---

execute:

echo: true

eval: true

warning: false

message: false

bibliography:

- ../references.bib

- ../refs/ch-09.bib

---

# Survival Analysis and Time-to-Default {#sec-ch09}

::: {.callout-note appearance="simple" icon="false"}

**Scope: both retail and corporate.** Survival and discrete-time hazard models. Retail vintage analysis (account-level time-to-default) and corporate firm-year hazards (@sec-ch09-shumway, popularized by Shumway 2001) share the same likelihood.

:::

## Overview {.unnumbered}

### A failure that motivates the chapter {.unnumbered}

A logistic regression trained on a 36-month auto-loan vintage at month 6 and scored at month 24 will mis-rank an obligor who defaulted in month 4 the same way it mis-ranks one who was censored in month 4: both look like a positive label at horizon 6 even though the first obligor exited the risk set and the second is still on book. Dropping censored observations biases the bad rate; keeping them as zeros biases it the other way. Either way the IFRS 9 stage-2 lifetime provision computed off the resulting score is wrong by tens of basis points (the direction depends on which censoring choice you made), and the Basel one-year through-the-cycle PD is mis-calibrated by enough to fail an SR 11-7 effective-challenge benchmark against any model that respects the time axis. The failure is structural: a binary classifier *cannot* represent the joint distribution of (event, time) that the regulator's question is asking about. It is also avoidable: the same data, rescored on a Cox PH or a discrete-time Shumway logit fit on the same loan-month panel, recovers the time-dependent AUC and lifts the calibration deviation at 24 months back inside the stage-2 SLA. The rest of the chapter is what that rescoring entails, what it costs, and how to defend it in writing to four regulators.

A binary default flag tells you whether a loan went bad. It does not tell you when. In consumer and corporate credit, the when matters at least as much as the whether. A loan that defaults in month 6 bleeds capital differently from a loan that defaults in month 36. An IFRS 9 stage-2 provision [@ifrs9] depends on the lifetime distribution of default, not on a point prediction. A Basel IRB model [@basel2006international] must deliver a through-the-cycle probability of default at a one-year horizon, plus term-structure inputs for stress tests [@bellotti2013forecasting]. The problem is intrinsically temporal, and treating it as classification throws away the most useful piece of the data: the time axis.

Survival analysis is the right tool. It was built in biostatistics [@kaplan1958nonparametric; @cox1972regression; @aalen1978nonparametric] to handle exactly the situation lenders face: the event of interest may not occur during the observation window (censoring), covariates influence the timing of the event (regression on times), and competing events can preempt the one you care about (prepayment terminates a loan without default). Retail credit adopted these methods early [@narain1992survival; @banasik1999not; @stepanova2002survival] and continues to refine them [@bellotti2009credit; @dirick2017time].

### The chapter's throughline {.unnumbered}

Default is a time-to-event problem with five structural assumptions a model can lock in: independence of censoring from the event clock, a parametric (or nonparametric) hazard shape, proportional hazards across covariates, a single absorbing event, no immune fraction, and homogeneity within an observed risk band. This chapter walks the family of estimators that progressively relaxes those assumptions, scores the cost of each relaxation under controlled stress, and lands the surviving roster on a regulator-grade Vietnamese consumer-credit case study where four of the five assumptions are violated at once.

### Three threads, one chapter {.unnumbered}

The chapter braids three threads. Knowing which one you are on at any moment is the difference between reading the chapter and being lost in it.

- **Thread M (methods).** The genealogy walk from Kaplan-Meier down each branch (Cox, AFT, competing risks, cure, the heterogeneity extensions, Shumway). Every method section opens with the credit question it answers and the limitation of the prior section that motivated it. This is the chapter's spine.

- **Thread P (production).** Every method has a "leave the notebook" companion: the `survival_diagnostics` package (@sec-ch09-defensibility-production), the `discrete_hazard` package (@sec-ch09-shumway-production), the FastAPI scoring service (@sec-ch09-deployment), the MLflow artifact lineage, the Spark-scale fits (@sec-ch09-scalability). Each Thread P interlude opens with one paragraph on why the code needs to leave the notebook.

- **Thread C (case).** Two applied case threads do different work. The controlled six-DGP stress benchmark at @sec-ch09-comparison-stress proves the cost sheet at @sec-ch09-comparison-matrix by violating one assumption per world with a known oracle. The Vietnam capstone at @sec-ch09-vietnam-code proves the chapter on a portfolio that triggers four assumption violations at once with no oracle and a regulator watching.

### Reader contract {.unnumbered}

Three concrete promises:

- *Methods reader.* Every model is implemented twice (from-scratch so the math is visible, and with a reference library: `lifelines`, `scikit-survival`, `statsmodels`). Every section opens with the credit question it answers and the prior-section limitation it relaxes.

- *Production reader.* Every method has a Thread P interlude with a versioned package, a schema validator, a FastAPI surface, and an MLflow lineage. The cross-cutting infrastructure is gathered around @sec-ch09-deployment.

- *Reviewer reader.* The chapter delivers a cost sheet (@sec-ch09-comparison-matrix), a routing aid (@sec-ch09-comparison-flowchart), an upgrade aid (@sec-ch09-marketing's extension selector), a controlled assumption-violation oracle (@sec-ch09-comparison-stress), and a no-oracle public-file reality check (@sec-ch09-benchmark), all calibrated against a regulator's pre-read.

The case for survival models is sharpest in emerging markets. Vietnamese consumer loans book with thin CIC histories, cash-flow incomes that flex with Tet, and informal-sector obligors whose default timing concentrates in months 2 to 6 when a seasonal cash buffer runs out. A one-year classification target hides both the seasonal spike and the early-prepayment culture that ends the risk window for a large fraction of the book. The capstone case study at @sec-ch09-vietnam returns to this with Circular 11/2021 default timing, competing-risk prepayment from Tet bonuses, vintage analysis under macro volatility, and Decree 13/2023 data-protection obligations.

This chapter develops the machinery, end to end, from nonparametric product-limit estimators (@sec-ch09-km-cox) to parametric accelerated failure time models (@sec-ch09-aft), through competing risks (@sec-ch09-competing), cure mixtures (@sec-ch09-cure), heterogeneity and state dependence (@sec-ch09-marketing), vintage analysis (@sec-ch09-vintage), and the discrete-time hazard formulation (@sec-ch09-shumway) popularized in corporate default by @shumway2001forecasting and @duffie2007multi.

### Model genealogy: what each step up buys you {.unnumbered}

Survival is a family of models, not a single estimator. Each member of the family relaxes a structural assumption that an earlier member relied on, and pays for that flexibility somewhere else (more data, more compute, weaker extrapolation, harder identification). @fig-ch09-genealogy is the chapter map. The cost sheet at @sec-ch09-comparison-matrix is the dual: each row is a node on the tree, each column an assumption an arrow into the node relaxed. The routing aid at @sec-ch09-comparison-flowchart compresses both into binary questions a model-risk pre-read answers in five minutes. The stress benchmark at @sec-ch09-comparison-stress drops the whole roster onto six controlled DGPs and turns each cost-sheet entry into a number.

```{mermaid}

%%| label: fig-ch09-genealogy

%%| fig-cap: "Survival model genealogy. Each arrow is labeled with the assumption a more sophisticated estimator relaxes relative to its parent. Grey: anti-pattern baseline (binary classifier discards the time axis). Blue: regression backbones (Cox, AFT, Shumway). Orange: structure relaxers that add unobserved heterogeneity, immunity, or fully nonparametric hazard shape. Green: competing-risk estimators that admit more than one terminating event. Purple: marketing-style retention. The right way to read this chapter is to walk the tree from a question (extrapolate past observed horizon? cluster effect? immune fraction? competing prepayment?) to the cheapest family that answers yes."

graph TD

BIN["Binary classifier<br/>(anti-pattern: discards 'when')"]

KM["Kaplan-Meier<br/>marginal S(t)"]

COX["Cox PH<br/>+ covariates (log-linear)"]

STR["Cox + strata<br/>baseline varies across groups"]

TVC["Cox + TVC<br/>covariates evolve over time"]

FR["Frailty Cox / Weibull<br/>+ unobserved cluster effect"]

AFT["AFT family<br/>(Weibull, LogNormal, LogLogistic)"]

CURE["Mixture cure<br/>+ immune fraction"]

AJ["Aalen-Johansen<br/>marginal CIF, multi-state"]

FG["Fine-Gray<br/>covariates on CIF"]

SHUM["Shumway discrete logit<br/>period basis, easy TVC"]

LCPWE["Latent-class PWE<br/>+ discrete heterogeneity"]

SBG["Shifted Beta-Geometric<br/>retention with beta heterogeneity"]

RSF["RSF / GBSurv<br/>tree-based, free hazard shape"]

DEEP["DeepSurv / XGB long-table<br/>scale to high-dim covariates"]

BIN -->|"+ time axis, + censoring"| KM

KM -->|"+ covariates (PH assumed)"| COX

KM -->|"+ parametric shape → lifetime PD"| AFT

KM -->|"+ competing event"| AJ

KM -->|"+ geometric retention + heterogeneity"| SBG

COX -->|"baseline per group"| STR

COX -->|"covariates change over time"| TVC

COX -->|"+ random effect on hazard"| FR

COX -->|"discretize time, fit as logit"| SHUM

COX -->|"drop log-linear, drop PH"| RSF

COX -->|"drop log-linear, scale up"| DEEP

AFT -->|"+ susceptible vs immune split"| CURE

AJ -->|"+ covariates on subdistribution"| FG

SHUM -->|"+ latent classes on hazard"| LCPWE

classDef base fill:#f4f4f8,stroke:#444,color:#111;

classDef regr fill:#eef3ff,stroke:#3355aa,color:#111;

classDef relax fill:#fff1d6,stroke:#b8860b,color:#111;

classDef compete fill:#e6f5ea,stroke:#2a8,color:#111;

classDef retain fill:#f0e6f7,stroke:#7a3ea1,color:#111;

class BIN,KM base;

class COX,STR,TVC,AFT,SHUM regr;

class FR,CURE,LCPWE,RSF,DEEP relax;

class AJ,FG compete;

class SBG retain;

```

A reader can use the map as a decision aid. *Need a one-year PD with the strongest discrimination on the file you have?* Walk down to RSF or GBSurv and accept that you cannot extrapolate past the longest training horizon. *Need a lifetime ECL curve to month 60 from a book observed only to month 36?* Walk down the AFT branch and pay with a parametric hazard shape. *Need a CIF that does not double-count prepayments as defaults?* Walk down to Aalen-Johansen, then to Fine-Gray once covariates matter. *Need a covariate effect that flips sign at age 12?* Walk down to TVC or to Shumway with a period basis. *Suspect a long-run immune fraction (revolvers who never default)?* Walk to mixture cure. *Suspect cluster heterogeneity (branches, dealers, originators)?* Walk to frailty Cox, or to latent-class PWE if the heterogeneity is discrete and the hazard shape is unknown. The chapter walks each branch, fits each model both from scratch and with a reference library, and closes at @sec-ch09-comparison with the same roster scored on six DGPs that each break exactly one assumption.

### Notation {.unnumbered}

- $T \in (0, \infty)$: time to default, a nonnegative random variable with density $f(t)$ and c.d.f. $F(t)$.

- $S(t) = \Pr(T > t) = 1 - F(t)$: survival function.

- $h(t) = \lim_{\Delta \downarrow 0} \Pr(t \le T < t+\Delta \mid T \ge t)/\Delta = f(t)/S(t)$: hazard rate.

- $H(t) = \int_0^t h(u)du = -\log S(t)$: cumulative hazard.

- $C$: right-censoring time, often administrative. We observe $Y = \min(T, C)$ and $\delta = \mathbf{1}\{T \le C\}$ (true default time seen), while $\delta= 0$: censored ($T >C$) (Loan still alive at cutoff $C$; default time unknown, only know $T > C$).

- $x \in \mathbb{R}^p$: time-fixed covariates (e.g., application attributes). $x(t)$: time-varying (e.g., unemployment rate in month $t$).

- $\beta \in \mathbb{R}^p$: regression coefficients in proportional hazards or AFT form.

- Vintage $v$: the origination period of a cohort. Age $a$: months since origination. Calendar $c = v + a$.

## Credit as survival {#sec-ch09-survival}

The logistic-regression failure that opened the chapter was a structural mismatch between the question (lifetime distribution of an event time) and the model (one-period probability of a binary label). The next page gives that question its language: a state machine for the loan, a likelihood that respects censoring, and three fundamental functions ($S$, $h$, $H$) that every estimator in the rest of the chapter is a parametrization of. Everything below in this section is data-side: shape of the panel, threats to identification, defensibility diagnostics. Everything from @sec-ch09-km-cox onward is a parametric or nonparametric specification of the hazard.

