it the default in regulated retail credit, even where it does not maximize AUC.

### WoE is univariate: handling interactions and non-linearity

WoE is computed one feature at a time, and the IV in @eq-iv treats each feature in isolation. The encoding captures non-linearity *within* a feature (e.g., the bin shape can be U-shaped, monotone, or step), but it does not capture any signal that lives only in the joint distribution of two or more columns. "High credit limit is risky only when paired with a thin payment history" is invisible to a WoE-plus-logistic model unless the interaction is engineered explicitly. Equivalently, the IV-based ranking is a marginal screen: a feature with low IV may still carry conditional information that a joint model would use, and a feature with high IV may be redundant given another already in the model.

This is the structural reason for the AUC gap pattern in the comparison above and in the end-to-end benchmark in @sec-ch03-benchmark. Three remedies sit on a complexity-versus-interpretability spectrum.

1. **Hand-built interaction features.** Cross-tabulate two binned features into a single categorical (`PAY_0` × `LIMIT_BAL_bin`), then WoE-encode the cross. The result stays inside the scorecard pipeline and remains auditable. Cost: combinatorial explosion if used liberally, and small bin counts that hurt stability.

2. **Two-dimensional supervised binning.** `optbinning` ships an `OptimalBinning2D` that solves the same MIP over a pair of features. Useful for a small number of known-interactive pairs (utilization × age of oldest tradeline is a classic).

3. **Segmented scorecards.** Fit one scorecard per pre-defined segment (thin-file vs thick-file, secured vs unsecured). Interactions with the segmenting variable are absorbed by the segmentation. @sec-ch31 treats this in depth.

If the dominant signal is genuinely interactive, none of the above competes with a tree ensemble that splits in arbitrary feature combinations by construction. The empirical fact that WoE-plus-logistic stays close to gradient boosting on regulated retail credit data is a statement about that data: monotone main effects from delinquency, utilization, and tenure dominate, and interactions are second-order, not a general property of the encoding. On data where interactions are first-order (fraud, marketing response on heterogeneous customer pools), the calculus reverses and a tree ensemble is the right starting point.

### A from-scratch implementation

It is good practice to verify the library against a short NumPy reference. The function below reproduces `optbinning`'s per-bin WoE for a fixed set of bin edges.

```{python}

#| label: woe-from-scratch

def woe_iv_from_bins(x: np.ndarray, y: np.ndarray, edges: np.ndarray,

laplace: float = 0.5):

"""Return (woe_per_bin, iv, bin_index_of_x) for a fixed set of edges."""

bin_idx = np.digitize(x, edges[1:-1], right=False)

df = pd.DataFrame({"bin": bin_idx, "y": y})

tab = (df.groupby("bin")["y"]

.agg(["count", "sum"])

.rename(columns={"count": "n", "sum": "b"}))

tab["g"] = tab["n"] - tab["b"]

total_b = max(tab["b"].sum(), 1.0)

total_g = max(tab["g"].sum(), 1.0)

p_b = (tab["b"] + laplace) / (total_b + laplace * len(tab))

p_g = (tab["g"] + laplace) / (total_g + laplace * len(tab))

woe = np.log(p_g / p_b)

iv = float(((p_g - p_b) * woe).sum())

return woe.to_dict(), iv, bin_idx

opt_var = bp.get_binned_variable("LIMIT_BAL")

lib_edges = np.concatenate([[-np.inf], opt_var.splits, [np.inf]])

woe_scratch, iv_scratch, _ = woe_iv_from_bins(

X_tr["LIMIT_BAL"].values, y_tr, lib_edges

)

iv_lib = float(opt_var.binning_table.build().loc["Totals", "IV"])

print(f"IV (optbinning): {iv_lib:.4f}")

print(f"IV (from-scratch): {iv_scratch:.4f}")

```

The two IV numbers (here $0.2002$ from `optbinning` and $0.1998$ from the scratch implementation) differ by about $4 \times 10^{-4}$, with the scratch value the smaller of the two. The gap is not a constant offset: it comes from the Laplace pseudo-count of $0.5$, which shrinks the empirical bin shares toward uniform, compresses the WoE magnitudes, and therefore lowers the IV. Setting `laplace=0` in `woe_iv_from_bins` reproduces `optbinning`'s value exactly whenever no bin is empty, which is the right cross-check to run during development. The pseudo-count earns its keep in production, where a single bin occasionally drops to zero in a refresh sample and an unsmoothed $\ln(0)$ would crash the scoring service.

### Reading a binning table

```{python}

#| label: binning-table-example

opt_var.binning_table.build().round(4)

```

This table is the canonical artifact a scorecard developer hands over for model validation. Each row is a bin. The columns show the bin boundaries, the fraction of the population in the bin, the event rate, the WoE, and the IV contribution. The totals row at the bottom gives the IV for the feature. Binning tables like this one are what SR 11-7 [@sr117] validators will read first when reviewing a scorecard submission.