A loan originated in month $v$ with principal $L$ and contractual term $M$ becomes a point in a state diagram. At each month $a = 1, 2, \ldots, M$ the loan is in exactly one of four states: current, delinquent, defaulted, closed (paid off, refinanced, or written off). The transition of interest is current-or-delinquent to defaulted. Call that random transition time $T$. Because the loan matures at month $M$, the event time is right-censored at $C = M$ unless the loan prepays, in which case a competing event removes the loan from the risk set early. This is the canonical survival setup [@cox1972regression; @prentice1978analysis]. @fig-ch09-states draws the state machine: solid arrows are within-loan rolls, the bold arrow into *Defaulted* is the event of interest, *Closed* is the competing event, and reaching age $M$ without either is administrative right-censoring.

```{mermaid}

%%| label: fig-ch09-states

%%| fig-cap: "Loan-month state diagram. Each month the loan occupies exactly one node. *Current* and *Delinquent* form the at-risk set; the bold transition to *Defaulted* is the survival event $T$. *Closed* (prepay, refinance, write-off short of default) is a competing event that removes the loan from the risk set. Reaching contractual maturity $a=M$ without default or closure is administrative right-censoring at $C=M$."

stateDiagram-v2

direction LR

[*] --> Current: origination a=0

Current --> Delinquent: miss payment

Delinquent --> Current: cure

Delinquent --> Defaulted: 90+ DPD, event T

Current --> Closed: prepay or refinance

Delinquent --> Closed: write-off or settlement

Current --> Censored: reach maturity a=M

Delinquent --> Censored: reach maturity a=M

Defaulted --> [*]

Closed --> [*]

Censored --> [*]

classDef risk fill:#eef3ff,stroke:#3355aa,color:#111;

classDef event fill:#fde2e2,stroke:#a33,color:#111,font-weight:bold;

classDef compete fill:#f4f4f8,stroke:#444,color:#111;

classDef cens fill:#eafaf1,stroke:#2a8,color:#111;

class Current,Delinquent risk;

class Defaulted event;

class Closed compete;

class Censored cens;

```

The three fundamental functions are equivalent descriptions of the same distribution:

$$

S(t) = \Pr(T > t) = \exp\{-H(t)\}, \qquad H(t) = \int_0^t h(u) du, \qquad h(t) = -\frac{d}{dt}\log S(t).

$$ {#eq-triplet}

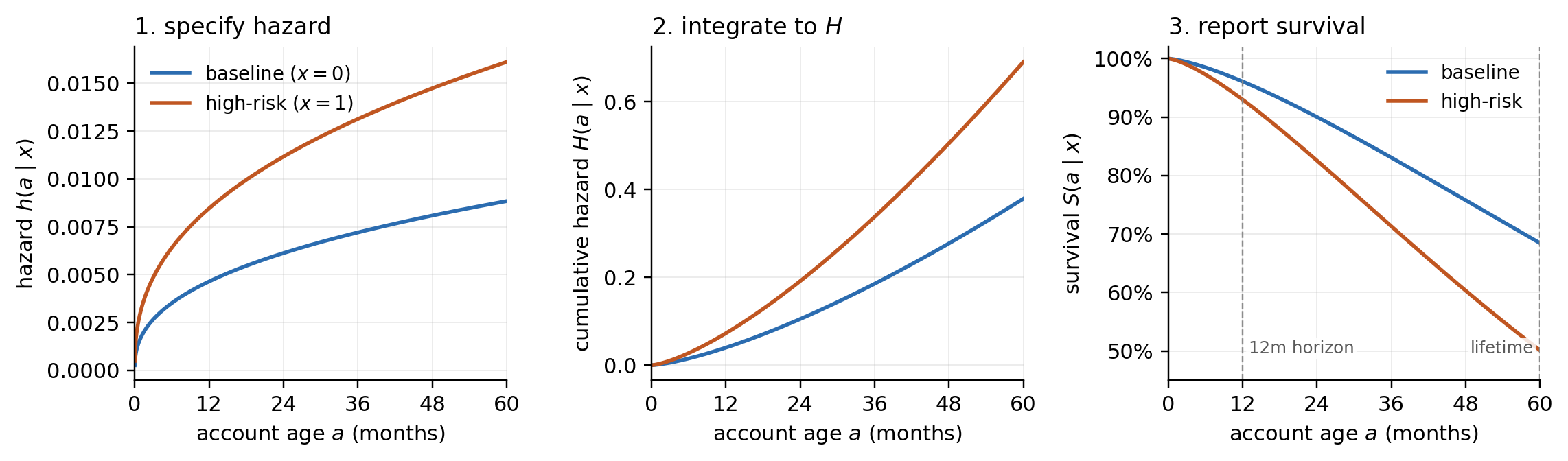

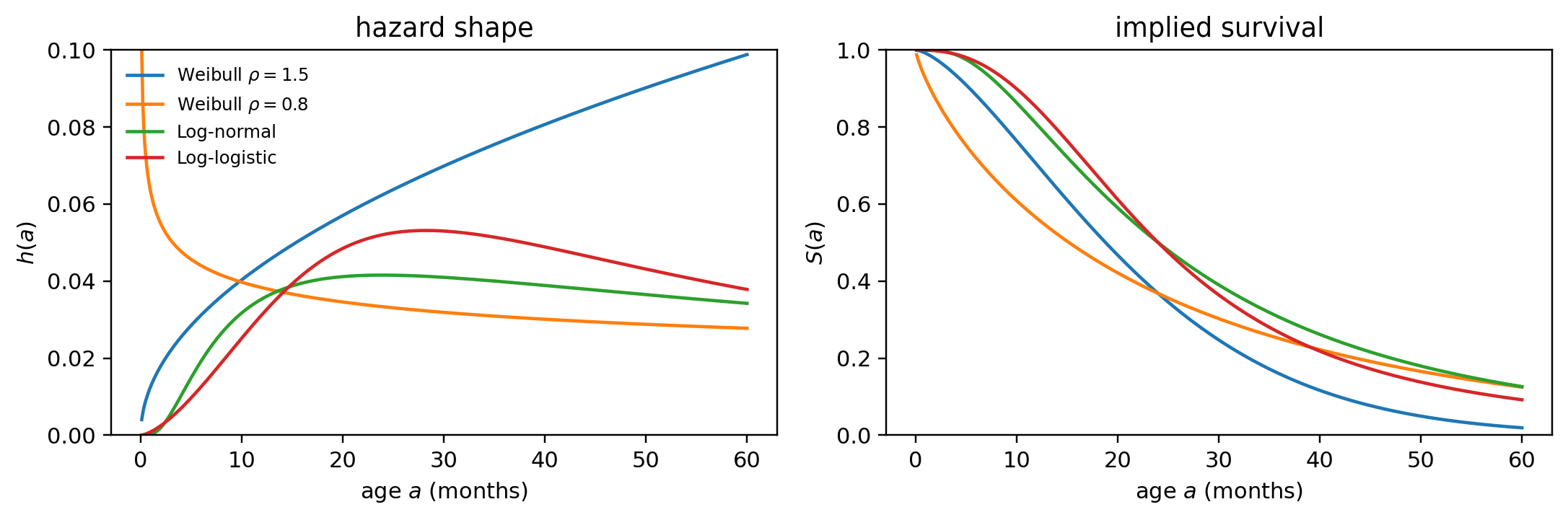

The hazard is the natural modeling primitive. It is local in time (unlike $S$ or $F$, which are cumulative), it is nonnegative (unlike derivatives of $F$, which are nonnegative only because $F$ is monotone), and covariates enter it in clean multiplicative or additive form. Credit risk measurement reports prefer $S(t)$ or the probability of default curve $F(t)$ because provisioning formulas, Basel risk-weight functions [@basel2017finalising], and stress tests quote lifetime or 12-month probabilities. A good modeler specifies $h$ and reports $S$. @fig-ch09-spec-report makes that workflow concrete: pick a parametric hazard, integrate to the cumulative hazard $H$, exponentiate to $S$, and read off the 12-month and lifetime PDs the report consumer actually wants.

### Right censoring and the likelihood

Right censoring is the defining feature of survival data. In retail credit, the most common form is administrative: the observation window ends at calendar time $\tau_{\text{end}}$, so a loan originated in month $v$ has follow-up $\tau_{\text{end}} - v$. Loans still current at $\tau_{\text{end}}$ contribute only their realized duration, not their (unobserved) default time.

Assume independent censoring: $T \perp C \mid x$. In words, among loans that share the same covariate vector $x$, the ones whose follow-up gets cut short carry no extra information about default timing beyond what their $x$ already says. Equivalently, the censoring mechanism is allowed to depend on $x$ (and on calendar time, since that is the same for everyone) but not on the latent $T$ once $x$ is conditioned on. If the assumption holds, the at-risk set $\mathcal{R}(t) = \{i : Y_i \ge t\}$ is a random sample of the population still at risk at age $t$, and the partial-likelihood and product-limit estimators treat each censored observation as "alive on its last seen day, future unknown" without bias.

Is the assumption realistic in retail credit? It is partly enforced by design and partly violated in practice. Three patterns matter:

1. *Administrative cutoff at* $\tau_{\text{end}}$ is the safe case. The data extraction date is exogenous to any individual loan's risk. Conditional on origination month $v$ and the covariate vector, the censoring time $C = \tau_{\text{end}} - v$ is deterministic, so $T \perp C \mid x, v$ holds by construction. This is why most credit-survival papers simply state "all censoring is administrative" and stop there.[^09-survival-analysis-1]

2. *Prepayment is the dangerous case.* A 36-month auto loan booked at month $v$ with covariates $x$ has a latent default time $T$ drawn from $h(t \mid x)$. At month 18, the borrower's credit improves (a fact not in $x$, unless you instrument refreshed scores), and a competitor offers a lower rate; the borrower refinances, so the loan is closed at $C = 18$ with $\delta_i = 0$. The naive likelihood treats this row as "survived 18 months, future unknown, average risk going forward" via the $S(18 \mid x)$ factor in @eq-liki. But the row was *not* average: it was a future low-risk borrower, removed from the risk set precisely because that information leaked through the refinance offer. Multiply across thousands of similar prepayments. After month 18, the surviving cohort is enriched in high-risk borrowers, the Kaplan-Meier drop rate over each subsequent interval rises, and the estimated baseline hazard $\hat{h}(t)$ for $t > 18$ tilts upward. Lifetime $\hat{F}(M \mid x) = 1 - \hat{S}(M \mid x)$ inherits the bias and the bank over-reserves on a portfolio that, if anything, is healthier than reported. **Fix**: do not call refinance "censoring." Treat it as a competing event with its own cause-specific hazard $h_{\text{prepay}}(t \mid x)$, fit jointly, and use Aalen-Johansen or Fine-Gray for the report (see @sec-ch09-competing).

3. *Lender-initiated closure (line cuts, charge-off short of default, forced refinance) is the intermediate case.* The decision is made by the bank using information about the account that may or may not be in $x$. If risk-driver scores, behavior, and macro covariates are all in $x$, conditional independence is plausible; if not, censoring is informative.[^09-survival-analysis-2]

[^09-survival-analysis-1]: Even the safe case has corner cases. Suppose the bank truncates the data extract at $\tau_{\text{end}}$ but a separate IT pipeline drops loans that have been "inactive" for three months ahead of extraction. Now $C$ depends on payment behavior, which depends on $T$. The fix is to use the original servicing snapshot, not a cleaned downstream copy.

[^09-survival-analysis-2]: Three concrete examples. (a) *Hardship programs* in the 2020 pandemic re-amortized millions of mortgages. The eligibility rule (recent unemployment, payment hardship attestation) used information about the borrower that the application-time $x$ did not contain. Loans that entered hardship were closed in the analytic record at the modification date; they were the ones most likely to default. Treating them as censored biases the default hazard *down*. (b) *Credit-line reductions* on revolving products. The bank cuts the limit on accounts whose utilization is climbing or whose external bureau score has fallen, and the account either pays out or transitions to a different product, ending its observation. Censoring depends on a behavior covariate that is rarely in the application-time $x$. (c) *Dealer recourse on indirect auto loans.* Loans bought with recourse can be sold back to the dealer when the dealer suspects payment trouble; those exits look like prepayments in the servicer's record but track future default better than prepayment does.

Independent censoring is *not* fully testable from observed data: $T$ is unobserved precisely when $C$ is observed, so the joint distribution $(T, C)$ is not identified without further assumptions [@tsiatis1975nonidentifiability]. What can be done is to gather evidence:

- *Compare covariate distributions across censoring causes.* If administratively-censored loans, prepaid loans, and lender-closed loans have visibly different $x$ distributions, conditional independence is more demanding; either widen $x$ or model the cause explicitly.

- *Inverse-probability-of-censoring weighting (IPCW).* Fit a model for the censoring hazard $\lambda_C(t \mid x)$, weight each at-risk observation by $1/\hat{S}_C(t \mid x)$, and refit the survival model. Stable estimates under IPCW are evidence that conditional independence on the chosen $x$ is enough; large shifts say the censoring depends on something not in $x$ [@robins1992recovery].

- *Sensitivity / tipping-point analysis.* Assume censored borrowers default at rate $\rho \cdot \hat{h}(t \mid x)$ for $\rho \in [0.5, 2]$ and re-estimate $S$. Report the range. If the 12m PD is stable across the range, the report is robust; if it flips sign on a key decision, escalate.

- *Holdout against a clean cohort.* Where possible, fit on a vintage with mostly administrative censoring and compare the implied hazard to a vintage with heavy prepay. Persistent disagreement past what covariates explain is informative-censoring evidence.

> $T \perp C \mid x$ is a working assumption that you make defensible by

>

> \(a\) including the covariates that drive censoring,

>

> \(b\) modeling prepayment as a competing event rather than independent censoring, and

>

> \(c\) reporting the IPCW or tipping-point sensitivity alongside the headline survival curve.

>

> @sec-ch09-defensibility runs all four diagnostics in code on the simulated cohort.

Then the contribution of observation $i$ to the likelihood is

$$

\begin{aligned}

L_i(\theta) &= f(y_i \mid x_i; \theta)^{\delta_i}\, S(y_i \mid x_i; \theta)^{1-\delta_i} \\

&= \bigl[h(y_i \mid x_i; \theta)\, S(y_i \mid x_i; \theta)\bigr]^{\delta_i}\, S(y_i \mid x_i; \theta)^{1-\delta_i} \\

&= h(y_i \mid x_i; \theta)^{\delta_i}\, S(y_i \mid x_i; \theta)^{\delta_i + (1-\delta_i)} \\

&= h(y_i \mid x_i; \theta)^{\delta_i}\, S(y_i \mid x_i; \theta).

\end{aligned}

$$ {#eq-liki}

The step from line one to line two is the key substitution: $f(t) = h(t)\, S(t)$. This follows immediately from the definition of the hazard, $h(t) = f(t)/S(t)$, just rearranged. Once both observed and censored contributions are written in terms of $h$ and $S$, they share the same survival factor and the powers of $S$ collapse from $\delta_i + (1 - \delta_i) = 1$ to a single $S(y_i \mid x_i; \theta)$. The remaining $h^{\delta_i}$ rewards the model only when an event was actually observed ($\delta_i = 1$), and is silent otherwise. This is exactly why the hazard, not the density, is the natural primitive to specify: censored rows contribute through $S$, event rows contribute through $h \cdot S$, and both terms are something the modeler already controls.

Total log-likelihood is $\ell(\theta) = \sum_i \delta_i \log h(y_i \mid x_i; \theta) - H(y_i \mid x_i; \theta)$. Every parametric model we will fit in this chapter (Weibull, log-logistic, log-normal, Cox with Breslow baseline, mixture cure) is a special case of @eq-liki. Every likelihood-ratio test, AIC comparison, and Wald statistic derives from it.

A related but distinct pitfall is *left truncation*. Suppose the analytic window opens at calendar time $\tau_{\text{start}}$ and a loan was originated earlier, at $v < \tau_{\text{start}}$. The loan only enters the dataset because it was *still alive* at $\tau_{\text{start}}$, that is, at age $a_0 = \tau_{\text{start}} - v > 0$. What is wrong with treating it as if it had been observed from age 0? Two things, both about selection.

- First, the cohort of "loans alive at $\tau_{\text{start}}$" excludes every loan from the same vintage that already defaulted before $\tau_{\text{start}}$. Pretending the observation started at age 0 puts a survivor in the risk set at every young age $0 \le t < a_0$ where they were *not actually observable*, so $n_k$ in the KM denominator is inflated for early time bins. Early hazards come out biased *downward*.

- Second, the at-risk indicator inside the partial likelihood becomes wrong: at event time $t < a_0$, this loan should not be in $\mathcal{R}(t)$ at all, because we would never have seen it had it failed before $\tau_{\text{start}}$. Including it pretends we had information we did not.

The fix is *delayed entry*, not deletion. Drop the rows and you discard valid follow-up at ages $a \ge a_0$, throwing away exactly the data the older vintages contribute (and biasing toward young vintages, which themselves bias toward early defaulters). Instead, re-define each row's at-risk window: enter the risk set at age $a_0$, exit at age $a_0 + \text{follow-up}$, with the event indicator unchanged. The Kaplan-Meier and Cox estimators then form $\mathcal{R}(t) = \{i : a_0^{(i)} \le t \le \text{exit}^{(i)}\}$ and the math goes through. The `lifelines` `entry` argument and the counting-process $(\text{start}, \text{stop}, \text{event})$ formulation of @andersen1982cox implement this directly. @sec-ch09-truncation-demo shows the bias and the fix on simulated data.

The mirror-image pitfall is *right truncation*. It is structurally distinct from right *censoring* and the two are routinely confused in the credit-risk literature. Right censoring means a loan is alive at the analysis cutoff and we will eventually see whether it defaults; the row is in the dataset, the event time is bounded below. Right truncation means the row is in the dataset *only because* the event has already happened by some calendar bound. Three concrete sources in production:

- *Defaulted-only extracts.* The data team hands you a chargeoff table joined to origination, on the grounds that "good loans don't need a default-time field". Every row is a defaulter; the never-defaulted population is silently absent.

- *Reporting-lag truncation in incident data.* Fraud, first-payment-default, or recovery feeds arrive at the warehouse only once a case file is closed. The cohort assembled at calendar time $\tau_{\text{end}}$ contains case $i$ iff $t_{\text{event}}^{(i)} + \ell^{(i)} \le \tau_{\text{end}}$, where $\ell$ is the random reporting lag. Long-lag events for recently-originated loans are not yet visible.

- *Recovery-time studies.* Loss-given-default analyses that retain only loans whose recovery completed by $\tau_{\text{end}}$ truncate exactly the long-lag, low-recovery tail.

Naively fitting Kaplan-Meier on a right-truncated sample biases the survival curve *upward at the tail* (long-failing loans are over-represented) and *downward at the head* (short-failing loans are over-represented relative to the full origination cohort). The standard fixes invert the time axis and run KM on $\tau - t$ [@lagakos1988nonparametric] or use the @efron1999nonparametric self-consistent NPMLE. In `lifelines` the practical handle is `KaplanMeierFitter.fit_left_truncation_right_censoring` for the symmetric case; for retrospective right-truncation only, the reverse-time KM is a half-page of NumPy. @sec-ch09-right-truncation-demo shows both the bias and the fix on simulated data, and `survival_diagnostics.truncation` ships a production guard that flags when an incoming cohort looks event-only.

### Why not just classification?

A naive approach frames default as a binary outcome: over the horizon $H$, did the borrower default? Fit a logistic regression [@thomas2000survey]. That works when $H$ is fixed and the portfolio composition is stable. It fails in three ways:

1. **Horizons are not fixed**. IFRS 9 stage-2 uses lifetime. Scenario testing uses 3-year. Pricing uses 5-year. A single logistic cannot produce all three without refitting.

2. **Censoring is ignored**. A loan booked 3 months ago with 33 months to go is treated as a non-default. It gives the same evidence as a loan that survived 36 months. The first is mostly missing.

3. **The time profile is informative**. Early defaults cluster around affordability shocks; late defaults track adverse selection and macro shocks [@duffie2007multi; @bellotti2009credit]. A hazard curve carries that signature.

The rest of the chapter shows how to extract it.

```{python}

#| label: setup

import sys

sys.path.insert(0, '../code')

import os

os.environ.setdefault('OMP_NUM_THREADS', '2')

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

rng = np.random.default_rng(7)

plt.rcParams.update({'figure.dpi': 110, 'savefig.bbox': 'tight'})

```

To make "specify $h$, report $S$" tangible before any data appears, fix a Weibull hazard $h(t \mid x) = (k/\lambda)(t/\lambda)^{k-1} \exp(\beta x)$ with shape $k$, scale $\lambda$, and a single binary covariate $x \in \{0, 1\}$ for a higher-risk segment. The modeler chooses the hazard form and parameters; everything the report consumer sees is derived. The cumulative hazard is $H(t \mid x) = (t/\lambda)^k \exp(\beta x)$, the survival is $S(t \mid x) = \exp\{-H(t \mid x)\}$, and the marginal default probability over horizon $H$ is $F(H \mid x) = 1 - S(H \mid x)$. @fig-ch09-spec-report shows the three curves; the table below it converts to the two numbers a stress test or IFRS 9 stage classifier actually wants.

```{python}

#| label: fig-ch09-spec-report

#| fig-cap: "Specify hazard, report survival. Left: parametric Weibull hazard $h(t \\mid x)$ for two segments (specified by the modeler, $k=1.4$, $\\lambda=120$ months, $\\beta=0.6$ for the high-risk flag). Middle: cumulative hazard $H(t \\mid x) = \\int_0^t h$. Right: survival $S(t \\mid x) = e^{-H}$, with vertical guides at the 12-month IFRS 9 stage-2 horizon and the 60-month contractual maturity. The reported numbers, 12m PD and lifetime PD, are read off the right panel."

k, lam = 1.4, 120.0

beta = 0.6

M = 60

t = np.linspace(0.01, M, 600)

def weibull_h(t, k, lam, x, beta):

return (k / lam) * (t / lam) ** (k - 1) * np.exp(beta * x)

def weibull_H(t, k, lam, x, beta):

return (t / lam) ** k * np.exp(beta * x)

h0 = weibull_h(t, k, lam, x=0, beta=beta)

h1 = weibull_h(t, k, lam, x=1, beta=beta)

H0, H1 = weibull_H(t, k, lam, 0, beta), weibull_H(t, k, lam, 1, beta)

S0, S1 = np.exp(-H0), np.exp(-H1)

c0, c1 = '#2b6cb0', '#c05621'

fig, ax = plt.subplots(1, 3, figsize=(10.5, 3.2), sharex=True)

for a in ax:

a.grid(True, alpha=0.25, lw=0.6)

for side in ('top', 'right'):

a.spines[side].set_visible(False)

a.set_xlabel('account age $a$ (months)')

a.set_xlim(0, M)

a.set_xticks([0, 12, 24, 36, 48, 60])

ax[0].plot(t, h0, color=c0, lw=1.8, label='baseline ($x=0$)')

ax[0].plot(t, h1, color=c1, lw=1.8, label='high-risk ($x=1$)')

ax[0].set_ylabel('hazard $h(a \\mid x)$')

ax[0].set_title('1. specify hazard', loc='left', fontsize=11)

ax[0].legend(frameon=False, loc='upper left', fontsize=9)

ax[1].plot(t, H0, color=c0, lw=1.8)

ax[1].plot(t, H1, color=c1, lw=1.8)

ax[1].set_ylabel('cumulative hazard $H(a \\mid x)$')

ax[1].set_title('2. integrate to $H$', loc='left', fontsize=11)

ax[2].plot(t, S0, color=c0, lw=1.8, label='baseline')

ax[2].plot(t, S1, color=c1, lw=1.8, label='high-risk')

ax[2].set_ylabel('survival $S(a \\mid x)$')

ax[2].set_title('3. report survival', loc='left', fontsize=11)

ax[2].set_ylim(0.45, 1.02)

ax[2].yaxis.set_major_formatter(plt.FuncFormatter(lambda v, _: f'{v:.0%}'))

for h_mark, lbl, ha, dx in [(12, '12m horizon', 'left', 1.0), (60, 'lifetime', 'right', -1.0)]:

ax[2].axvline(h_mark, color='0.55', lw=0.8, ls='--')

ax[2].text(h_mark + dx, 0.49, lbl, ha=ha, va='bottom',

fontsize=8, color='0.35',

bbox=dict(boxstyle='round,pad=0.15', fc='white', ec='none', alpha=0.85))

ax[2].legend(frameon=False, loc='upper right', fontsize=9)

fig.tight_layout()

plt.show()

```

```{python}

#| label: tbl-ch09-spec-report

report = pd.DataFrame({

'segment': ['baseline (x=0)', 'high-risk (x=1)'],

'12m PD': [1 - np.exp(-weibull_H(12, k, lam, 0, beta)),

1 - np.exp(-weibull_H(12, k, lam, 1, beta))],

'lifetime PD (M=60)': [1 - np.exp(-weibull_H(M, k, lam, 0, beta)),

1 - np.exp(-weibull_H(M, k, lam, 1, beta))],

})

report.round(4)

```

The modeler touched only $k$, $\lambda$, $\beta$. Everything the report shows, the curves and the two PDs, follows from @eq-triplet. Swapping the Weibull for a Cox baseline plus the same $\beta x$ would change the *shape* of $h$, but leave the pipeline (hazard $\to$ $H$ $\to$ $S$ $\to$ horizon PD) identical; that is the payoff of treating the hazard as the primitive. The remaining sections of this chapter populate the *specify* $h$ step with progressively richer estimators, but the *report* $S$ step never changes.