Three diagnostics in the binning table carry most of the validation signal. First, the WoE column should be monotone when the feature is ordinal and the business logic calls for monotonicity. An income feature that increases in WoE, then dips for the highest bin, then increases again, either has too many bins, has a sample-size problem, or has a real structural break (high earners with complicated tax situations, for instance) that needs a dedicated flag. Second, the bin-share column (often labeled `count (%)`) should not have any bin with less than 3 to 5 percent of the population. Small bins have unstable WoE and produce scorecards that swing wildly under resampling. Third, the event rate column should step smoothly across bins when ordered by WoE. Large jumps suggest that the bin boundaries are not where the risk boundary actually sits.

The `optbinning` algorithm is a mixed-integer programming formulation that enforces these properties globally rather than through heuristic post-processing [@navas2020optimal]. It extends the classical supervised discretization literature, which treats binning as a greedy information-gain split, by adding constraints that express what a scorecard developer would actually want. The classical reference is @fayyad1993multi, which uses a minimum description length principle to choose the number of bins. The MIP formulation subsumes this as a special case with different constraints.

### Edge cases in WoE encoding

Three edge cases appear in almost every scorecard build, and each has a standard fix.

**Zero-count bins.** A bin may contain no goods or no bads in the training sample. The raw WoE in @eq-woe is then $\ln 0$ or $-\infty$. Three fixes exist:

1. A Laplace smoothing term adds a pseudo-count of $0.5$ or $1$ to each bin.

2. A bin merge folds the offending bin into an adjacent bin with consistent risk.

3. An `optbinning` constraint on minimum bin size avoids the zero-count state entirely during fitting.

> The Laplace fix is the simplest and adequate for most production code.

**Out-of-range values at scoring time.** Production data may contain values that fall outside the training-time range. For numeric features, the conventional answer is to extend the outermost bins to $(-\infty, \text{edge}_1]$ and $(\text{edge}_{J-1}, \infty)$, so every value maps to a bin. For categorical features, the analog is to keep a catch-all level that absorbs unseen categories with a WoE set equal to the population-weighted average of the observed levels.

**Missing values.** `optbinning` treats missing values as a separate bin, which is the behavior we want. If the missingness itself is informative, the WoE of the missing bin will be nonzero, and the model will use it. If not, the WoE will be close to zero, and the model ignores it. Either way, the treatment is explicit rather than hidden behind a mean imputation.

### Stability of WoE under resampling

A scorecard is only useful if the bin edges and WoE values are stable. Two diagnostics verify stability: bootstrap resampling and through-time partitioning.

```{python}

#| label: woe-bootstrap

from optbinning import OptimalBinning

x_var = X_tr["PAY_0"].values

y_var = y_tr

boot_iv = []

boot_edges = []

boot_rng = np.random.default_rng(0)

for b in range(25):

idx = boot_rng.integers(0, len(x_var), size=len(x_var))

ob = OptimalBinning(name="PAY_0", dtype="numerical", max_n_bins=6)

ob.fit(x_var[idx], y_var[idx])

iv_b = float(ob.binning_table.build().loc["Totals", "IV"])

boot_iv.append(iv_b)

boot_edges.append(tuple(np.round(ob.splits, 3)))

pd.DataFrame({

"statistic": ["mean IV", "std IV", "min IV", "max IV"],

"value": [np.mean(boot_iv), np.std(boot_iv),

np.min(boot_iv), np.max(boot_iv)],

}).round(4)

```

If the bootstrap standard deviation of IV is large relative to the mean, the feature's binning is unstable and the scorecard will be brittle. On the `PAY_0` feature the bootstrap spread is modest, which is the expected picture for a strongly predictive feature. Features that fail bootstrap stability almost always benefit from a coarser binning.

### The relationship to supervised discretization

WoE is one member of a family of supervised discretization methods. @fayyad1993multi introduced the entropy-based minimum description length principle for choosing the number of bins. Chi-merge and ChiSquare-based methods use a test of independence between adjacent bins as the merge criterion. The CART tree, treated at length in @sec-ch11, is a univariate supervised binner when grown as a stump, and its splitting criterion is Gini impurity rather than WoE. All of these methods can be expressed as choices of the split function and the stopping criterion; the `optbinning` MIP formulation lets the user specify both explicitly.

The deep reason WoE dominates in credit is not statistical performance but interpretability. A CART split gives a threshold and a count; WoE gives a threshold, a count, and a log-odds contribution that plugs directly into a points-based scorecard. The transformation from WoE to scorecard points is linear in the log-odds, which @sec-ch07 works out in detail.

### Do modern algorithms still need binning and WoE?

A reasonable reading of the chapter so far is that WoE is a piece of legacy machinery that exists because logistic regression cannot handle non-linearity on its own. Gradient boosting splits at arbitrary thresholds, neural networks learn arbitrary feature transformations, and either approach matches the AUC of a WoE-plus-logistic pipeline on most retail credit data. So why bin?