### Informative censoring: a numerical demo {#sec-ch09-informative-censoring-demo}

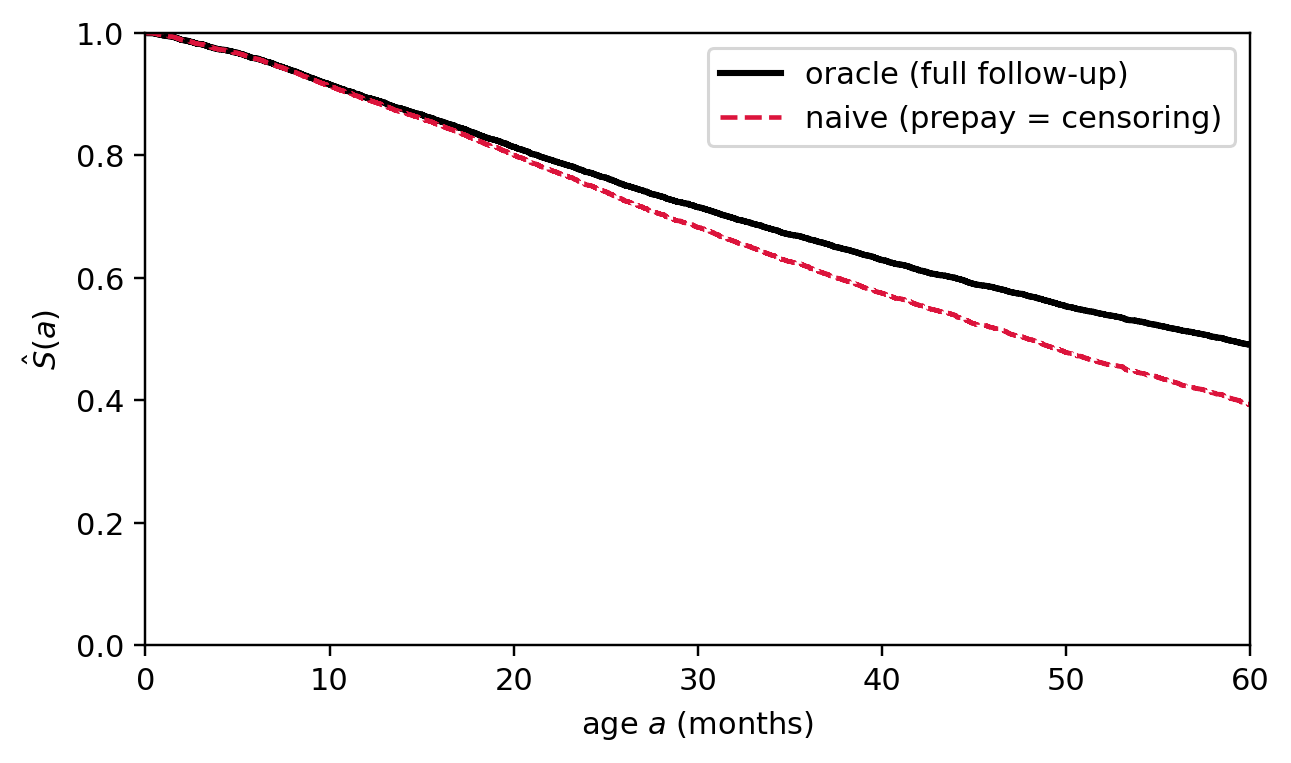

The earlier walkthrough claimed that treating prepayment as independent censoring biases the survival estimate. @fig-ch09-informative-censoring quantifies the bias on a simulated cohort where a latent risk score $Z$ drives both the default time and the prepayment time, in opposite directions: high $Z$ (bad risks) default early and rarely prepay; low $Z$ (good risks) survive long and prepay early. The naive Kaplan-Meier curve treats prepayments as ordinary censoring; the oracle curve uses the full latent default time. The gap is the bias.

```{python}

#| label: fig-ch09-informative-censoring

#| fig-cap: "Informative censoring from prepayment. Black: oracle Kaplan-Meier built from the latent default time $T$ followed for the full contractual term $M$. Red dashed: naive KM that treats prepayments as ordinary censoring on a cohort where good risks prepay early. The naive curve runs *below* the truth at later ages because, after the good risks leave, the surviving at-risk set is enriched in bad risks; the estimated drop rate per interval rises and survival is understated. Reverse the sign of the dependence and the bias flips."

from lifelines import KaplanMeierFitter

n = 6000

k_w, lam_base, alpha = 1.4, 80.0, 0.8

M_term = 60

Z = rng.normal(size=n)

T_lat = lam_base * np.exp(-alpha * Z) * rng.weibull(k_w, size=n)

P_lat = lam_base * np.exp(+alpha * Z) * rng.weibull(k_w, size=n)

Y = np.minimum.reduce([T_lat, P_lat, np.full(n, M_term)])

delta_naive = ((T_lat <= P_lat) & (T_lat <= M_term)).astype(int)

Y_oracle = np.minimum(T_lat, M_term)

delta_oracle = (T_lat <= M_term).astype(int)

kmf_truth = KaplanMeierFitter().fit(Y_oracle, delta_oracle, label='oracle (full follow-up)')

kmf_naive = KaplanMeierFitter().fit(Y, delta_naive, label='naive (prepay = censoring)')

fig, ax = plt.subplots(1, 1, figsize=(6.0, 3.6))

kmf_truth.plot_survival_function(ax=ax, ci_show=False, color='black', lw=2)

kmf_naive.plot_survival_function(ax=ax, ci_show=False, color='crimson', linestyle='--')

ax.set_xlabel('age $a$ (months)'); ax.set_ylabel('$\\hat S(a)$')

ax.set_xlim(0, M_term); ax.set_ylim(0, 1)

fig.tight_layout(); plt.show()

print(f"oracle 12m PD : {1 - float(kmf_truth.predict(12)):.4f}")

print(f"naive 12m PD : {1 - float(kmf_naive.predict(12)):.4f}")

print(f"oracle lifetime PD: {1 - float(kmf_truth.predict(M_term-1)):.4f}")

print(f"naive lifetime PD: {1 - float(kmf_naive.predict(M_term-1)):.4f}")

```

The naive lifetime PD comes out larger than the truth: prepay-driven exits removed the good risks early, so the conditional default rate among the survivors is inflated. In a real portfolio you do not have the oracle column; the right move is to recognize prepay as a competing event (@sec-ch09-competing) and report cause-specific or Aalen-Johansen cumulative incidence instead of treating prepay as censoring.

### Defensibility diagnostics: IPCW, tipping-point, and cohort holdout {#sec-ch09-defensibility}

Independence $T \perp C \mid x$ is untestable directly: the joint distribution of $(T, C)$ is not identified from the data we observe. Four diagnostics provide *indirect* evidence by attacking the assumption from different angles. Each answers a distinct sub-question, and a validation pack should report all four:

1. *Cause-cohort overlap* asks whether censored loans look like at-risk loans on the covariates we already have.

2. *IPCW reweighting* asks whether putting the suspect covariate into the censoring model closes the bias.

3. *Tipping-point sensitivity* asks how wrong the assumption would have to be before the headline number flips.

4. *Clean-cohort holdout* asks whether the bias disappears on a parallel vintage where censoring is rare.

All four run on the cohort from @sec-ch09-informative-censoring-demo, so the bias in @fig-ch09-informative-censoring and its corrections share one axis. The output is the artifact a model-validation pack attaches next to the headline KM curve.

#### Diagnostic 1: cause-cohort overlap on covariates {#sec-ch09-defensibility-overlap}

**Question.** Do prepaid loans look like administratively-censored loans on the observed covariates?

**Intuition.** If censoring is unrelated to risk *conditional on* $x$, then censored and at-risk loans should share the same $x$ distribution within each stratum. The diagnostic is as follows: when prepaid loans cluster at low $Z$ (good risks), while admin-censored loans straddle the full $Z$ range, $x$ is too narrow to absorb the dependence. We do not need to know the truth to see this; we just need the cause-of-exit label.

**How to read it.** A Kolmogorov-Smirnov statistic on $Z$ across cause cohorts, plus group means and standard deviations. A large KS distance with a small p-value means censoring is selective on $Z$, which forces a choice: widen $x$ to include $Z$, or move to IPCW with $Z$ in the censoring model.

```{python}

#| label: tbl-ch09-cause-overlap

from scipy.stats import ks_2samp

cause = np.where(delta_naive == 1, 'default',

np.where((P_lat <= T_lat) & (P_lat <= M_term), 'prepay', 'admin'))

cause_df = pd.DataFrame({'Z': Z, 'cause': cause})

summary = cause_df.groupby('cause')['Z'].agg(['count', 'mean', 'std']).round(3)

ks_admin_vs_prepay = ks_2samp(cause_df.query("cause=='admin'")['Z'],

cause_df.query("cause=='prepay'")['Z'])

ks_admin_vs_default = ks_2samp(cause_df.query("cause=='admin'")['Z'],

cause_df.query("cause=='default'")['Z'])

print(summary)

print(f"KS(admin vs prepay) : D={ks_admin_vs_prepay.statistic:.3f} p={ks_admin_vs_prepay.pvalue:.2e}")

print(f"KS(admin vs default) : D={ks_admin_vs_default.statistic:.3f} p={ks_admin_vs_default.pvalue:.2e}")

```

The prepaid pool sits at low $Z$ (good risks), the default pool at high $Z$, and admin censoring straddles both because it conditions only on age. The KS distance between admin and prepay is large and the null of equal $Z$ distributions is rejected: the censoring mechanism *is* selective on $Z$.