The honest answer has two parts. The first is that for **predictive performance alone**, you do not need WoE if your downstream model is a tree ensemble or a sufficiently regularized neural network. The end-to-end benchmark in @sec-ch03-benchmark makes this explicit: a gradient-boosted model on raw features matches the WoE-plus-logistic configuration on Taiwan within noise. Tree learners pick their own thresholds, absorb missingness through surrogate splits or dedicated handling, and are insensitive to monotone transforms of inputs. WoE is computationally and statistically wasted on them.

The second part is that **production credit scoring is not a pure prediction problem**. It carries six constraints that WoE-style preprocessing addresses by construction and that modern algorithms address only with extra effort:

- **Reason codes for adverse action notices** under ECOA Reg B and FCRA §1681m must be ordered, stable, and explainable per applicant. A scorecard derives reason codes mechanically from the per-bin WoE contributions; a gradient boosting model derives them from SHAP values, which are post-hoc, sample-dependent, and not always monotone in the underlying feature, even when the feature is supposed to be.

- **Monotonicity constraints** on features such as utilization, delinquency, and tenure are required by both regulators and underwriters. WoE binning enforces monotonicity at the binning step; LightGBM and XGBoost support monotonicity flags but at a real cost in fit, and neural networks need either a Lipschitz architecture or a monotone-by-construction layer such as in @sill1998monotonic.

- **Stability under population drift** is harder to guarantee with continuous splits chosen on a single training sample than with bins reviewed against a stability index. Champion scorecards stay in production five-plus years; champion gradient-boosted models are typically refreshed every quarter.

- **Auditability of the model artifact** by SR 11-7 model risk management groups, by GDPR Article 22 explainability reviewers in the EU, and by a non-technical credit committee. The binning table is the artifact those audiences read. SHAP and partial dependence are explanations *of* the artifact, not the artifact itself.

- **Reproducibility across pipelines.** A binning table can be re-implemented by a different team in a different language with the same WoE values. A gradient-boosted model with a particular set of hyperparameters cannot be reproduced exactly outside the original training pipeline.

- **Sample efficiency for thin-file segments.** Where the relevant subpopulation is small (frontier-market lenders, new-to-credit applicants, niche product lines), a five-bin discretization extracts more reliable signal than a continuous spline that needs many degrees of freedom to fit non-linearity.

The pragmatic stack used by many regulated lenders today is a hybrid. Gradient boosting on raw or lightly engineered features is used for ranking and for the challenger model; a WoE-binned logistic scorecard is used for the production decision model that is actually deployed. The two are reconciled with a calibration step. Where a single model must serve both purposes, the rising option is the **Explainable Boosting Machine** (EBM) of @lou2013accurate and @nori2019interpretml, which fits a generalized additive model with one shape function per feature and optionally one shape function per pairwise interaction. EBMs are essentially a continuous-bin generalization of WoE, with the per-feature shape playing the role of the WoE column and the per-pair shape playing the role of an `OptimalBinning2D` cross. They typically match gradient boosting on AUC while preserving the per-feature artifact regulators expect.

So the short answer to "is this an artifact of logistic regression from decades ago?" is: only the *encoding* is. The underlying constraints (e.g., reason codes, monotonicity, stability, auditability, sample efficiency) are not artifacts of the algorithm; they are properties of the regulatory and operational environment in which credit models live. WoE persists because it satisfies those constraints almost for free, not because anyone is nostalgic for the 1970s.

## Missing data {#sec-ch03-missing}

Every real credit data set has missing values. A bureau-less applicant has no tradelines. An application that skipped an optional field has nulls. An open-banking connection that failed mid-session has a truncated history. How missingness gets handled determines, in practice, whether a model works in production for the tail of the customer base where it matters most.

### Rubin's taxonomy

@rubin1976inference classified missing-data mechanisms into three types. Let $X$ be the complete data, $M$ the missingness indicator matrix, and $X_{\mathrm{obs}}, X_{\mathrm{mis}}$ the observed and missing partitions.

- **MCAR** (missing completely at random): $\Pr(M \mid X) = \Pr(M)$. Missingness is independent of both observed and unobserved data. Rare in practice. The classic example is a random sensor dropout.

- **MAR** (missing at random): $\Pr(M \mid X) = \Pr(M \mid X_{\mathrm{obs}})$. Missingness depends only on observed variables. An income field that is more likely to be blank for younger applicants is MAR, because age is observed. Under MAR, likelihood-based methods such as multiple imputation are unbiased.

- **MNAR** (missing not at random): $\Pr(M \mid X)$ depends on $X_{\mathrm{mis}}$. Missingness depends on the unobserved value itself. High earners who decline to report income are MNAR. Imputation alone cannot recover the full data distribution without assumptions.

@little2019statistical gives the textbook treatment. For scorecard work, the relevant message is that MCAR is a convenient fiction, MAR is often defensible given rich observed data, and MNAR is the state of the world for sensitive fields like income, mortgage balance on outside institutions, or credit applications at competitors.

### Imputation strategies

Five strategies cover most of what a scorecard pipeline needs:

1. **Simple statistic**: replace with the column mean, median, or mode. Fast, unbiased under MCAR, biased otherwise. Collapses variance.