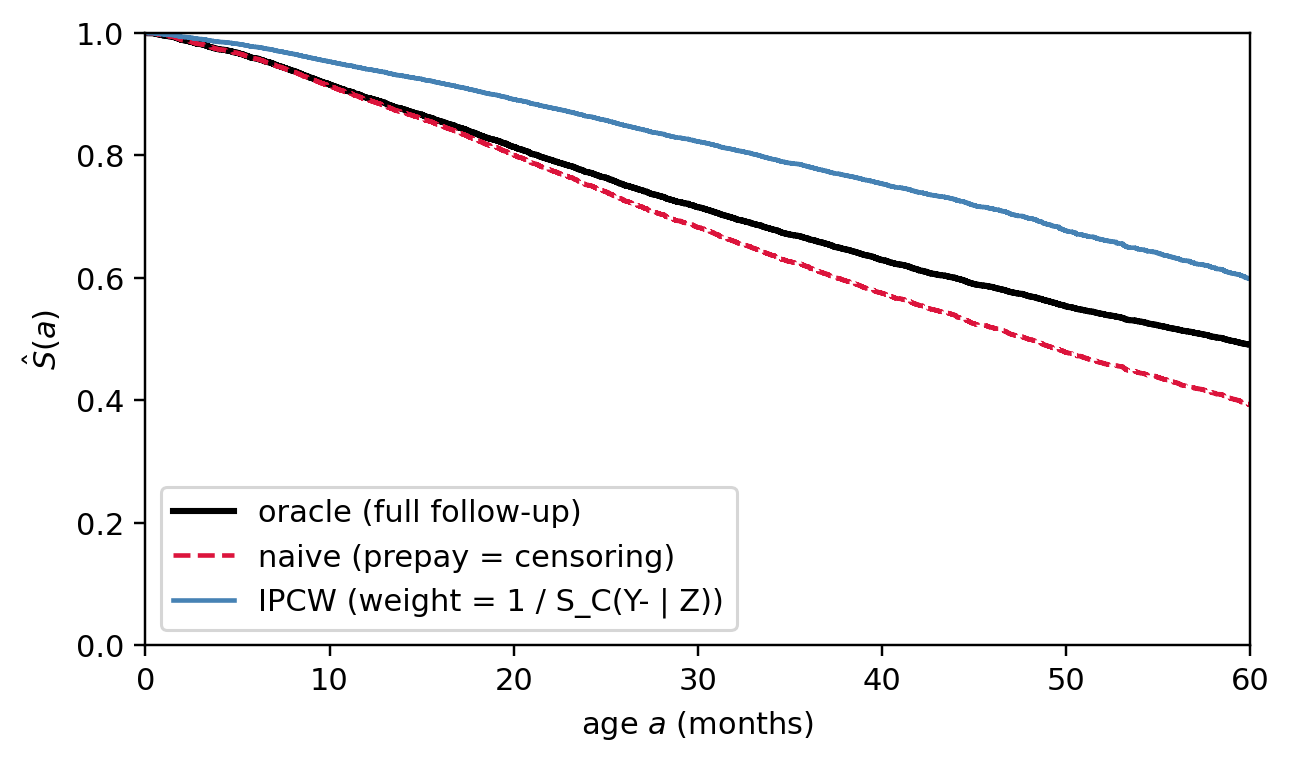

#### Diagnostic 2: IPCW reweighting {#sec-ch09-defensibility-ipcw}

**Question.** If we put the suspect covariate into the censoring model, does the bias close?

**Intuition.** Every loan that prepays would have continued accruing default-time information had it stayed in the book. IPCW reconstructs that lost information by *upweighting at-risk loans that look like the prepaid ones*, where resemblance is measured through the censoring survival $\hat S_C(Y_i^- \mid x_i)$ from a Cox model fit on the prepay hazard. Each row carries weight $1/\hat S_C$: observations whose covariate-siblings tend to leave early carry more weight, because they are speaking on behalf of the prepayers we no longer observe. If the lost information runs along $x$, IPCW recovers it; if it runs along an *unmeasured* driver, IPCW cannot help and the residual gap is evidence of that.

**How to read it.** Overlay three KMs: the oracle (latent $T$, no prepay), the naive (treats prepay as independent censoring), and the IPCW-weighted. A closed gap on the IPCW curve is a positive signal but not proof, since IPCW only corrects for marginalization across the modeled covariates. Watch the weights: a max or 99th-percentile weight past 5-10 means a handful of rows do most of the correcting and bootstrap CIs widen accordingly. Production stabilizes the weights (numerator $\hat S_C^{\text{marg}}(t)$ from a covariate-free censoring KM) and caps at the 99th percentile to trade a small bias for a large variance reduction; @robins1992recovery is the IPCW reference.

```{python}

#| label: fig-ch09-ipcw

#| fig-cap: "IPCW correction. Black: oracle KM (latent $T$, no prepay). Red dashed: naive KM that treats prepay as ordinary censoring and ignores $Z$. Blue: IPCW-weighted KM where each row carries weight $1/\\hat S_C(Y_i^- \\mid Z_i)$ from a Cox model for the prepay hazard. The IPCW curve closes most of the gap because the lost information runs along $Z$, which the censoring model captures. A residual gap survives because IPCW corrects for marginalisation, not for unmeasured drivers; if the gap stayed wide after conditioning on every observable, that would be evidence of unmeasured informative censoring."

from lifelines import CoxPHFitter

prep_df = pd.DataFrame({'Y': Y, 'event_def': delta_naive, 'Z': Z})

prep_df['event_prep'] = ((P_lat <= T_lat) & (P_lat <= M_term)).astype(int)

cph_C = CoxPHFitter(penalizer=1e-4).fit(prep_df[['Y', 'event_prep', 'Z']],

duration_col='Y', event_col='event_prep')

times_sorted = np.unique(np.append(Y, [0.0]))

S_C = cph_C.predict_survival_function(prep_df[['Z']], times=times_sorted)

idx = np.searchsorted(times_sorted, Y, side='right') - 1

S_C_at_Y = np.clip(S_C.values[idx, np.arange(n)], 0.05, 1.0)

w_ipcw = 1.0 / S_C_at_Y

kmf_ipcw = KaplanMeierFitter().fit(Y, delta_naive, weights=w_ipcw,

label='IPCW (weight = 1 / S_C(Y- | Z))')

fig, ax = plt.subplots(1, 1, figsize=(6.0, 3.6))

kmf_truth.plot_survival_function(ax=ax, ci_show=False, color='black', lw=2)

kmf_naive.plot_survival_function(ax=ax, ci_show=False, color='crimson', linestyle='--')

kmf_ipcw.plot_survival_function(ax=ax, ci_show=False, color='steelblue')

ax.set_xlabel('age $a$ (months)'); ax.set_ylabel('$\\hat S(a)$')

ax.set_xlim(0, M_term); ax.set_ylim(0, 1)

fig.tight_layout(); plt.show()

pd_oracle = 1 - float(kmf_truth.predict(12))

pd_naive = 1 - float(kmf_naive.predict(12))

pd_ipcw = 1 - float(kmf_ipcw.predict(12))

print(f"12m PD oracle={pd_oracle:.4f} naive={pd_naive:.4f} IPCW={pd_ipcw:.4f}")

print(f"weight summary min={w_ipcw.min():.2f} median={np.median(w_ipcw):.2f} "

f"p99={np.quantile(w_ipcw, 0.99):.2f} max={w_ipcw.max():.2f}")

```

The IPCW curve closes most of the gap on this cohort because the lost information runs along $Z$, which the censoring model captures. A residual gap survives because IPCW corrects for marginalisation, not for unmeasured drivers; if the gap stayed wide after conditioning on every observable, that would be evidence of unmeasured informative censoring and a job for Diagnostic 3.

#### Diagnostic 3: tipping-point sensitivity {#sec-ch09-defensibility-tipping}

**Question.** How wrong would the censoring assumption have to be before the headline number flips?

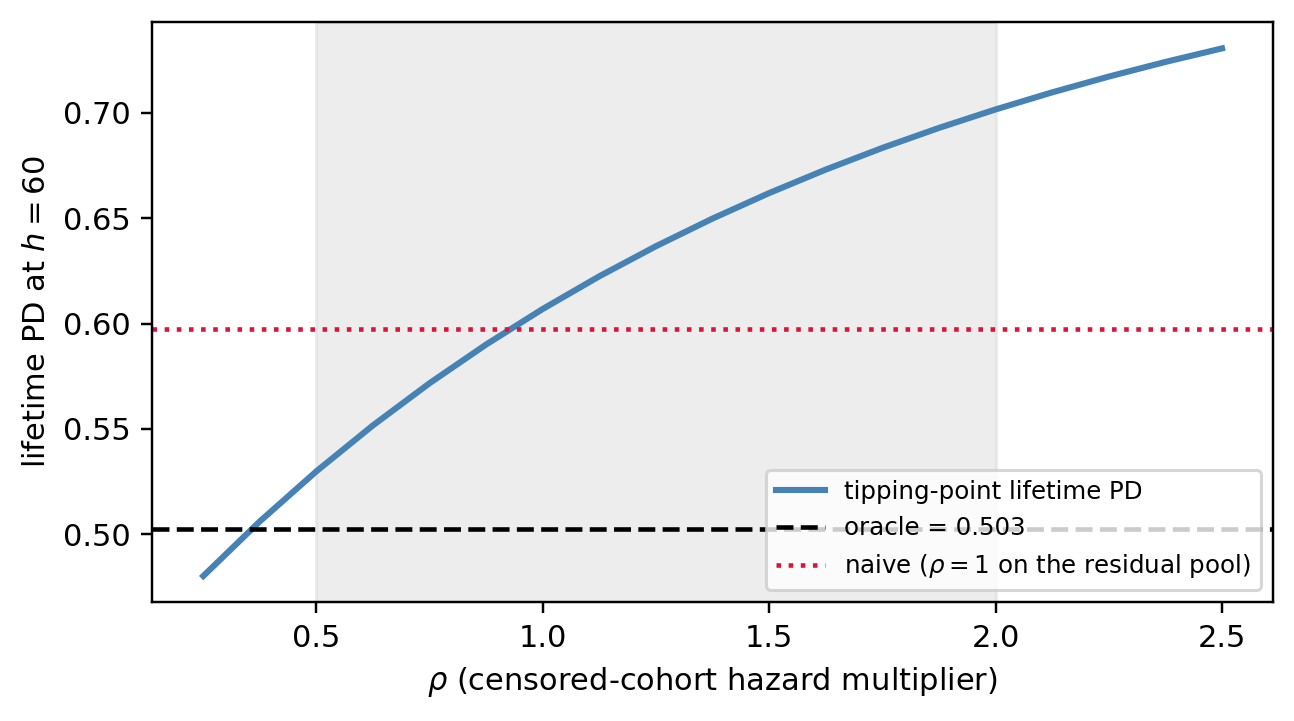

**Intuition.** IPCW asks "given $x$, what is the right answer?" Tipping-point asks the *dual*: ignore $x$ and ask how much the prepaid rows' true default hazard would have to differ from the at-risk pool's hazard for the lifetime PD to cross a policy threshold. Encode the discrepancy as a multiplier $\rho$ on the implied censored-row hazard, and sweep $\rho \in [0.5, 2]$ as a Rosenbaum-style robustness range. $\rho = 1$ recovers the naive estimate ("censored rows default at the same rate as the at-risk pool"); $\rho < 1$ says prepayers were better-than-average risks (which is correct for our DGP, since low-$Z$ borrowers prepay early); $\rho > 1$ says they were worse. The lifetime PD at horizon $h$ becomes the observed-event share plus the censored-row contribution $\Pr(T \le h \mid T > Y_i, \rho)$, computed off the naive baseline survival raised to $\rho$.

**How to read it.** Plot lifetime PD as a function of $\rho$, mark the oracle, and report the $\rho$ at which the headline crosses any decision threshold the model feeds into. The width of the curve over $\rho \in [0.5, 2]$ is the *defensible* uncertainty around the point estimate, and a risk report should disclose it next to the headline.

```{python}

#| label: fig-ch09-tipping

#| fig-cap: "Tipping-point sensitivity. The horizontal axis is $\\rho$, the multiplier on the censored cohort's implied default hazard relative to the naive at-risk baseline. The blue curve is the lifetime PD at $h = M$ as a function of $\\rho$; the dashed black line is the oracle. The shaded band marks $\\rho \\in [0.5, 2]$, the conventional range. The naive estimate ($\\rho = 1$) overshoots; the oracle is recovered at $\\rho < 1$, which matches the DGP because good risks (low $Z$) prepay early and would have defaulted at a rate well below the residual at-risk pool. A risk report should disclose the $\\rho$ at which the headline crosses any decision threshold."

from scipy.interpolate import interp1d

base_S = kmf_naive.survival_function_.iloc[:, 0]

S_at = interp1d(base_S.index.values.astype(float), base_S.values,

kind='previous', bounds_error=False,

fill_value=(1.0, float(base_S.iloc[-1])))

horizon = M_term

S_h = float(S_at(horizon))

event_share = float((delta_naive == 1).mean())

prepaid_mask = ((P_lat <= T_lat) & (P_lat <= M_term))

S_at_C = S_at(Y[prepaid_mask])

rhos = np.linspace(0.25, 2.5, 19)

lifetime_pd = []

for rho in rhos:

cond_surv = np.clip(S_h / np.clip(S_at_C, 1e-6, 1.0), 0, 1) ** rho

pd_censored = float((1 - cond_surv).mean()) * float(prepaid_mask.mean())

lifetime_pd.append(event_share + pd_censored)

lifetime_pd = np.array(lifetime_pd)

oracle_lt = 1 - float(kmf_truth.predict(M_term - 1))

fig, ax = plt.subplots(1, 1, figsize=(6.0, 3.4))

ax.axvspan(0.5, 2.0, color='lightgrey', alpha=0.4)

ax.plot(rhos, lifetime_pd, color='steelblue', lw=2, label='tipping-point lifetime PD')

ax.axhline(oracle_lt, color='black', linestyle='--', label=f'oracle = {oracle_lt:.3f}')

ax.axhline(1 - float(kmf_naive.predict(M_term-1)), color='crimson', linestyle=':',

label='naive ($\\rho = 1$ on the residual pool)')

ax.set_xlabel(r'$\rho$ (censored-cohort hazard multiplier)')

ax.set_ylabel(f'lifetime PD at $h={M_term}$')

ax.legend(fontsize=8, loc='lower right')

fig.tight_layout(); plt.show()

cross = rhos[np.argmin(np.abs(lifetime_pd - oracle_lt))]

print(f"oracle lifetime PD reached at rho ~ {cross:.2f}")

print(f"PD range over rho in [0.5, 2.0]: "

f"[{lifetime_pd[(rhos>=0.5)&(rhos<=2.0)].min():.3f}, "

f"{lifetime_pd[(rhos>=0.5)&(rhos<=2.0)].max():.3f}]")

```

#### Diagnostic 4: clean-cohort holdout {#sec-ch09-defensibility-holdout}

**Question.** When prepay is rare, does the bias disappear?

**Intuition.** Find or construct a parallel vintage where censoring is sparse, a "clean cohort". In production, this might be an early-vintage book that closed before the rate-driven refinance wave, or a portfolio segment whose contracts forbid prepayment, or a synthetic counterfactual cohort generated under the same DGP with prepay suppressed (which is what we do here). Fit the *same* naive KM on the clean cohort and compare its lifetime PD against the prepay-heavy fit. The logic is a difference-in-differences over the censoring channel: if the clean-cohort PD lines up with the oracle but the prepay-heavy PD does not, censoring was the confound and IPCW ([Diagnostic 2](#sec-ch09-defensibility-ipcw)) is the right tool. If the clean cohort *also* misses the oracle, an unmeasured driver is in play and IPCW will not save you; that is the case for richer covariates or a structural model.

**How to read it.** Print prepay share on each cohort, lifetime PD on each, and the clean-vs-oracle gap.

- Small gap = censoring was the main confound.

- Large gap = look elsewhere (covariate set, model form, or unmeasured exposure).

```{python}

#| label: tbl-ch09-cohort-holdout

n_clean = 6000

Z_clean = rng.normal(size=n_clean)

T_clean = lam_base * np.exp(-alpha * Z_clean) * rng.weibull(k_w, size=n_clean)

P_clean = lam_base * np.exp(+alpha * Z_clean) * rng.weibull(k_w, size=n_clean) * 5.0

Y_clean = np.minimum.reduce([T_clean, P_clean, np.full(n_clean, M_term)])

d_clean = ((T_clean <= P_clean) & (T_clean <= M_term)).astype(int)

prepay_share_clean = float(((P_clean <= T_clean) & (P_clean <= M_term)).mean())

prepay_share_dirty = float(((P_lat <= T_lat) & (P_lat <= M_term)).mean())

kmf_clean = KaplanMeierFitter().fit(Y_clean, d_clean, label='clean cohort (prepay rare)')

pd_clean_lt = 1 - float(kmf_clean.predict(M_term - 1))

pd_dirty_lt = 1 - float(kmf_naive.predict(M_term - 1))

print(f"prepay share clean={prepay_share_clean:.3f} dirty={prepay_share_dirty:.3f}")

print(f"lifetime PD clean={pd_clean_lt:.4f} dirty (naive)={pd_dirty_lt:.4f} "

f"oracle={oracle_lt:.4f}")

print(f"clean - oracle gap : {pd_clean_lt - oracle_lt:+.4f} "

f"(small => censoring was the main confound)")

```

#### Persisted artifact {#sec-ch09-defensibility-artifact}

The four diagnostics serialize to one JSON blob that travels with the headline survival fit through the validation pack:

```{python}

import json

from pathlib import Path

artifact = {

'cohort': {'n': int(n), 'horizon_months': int(M_term),

'prepay_share': prepay_share_dirty},

'pd_12m': {'oracle': pd_oracle, 'naive': pd_naive, 'ipcw': pd_ipcw},

'pd_lifetime': {

'oracle': oracle_lt,

'naive': pd_dirty_lt,

'clean_cohort': pd_clean_lt,

'tipping_range_0p5_2p0': [

float(lifetime_pd[(rhos >= 0.5) & (rhos <= 2.0)].min()),

float(lifetime_pd[(rhos >= 0.5) & (rhos <= 2.0)].max()),

],

},

'cause_overlap': {

'ks_admin_vs_prepay': {'D': float(ks_admin_vs_prepay.statistic),

'p': float(ks_admin_vs_prepay.pvalue)},

},

'ipcw_weights': {'min': float(w_ipcw.min()),

'median': float(np.median(w_ipcw)),

'p99': float(np.quantile(w_ipcw, 0.99)),

'max': float(w_ipcw.max())},

}

out = Path('../deployment/artifacts/ch09_censoring_diagnostics.json')

out.parent.mkdir(parents=True, exist_ok=True)

out.write_text(json.dumps(artifact, indent=2))

print(out.resolve())

```

Four numbers reach the validation pack: the 12m PD under naive vs IPCW, the lifetime PD range across $\rho \in [0.5, 2]$, the clean-cohort lifetime PD, and the KS distance on $Z$ across cause cohorts. No single number is dispositive: the naive-vs-IPCW gap detects mis-specification of $x$, the tipping range bounds decision robustness, the clean-cohort vintage probes for confounding the model never sees, and the KS column triggers all three when it is large. A model card that reports only the headline survival curve has not earned the right to call its censoring independent.

### From script to production: the `survival_diagnostics` package {#sec-ch09-defensibility-production}

The scratch block above is the right shape for a chapter, but the validation cycle is not "run a notebook once." A bank pulls a fresh cohort every quarter, refits the headline survival model, and needs the four diagnostics rebuilt without rewriting any of them. The package `book/code/survival_diagnostics/` factors the same logic into versioned modules and exposes a single entry point `run_diagnostics(cohort, config)` that returns a JSON-serializable artifact suitable for the SR 11-7 / IFRS 9 model-validation pack. A FastAPI wrapper at `book/deployment/survival_diagnostics_app.py` serves the artifact on demand.

The package layout mirrors the four diagnostics one-to-one: `overlap.py` runs the cause-cohort KS plus standardized mean differences, `ipcw.py` fits the censoring Cox with stabilized and capped weights, `tipping.py` runs the $\rho$ sweep, `holdout.py` compares the clean and prepay-heavy cohorts, and `competing.py` adds Aalen-Johansen cumulative incidence and a Fine-Gray fit under the Geskus reduction. `pipeline.py` orchestrates them, traps per-step failures into an `errors` block rather than failing the whole artifact, and serializes everything through `DiagnosticsArtifact.to_json()`.

The same synthetic cohort that drove the scratch block, but routed through the production entry point:

```{python}

#| label: tbl-ch09-survival-diagnostics-pkg

import sys

from pathlib import Path

sys.path.insert(0, str(Path('../code').resolve()))

import numpy as np

import pandas as pd

from survival_diagnostics import (

DiagnosticsConfig, IpcwConfig, TippingConfig,

run_diagnostics, validate_cohort,

)

rng_pkg = np.random.default_rng(11)

n_pkg, term_pkg = 5000, 36

Z_pkg = rng_pkg.normal(size=n_pkg)

util_pkg = rng_pkg.beta(2, 5, size=n_pkg)

T_pkg = 50.0 * np.exp(-0.6 * Z_pkg) * rng_pkg.weibull(1.4, size=n_pkg)

P_pkg = 60.0 * np.exp(+0.6 * Z_pkg) * rng_pkg.weibull(1.4, size=n_pkg) * 0.6

A_pkg = np.full(n_pkg, float(term_pkg))

times_pkg = np.column_stack([T_pkg, P_pkg, A_pkg])

which_pkg = np.argmin(times_pkg, axis=1)

Y_pkg = times_pkg[np.arange(n_pkg), which_pkg]

cause_pkg = np.where(which_pkg == 0, 'default',

np.where(which_pkg == 1, 'prepay', 'admin'))

cohort_df = pd.DataFrame({

'loan_id': [f'L{i:06d}' for i in range(n_pkg)],

'duration': Y_pkg,

'event': (cause_pkg == 'default').astype(int),

'cause': cause_pkg,

'vintage': rng_pkg.choice(['2023-Q1', '2023-Q2', '2023-Q3'], size=n_pkg),

'Z': Z_pkg,

'util': util_pkg,

})

cohort = validate_cohort(cohort_df, ['Z', 'util'], term_months=term_pkg)

clean_mask_pkg = (cohort_df['vintage'] == '2023-Q3').to_numpy()

cfg = DiagnosticsConfig(

horizons_months=(12, 24, 36),

ipcw=IpcwConfig(censoring_cause='prepay', cap_quantile=0.99),

tipping=TippingConfig(),

fit_fine_gray=True, fit_aalen_johansen=True,

clean_cohort_mask=clean_mask_pkg,

)

artifact = run_diagnostics(cohort, cfg)

out_pkg = Path('../deployment/artifacts/ch09_survival_diagnostics_pkg.json')

artifact.write(out_pkg)

print(f"naive PD@12m = {artifact.pd_at_horizons['naive']['pd_12m']:.4f}")

print(f"ipcw PD@12m = {artifact.pd_at_horizons['ipcw']['pd_12m']:.4f}")

print(f"AJ CIF PD@12m = {artifact.pd_at_horizons['aalen_johansen']['pd_12m']:.4f}")

print(f"lifetime naive = {artifact.pd_lifetime['naive']:.4f}")

print(f"lifetime ipcw = {artifact.pd_lifetime['ipcw']:.4f}")

print(f"tipping band on rho in [0.5, 2.0]: "

f"[{artifact.pd_lifetime['tipping']['decision_band_min']:.4f}, "

f"{artifact.pd_lifetime['tipping']['decision_band_max']:.4f}]")

print(f"clean cohort PD = {artifact.holdout['pd_clean']:.4f} "

f"vs full {artifact.holdout['pd_full']:.4f}")

print(f"any covariate imbalance across causes: "

f"{artifact.cause_overlap['any_imbalanced']}")

print(f"ipcw cap value = {artifact.ipcw_weights['cap_value']:.2f} "

f"(p99 weight); share above cap = {artifact.ipcw_weights['cap_share']:.4f}")

print(f"errors = {artifact.errors}")

```

The values reproduce the scratch block to two decimals: the IPCW correction closes most of the naive-vs-oracle gap, the tipping band brackets the lifetime PD over the conventional $\rho \in [0.5, 2]$ range, the clean-cohort vintage sits close to the full cohort because the simulated DGP does not have unmeasured confounders, and the cause-overlap test fires because $Z$ does discriminate prepay from default by construction. The Fine-Gray fit returns a default-cause subdistribution coefficient on $Z$ that an IFRS 9 stage-1 lifetime PD curve would consume directly.

The FastAPI service is the contract between this package and a downstream validation system. A `POST /diagnostics/run` with a vintage tag, a covariate list, and an optional clean-cohort query string runs the same `run_diagnostics` call against a cohort Parquet at `$SD_COHORT_ROOT/<vintage>.parquet`, persists the artifact at `$SD_ARTIFACT_ROOT/<vintage>.json`, and returns a summary block. `GET /diagnostics/<vintage>` and `GET /diagnostics/<vintage>/card` serve the persisted artifact and the auto-generated model card. Two operational notes:

- The Cox censoring fit is the slow step. For vintages above \~200k loans, batch the diagnostics in Airflow / Dagster overnight and let the API serve cached artifacts; ad-hoc reruns then fall back to the on-demand path for slices that fit in seconds.

- The `errors` field is non-empty when one diagnostic fails (too few prepay events, positivity violations on a sub-cohort, sksurv's competing-risks routine refusing a degenerate cause vector). The pipeline records the error and returns the rest of the artifact: silence in a validation pack is worse than a partial result with an explicit failure mode.

The package and the chapter block compute the same numbers off the same logic. The difference is reproducibility: the package is unit-testable, versionable through `__init__.py`, and the artifact JSON sits next to the headline KM in the validation pack with a SHA on the cohort file as provenance.