2. **Indicator plus statistic**: add a binary "was missing" column and impute the underlying value. Captures the information in the fact of missingness, which for credit is often predictive on its own.

3. **k-nearest neighbors**: find the $k$ most similar rows under a defined distance, average their values. Works well when the data has strong local structure. Compute scales quadratically with sample size.

4. **Multivariate iterative (MICE)**: model each incomplete feature as a function of the others, iterate to convergence [@vanbuuren2011mice; @white2011multiple]. Scikit-learn's `IterativeImputer` is the Python implementation. Recovers MAR under mild assumptions.

5. **Model-based with native support**: tree learners like XGBoost, LightGBM, and CatBoost natively route missing values to the child node that minimizes loss. For those learners, imputation is a pre-model choice only if you also run a linear benchmark.

For credit scoring, the missing-indicator strategy deserves first-line status. If an applicant failed to fill in an optional field, that refusal often correlates with risk. Losing it by silent mean-imputation is a substantive information loss.

### Simulated experiment on German credit

We take the German credit data, inject missingness under the three mechanisms, and compare five imputation strategies on the downstream AUC of a logistic model.

```{python}

#| label: missing-sim-setup

from sklearn.experimental import enable_iterative_imputer # noqa: F401

from sklearn.impute import SimpleImputer, KNNImputer, IterativeImputer

from sklearn.linear_model import LogisticRegression

from sklearn.pipeline import Pipeline

from sklearn.preprocessing import StandardScaler

from sklearn.model_selection import train_test_split

rng_miss = np.random.default_rng(0)

df_ger = load_german_credit()

num_cols = ["duration", "amount", "age", "installment_rate",

"residence_since", "existing_credits", "people_liable"]

X_full = df_ger[num_cols].astype(float).copy()

y_full = df_ger["default"].values

def inject_mcar(X, frac, rng):

X = X.copy()

for c in X.columns:

mask = rng.random(len(X)) < frac

X.loc[mask, c] = np.nan

return X

def inject_mar(X, driver, frac, rng):

X = X.copy()

thr = X[driver].quantile(0.6)

for c in [c for c in X.columns if c != driver]:

p = np.where(X[driver] > thr, frac, frac * 0.2)

mask = rng.random(len(X)) < p

X.loc[mask, c] = np.nan

return X

def inject_mnar(X, frac, rng):

X = X.copy()

for c in X.columns:

thr = X[c].quantile(0.7)

p = np.where(X[c] > thr, frac, frac * 0.1)

mask = rng.random(len(X)) < p

X.loc[mask, c] = np.nan

return X

```

The MCAR mechanism drops each cell independently with probability 0.2. The MAR mechanism drops a cell with probability 0.4 when `duration` is in the top 40 percent and 0.08 otherwise. The MNAR mechanism drops a cell with probability 0.4 when the cell's own value is in the top 30 percent of its column and 0.04 otherwise. Credit analogs map cleanly: MAR is "applicants with long tenure skip optional fields"; MNAR is "applicants with high balances skip the balance field".

```{python}

#| label: missing-sim-run

from sklearn.metrics import roc_auc_score

def eval_imputer(Xtr, Xte, ytr, yte, imputer):

pipe = Pipeline([

("imp", imputer),

("scale", StandardScaler()),

("lr", LogisticRegression(max_iter=1000)),

])

pipe.fit(Xtr, ytr)

p = pipe.predict_proba(Xte)[:, 1]

return roc_auc_score(yte, p)

mechanisms = {

"MCAR": lambda X: inject_mcar(X, 0.2, rng_miss),

"MAR": lambda X: inject_mar(X, "duration", 0.4, rng_miss),

"MNAR": lambda X: inject_mnar(X, 0.4, rng_miss),

}

imputers = {

"mean": SimpleImputer(strategy="mean"),

"median": SimpleImputer(strategy="median"),

"mean+ind": SimpleImputer(strategy="mean", add_indicator=True),

"kNN(5)": KNNImputer(n_neighbors=5),

"MICE": IterativeImputer(max_iter=10, random_state=0),

}

records = []

for mech_name, inject in mechanisms.items():

Xm = inject(X_full)

Xtr, Xte, ytr, yte = train_test_split(

Xm, y_full, test_size=0.3, random_state=0, stratify=y_full

)

for imp_name, imp in imputers.items():

auc = eval_imputer(Xtr, Xte, ytr, yte, imp)

records.append({"mechanism": mech_name, "imputer": imp_name, "AUC": auc})

res_miss = (pd.DataFrame(records)

.pivot(index="imputer", columns="mechanism", values="AUC")

.round(4))

res_miss

```

Two observations. First, no imputer dominates across all three mechanisms, which is the expected result once we understand that each method encodes different assumptions. Under MCAR the mean-plus-indicator strategy leads because the indicator itself is random and the underlying distribution is symmetric. Under MAR, mean or median imputation is competitive because the drivers are observed in the other features. Under MNAR no method recovers the full signal. The second observation is that the differences are small in absolute terms, a few AUC points, but they compound into large differences in expected profit when stacked across features. This is where adding a missingness indicator pays dividends for essentially zero cost.