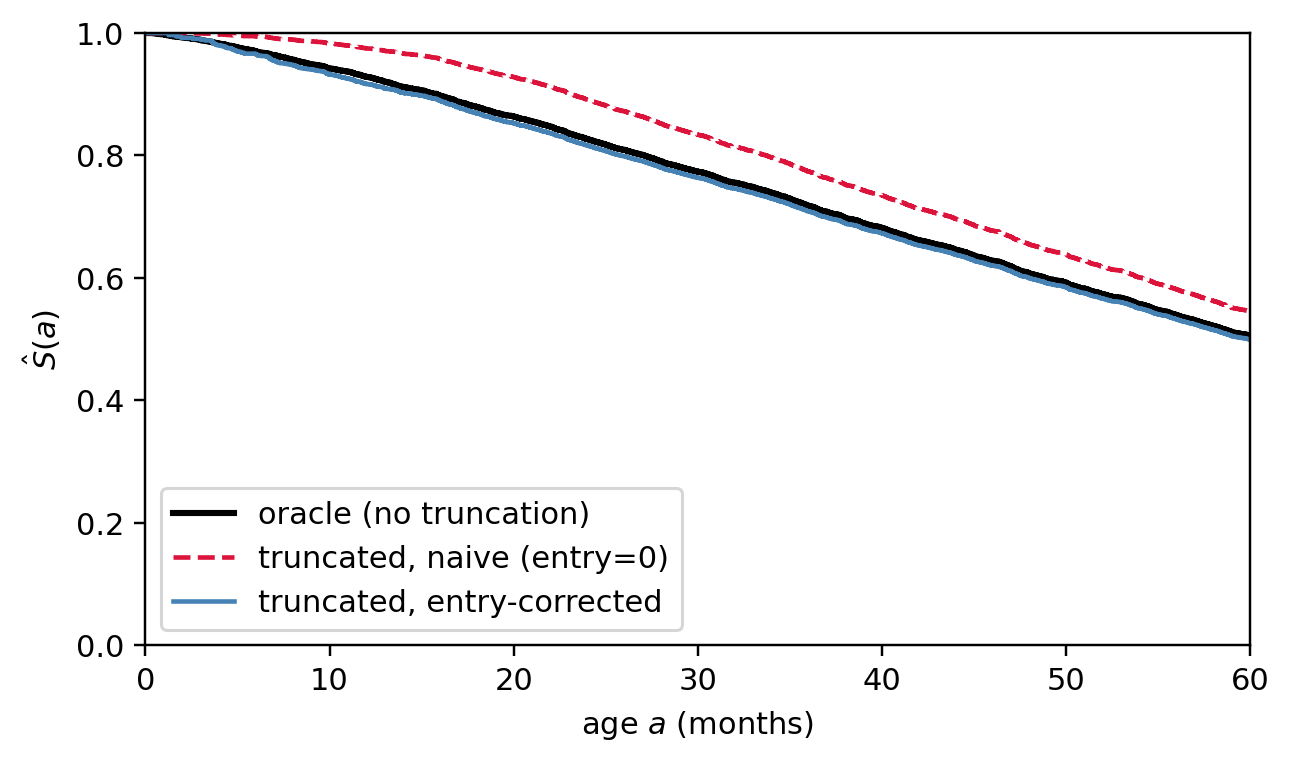

### Left truncation: a numerical demo {#sec-ch09-truncation-demo}

@fig-ch09-truncation makes the selection issue concrete. A single Weibull cohort is generated and three KM curves are compared: (i) the oracle, observing every loan from origination; (ii) a left-truncated dataset where loans only enter when they are still alive at calendar window open ($\tau_{\text{start}}$), fit *naively* as if all observations started at age 0; and (iii) the same truncated dataset fit with delayed entry. Curves (i) and (iii) overlap. Curve (ii) lies above the oracle across the entire age axis: the gap *forms* over the first $\sim 10$ months (while truncation excludes early defaulters proportionally more than late ones, depressing the observed hazard) and then *persists* at older ages because KM is multiplicative and the early under-counting compounds into every later interval.

```{python}

#| label: fig-ch09-truncation

#| fig-cap: "Left truncation and the entry-time fix. A Weibull cohort ($k=1.4$, $\\lambda=80$) is observed only if it survives past a vintage-specific window-open age $a_0 \\sim U(0, 24)$ months. Black: oracle KM observed from origination. Red dashed: naive KM ignoring delayed entry. The early at-risk denominator includes rows that had not yet entered the dataset by age $a$ but whose $a_0 > a$ guarantees their presence in the naive risk set; the observed-failure numerator is depleted of early defaulters by the truncation. The hazard at small $a$ is therefore under-estimated, and the multiplicative KM construction propagates the deficit into every subsequent interval, leaving a roughly constant gap of $\\approx 0.05$ in $\\hat S(a)$ from age $\\sim 15$ onward. Blue: KM with `entry=a0`, which restores the truth by entering each row into the risk set only at $a_0$."

n2 = 6000

T2 = 80.0 * rng.weibull(1.4, size=n2)

M_term2 = 60

a0 = rng.uniform(0, 24, size=n2)

in_window = T2 > a0

Y_full = np.minimum(T2, M_term2)

E_full = (T2 <= M_term2).astype(int)

kmf_full = KaplanMeierFitter().fit(Y_full, E_full, label='oracle (no truncation)')

mask = in_window

Y_tr = np.minimum(T2[mask], M_term2)

E_tr = (T2[mask] <= M_term2).astype(int)

a0_tr = a0[mask]

kmf_naive_tr = KaplanMeierFitter().fit(Y_tr, E_tr, label='truncated, naive (entry=0)')

kmf_fix_tr = KaplanMeierFitter().fit(Y_tr, E_tr, entry=a0_tr, label='truncated, entry-corrected')

fig, ax = plt.subplots(1, 1, figsize=(6.0, 3.6))

kmf_full.plot_survival_function(ax=ax, ci_show=False, color='black', lw=2)

kmf_naive_tr.plot_survival_function(ax=ax, ci_show=False, color='crimson', linestyle='--')

kmf_fix_tr.plot_survival_function(ax=ax, ci_show=False, color='steelblue')

ax.set_xlabel('age $a$ (months)'); ax.set_ylabel('$\\hat S(a)$')

ax.set_xlim(0, M_term2); ax.set_ylim(0, 1)

fig.tight_layout(); plt.show()

for h_mark in (6, 24):

truth = 1 - float(kmf_full.predict(h_mark))

naive = 1 - float(kmf_naive_tr.predict(h_mark))

fix = 1 - float(kmf_fix_tr.predict(h_mark))

print(f"{h_mark:>2}m PD truth={truth:.4f} naive={naive:.4f} corrected={fix:.4f}")

```

The naive PD sits below the truth at both horizons. Two readings of the same gap matter for different audiences. In *absolute* PD, the bias grows with horizon (0.024 at 6m, 0.065 at 24m) because the early hazard deficit propagates multiplicatively, so risk reports keyed off lifetime PD are most distorted at long horizons. In *relative* PD, the bias is largest at the youngest ages (81% of truth at 6m, 37% at 24m) because the truth itself is small there: the truncation removes proportionally more of the early defaulters, and a small absolute deficit is a large fraction of a small denominator. Both readings vanish under the entry-corrected fit, which sits within Monte Carlo noise of the oracle at every horizon. The same correction extends to Cox: pass an `entry` column (or use the start/stop counting-process layout) and the partial-likelihood risk set $\mathcal{R}(t)$ is built from $\{i : a_0^{(i)} \le t \le \text{exit}^{(i)}\}$ instead of $\{i : \text{exit}^{(i)} \ge t\}$. Both fixes cost a single column in the input frame.

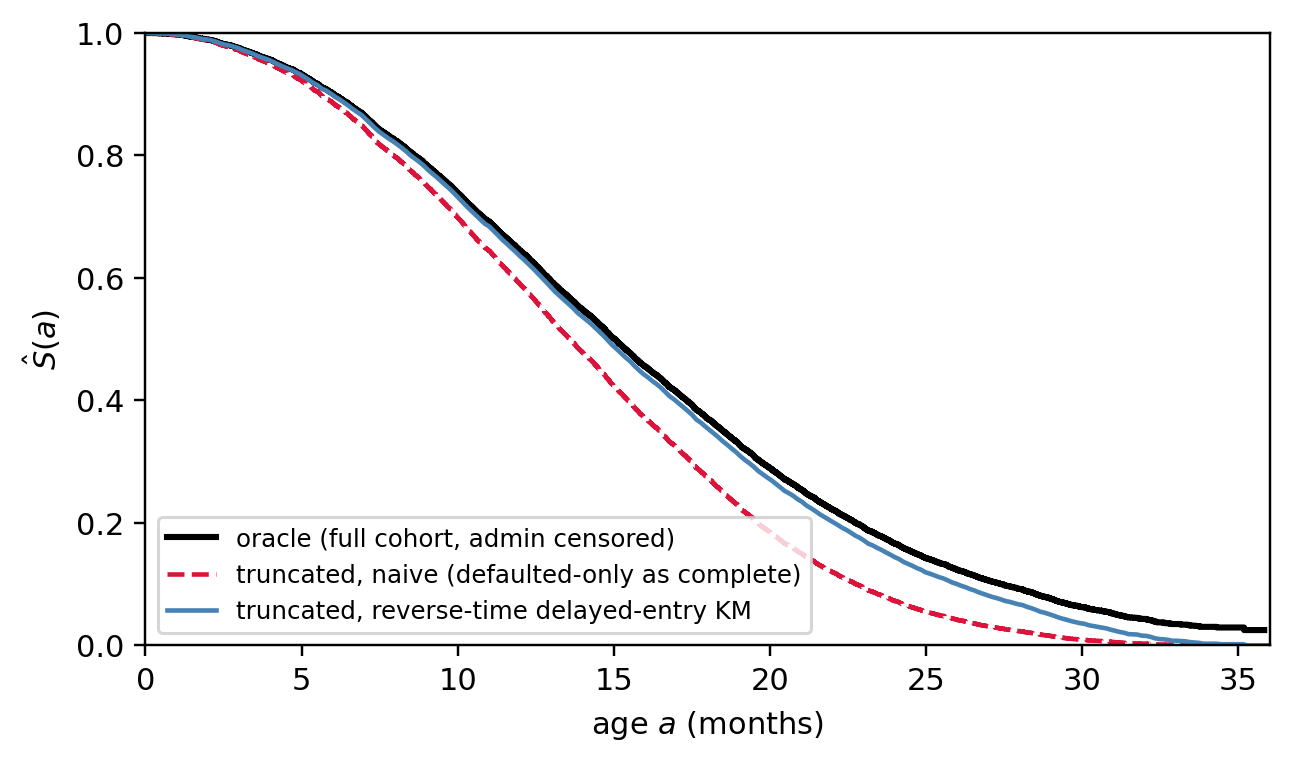

### Right truncation: a numerical demo {#sec-ch09-right-truncation-demo}

Right truncation has a different fingerprint and a different fix. We simulate the *defaulted-only extract* case: a Weibull cohort is generated from origination, the analysis cutoff is $\tau_{\text{end}}$ months after the earliest origination, and we keep only the loans that have already defaulted by the cutoff. The pretend-it-is-complete sample is what arrives in the warehouse when a chargeoff team hands you "the default file" without the at-risk denominator.

A clarification on what is identifiable. With right truncation alone, the data identify the *conditional* event-time distribution on the observed support $[0, t^*]$ where $t^* = \max_i R_i$ and $R_i = \tau_{\text{end}} - v_i$ is the per-row truncation bound, that is, $F_T(t)/F_T(t^*)$. The marginal $F_T$ on the full support is unidentifiable from the truncated sample alone; recovering it requires either an external estimate of $F_T(t^*)$ (e.g. a known portfolio default rate) or a parametric tail. The simulation below is calibrated so $F_T(t^*) \approx 1$, which lets us read the conditional and unconditional CDFs as essentially the same number; the production code reports the conditional CDF and flags whenever $t^*$ is materially below the credit-policy horizon.