### When to use which

A practical decision rule for scorecard work:

- **Categorical feature with natural "missing" level**: keep the missing level as its own bin. WoE handles it. This is the default in `optbinning`.

- **Continuous numeric with MAR missingness and rich observed data**: `IterativeImputer` (MICE) with a small number of iterations. Add an indicator if missingness rate exceeds 5 percent.

- **Sparse high-dimensional matrix with MNAR fields**: keep the indicator, impute the value with a median. Do not try to be clever.

- **Tree learner downstream**: do not impute. Pass NaNs through. Compare to imputation only if required by governance.

- **Linear or neural scorecard**: impute explicitly and persist the imputer in the same artifact as the model.

The industry's single largest imputation failure mode is pipeline drift. The training data had a missingness rate of 2 percent for income. The production data has 15 percent, because a downstream upstream vendor changed a default. The imputer silently mean-fills the missing values, and the score concentrates near the population mean. Monitor missingness rates on every feature in production with the same care that you monitor PSI (@sec-ch16).

### What about matrix completion, GAIN, MIWAE, MissForest? {#sec-ch03-sota-imputers}

A reasonable reader will ask why the list above stops at MICE when the imputation literature has moved on to low-rank matrix completion [@mazumder2010softimpute], random-forest imputation [@stekhoven2012missforest], generative-adversarial imputation [@yoon2018gain], deep-latent-variable imputation [@mattei2019miwae], and AutoML-style imputer selection [@jarrett2022hyperimpute]. The answer is not that these methods are bad. They are excluded from the recommended scorecard pipeline for four reasons that all bind at the same time in credit.

First, **low-rank assumptions do not fit credit feature matrices**. Matrix completion methods assume the underlying data matrix is approximately low-rank, which is the right model for collaborative filtering (a few latent taste factors generate every user-item rating) and for image inpainting (smoothness in pixel space). Credit features are a heterogeneous mix of bureau scores, demographics, employment fields, behavioral aggregates, and self-reported items. There is no shared low-dimensional latent factor that generates all of them, and SoftImpute-style nuclear-norm completion silently shrinks toward a basis that has no interpretation. Empirically, low-rank completion is competitive on dense numeric panels (e.g., genomics) and weak on the wide mixed-type tables that scorecards consume.

Second, **the inference-time story is broken or expensive**. A scorecard must score one new applicant in milliseconds. Matrix completion, GAIN, and MIWAE were all designed for the in-sample setting, where you complete a fixed matrix once. Out-of-sample completion for a single new row requires either projection onto a stored basis (matrix completion), a forward pass through a generator trained on potentially stale data (GAIN), or sampling from a learned posterior (MIWAE). Each of these adds a second model to the production path that must itself be versioned, monitored for drift, and validated under SR 11-7. The marginal AUC gain rarely justifies the operational cost.

Third, **the empirical lift on tabular data is small**. Two large published benchmarks of imputation methods on tabular data, @jager2021benchmark and @lemorvan2021whatsgood, both find that median imputation with a missing-indicator column is within one or two AUC points of the best deep imputer on essentially every downstream classification task they test. Where the deep methods win, they win by margins that are smaller than the variance across random seeds. For credit, where the dominant model is a gradient-boosted tree that handles NaN natively (@sec-ch12-xgboost), the practical gain from a sophisticated imputer is close to zero.

Fourth, **governance penalizes opacity**. A bank validator will ask three questions about any imputer: what assumption does it encode, what happens when production missingness drifts, and how would you detect a regression. Median-plus-indicator answers all three in one sentence each. GAN- or VAE-based imputation answers none of them cleanly, and the validator will require a separate model risk file, a champion-challenger setup, and ongoing monitoring of the imputer's own outputs. This burden is real and is why most production scorecards still ship with median-plus-indicator or with a tree learner that ignores the question entirely.

The honest summary is that matrix completion and its deep-learning successors are excellent tools for the problems they were designed for (collaborative filtering, image inpainting, gene-expression panels) and a poor fit for the wide-mixed-type, low-latency, high-governance environment of credit scoring. The gap is not theoretical sophistication; it is fit-for-purpose. A team that wants to experiment with HyperImpute or MissForest as a challenger to the median-plus-indicator champion should do so, but the production default belongs with the simpler tool.

### Multiple imputation and variance inflation

Single imputation, where each missing cell is replaced with one value, systematically understates downstream standard errors. Multiple imputation draws $M$ imputed data sets, fits the model on each, and combines the results using the rules of @rubin1976inference. @vanbuuren2011mice and @white2011multiple treat the methodology in detail. For credit scoring, the pragmatic reality is that $M = 1$ is almost always used. The argument is that scorecard inference is about the predicted probability rather than the coefficient standard errors, and the downstream decisions (approve, decline, price) are robust to the kind of variance inflation that single imputation glosses over. That argument is correct for pure decision-making, but breaks down when the model's coefficients are used in capital calculations under Basel IRB, where the regulator cares about the confidence interval around the PD. Banks that run IRB models generally carry a multiple-imputation pipeline for a subset of critical features, even when single imputation is the default for decision making.

### Imputation and monotonicity

A subtle but important property of any imputer is whether it preserves the monotone risk structure that scorecard binning relies on. Mean imputation breaks monotonicity because the imputed value sits near the middle of the distribution, while the underlying missing-value risk may be at one of the tails. Median imputation has the same problem. An imputation strategy that restores monotonicity is to impute to the value that matches the observed risk of the missing group. Operationally, this means fitting a univariate logistic regression of the label on the feature in the non-missing subsample, then assigning the imputed value so that the predicted log-odds of a missing row equals the empirical log-odds of the missing subset. This is worth the effort when downstream scorecard monotonicity is a constraint, and overkill otherwise.

The construction is short enough to demonstrate in code. We inject MNAR missingness on `duration` (longer-duration applicants are more likely to have the field blank, and longer duration is also riskier), then compare the imputed value chosen by the mean, the median, and the risk-matched rule.

```{python}

#| label: risk-matched-impute

from sklearn.linear_model import LogisticRegression as _LR

rng_rmi = np.random.default_rng(7)

X_rmi = X_full.copy()

thr_d = X_rmi["duration"].quantile(0.6)

p_drop = np.where(X_rmi["duration"] > thr_d, 0.6, 0.05)

miss_mask = rng_rmi.random(len(X_rmi)) < p_drop

X_rmi.loc[miss_mask, "duration"] = np.nan

obs = ~X_rmi["duration"].isna()

x_obs = X_rmi.loc[obs, "duration"].values.reshape(-1, 1)

y_obs = y_full[obs]

y_mis = y_full[~obs]

p_mis = y_mis.mean()

logit_mis = np.log(p_mis / (1 - p_mis))

uni = _LR(penalty=None, max_iter=1000).fit(x_obs, y_obs)

a, b = float(uni.intercept_[0]), float(uni.coef_[0, 0])

x_risk = (logit_mis - a) / b

cmp = pd.DataFrame({

"strategy": ["mean", "median", "risk-matched"],

"imputed_value": [

X_rmi["duration"].mean(),

X_rmi["duration"].median(),

x_risk,

],

})

cmp["pred_logit_at_imp"] = a + b * cmp["imputed_value"]

cmp["empirical_logit_missing"] = logit_mis

cmp["abs_gap"] = (cmp["pred_logit_at_imp"] - logit_mis).abs()

cmp.round(3)

```

The risk-matched row has `abs_gap` equal to zero by construction. The mean and median rows have a positive gap whose sign tells you which direction the imputer is pulling the missing population: a negative `pred_logit_at_imp` minus `empirical_logit_missing` means mean or median imputation is making the missing rows look safer than they really are, which is exactly the failure mode that breaks monotonicity in the downstream scorecard.

```{python}

#| label: risk-matched-auc

def fill_and_score(value, X_in):

Xf = X_in.copy()

Xf["duration"] = Xf["duration"].fillna(value)

Xtr, Xte, ytr, yte = train_test_split(

Xf, y_full, test_size=0.3, random_state=0, stratify=y_full

)

pipe = Pipeline([("scale", StandardScaler()),

("lr", LogisticRegression(max_iter=1000))])

pipe.fit(Xtr, ytr)

return roc_auc_score(yte, pipe.predict_proba(Xte)[:, 1])

aucs = {row.strategy: fill_and_score(row.imputed_value, X_rmi)

for row in cmp.itertuples()}

pd.Series(aucs, name="AUC").round(4).to_frame()

```

The AUC differences are typically small on a single feature, which matches the broader finding from the simulated experiment above. The point of risk matching is not to win the AUC race; it is to keep the scorecard's monotone risk structure intact when the binning step downstream insists on it. Two further notes. First, the rule generalizes from a single feature to a multivariate setting by replacing the univariate logit with a model that uses all observed features and solving for the imputed value of the missing column at the row's own observed covariates. Second, the rule is a single-imputation device. If you need calibrated standard errors, draw the imputed value from the posterior predictive distribution of the univariate logit instead of using the point estimate, then average across draws using Rubin's rules.

### Missingness indicator interpretation

When a missingness indicator column is added, the logistic coefficient on it has a direct risk interpretation. Let $M_j$ be the indicator that feature $j$ is missing and $X_j^{\text{imp}}$ be the imputed value. The fitted model has the form

$$

\mathrm{logit} \Pr(Y=1 \mid X, M)

= \alpha + \beta_j X_j^{\text{imp}} + \gamma_j M_j + \cdots

$$ {#eq-missing-indicator}

The coefficient $\gamma_j$ measures the risk premium (or discount) associated with the fact of missingness itself, holding the imputed value constant. A positive $\gamma_j$ with a substantial magnitude says that a missing-on-$X_j$ row is riskier than an observed row with the same imputed value, which is direct evidence that the missingness mechanism is MNAR. A near-zero $\gamma_j$ is evidence that the mechanism is plausibly MCAR or MAR.

> Two cautions apply. First, the indicator is colinear with the imputed value if every imputed row shares the same value, which in mean imputation is always the case for a single feature. Regularized logistic regression handles this cleanly; unpenalized logistic regression may show nonfinite standard errors. Second, if two features have correlated missingness (for example, both self-reported income and self-reported employment length are blank for the same applicant), adding both indicators recovers almost all the useful signal but can make the model's bias unstable across resampling. A joint "application-form incomplete" indicator often works better than two separate indicators.

## Feature selection

Scorecards live with more features than they use. A fintech's feature store routinely holds thousands of columns. A deployed model uses 10 to 60. The process of getting from one to the other is feature selection. Four approaches cover almost everything production teams deploy.

### IV filter

The simplest screen is to rank every feature by information value and keep the top $K$, or keep every feature with $\mathrm{IV} \ge 0.02$. This is a univariate filter. It ignores correlations. In a scorecard with 500 candidate features and heavy correlation, it is nevertheless the right first step, because it cuts the search space from 500 to 100 or 50 before any multivariate method runs.

```{python}

#| label: iv-filter-example

iv_filter = iv_tbl[iv_tbl["iv"] >= 0.02].reset_index(drop=True)

print(f"Features with IV >= 0.02: {len(iv_filter)} of {len(iv_tbl)}")

iv_filter.head(10).round(3)

```

On Taiwan most of the 23 numeric features clear the 0.02 threshold. The handful that fall below are demographic fields whose marginal signal is weak once `LIMIT_BAL` and the payment-delinquency block are in the pool. On a raw feature store with thousands of variables, two-thirds typically fall below.

### LASSO

The LASSO [@tibshirani1996regression] adds an $\ell_1$ penalty to the logistic log-likelihood,

$$

\hat\beta(\lambda) = \arg\min_{\beta_0, \beta}

\Big\{ -\tfrac{1}{n}\sum_{i=1}^n \ell_i(\beta_0, \beta)

+ \lambda \sum_{j=1}^{p} |\beta_j| \Big\},

$$ {#eq-lasso}

where $\ell_i$ is the per-observation log-likelihood. For $\lambda$ large, the solution is the null model; for $\lambda = 0$ the solution is ordinary logistic regression. Between those extremes, coefficients enter one at a time as $\lambda$ decreases, which gives the characteristic LASSO path. Features whose coefficients remain at zero across most of the path are dropped. The `glmnet` coordinate-descent algorithm [@friedman2010regularization] is the standard solver.

Three properties make LASSO attractive for scorecard selection. First, it handles correlated features by picking one and shrinking the others, which reduces the collinearity problem that flat logistic regression suffers on WoE-encoded features. Second, the regularization path is cheap to compute, so a team can inspect the entire trajectory rather than committing to a single $\lambda$. Third, the elastic net extension [@zou2005regularization] smooths the all-or-nothing selection into a convex combination with ridge regularization, which is usually the better default in production.

```{python}

#| label: lasso-path

from sklearn.linear_model import LogisticRegression

from sklearn.preprocessing import StandardScaler

from sklearn.model_selection import train_test_split

df_tw = load_taiwan_default().drop(columns=["id"])

y = df_tw["default"].values.astype(int)

X = df_tw.drop(columns=["default"]).values.astype(float)

X_tr, X_te, y_tr, y_te = train_test_split(

X, y, test_size=0.3, random_state=42, stratify=y

)

sc = StandardScaler().fit(X_tr)

X_tr_s = sc.transform(X_tr)

X_te_s = sc.transform(X_te)

Cs = np.logspace(-3, 1, 25)

feat_names = df_tw.drop(columns=["default"]).columns.tolist()

coefs = np.zeros((len(Cs), X_tr_s.shape[1]))

for i, C in enumerate(Cs):

m = LogisticRegression(penalty="l1", solver="liblinear",

C=C, max_iter=2000)

m.fit(X_tr_s, y_tr)

coefs[i] = m.coef_[0]

fig, ax = plt.subplots(figsize=(7, 4.2))

for j in range(coefs.shape[1]):

ax.plot(Cs, coefs[:, j], lw=1.0)

ax.set_xscale("log")

ax.axhline(0, color="k", lw=0.6)

ax.set_xlabel("Inverse regularization strength C (larger C = weaker penalty)")

ax.set_ylabel("Coefficient")

ax.set_title("LASSO logistic regression path on Taiwan default")

plt.tight_layout()

plt.show()

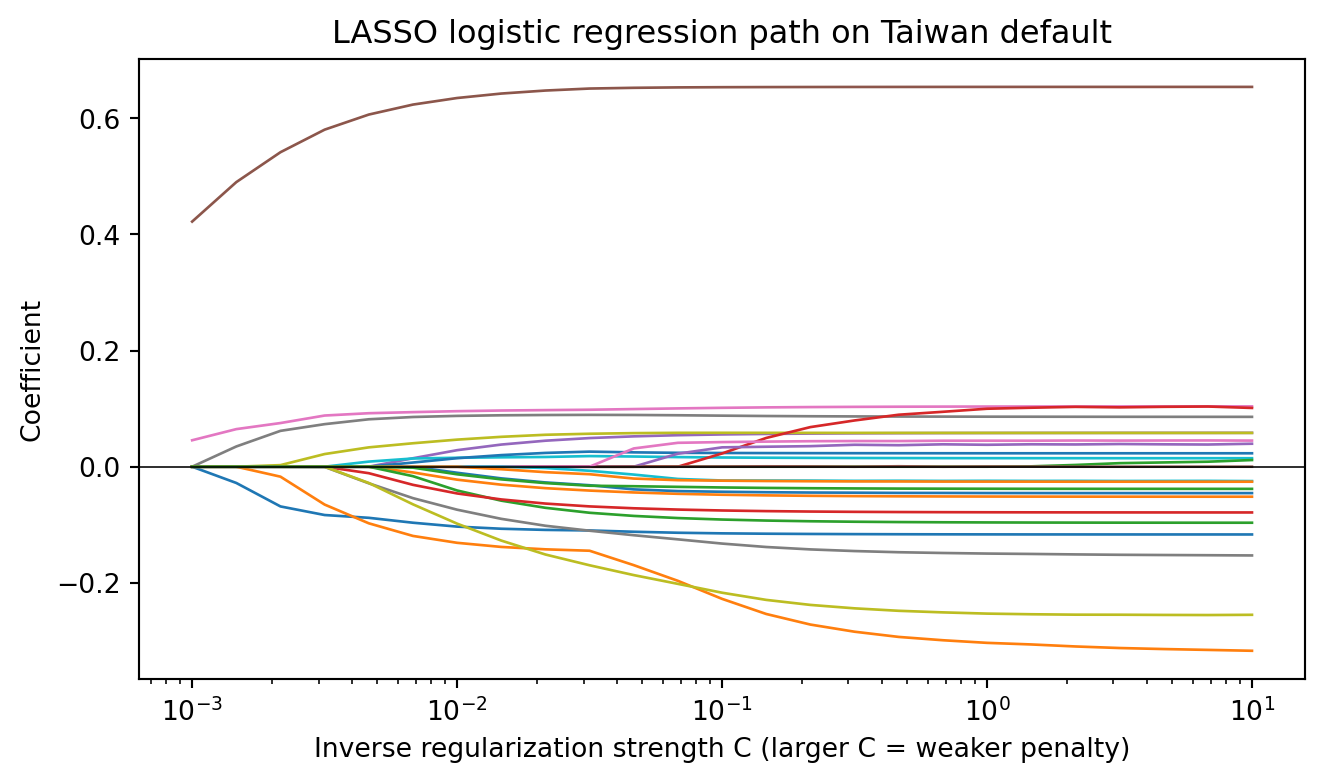

```

The shape of this plot is typical. At the strongest penalty most coefficients are zero; as the penalty weakens the `PAY_0` family enters first, followed by `LIMIT_BAL` and `PAY_AMT`. When two highly collinear features are present, the LASSO picks one and keeps the other at zero until the penalty is very weak. That behavior is the motivation for the elastic net extension.

```{python}

#| label: lasso-select

C_star = 0.02

m_star = LogisticRegression(penalty="l1", solver="liblinear",

C=C_star, max_iter=2000).fit(X_tr_s, y_tr)

kept = np.array(feat_names)[m_star.coef_[0] != 0]

dropped = np.array(feat_names)[m_star.coef_[0] == 0]

print(f"Kept ({len(kept)}): {list(kept)}")

print(f"Dropped ({len(dropped)}): {list(dropped)}")

```

At $C = 0.02$, the LASSO drops the weakest features and keeps a compact subset. The practical workflow is to cross-validate over $\lambda$ to pick the operating point, then stability-select across bootstrap resamples to drop features that enter the solution only intermittently.

### Mutual information and permutation importance

Two nonparametric alternatives round out the toolkit.

Mutual information $I(X_j; Y) = \sum_{x,y} p(x,y) \ln \frac{p(x,y)}{p(x)p(y)}$ is closely related to IV. For a binary $Y$, $I(X_j; Y) = H(Y) - H(Y \mid X_j)$, which measures the expected reduction in label entropy from knowing $X_j$. `sklearn.feature_selection.mutual_info_classif` estimates it for continuous and discrete features.

Permutation importance [@breiman2001random; @altmann2010permutation] measures the drop in model performance when a single feature is randomly permuted on the validation set. It is model-agnostic and captures interactions that univariate IV misses. The cost is that permutation importance for correlated features is misleading: permuting one feature often leaves the information intact through its correlated neighbor, so the importance of both looks low. Conditional permutation variants partly fix this.

```{python}