@fig-ch09-right-truncation overlays three curves. (i) The oracle KM, fit on the full origination cohort with administrative right-censoring at $\tau_{\text{end}}$, is the truth we are trying to recover. (ii) The naive KM, fit on the defaulted-only subsample as if it were complete, is biased: every observation is an event, so the estimator collapses to the empirical CDF of $\{T_i \mid T_i \le R_i\}$, which over-represents short failure times. (iii) The reverse-time delayed-entry KM applies the @lagakos1988nonparametric construction: with $X_i = t^* - T_i$ and $B_i = t^* - R_i$, the right-truncation constraint $T_i \le R_i$ becomes the left-truncation constraint $B_i \le X_i$, and forward-time delayed-entry KM on $(B_i, X_i)$ with all-event indicator gives $\widehat F_T(t)/\widehat F_T(t^*) = \widehat S_X(t^* - t)$. Curves (i) and (iii) overlap to within Monte Carlo noise; curve (ii) does not.

```{python}

#| label: fig-ch09-right-truncation

#| fig-cap: "Right truncation and the reverse-time delayed-entry fix. A Weibull cohort ($k=2.0$, $\\lambda=18$) is generated from origination over 18 calendar months and observed until calendar cutoff $\\tau_{\\text{end}}=36$. The scale is calibrated so $F_T(t^*) \\approx 0.98$, which lets us compare the reverse-time correction (which identifies $F_T/F_T(t^*)$) to the oracle without separately re-scaling. Black: oracle KM on the full origination cohort with administrative right-censoring at the cutoff. Red dashed: naive KM on the defaulted-only subsample treating it as if it were complete. Blue: reverse-time delayed-entry KM (Lagakos 1988) on the truncated sample, which inverts the time axis so the right truncation becomes left truncation and the standard delayed-entry KM applies. The naive curve overstates early-age PD because the truncated sample concentrates the mass on short failure times."

n3 = 12000

v3 = rng.uniform(0, 18, size=n3)

T3 = 18.0 * rng.weibull(2.0, size=n3)

tau_end = 36.0

R3 = tau_end - v3 # per-row right-truncation bound

# (i) Oracle: full cohort, admin censoring at calendar cutoff.

Y_oracle = np.minimum(T3, R3)

E_oracle = (T3 <= R3).astype(int)

kmf_oracle = KaplanMeierFitter().fit(Y_oracle, E_oracle,

label='oracle (full cohort, admin censored)')

# (ii) Right-truncated sample: keep only loans whose default landed

# before the cutoff. Every retained row is a defaulter.

trunc = T3 <= R3

T_obs = T3[trunc]

R_obs = R3[trunc]

kmf_naive_rt = KaplanMeierFitter().fit(

T_obs, np.ones_like(T_obs, dtype=int),

label='truncated, naive (defaulted-only as complete)',

)

# (iii) Reverse-time delayed-entry KM (Lagakos 1988).

# X_i = t* - T_i (reversed-time exit), B_i = t* - R_i (reversed-time entry).

# The right-truncation constraint becomes a left-truncation constraint;

# delayed-entry KM with entry=B and all-event indicator gives

# F_T(t)/F_T(t*) = S_X(t* - t).

t_star = float(R_obs.max())

X_rev = t_star - T_obs

B_rev = t_star - R_obs

kmf_rev = KaplanMeierFitter().fit(

X_rev, np.ones_like(X_rev, dtype=int), entry=B_rev,

)

ages = np.linspace(0.0, tau_end, 256)

s_rev_back = 1.0 - kmf_rev.survival_function_at_times(

np.maximum(t_star - ages, 0.0)

).values

fig, ax = plt.subplots(1, 1, figsize=(6.0, 3.6))

kmf_oracle.plot_survival_function(ax=ax, ci_show=False, color='black', lw=2)

kmf_naive_rt.plot_survival_function(ax=ax, ci_show=False, color='crimson', linestyle='--')

ax.plot(ages, s_rev_back, color='steelblue',

label='truncated, reverse-time delayed-entry KM')

ax.set_xlabel('age $a$ (months)'); ax.set_ylabel('$\\hat S(a)$')

ax.set_xlim(0, tau_end); ax.set_ylim(0, 1)

ax.legend(loc='lower left', fontsize=8)

fig.tight_layout(); plt.show()

def _s_rev(a: float) -> float:

return 1.0 - float(kmf_rev.survival_function_at_times(

np.array([max(t_star - a, 0.0)])).values[0])

rt_rows = []

for h_mark in (6, 12, 24):

truth = 1.0 - float(kmf_oracle.predict(h_mark))

naive = 1.0 - float(kmf_naive_rt.predict(h_mark))

fix = 1.0 - _s_rev(h_mark)

rt_rows.append({'horizon_m': h_mark,

'oracle_PD': truth,

'naive_PD': naive,

'reverse_time_PD': fix,

'naive_minus_oracle_bps': (naive - truth) * 1e4,

'reverse_minus_oracle_bps': (fix - truth) * 1e4})

rt_df = pd.DataFrame(rt_rows).round(4)

print(rt_df.to_string(index=False))

```

Three things to read off the printed table:

- First, the naive estimator overstates PD at every horizon: the defaulted-only sample is dominated by short failure times, so the empirical CDF climbs too fast.

- Second, the bias is largest at the youngest ages and shrinks with $h$, because by $h \approx t^*$ the naive empirical CDF is forced to one (every retained row defaulted by then) regardless of cohort.

- Third, the reverse-time delayed-entry KM matches the oracle to within tens of basis points across two horizons, which is the practical demonstration that the fix is the right one. Lifelines' `KaplanMeierFitter.fit_left_truncation_right_censoring` covers the symmetric case where both biases are present at once.

The production lesson is that the *first* check on any incoming cohort should be whether the event indicator is degenerate. If `event.mean() == 1` the cohort is event-only and a right-truncation correction is mandatory; if `event.mean() < 0.001` the cohort may have lost the defaulter join, which is the mirror failure mode and equally damaging. `survival_diagnostics.truncation` wraps both checks, fits the appropriate corrected KM, and emits an artifact field that the validation pipeline blocks on when the corrected and naive lifetime PDs disagree by more than the configured basis-point threshold.

### Truncation diagnostics in production {#sec-ch09-truncation-prod}

The chapter demos and the production code share a single implementation path. `detect_truncation(duration, event, entry=..., vintage_age_at_cutoff=...)` ingests exactly the columns each correction needs, fits the delayed-entry KM (left truncation) and the reverse-time delayed-entry KM (right truncation) under the hood, and returns a typed result with bias deltas in basis points. The summary table below is the same artifact field the FastAPI service writes into the validation pack JSON.

```{python}

#| label: tbl-ch09-truncation-prod

#| tbl-cap: "Production truncation artifact for the two simulated cohorts above. `delta_bps` is corrected minus naive PD at each horizon, in basis points; `blocks=True` means the truncation gap exceeds 50 bps at one or more horizons and the validation pipeline halts the run."

from survival_diagnostics import (

TruncationConfig, detect_truncation, truncation_summary_table,

)

# (a) Left-truncated cohort: re-use the entry-time setup from earlier.

cfg = TruncationConfig(horizons_months=(6, 12, 24, 36), bias_block_bps=50.0)

left_res = detect_truncation(Y_tr, E_tr, entry=a0_tr, config=cfg)

left_tbl = truncation_summary_table(left_res).round(4)

print("=== left-truncation production artifact ===")

print(f"flags = needs_left={left_res.flags.needs_left_truncation_fix} "

f"blocks={left_res.blocks}")

print(left_tbl.to_string(index=False))

# (b) Right-truncated cohort: re-use the defaulted-only extract.

cfg2 = TruncationConfig(horizons_months=(6, 12, 24), bias_block_bps=50.0)

right_res = detect_truncation(

T_obs, np.ones_like(T_obs, dtype=int),

vintage_age_at_cutoff=R_obs, config=cfg2,

)

right_tbl = truncation_summary_table(right_res).round(4)

print("\n=== right-truncation production artifact ===")

print(f"flags = event_only={right_res.flags.looks_event_only} "

f"needs_right={right_res.flags.needs_right_truncation_fix} "

f"blocks={right_res.blocks}")

print(right_tbl.to_string(index=False))

```

Two points worth restating. The artifact is non-fatal by design: the pipeline records `blocks=True` and stops the validation run, but it preserves the rest of the diagnostic so reviewers see *which* check fired. And the `entry_age_months` and `vintage_age_at_cutoff_months` columns on the FastAPI request body are optional: a cohort assembled from a clean origination snapshot needs neither, but a cohort assembled from a calendar-window snapshot or a chargeoff feed needs at least one, and the model card escalation rule is the audit-side enforcement of that requirement.

## Input data layouts {#sec-ch09-data-layouts}

Survival fitters disagree on what their input looks like. The same cohort feeds Kaplan-Meier in lifelines, a Cox fit in scikit-survival, a Shumway logit in statsmodels, and a Fine-Gray Geskus reduction in lifelines, and each one wants a *different* in-memory shape. Most "the package crashed" tickets in production trace to a layout mismatch, not a modeling bug. This section materializes a small synthetic cohort and shows the `head()` of every layout the rest of the chapter uses, with the package and fitter that consumes each one.

We use six loans so the printed frames fit on one screen. The same construction scales to a real portfolio without changes.

```{python}

#| label: layouts-cohort

import numpy as np

import pandas as pd

cohort = pd.DataFrame({

'loan_id': np.arange(6),

'vintage': [0, 0, 1, 1, 2, 2], # origination cohort (calendar month)

'entry_age': [0, 0, 0, 6, 0, 0], # months on book at study entry (left truncation)

'duration': [12, 24, 18, 30, 9, 36],

'event': [1, 0, 1, 0, 1, 0], # 1 = default, 0 = censored

'cause': [1, 0, 2, 0, 1, 0], # 1 = default, 2 = prepay, 0 = censored

'fico': [620, 720, 660, 700, 580, 740],

'ltv': [0.85, 0.65, 0.75, 0.70, 0.95, 0.55],

})

print(cohort)

```

Loan 3 enters the risk set six months after origination (the left-truncation case from @sec-ch09-truncation-demo). Loan 2 exits via prepayment, the competing risk in @sec-ch09-competing. Everything else is a vanilla right-censored observation.

### Layout 1: wide per-loan frame {#sec-ch09-layout-wide}

One row per loan, with `duration` and `event` columns and any number of fixed-at-origination covariates. This is the layout `lifelines` expects across `KaplanMeierFitter`, `CoxPHFitter`, and the AFT family (`WeibullAFTFitter`, `LogNormalAFTFitter`, `LogLogisticAFTFitter`).

```{python}

#| label: layouts-wide

wide = cohort[['loan_id', 'duration', 'event', 'fico', 'ltv']]

print(wide.head())

```

Consumers:

- `KaplanMeierFitter().fit(wide['duration'], wide['event'])` — see @sec-ch09-km-cox.

- `CoxPHFitter().fit(wide.drop(columns='loan_id'), 'duration', 'event')` — see @sec-ch09-km-cox.

- `WeibullAFTFitter().fit(wide.drop(columns='loan_id'), 'duration', 'event')` — see @sec-ch09-aft.

Add an `entry` column to handle left truncation in lifelines: `KaplanMeierFitter().fit(durations, events, entry=cohort['entry_age'])`. The Cox equivalent in lifelines is `CoxPHFitter().fit(..., entry_col='entry_age')`. Both implementations build the risk set $\mathcal{R}(t) = \{i : a_0^{(i)} \le t \le \text{exit}^{(i)}\}$ from those two columns.

### Layout 2: scikit-survival structured array {#sec-ch09-layout-sksurv}

`scikit-survival` separates the response from the design matrix. The response is a NumPy *structured array* of `(event_bool, time_float)` records; the design is a plain 2-D feature array.

```{python}

#| label: layouts-sksurv

from sksurv.util import Surv

y_sksurv = Surv.from_arrays(

event=cohort['event'].astype(bool).values,

time=cohort['duration'].astype(float).values,

)

X_sksurv = cohort[['fico', 'ltv']].to_numpy(dtype=float)

print('y dtype:', y_sksurv.dtype)

print('y[:6] :', y_sksurv[:6])

print('X[:6] :')

print(X_sksurv[:6])

```

Consumers:

- `RandomSurvivalForest().fit(X_sksurv, y_sksurv)` — see @sec-ch09-benchmark.

- `GradientBoostingSurvivalAnalysis().fit(X_sksurv, y_sksurv)` — see @sec-ch09-benchmark.

- `CoxPHSurvivalAnalysis().fit(X_sksurv, y_sksurv)` (the sksurv Cox, distinct from the lifelines one).

- Metrics: `concordance_index_censored`, `cumulative_dynamic_auc`, `integrated_brier_score` all read this dtype directly.

The dtype convention `[('event', '?'), ('time', '<f8')]` is non-negotiable. Pass a 2-column DataFrame and sksurv raises `ValueError: y must be a structured array`.

### Layout 3: counting-process start-stop episodes {#sec-ch09-layout-counting}

The counting-process layout of @andersen1982cox splits each loan's follow-up into one or more $[\text{start}, \text{stop})$ episodes. Each episode carries its own covariate vector and an event flag that fires only on the episode where the event occurs. This is the universal layout for left truncation, time-varying covariates, and time-varying coefficients (@sec-ch09-ph-fix-tvc).

```{python}

#| label: layouts-counting

counting = cohort[['loan_id', 'entry_age', 'duration', 'event', 'fico', 'ltv']].copy()

counting['start'] = counting['entry_age']

counting['stop'] = counting['entry_age'] + counting['duration']

counting = counting[['loan_id', 'start', 'stop', 'event', 'fico', 'ltv']]

print(counting.head())

```

Consumers: