---

execute:

echo: true

eval: true

---

# Reject Inference and Sample Selection {#sec-ch10}

::: {.callout-note appearance="simple" icon="false"}

**Scope: retail.** Reject inference for application scoring on consumer portfolios, where rejected-applicant volumes are large enough to fit the parametric MNAR machinery developed here. Corporate originations are too heterogeneous and too small a sample for the same approach.

:::

## Overview {.unnumbered}

A lender's data generation process is not i.i.d. from the applicant population. Only the accepted see a loan, and only the accepted produce an outcome we can label. Every estimator that trains on accepted-only data, and every validation curve drawn from accepted-only data, therefore answers a different question than the one a credit officer is asking. The officer asks: what is the probability of default for this applicant in the unrestricted pool? The accepted-only model answers: what is the probability of default for applicants who resemble those the incumbent policy chose to fund?

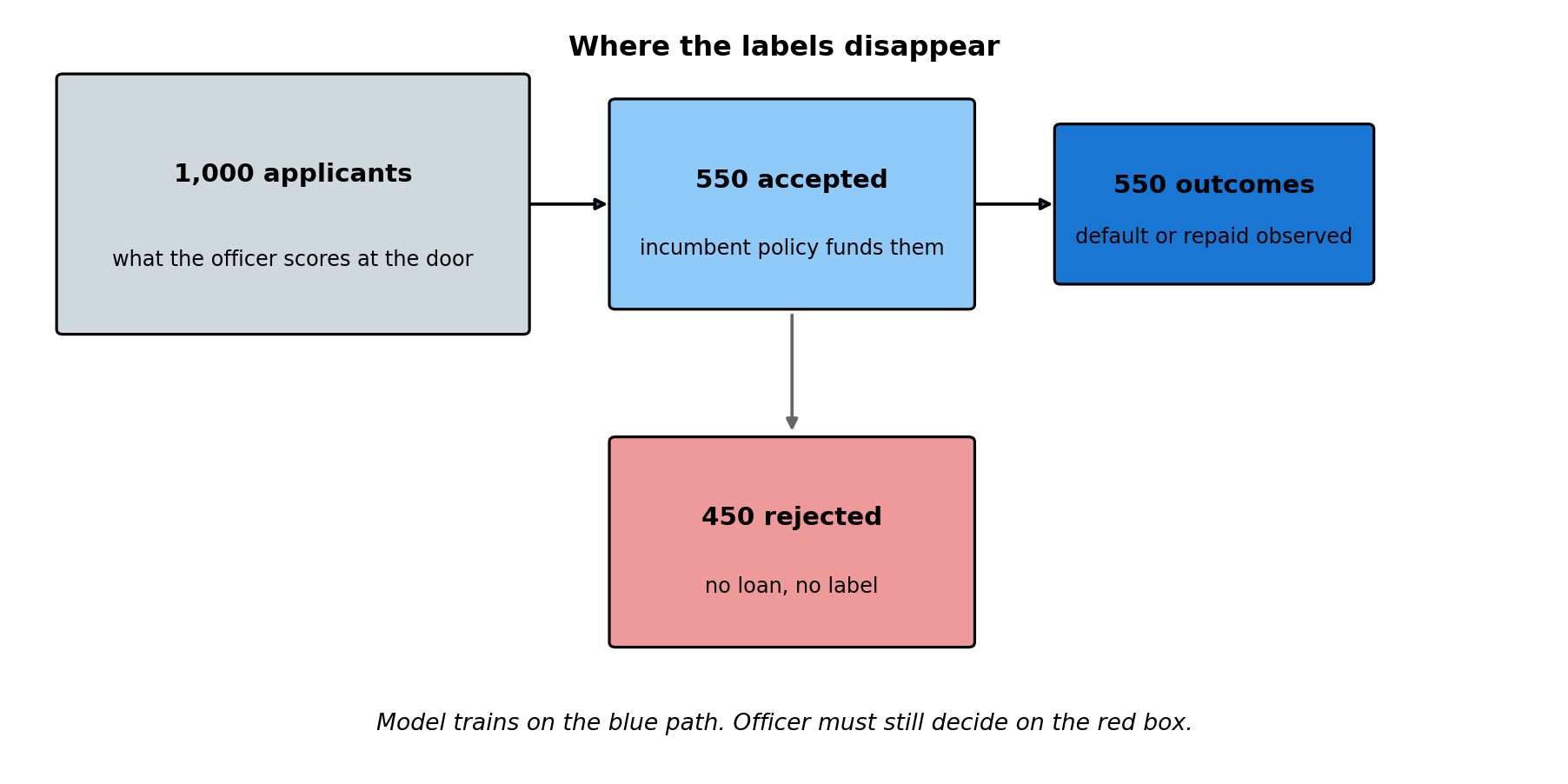

Two pictures fix the geometry before any algebra. @fig-ch10-visibility-funnel shows where labels disappear in the data pipeline. @fig-ch10-conditional-shift shows what that disappearance does to the curves a modeler actually plots.

```{python}

#| label: fig-ch10-visibility-funnel

#| fig-cap: "From applicants to labels. Of every 1,000 through-the-door applicants, the incumbent policy funds roughly 550 and the bureau later returns a default-or-repaid outcome on those 550. The other 450 produce no label. Any model trained on the blue path is fit on the funded slice only; the credit officer must still answer for the red box at decision time."

import matplotlib.pyplot as plt

import matplotlib.patches as mpatches

fig, ax = plt.subplots(figsize=(9.5, 4.8))

ax.set_xlim(0, 10)

ax.set_ylim(0, 6)

ax.axis("off")

def box(x, y, w, h, color, label, sublabel):

rect = mpatches.FancyBboxPatch(

(x, y), w, h, boxstyle="round,pad=0.04",

facecolor=color, edgecolor="black", linewidth=1.2,

)

ax.add_patch(rect)

ax.text(x + w / 2, y + h * 0.62, label,

ha="center", va="center", fontsize=11, fontweight="bold")

ax.text(x + w / 2, y + h * 0.28, sublabel,

ha="center", va="center", fontsize=9)

box(0.3, 3.5, 3.0, 2.0, "#cfd8dc",

"1,000 applicants", "what the officer scores at the door")

box(3.9, 3.7, 2.3, 1.6, "#90caf9",

"550 accepted", "incumbent policy funds them")

box(6.8, 3.9, 2.0, 1.2, "#1976d2",

"550 outcomes", "default or repaid observed")

box(3.9, 1.0, 2.3, 1.6, "#ef9a9a",

"450 rejected", "no loan, no label")

ax.annotate("", xy=(3.88, 4.5), xytext=(3.32, 4.5),

arrowprops=dict(arrowstyle="-|>", lw=1.4))

ax.annotate("", xy=(6.78, 4.5), xytext=(6.22, 4.5),

arrowprops=dict(arrowstyle="-|>", lw=1.4))

ax.annotate("", xy=(5.05, 2.65), xytext=(5.05, 3.65),

arrowprops=dict(arrowstyle="-|>", lw=1.4, color="0.4"))

ax.text(5.0, 0.35,

"Model trains on the blue path. Officer must still decide on the red box.",

ha="center", va="center", fontsize=10, style="italic")

ax.text(5.0, 5.75,

"Where the labels disappear",

ha="center", va="center", fontsize=12, fontweight="bold")

plt.tight_layout()

plt.show()

```

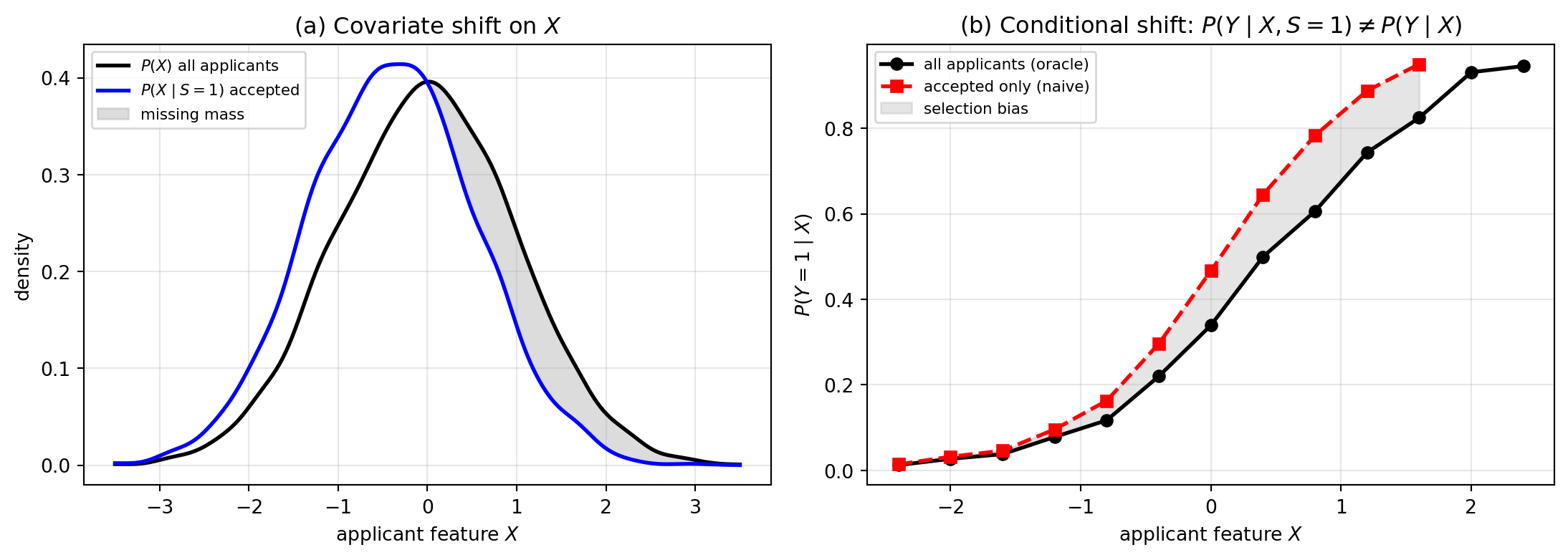

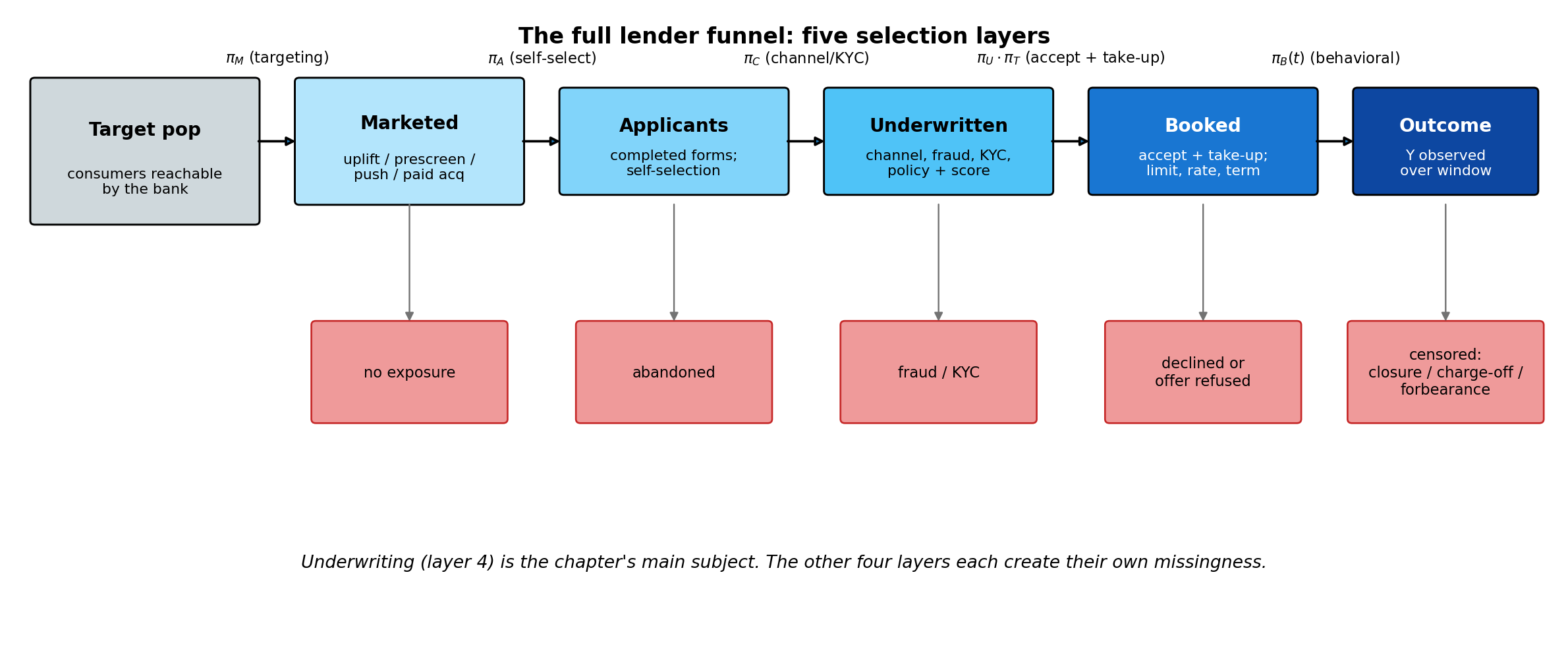

The funnel is descriptive. The substantive damage is visible on a default-rate curve. @fig-ch10-conditional-shift shows what happens when we draw the same plot using the full applicant population (which we know only because this is a simulation) and using the accepted slice (which is all a real lender ever sees). The three-box version of the funnel collapses several real selection layers (pre-application targeting, application self-selection, channel and KYC gates, take-up, and post-booking management) into a single accept/decline arrow; @sec-ch10-full-funnel returns to the full five-layer view and gives a separate correction for each layer.

```{python}

#| label: fig-ch10-conditional-shift

#| fig-cap: "Two faces of the selection problem on a synthetic through-the-door population (n = 8,000) with bivariate-normal correlation $\\rho = 0.6$ between the latent default error and the latent acceptance error. (a) Covariate shift: the accepted-population density of the feature $X$ is pulled toward the safer (lower-$X$) side because the policy declines high-$X$ applicants. (b) Conditional shift: the empirical default rate plotted against $X$ is uniformly higher on the accepted slice than on the through-the-door population, even after conditioning on $X$, because the policy accepts on a latent signal positively correlated with the default error. The shaded gap in (b) is the bias that reject inference must close; it cannot be removed by reweighting on $X$ alone because it comes from selection on the unobserved error, not from feature imbalance."

import numpy as np

import matplotlib.pyplot as plt

from scipy import stats

from scipy.stats import gaussian_kde

rng_fig = np.random.default_rng(20260428)

n_fig = 8_000

X_fig = rng_fig.standard_normal(n_fig)

Z_fig = rng_fig.standard_normal(n_fig)

rho_fig = 0.6

u_fig = rng_fig.standard_normal(n_fig)

v_fig = rho_fig * u_fig + np.sqrt(1 - rho_fig**2) * rng_fig.standard_normal(n_fig)

y_star_fig = -0.4 + 0.9 * X_fig + u_fig

y_fig = (y_star_fig > 0).astype(int)

s_star_fig = -0.7 * X_fig + 0.9 * Z_fig + v_fig

s_fig = (s_star_fig > 0).astype(int)

fig, axes = plt.subplots(1, 2, figsize=(11.5, 4.2))

ax = axes[0]

xs = np.linspace(-3.5, 3.5, 400)

kde_all = gaussian_kde(X_fig)(xs)

kde_acc = gaussian_kde(X_fig[s_fig == 1])(xs)

ax.plot(xs, kde_all, "k-", lw=2.0, label=r"$P(X)$ all applicants")

ax.plot(xs, kde_acc, "b-", lw=2.0, label=r"$P(X \mid S=1)$ accepted")

ax.fill_between(xs, kde_all, kde_acc, where=(kde_all > kde_acc),

color="0.7", alpha=0.45, label="missing mass")

ax.set_xlabel(r"applicant feature $X$")

ax.set_ylabel("density")

ax.set_title("(a) Covariate shift on $X$")

ax.legend(fontsize=8, loc="upper left")

ax.grid(alpha=0.3)

ax = axes[1]

bins = np.linspace(-3, 3, 16)

mid = 0.5 * (bins[:-1] + bins[1:])

def binmean(mask):

out = np.full_like(mid, np.nan, dtype=float)

for i in range(len(mid)):

m = mask & (X_fig >= bins[i]) & (X_fig < bins[i + 1])

if m.sum() > 30:

out[i] = y_fig[m].mean()

return out

emp_all = binmean(np.ones(n_fig, dtype=bool))

emp_acc = binmean(s_fig == 1)

ax.plot(mid, emp_all, "ko-", lw=2.0, label="all applicants (oracle)")

ax.plot(mid, emp_acc, "rs--", lw=2.0, label="accepted only (naive)")

valid = np.isfinite(emp_all) & np.isfinite(emp_acc)

ax.fill_between(mid[valid], emp_all[valid], emp_acc[valid],

color="0.75", alpha=0.4, label="selection bias")

ax.set_xlabel(r"applicant feature $X$")

ax.set_ylabel(r"$P(Y=1 \mid X)$")

ax.set_title(r"(b) Conditional shift: $P(Y \mid X, S=1) \neq P(Y \mid X)$")

ax.legend(fontsize=8, loc="upper left")

ax.grid(alpha=0.3)

plt.tight_layout()

plt.show()

```

Panel (a) is what reweighting fixes: the feature distribution differs between funded and through-the-door, and inverse probability weights on $X$ recover $P(X)$ from $P(X \mid S=1)$. Panel (b) is what reweighting cannot fix: even at the same $X$, the accepted applicants default *more*, because the underwriter accepted on signals that we never recorded and that also predict default. (The opposite sign of the gap, accepted defaulting *less*, would arise if the underwriting signals were negatively correlated with the default error, i.e. effective screening on unobservables; we treat both regimes symmetrically when we discuss the sign of $\hat\rho$ in @sec-ch10-heckman-selection-correction.) That is the part of the gap that motivates Heckman, the impossibility result, and everything that follows in this chapter.

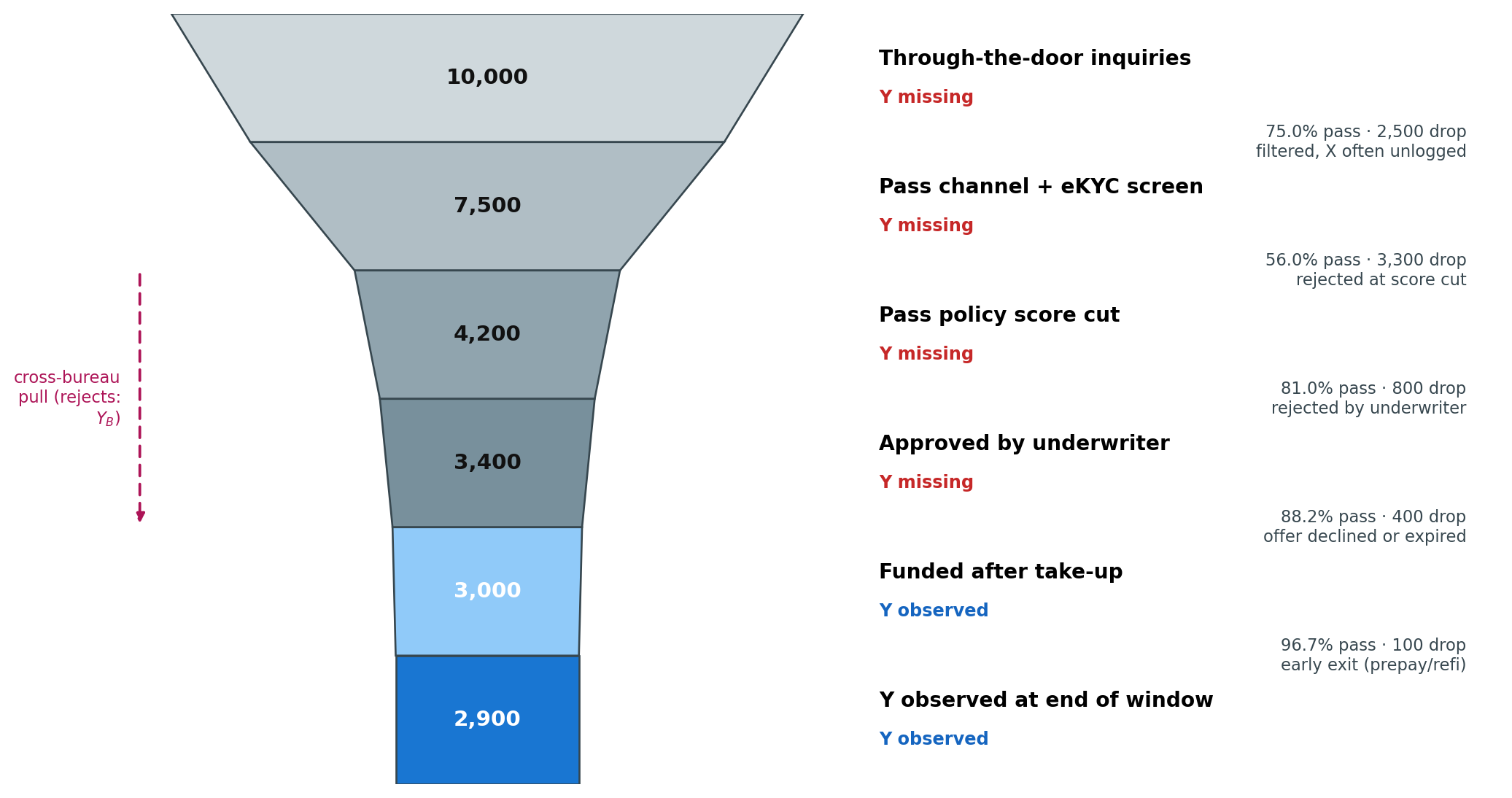

Before tackling the methods in turn, it helps to map every stage where selection bias enters and every identification condition a corrective method might lean on. We use three views in turn. @fig-ch10-funnel-volumes plots the typical drop-off in counts at each gate, so the order-of-magnitude problem is visible at a glance. @fig-ch10-selection-roadmap is a stage-level DAG of the same pipeline, with the labelled exits where $Y$ is missing or imported from a bureau. @tbl-ch10-bias-dimensions then catalogues the seven *selection-bias dimensions* (D1 through D7) that any reject inference exercise has to take an explicit position on, the stage at which each one binds, and the section of the chapter that addresses it. A note on terminology. We call D1 through D7 *selection-bias dimensions* (or *identification checkpoints*) rather than *moderators*: in the standard statistical usage a moderator is a variable that interacts with $X$ to shift the $X \to Y$ relationship, whereas D1 through D7 are a mix of bias *sources* (D2, D3), positivity and identification *assumptions* (D1, D4), and external-validity *threats* (D5, D6, D7). Each subsequent section of the chapter targets one or more of these dimensions, and the impossibility result of @sec-ch10-impossibility says exactly which combinations the accepted-only sample can never settle on its own.

```{python}

#| label: fig-ch10-funnel-volumes

#| fig-cap: "Typical drop-off through a Vietnamese consumer-finance acquisition funnel for 10,000 through-the-door inquiries. Band widths are proportional to surviving counts; the right column reads off the absolute count, the labelled-Y indicator, and the stage-to-stage pass rate. Only the bottom two bands carry an observed default outcome $Y$ for the lender; the rejected (red) band is the population that bureau extrapolation tries to recover, and the filtered (grey) band is the population whose features were never even logged. The funded slice is roughly 30 percent of the through-the-door pool, yet a naive PD model can only be trained on it."

import matplotlib.pyplot as plt

import matplotlib.patches as mpatches

import numpy as np

stages = [

("Through-the-door inquiries", 10_000, "#cfd8dc", False, None),

("Pass channel + eKYC screen", 7_500, "#b0bec5", False, "filtered, X often unlogged"),

("Pass policy score cut", 4_200, "#90a4ae", False, "rejected at score cut"),

("Approved by underwriter", 3_400, "#78909c", False, "rejected by underwriter"),

("Funded after take-up", 3_000, "#90caf9", True, "offer declined or expired"),

("Y observed at end of window", 2_900, "#1976d2", True, "early exit (prepay/refi)"),

]

counts = np.array([c for _, c, _, _, _ in stages], dtype=float)

labels = [s for s, _, _, _, _ in stages]

colors = [c for _, _, c, _, _ in stages]

y_obs = [yo for _, _, _, yo, _ in stages]

drop_reasons = [r for _, _, _, _, r in stages]

top = counts.max()

widths = counts / top

fig, ax = plt.subplots(figsize=(11, 5.8))

ax.set_xlim(-0.7, 1.6)

ax.set_ylim(0, len(stages))

ax.invert_yaxis()

ax.axis("off")

def trapezoid(y, w_top, w_bot, color):

cx = 0.0

pts = [

(cx - w_top / 2, y),

(cx + w_top / 2, y),

(cx + w_bot / 2, y + 1),

(cx - w_bot / 2, y + 1),

]

poly = mpatches.Polygon(pts, closed=True, facecolor=color,

edgecolor="#37474f", linewidth=1.0)

ax.add_patch(poly)

for i in range(len(stages)):

w_top = widths[i]

w_bot = widths[i + 1] if i + 1 < len(stages) else widths[i]

trapezoid(i, w_top, w_bot, colors[i])

ax.text(0.0, i + 0.5, f"{int(counts[i]):,}",

ha="center", va="center", fontsize=11,

color="white" if i >= len(stages) - 2 else "#111",

fontweight="bold")

badge = "Y observed" if y_obs[i] else "Y missing"

badge_color = "#1565c0" if y_obs[i] else "#c62828"

ax.text(0.62, i + 0.35, labels[i],

ha="left", va="center", fontsize=10.5, fontweight="bold")

ax.text(0.62, i + 0.65, badge,

ha="left", va="center", fontsize=9, color=badge_color,

fontweight="bold")

if i + 1 < len(stages):

conv = counts[i + 1] / counts[i] * 100

drop = int(counts[i] - counts[i + 1])

reason = drop_reasons[i + 1] or ""

ax.text(1.55, i + 1, f"{conv:4.1f}% pass · {drop:,} drop\n{reason}",

ha="right", va="center", fontsize=8.5, color="#37474f")

ax.annotate("", xy=(-0.55, 4.0), xytext=(-0.55, 2.0),

arrowprops=dict(arrowstyle="-|>", lw=1.4,

linestyle=(0, (4, 3)), color="#ad1457"))

ax.text(-0.58, 3.0, "cross-bureau\npull (rejects:\n$Y_B$)",

ha="right", va="center", fontsize=8.5, color="#ad1457")

plt.tight_layout()

plt.show()

```

::: no-panzoom

```{mermaid}

%%| label: fig-ch10-selection-roadmap

%%| fig-cap: "Stage-level DAG of the selection pipeline. Solid arrows are the funded path on which $Y$ is observed; red boxes mark exits where $Y$ is missing for the lender; dotted arrows are optional ports where the lender can pull a bureau outcome $Y_B$ on rejected applicants. The seven selection-bias dimensions D1 through D7 are catalogued in @tbl-ch10-bias-dimensions; this diagram intentionally omits the dimension labels from the nodes so the pipeline structure stays legible."

flowchart TD

classDef stage fill:#eceff1,stroke:#455a64,color:#111;

classDef gate fill:#fff8e1,stroke:#b58900,color:#111;

classDef obs fill:#1976d2,stroke:#0d47a1,color:#fff;

classDef miss fill:#ef9a9a,stroke:#c62828,color:#111;

classDef bureau fill:#f8bbd0,stroke:#ad1457,color:#111;

A["Through-the-door applicant<br/>X observed, Z partial, U and V latent"]:::stage

S1{{"Stage 1: channel and eKYC screen"}}:::gate

L1["Filtered pre-score<br/>X often not stored"]:::miss

S2{{"Stage 2: policy and underwriter decision"}}:::gate

REJ["Rejected (S=0)<br/>Y missing for the lender"]:::miss

YB["Bureau outcome Y_B<br/>different lender, different product"]:::bureau

ACC["Funded (S=1)<br/>limit, rate, term"]:::stage

PW{{"Stage 3: performance window<br/>vintage v, macro state m"}}:::gate

PRP["Prepay or refinance<br/>competing event (ch 9)"]:::miss

Y["Outcome Y observed"]:::obs

A --> S1

S1 -->|fail| L1

S1 -->|pass| S2

S2 -->|S=0| REJ

S2 -->|S=1| ACC

REJ -.->|cross-bureau pull| YB

ACC --> PW

PW --> Y

PW -.->|early exit| PRP

```

:::

| ID | Selection-bias dimension | Stage where it binds | Section that addresses it |

|------------------|------------------|------------------|-------------------|

| D1 | Policy overlap: is $P(S{=}1 \mid x) > 0$ everywhere on the support of $X$? | Stage 1 hard pre-screens; Stage 2 score cut | @sec-ch10-observable, @sec-ch10-rdd |

| D2 | Covariate shift on $X$: $P(X \mid S{=}1) \neq P(X)$ | Stage 2 (and Stage 1 if it depends on $X$) | @sec-ch10-augmentation-hsias-parceling-and-its-fuz, @sec-ch10-modern |

| D3 | Selection on unobservables: $\mathrm{Corr}(U,V) \neq 0$ | Stage 2 (underwriter signals not in $X$) | @sec-ch10-heckman-selection-correction, @sec-ch10-modern |

| D4 | Exclusion restriction: a $Z$ that shifts $S$ but not $Y$ | Stage 2 (assumption about the design) | @sec-ch10-heckman-selection-correction |

| D5 | Vintage and macro state: through-the-cycle vs point-in-time | Stage 3 performance window | @sec-ch10-targeting, @sec-ch10-behavioral |

| D6 | Bureau product gap: limit, rate, servicer differ from the lender's product | Bureau path on rejects | @sec-ch10-bureau-extrapolation |

| D7 | Within-reject bureau coverage: 10 to 30 percent of rejects have no trade-line | Bureau path on rejects | @sec-ch10-bureau-extrapolation |

: Seven selection-bias dimensions that every reject-inference method must take a position on. Each row names the stage of @fig-ch10-selection-roadmap at which the dimension first binds, and the section of the chapter where it is treated. {#tbl-ch10-bias-dimensions}

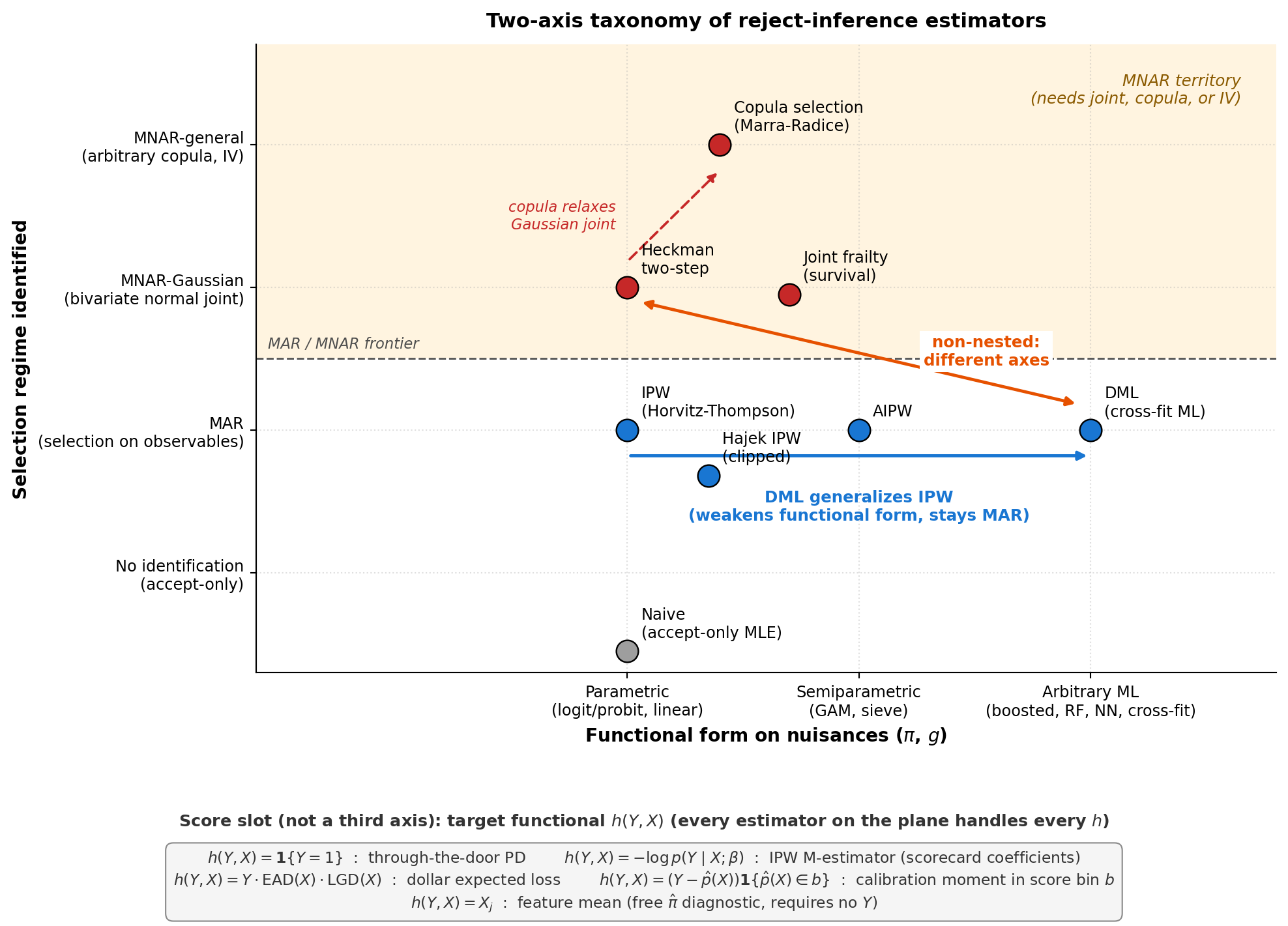

A short reading guide. Augmentation and parceling (@sec-ch10-augmentation-hsias-parceling-and-its-fuz) leans on D2 alone and assumes D3 away. Bureau extrapolation (@sec-ch10-bureau-extrapolation) buys D3 by importing $Y_B$ but inherits D5, D6, and D7. Heckman (@sec-ch10-heckman-selection-correction) trades D3 for parametric structure plus D4. AIPW, copulas, deep generative imputation, importance weighting, and PU learning (@sec-ch10-modern) each relax one Heckman primitive. Observable-engine methods (@sec-ch10-observable) attack D1 directly when the lender owns the decision engine. EM and pseudo-labeling (@sec-ch10-em) exploit cluster structure when none of the above is available.

This chapter treats the gap between those two questions as the subject in its own right. We formalize the missing-data taxonomy (@sec-ch10), derive the Heckman (1979) two-step selection correction in full (@sec-ch10-heckman-selection-correction), state and prove the Hand and Henley (1997) impossibility result (@sec-ch10-impossibility), and write the EM algorithm that underpins a self-training reject inference loop (@sec-ch10-em). We then go beyond Heckman with five modern estimators: doubly robust AIPW (@robins1994estimation, @chernozhukov2018double), copula-based selection (@marra2017bivariate), deep generative imputation (@mancisidor2020deep), covariate-shift importance weighting (@sugiyama2007covariate, @bickel2009discriminative), and positive-unlabeled learning (@kiryo2017positive). A separate strand handles the case where the lender observes its own decision engine, where regression-discontinuity (@hahn2001identification, @imbens2008recent) and exact-propensity weighting recover identification without parametric assumptions. A method-agnostic AIPW score unifies these threads and translates one-for-one to the survival-censoring problem of @sec-ch09 and to LDA, gradient boosting, and lifetime PD elsewhere in the book. We close with two modern practitioner views: the marketplace-lending perspective of @vallee2019marketplace and the automation/disparity evidence of @howell2024lender.

The chapter is deliberately not a tour of reject inference recipes. The recipes without the identifiability argument behind them are dangerous in production, because a plausible looking PD curve on rejected applicants can coexist with arbitrarily wrong truth. That is the Hand and Henley point, and the rest of the chapter is an attempt to meet it with either extra structure (exclusion restrictions, parametric families) or extra data (bureau outcomes, through-the-door bureau vintages).

The problem is most severe in emerging markets. A Vietnamese consumer lender rolling out eKYC under Circular 16/2020/TT-NHNN sees through-the-door volumes ten times its booked volume, decline rates above 70 percent are routine at the consumer-finance subsidiaries of joint-stock banks, and CIC lookups skew toward the thinnest of thin files [@sbv2020ekyc; @cicvn2023report]. Informal income, Tet-induced cash-flow compression, and macro volatility mean the selection rule correlates with unobservables that also drive default. The closing emerging-market section returns to this with CIC-based bureau extrapolation, Heckman exclusion candidates specific to Vietnam, and Decree 13/2023 constraints on how rejected-applicant data can be retained and reused.

## Notation {#sec-ch10-notation .unnumbered}

Let $X \in \mathbb{R}^p$ be the application features observed at decision time, $Z \in \mathbb{R}^q$ be a vector used in the selection decision but excluded from the outcome equation, and $Y \in \{0,1\}$ the default indicator over a fixed performance window. Let $S \in \{0,1\}$ be the accept indicator ($S=1$ if the incumbent policy funded the loan). Only $(X, Z, S)$ are observed for the full through-the-door population. $Y$ is observed only when $S = 1$.

Throughout the chapter, $\phi$ and $\Phi$ denote the standard normal density and CDF. The inverse Mills ratio is $\lambda(a) = \phi(a)/\Phi(a)$. Expectations over the unobserved error vector $(u, v)$ respect the bivariate normal joint structure assumed in @heckman1979sample, with correlation $\rho$ and outcome-side standard deviation $\sigma$ (normalized to 1 in the probit case).

**Nuisance functions.** []{#sec-ch10-nuisance-def} The chapter uses the word *nuisance* in its semiparametric-statistics sense, not its everyday sense. The *parameter of interest* (also called the target functional) is the object the lender actually wants to estimate: the through-the-door PD $\mu_0(x) = P(Y = 1 \mid X = x)$, the scorecard coefficients $\beta$, the dollar expected loss on a policy region, or any other functional of the full-population law. A *nuisance function* (or *nuisance parameter* when finite-dimensional) is any other quantity that the estimator needs as an input but that the lender does not care about reporting. In this chapter the two recurring nuisances are the propensity $\pi(x, z) = P(S = 1 \mid X = x, Z = z)$ (the probability the incumbent policy accepts an applicant with features $(x, z)$) and the accept-conditional outcome regression $g(x) = \mathbb{E}[Y \mid X = x, S = 1]$ (the booked-sample default rate at $X = x$). In plain English, $\pi$ models *who gets in* and $g$ models *how the people who got in performed*; neither is the answer the credit officer wants, but the AIPW score $\hat\mu(x) = g(x) + (S / \pi(x, z))(Y - g(x))$ needs both to recover the through-the-door PD. The name *nuisance* is historical (the term goes back to @neyman1948consistent and the semiparametric efficiency literature collected in @vandervaart1998asymptotic): these functions are a *nuisance* because their estimation error has to be controlled to get a clean inference statement on the parameter of interest, even though their values are not themselves the answer. Two practical consequences of this framing recur in the chapter. (i) *A nuisance can be misspecified and the estimator still consistent.* AIPW is *doubly robust* precisely in the sense that if either $\pi$ or $g$ equals the truth, the estimator recovers $\mu_0$ even when the other nuisance is wrong (@sec-ch10-heckman-vs-dml). (ii) *Nuisances can be fit by arbitrary machine learning.* Under Neyman orthogonality and cross-fitting, both $\hat\pi$ and $\hat g$ are allowed to converge at the slow $o(n^{-1/4})$ rate that flexible learners like gradient boosting deliver, and the second-stage estimator of the parameter of interest still inherits the textbook $\sqrt n$ rate and a usable confidence interval (@chernozhukov2018double, formalized at @eq-dml-rate). In a survival or expected-loss extension the nuisance pair generalizes naturally: $\pi$ becomes a censoring or selection hazard, $g$ becomes a conditional survival or loss surface, but the role in the estimator stays the same.

## The selection bias problem {#sec-ch10-reject}

### The naive fit and what it estimates

Fix the incumbent policy as a deterministic rule $s(x, z)$ with $S = s(X, Z)$ almost surely (we relax this later). The lender observes $\{(X_i, Z_i, Y_i) : S_i = 1\}$. A naive maximum-likelihood fit of a PD model $P(Y=1 \mid X; \beta)$ on this sample estimates

$$

\beta_{\text{naive}} = \arg\max_\beta \mathbb{E}\big[ \log P(Y \mid X; \beta) \big\vert S = 1 \big].

$$ {#eq-naive-target}

The target is the conditional on $S=1$. When the decision rule depends on $X$, the feature marginal $P(X \mid S=1)$ is shifted relative to $P(X)$. When the decision rule also correlates with unobservables that drive $Y$, the conditional $P(Y \mid X, S=1)$ is shifted relative to $P(Y \mid X)$. The first shift is covariate shift, fixable with reweighting when the target distribution is known. The second shift is selection bias proper, and it is what reject inference tries to repair.

The distinction matters because there exist rules that induce covariate shift without selection bias. If $s(X, Z) = \mathbf{1}\{Z > 0\}$ and $Z$ is independent of $(Y, X)$, then $P(Y \mid X, S=1) = P(Y \mid X)$ and there is nothing to correct. The pathology is when $s$ depends on $X$ in a way that covaries with the residual in the outcome model, or when $s$ depends on latent information unobserved to the modeler that is also predictive of $Y$. In consumer credit both are the norm. Loan officers read free-text notes, underwriters flag informal income, overlays include desk-level intuition, and all of that ends up baked into the accept decision but absent from the feature store.

### Two mechanisms {#sec-ch10-two-mechanisms}

To make the distinction concrete, fix one outcome model and run two selection rules through it. The outcome model has one observable feature $X$ and one latent residual $U$ that stands in for everything not in the feature store: informal-income flags, free-text underwriter notes, desk overlays. Two selection rules differ only in what drives the accept decision. @fig-ch10-two-mechanisms-a and @fig-ch10-two-mechanisms-b show the mechanism graphs in turn; the only structural difference is the arrow into $S$ in the second graph. In both graphs $Y$ is the latent default that *would* be realized if the applicant were funded; $S$ governs whether we observe $Y$, not whether it occurs, which is why no arrow runs from $S$ into $Y$.

::: no-panzoom

```{mermaid}

%%| label: fig-ch10-two-mechanisms-a

%%| fig-cap: "Scenario A: covariate shift only. Squares are observed at decision time; dashed circles are latent residuals the modeler does not see. The accept rule depends on observable $X$ and an independent noise $W$, so $P(X \\mid S=1)$ shifts relative to $P(X)$ but the conditional $P(Y \\mid X)$ is preserved. Reweighting on $X$ alone closes the gap."

flowchart TB

classDef obs fill:#cfd8dc,stroke:#37474f,color:#111;

classDef lat fill:#fff,stroke:#c62828,color:#c62828;

classDef noise fill:#fff,stroke:#90a4ae,color:#455a64;

classDef sel fill:#90caf9,stroke:#0d47a1,color:#111;

classDef out fill:#1976d2,stroke:#0d47a1,color:#fff;

XA["X<br/>features"]:::obs

UA(("U<br/>latent residual")):::lat

WA(("W<br/>noise, indep of U")):::noise

SA{{"S<br/>accept if W > X"}}:::sel

YA["Y<br/>default"]:::out

XA --> YA

UA --> YA

XA --> SA

WA --> SA

```

:::

::: no-panzoom

```{mermaid}

%%| label: fig-ch10-two-mechanisms-b

%%| fig-cap: "Scenario B: selection bias proper. The accept rule depends on a latent $V$ correlated with the outcome residual $U$ (correlation $\\rho$). The marginal $P(X \\mid S=1)$ is identical to Scenario A by construction, so both induce the same covariate shift, but here the conditional $P(Y \\mid X, S=1) \\ne P(Y \\mid X)$. That single arrow from $U$ into $V$ is what reject inference exists to address."

flowchart TB

classDef obs fill:#cfd8dc,stroke:#37474f,color:#111;

classDef lat fill:#fff,stroke:#c62828,color:#c62828;

classDef sel fill:#90caf9,stroke:#0d47a1,color:#111;

classDef out fill:#1976d2,stroke:#0d47a1,color:#fff;

XB["X<br/>features"]:::obs

UB(("U<br/>latent residual")):::lat

VB(("V<br/>Corr with U = 0.6")):::lat

SB{{"S<br/>accept if V > X"}}:::sel

YB["Y<br/>default"]:::out

XB --> YB

UB --> YB

XB --> SB

VB --> SB

UB -.->|rho| VB

```

:::

Now drive the two graphs through a simulation. Both scenarios share the through-the-door feature $X$, the outcome residual $U$, and the outcome rule $Y = \mathbf{1}\{0.7X + U > 0.5\}$. Scenario A's accept rule depends on an independent noise $W$, so within any $X$-bin the accept slice is a uniform random subsample of the bin and inherits the bin's $U$ distribution. Scenario B's accept rule depends on $V$ with $\mathrm{Corr}(U, V) = 0.6$, so within any $X$-bin the accepted ones are exactly the applicants with the highest $V$, which by correlation are the applicants with the highest $U$, which by the outcome rule are the applicants most likely to default. The marginal accept rate and the marginal $P(X \mid S=1)$ are identical across the two scenarios by construction.

```{python}

#| label: tbl-ch10-two-mechanisms

#| tbl-cap: "Default rate within $X$-bins on a synthetic through-the-door population (n = 200,000). The full-population column is the truth a credit officer wants. Scenario A's accept-only column matches the truth bin-by-bin within Monte-Carlo noise: the accept rule is independent of the outcome residual, so covariate shift skews the support of $X$ but not the conditional. Scenario B's accept-only column is uniformly higher than the truth: even within a fixed $X$-bin, accepts are the applicants with the highest $V$, and $V$ is correlated with $U$ which drives $Y$. The B-minus-truth column is the bias that reweighting on $X$ alone cannot close."

import numpy as np

import pandas as pd

rng = np.random.default_rng(20260503)

n = 200_000

rho = 0.6

U = rng.standard_normal(n)

V = rho * U + np.sqrt(1.0 - rho**2) * rng.standard_normal(n)

W = rng.standard_normal(n)

X = rng.standard_normal(n)

Y = ((0.7 * X + U) > 0.5).astype(int)

S_A = ((W - X) > 0.0).astype(int)

S_B = ((V - X) > 0.0).astype(int)

bin_edges = np.array([-2.0, -1.0, -0.5, 0.0, 0.5, 1.0, 2.0])

rows = []

for lo, hi in zip(bin_edges[:-1], bin_edges[1:]):

in_bin = (X >= lo) & (X < hi)

p_truth = Y[in_bin].mean()

p_A = Y[in_bin & (S_A == 1)].mean()

p_B = Y[in_bin & (S_B == 1)].mean()

rows.append({

"X bin": f"[{lo:+.1f}, {hi:+.1f})",

"n in bin": int(in_bin.sum()),

"P(Y=1|X) truth": f"{p_truth:.3f}",

"Scenario A P(Y=1|X,S=1)": f"{p_A:.3f}",

"Scenario B P(Y=1|X,S=1)": f"{p_B:.3f}",

"B - truth": f"{p_B - p_truth:+.3f}",

})

print(pd.DataFrame(rows).to_string(index=False))

print(

f"\nMarginal accept rate A: {S_A.mean():.3f} B: {S_B.mean():.3f}"

f"\nMarginal E[X | S=1] A: {X[S_A==1].mean():+.3f} B: {X[S_B==1].mean():+.3f}"

)

```

Read @tbl-ch10-two-mechanisms column by column. The first numeric column is the truth: the bin-conditional default rate on the full applicant pool. The Scenario A column matches it bin-by-bin within Monte-Carlo noise, which is exactly the statement that covariate shift alone does not move the conditional. The Scenario B column is higher than the truth in every bin, and the gap is uniform in sign. That uniform upward shift is what "selection bias proper" looks like in numbers: the accepted slice is *riskier* than the through-the-door population at every value of $X$, not because the lender accepted harder-$X$ applicants (the marginal $E[X \mid S=1]$ is identical across A and B by construction), but because within each $X$-bin the accepted ones have systematically higher $U$.

The geometric reading is that Scenario A's accept set is a uniform random sample of each $X$-slice of the through-the-door population, while Scenario B's accept set is the upper-$V$ tail of each $X$-slice, and the upper-$V$ tail is also the upper-$U$ tail because of the $\rho$ arrow. An importance-weighting estimator that targets $P(X)$ from $P(X \mid S=1)$ corrects both scenarios' marginal shift identically; the Scenario B residual gap survives the reweighting because the bin-conditional $U$ distribution is no longer $N(0,1)$ inside $S=1$.

The Scenario B residual conditional gap $P(Y \mid X, S=1) - P(Y \mid X)$, which survives reweighting on $X$, is what @sec-ch10-heckman-selection-correction writes as $\rho \sigma \lambda(\cdot)$ and adds as an extra regressor, what the copula-selection and deep-generative imputation methods in @sec-ch10-modern attack with a parametric joint on the latent errors, and what @sec-ch10-bureau-extrapolation sidesteps by importing $Y_B$ for the rejects directly. A separate family of estimators in @sec-ch10-modern (IPW, AIPW, DML, and covariate-shift importance weighting) addresses only the *marginal* gap $P(X) \neq P(X \mid S=1)$ and identifies the through-the-door PD by reweighting on $\pi(X, Z)$ alone; that family is consistent on Scenario A but biased on Scenario B, and the algebraic reason no amount of flexibility on its nuisances can cross the MAR/MNAR frontier is laid out in @sec-ch10-heckman-vs-dml. Each MNAR-branch method takes a different position on what structure or what data is available to identify $\rho$ (or its non-Gaussian generalization), but every method in this chapter exists because of @fig-ch10-two-mechanisms-b, not @fig-ch10-two-mechanisms-a.

### Rubin's missing-data taxonomy

The modern framing is @rubin1976inference. Call the full outcome vector $Y = (Y_{\text{obs}}, Y_{\text{mis}})$ and the missingness indicator $M = 1 - S$. The joint density factors as

$$

\begin{aligned}

p(Y_{\text{obs}}, Y_{\text{mis}}, M \mid X, Z; \theta, \psi)

={}& p(Y_{\text{obs}}, Y_{\text{mis}} \mid X; \theta) \\

& \cdot p(M \mid Y_{\text{obs}}, Y_{\text{mis}}, X, Z; \psi).

\end{aligned}

$$ {#eq-joint-missing}

Three regimes matter:

- Missing completely at random (MCAR): $p(M \mid Y, X, Z) = p(M)$. Selection is independent of both observed and unobserved data. Naive fits are consistent. This is the regime a randomized credit-offer experiment generates.

- Missing at random (MAR): $p(M \mid Y, X, Z) = p(M \mid X, Z)$. Selection depends only on observables. Inverse probability weighting on $(X, Z)$ is sufficient. This is the regime that augmentation and bureau-based extrapolation lean on.

- Missing not at random (MNAR): $p(M \mid Y, X, Z)$ depends on $Y$ even after conditioning on $(X, Z)$. Selection is driven by something not in the feature store that also drives default. No amount of reweighting on $(X, Z)$ suffices. This is the regime that motivates Heckman and the impossibility result.

::: {.callout-tip appearance="simple"}

**Reader trap: knowing the rule is not the same as MAR.** A natural first reaction to the credit setup is: *we know why the bank rejected these applicants (low score, failed affordability, blacklist hit), so the missingness must be MAR.* That intuition is wrong in general, and the wrongness is the reason this chapter exists.

MAR is a statement about whether the rule depends only on variables *in the modeler's feature store*, not whether the *lender* knows what the rule is. Those two information sets are usually different. The lender's decision sits on top of $(X, Z)$ plus whatever the loan officer, the policy overlay, the dealer-tier override, the fraud-flag committee, or an undocumented bureau pull added on the day of decision. The modeler typically inherits $(X, Z)$ and almost none of the residual.

A quick diagnostic. Can you reconstruct the accept-or-decline decision exactly from $(X, Z)$ alone?

- Yes: the missingness is MAR. The remaining problem is overlap. Some regions of $(X, Z)$ have $P(S{=}1 \mid X, Z) = 0$ by policy, and $P(Y \mid X, Z)$ is unidentified there without extra structure. That is the Hand-Henley region of @sec-ch10-impossibility, not an MNAR failure.

- No: the part of the rule you cannot reproduce sits inside the latent error $V$. Whenever underwriter judgment is informative about default (which is the entire reason banks pay underwriters), $V$ correlates with the outcome error $U$, and the missingness is MNAR. Reweighting on $(X, Z)$ cannot recover $P(Y \mid X)$ on the rejected segment.

Plain-English version for the credit officer in the room. A bureau-score cutoff at 620 looks MAR-by-design when you draw the policy on the board. The realised accept set is not the score-cutoff set; it is the score-cutoff set minus manual declines, plus manual approvals on thin files, minus fraud-flag holds, plus regional appetite overrides. That residual layer is exactly what the override committee gets paid to add, and what it adds is correlated with default by construction. So the realised accept set is the upper tail of a latent index the modeler does not see, not a clean function of $(X, Z)$, and the gap between "knowing the rule" and "MAR" is precisely the size of that override layer.

The working posture in this chapter is therefore to treat retail reject inference as MNAR by default, and to earn the MAR label only on a slice of the portfolio where the conditioning-set enrichment diagnostic (next paragraph, plus @sec-ch10-other-assumption-diagnostics) shows that absorbing more of the underwriter's view stops moving $P(Y \mid X, Z, S{=}1)$.

:::

The practical trap is that MAR versus MNAR is untestable from the observed data alone. The observed likelihood integrates over the unobserved $Y_{\text{mis}}$, and two joint densities with identical $p(Y_{\text{obs}} \mid X, Z, S=1)$ can differ arbitrarily on $p(Y_{\text{mis}} \mid X, Z, S=0)$. Any claim that the selection is MAR is an assumption on structure, not a hypothesis that the data can refute.

Untestable in the strict identification sense does not mean uninformative. The data cannot adjudicate MAR versus MNAR globally, but several diagnostics shift the validator's posterior on which regime is operating, and credible reject-inference work pairs the structural assumption with at least one of them. First, sensitivity bounds quantify how strongly the latent driver would have to push selection before the MAR-based PD breaches the decision tolerance: Conley plausibly-exogenous bounds (@sec-ch10-iv-diagnostics-code), Rosenbaum $\Gamma$ for matched designs, and Oster $\delta$ for linear specifications. If a one-standard-deviation push on the unobservable leaves the PD untouched, MNAR may be present but is decision-irrelevant. Second, worst-case Manski and Horowitz bounds on the rejected segment hold under any selection mechanism; if their width is narrow enough to sign the lending decision the MAR-versus-MNAR debate is moot, and if it is wide the data are simply silent on the question. Third, policy quasi-experiments such as cutoff fuzziness, randomized overlays, and rare blanket-approval pilots (@sec-ch10-design-based) generate small windows of MAR-by-construction in which the MAR-extrapolated PD can be benchmarked against realized default among previously-rejected applicants. Fourth, conditioning-set enrichment is a stability test: as the feature representation absorbs information the underwriter saw (income-doc flags, branch identifier, originator, soft-signal extracts), a conditional default rate that stabilizes across additions is consistent with MAR within the enriched set, while a curve that keeps shifting with each new variable suggests the latent driver is still outside the conditioning set. Fifth, the Heckman $\rho$ estimate is informative when an exclusion restriction is defensible (@sec-ch10-heckman-assumptions), and uninformative otherwise because identification then rests on the bivariate-normal functional form alone. None of these falsify the impossibility claim. They let the validator state a defensible posterior on the mechanism rather than cite an assumption and stop.

### The credit officer's version

A credit officer rarely thinks in these terms. The version that lands is a counterfactual: hold out every fifth applicant at random, approve them regardless of score, watch the portfolio. That is the golden standard, and where it exists (often in small test-and-learn pockets inside marketing) it is the only evidence that settles the question. The rest of reject inference is an attempt to simulate this experiment from non-experimental data, with varying degrees of honesty about what that requires.

Two assumptions are load-bearing.

1. One, the feature representation $X$ is rich enough that the residual selection on unobservables is small.

2. Two, the decision rule has some idiosyncratic variation, either an instrument (a feature that shifts $S$ without shifting $Y$) or overlap (a positive probability of accept at every $X$). The second is policy design: a bureau-cut at 620 with zero variance at 619 and 621 produces no overlap, while stochastic approvals or score-band-level manual review produce some.

Without either assumption, reject inference is extrapolation to regions the data has never seen, and the extrapolation relies entirely on the functional form.

The punchline for this chapter is that every reject inference method is a tradeoff between these two assumptions and the price of being wrong. We treat them in increasing order of the structure they impose: augmentation and parceling (@sec-ch10-augmentation-hsias-parceling-and-its-fuz) lean on MAR plus smoothness; Heckman (@sec-ch10-heckman-selection-correction) leans on bivariate normality plus an exclusion restriction; semi-supervised methods (@sec-ch10-em) lean on cluster structure; and the impossibility result (@sec-ch10-impossibility) tells us what none of them can do without a genuinely exogenous source of variation.

## Formal setup

The through-the-door population generates an i.i.d. sample $(X_i, Z_i, U_i, V_i)$ from a joint distribution $F$. The latent default score is

$$

Y^*_i = X_i^\top \beta + U_i, \qquad Y_i = \mathbf{1}\{Y^*_i > 0\},

$$ {#eq-latent-default}

and the latent selection score is

$$

S^*_i = X_i^\top \gamma_X + Z_i^\top \gamma_Z + V_i, \qquad S_i = \mathbf{1}\{S^*_i > 0\}.

$$ {#eq-latent-selection}

The errors $(U, V)$ have zero mean and joint distribution $G$. The Heckman model assumes $G$ is bivariate normal with unit marginals and correlation $\rho$. The exclusion restriction holds if $Z$ enters @eq-latent-selection but not @eq-latent-default.

The observed-data likelihood for any model in this family, given $n$ i.i.d. applicants, is

$$

\mathcal{L}(\theta) = \prod_{i: S_i = 0} P(S_i = 0 \mid X_i, Z_i; \theta) \times \prod_{i: S_i = 1} P(S_i = 1, Y_i \mid X_i, Z_i; \theta).

$$ {#eq-observed-likelihood}

where:

- $\mathcal{L}(\theta)$ is the observed-data likelihood as a function of the full parameter vector $\theta = (\beta, \gamma_X, \gamma_Z, \rho)$, that is, the default coefficients, the selection coefficients, and the error correlation.

- $\theta$ collects every parameter the model needs to estimate, so maximizing $\mathcal{L}(\theta)$ jointly fits the default equation, the selection equation, and their dependence.

- $i = 1, \ldots, n$ indexes the i.i.d. applicants in the through-the-door population, both accepted and rejected.

- $S_i \in \{0, 1\}$ is the selection indicator: $S_i = 1$ if applicant $i$ was accepted (booked), $S_i = 0$ if rejected.

- $Y_i \in \{0, 1\}$ is the default outcome, observed only for $S_i = 1$.

- $X_i$ is the vector of covariates that enters both the default and selection equations (income, debt-to-income, bureau score, and so on).

- $Z_i$ is the vector of exclusion-restriction variables that enter the selection equation only (for example, branch capacity or a policy threshold), not the default equation.

- $\prod_{i: S_i = 0} P(S_i = 0 \mid X_i, Z_i; \theta)$ is the rejected-side contribution: for each rejected applicant we observe only that they were rejected, so the likelihood contains only the marginal selection probability.

- $\prod_{i: S_i = 1} P(S_i = 1, Y_i \mid X_i, Z_i; \theta)$ is the accepted-side contribution: for each accepted applicant we observe both acceptance and the default label, so the likelihood contains the joint probability of being accepted and defaulting (or not).

The joint factor on the accepted side is what distinguishes Heckman from a naive fit: $P(S=1, Y \mid X, Z)$ integrates over $(U, V)$ with the joint distribution, so $P(Y \mid X, Z, S=1) \neq P(Y \mid X)$ whenever $\rho \neq 0$.

Intuitively, the naive fit treats the accepted likelihood as if $S=1$ were just a sample-selection convenience that drops out once we condition on $X$. The Heckman likelihood refuses that shortcut. Because $U$ (the default shock) and $V$ (the selection shock) share unobserved drivers, knowing that an applicant cleared underwriting ($S=1$) is itself information about $U$, and so about $Y$. The integral over the joint distribution is the formal way of saying: average the default probability across the values of $U$ that are consistent with this applicant having been accepted, not across all values of $U$ in the population. Those two averages disagree exactly to the extent that $\rho \neq 0$.

In our credit case, the unobserved component of $V$ is everything the underwriter saw that we did not record: handwritten notes, the way the applicant answered probing questions, branch manager judgement on a marginal file, soft signals from a Tet-season cash-flow review. If those same soft signals also predict repayment (and they typically do, which is why the underwriter weighted them), then $\mathrm{Corr}(U,V) = \rho < 0$ in our sign convention: applicants whose unobservables push them toward acceptance also have unobservables that push them away from default. Conditioning on $S=1$ then pulls the default distribution down. A naive logistic regression on booked loans estimates this pulled-down distribution and silently calls it the through-the-door PD. The joint factor on the accepted side is the bookkeeping device that prevents that silent substitution.

For outcomes, we consider two canonical cases. In the linear case (used mostly in econometric wage equations), $Y = X^\top \beta + U$ is continuous and observed for $S=1$. In the binary case (which dominates credit), $Y \in \{0,1\}$ is a probit outcome. Both have closed-form two-step estimators based on the inverse Mills ratio, derived in the next section.

## The impossibility result {#sec-ch10-impossibility}

Before any method, we have to know what the observed data can and cannot answer. The impossibility result of @hand1997statistical is the identification ceiling that every reject-inference estimator either accepts or pays to escape; the methods that follow are organized around what they pay.

### Hand and Henley's observation

@hand1997statistical stated what is arguably the central limit of reject inference as a statistical procedure. The observed data consist of

$$

\{(X_i, Z_i, S_i)\}_{i=1}^n \cup \{(X_i, Y_i) : S_i = 1\}.

$$ {#eq-observed-data}

In plain English: for every applicant $i$ we see their features $X_i$, any side information $Z_i$ (for example a referral channel or a credit-bureau pull), and the underwriting decision $S_i$ (accept or reject). We see the repayment outcome $Y_i$ only for the applicants who were accepted and booked. For the rejects we have an application file and a "no" stamp on it, nothing else. A concrete picture: out of 10,000 applications, 4,000 are booked and we learn whether each of the 4,000 defaulted; for the other 6,000 we have application data only.

The goal is to estimate $P(Y=1 \mid X=x)$ for every $x$, including the region where $P(S=1 \mid X=x) = 0$. In words, we want the through-the-door default probability for every kind of applicant, including the kinds that the lender's policy has historically rejected with probability one ("nobody with a FICO under 580 and a thin file ever got booked here"). In that region, the observed sample contains zero information about the $Y$ distribution. Any estimator that delivers a value for $P(Y=1 \mid X=x)$ in that region is extrapolating from either a parametric assumption or an auxiliary data source. The picture: we are being asked to draw a default curve over a part of feature space that contains no booked loans at all, and so no defaults and no non-defaults to learn from; any number we report there has to come from a modeling assumption (such as "the same logistic curve continues") or from outside data (such as a bureau-wide cohort of applicants other lenders did book).

More strongly: two data-generating processes with identical $P(Y \mid X, S=1)$ on $\{x : P(S=1 \mid X=x) > 0\}$ and different $P(Y \mid X, S=0)$ on $\{x : P(S=1 \mid X=x) = 0\}$ produce identical observed-data likelihoods. Read as a sentence: imagine two parallel worlds in which the booked-loan default behavior is exactly the same, but the rejected applicants behave very differently. World A: rejects would have defaulted at 20 percent. World B: rejects would have defaulted at 80 percent. We cannot tell which world we are in from our data, because the rejected applicants never produced an outcome we could see. Maximum-likelihood estimation cannot distinguish them, and no transformation of the data can either. The observed sample is simply uninformative about that region. The likelihood, which is the only thing a statistical estimator has to work with, takes the same numerical value in both worlds, so no amount of clever fitting can tell them apart.

### Formal statement

Let $\mathcal{F}$ be the set of all joint distributions $F_{X, Z, S, Y}$ consistent with the observed data likelihood. Think of $\mathcal{F}$ as the catalog of every possible "true world" that could have produced the application book we actually see. Partition $\mathcal{F}$ by the through-the-door conditional default function $f(x) = P_F(Y=1 \mid X=x)$. That is, group those candidate worlds by what they imply about the default rate for each kind of applicant, accepted or not. Then the set

$$

\mathcal{F}(f) = \{F \in \mathcal{F} : P_F(Y=1 \mid X=x) = f(x) \text{ for all } x\}

$$ {#eq-f-of-f}

is the bucket of worlds that share the same through-the-door curve $f$. Its key property: for any two $f_1, f_2$ with $f_1 = f_2$ on the support of $X$ in the accepted sample, $\mathcal{F}(f_1)$ and $\mathcal{F}(f_2)$ share the same observed-data likelihood. In layman terms: if two candidate truths agree on the booked-applicant region but disagree on the rejected region, the data cannot tell which one is correct. Reject inference must pick one element of the equivalence class; the observed data does not pin down which. So choosing a reject-inference method is, in effect, choosing which member of this tied set to call "the answer", and that choice is made by assumption, not by the data.

The proof is a counting argument. The observed likelihood depends on $P(S=1, Y \mid X, Z)$ on the accept side and $P(S=0 \mid X, Z)$ on the reject side, integrated over $X$ and $Z$. In simple terms, the data tells us two things and only two things: for booked applicants we learn the joint behavior of "accepted and defaulted"; for rejected applicants we learn only that they were rejected. On the reject side, the marginal $P(S=0 \mid X, Z)$ places no constraint on $P(Y \mid X, Z, S=0)$, because $Y$ is unobserved. Knowing the reject rate tells us nothing about how the rejects would have repaid. On the accept side, $P(S=1, Y \mid X, Z)$ pins down $P(Y \mid X, Z, S=1)$ times $P(S=1 \mid X, Z)$. The booked side tells us the booked-applicant default rate and the acceptance rate, but only for booked applicants. Neither component constrains $P(Y \mid X, Z, S=0)$. Neither piece touches the would-have-been default rate among rejects. The through-the-door conditional $P(Y \mid X, Z)$ is the mixture

$$

P(Y \mid X, Z) = P(Y \mid X, Z, S=1) P(S=1 \mid X, Z) + P(Y \mid X, Z, S=0) P(S=0 \mid X, Z),

$$ {#eq-mixture}

which reads as: the population default rate for a given profile is a weighted average of the default rate among accepts (weighted by how often that profile is accepted) and the default rate among rejects (weighted by how often it is rejected). Component by component:

- $P(Y \mid X, Z)$ is the **through-the-door default probability**: across everyone who ever walked in with features $X$ and side information $Z$, what fraction would have defaulted on the product. This is the quantity the credit-risk team actually wants for portfolio strategy, pricing, and capital, because it does not depend on the current accept/reject policy.

- $P(Y \mid X, Z, S=1)$ is the **booked-applicant default rate** for that profile: the default rate we see in the loan-tape among applicants of type $(X, Z)$ who were approved and funded. This is what a naive logistic regression on booked loans estimates.

- $P(S=1 \mid X, Z)$ is the **acceptance probability** (also called the propensity score in the design-based literature): the fraction of $(X, Z)$ applicants the underwriting policy lets through. For a thin-file applicant this can be near zero; for a prime-bureau applicant it can be near one.

- $P(Y \mid X, Z, S=0)$ is the **counterfactual reject default rate**: the fraction of $(X, Z)$ applicants who were turned away that would have defaulted had they been booked. Nobody observes this in the data, because rejected applicants never produce a $Y$.

- $P(S=0 \mid X, Z) = 1 - P(S=1 \mid X, Z)$ is the **rejection probability**: the residual share of $(X, Z)$ applicants the policy turns down. It is mechanically determined once the acceptance probability is set.

For example, if 70 percent of profile-$x$ applicants are booked and they default at 5 percent, and the 30 percent who are rejected would have defaulted at 25 percent, the through-the-door rate is $0.7 \times 0.05 + 0.3 \times 0.25 = 0.11$. The 11 percent is what the portfolio truly faces if the policy were lifted; the 5 percent is what the loan tape shows; the 6-point gap is exactly the booking selection effect that reject inference exists to recover. And the unobserved component $P(Y \mid X, Z, S=0)$ is free. The reject-side default rate (the 25 percent in the example) is unconstrained by the data, so swapping in any other number, 5, 50, or 80 percent, produces an equally valid candidate truth. Hand and Henley's result is that freedom: the data fixes the booked-side default rate and the accept/reject split, but it puts no number on the rejected side, and every choice for that number yields a consistent story.

### What the theorem does not say

The impossibility is conditional on using only the observed sample under the stated assumptions. It does not prevent estimation under additional assumptions. Heckman's bivariate normality is such an assumption: it ties $P(Y \mid X, Z, S=0)$ to $P(Y \mid X, Z, S=1)$ through $\rho$ and the exclusion restriction. If the assumption holds, identification is restored. If it fails, Heckman gives an answer that is no better than parceling; it is just a specific wrong answer rather than an admission of ignorance.

The theorem also does not rule out progress when $\{x : P(S=1 \mid X=x) = 0\}$ is empty. Stochastic acceptance, whether from a random-trial overlay or from residual noise in judgmental underwriting, restores overlap. Under overlap every $x$ has both accepted and rejected observations, and inverse-probability weighting recovers $P(Y \mid X)$ consistently under MAR. Hand and Henley applies in the extreme case of perfectly deterministic acceptance by $X$; overlap is the escape.

### Practical implication

The impossibility result gives us a discipline. Any reject inference method should be paired with a statement of what extra structure it imposes and what happens when that structure fails. Parceling assumes MAR plus smoothness. Heckman assumes bivariate normality plus an exclusion restriction. Self-training assumes cluster structure in $X$. Bureau-based extrapolation swaps the assumption for an auxiliary dataset, with its own selection problem. No method solves the problem without one of these assumptions. Model risk management should document which. The remainder of the chapter walks the method families in order of weakening assumptions: parceling (@sec-ch10-augmentation-hsias-parceling-and-its-fuz) and EM (@sec-ch10-em) under MAR, Heckman (@sec-ch10-heckman-selection-correction) and copulas (@sec-ch10-modern) under parametric MNAR, and the design-based / observable-engine route (@sec-ch10-observable, with the propensity-weighted variant in @sec-ch10-heckman-vs-dml) that sidesteps the joint by injecting or observing the propensity. Bureau-based extrapolation (@sec-ch10-bureau-extrapolation) sits alongside these as the route that replaces a parametric assumption with an auxiliary dataset.

### An empirical impossibility result

To demonstrate @eq-f-of-f directly, we construct two data generating processes with identical $P(Y \mid X, S=1)$ and different $P(Y \mid X, S=0)$, then show that every reject inference method that uses only the observed data fits them identically.

```{python}

#| label: ch10-impossibility-imports

import numpy as np

import matplotlib.pyplot as plt

import sys

sys.path.insert(0, '../code')

from creditutils import stable_sigmoid

from sklearn.linear_model import LogisticRegression

```

```{python}

rng2 = np.random.default_rng(777)

m = 30_000

x_imp = rng2.standard_normal(m)

# Acceptance rule depends purely on x: everyone with x > -0.3 is accepted

accept_imp = x_imp > -0.3

# Accepted conditional P(Y=1 | X, S=1) is the same in both scenarios

p_acc = stable_sigmoid(1.0 * x_imp - 1.0)

y_acc = (rng2.uniform(size=m) < p_acc).astype(int)

# Two different P(Y=1 | X, S=0):

# A: same logistic (benign extrapolation)

# B: systematically higher (the classic adverse-selection story)

pA = stable_sigmoid(1.0 * x_imp - 1.0)

pB = stable_sigmoid((1.0 * x_imp - 1.0) + 2.0)

y_rejA = (rng2.uniform(size=m) < pA).astype(int)

y_rejB = (rng2.uniform(size=m) < pB).astype(int)

yA = np.where(accept_imp, y_acc, y_rejA)

yB = np.where(accept_imp, y_acc, y_rejB)

# Observed data is identical on the accept side; fit the same accept-only model

modelA = LogisticRegression().fit(x_imp[accept_imp].reshape(-1,1),

yA[accept_imp])

modelB = LogisticRegression().fit(x_imp[accept_imp].reshape(-1,1),

yB[accept_imp])

print(f"Scenario A: intercept={modelA.intercept_[0]:.3f}, coef={modelA.coef_[0,0]:.3f}")

print(f"Scenario B: intercept={modelB.intercept_[0]:.3f}, coef={modelB.coef_[0,0]:.3f}")

print(f"True rejected default rate A: {y_rejA[~accept_imp].mean():.3f}")

print(f"True rejected default rate B: {y_rejB[~accept_imp].mean():.3f}")

```

The accept-only fits are numerically identical across the two scenarios. The true rejected default rates differ by roughly 10 percentage points. Any extrapolation method that does not use information beyond the accepted sample will produce the same PD curve on the rejected side for both scenarios. One curve is right; the other is off by 10 points of PD. The observed data contains zero signal about which one is correct. This is the Hand and Henley result rendered in code.

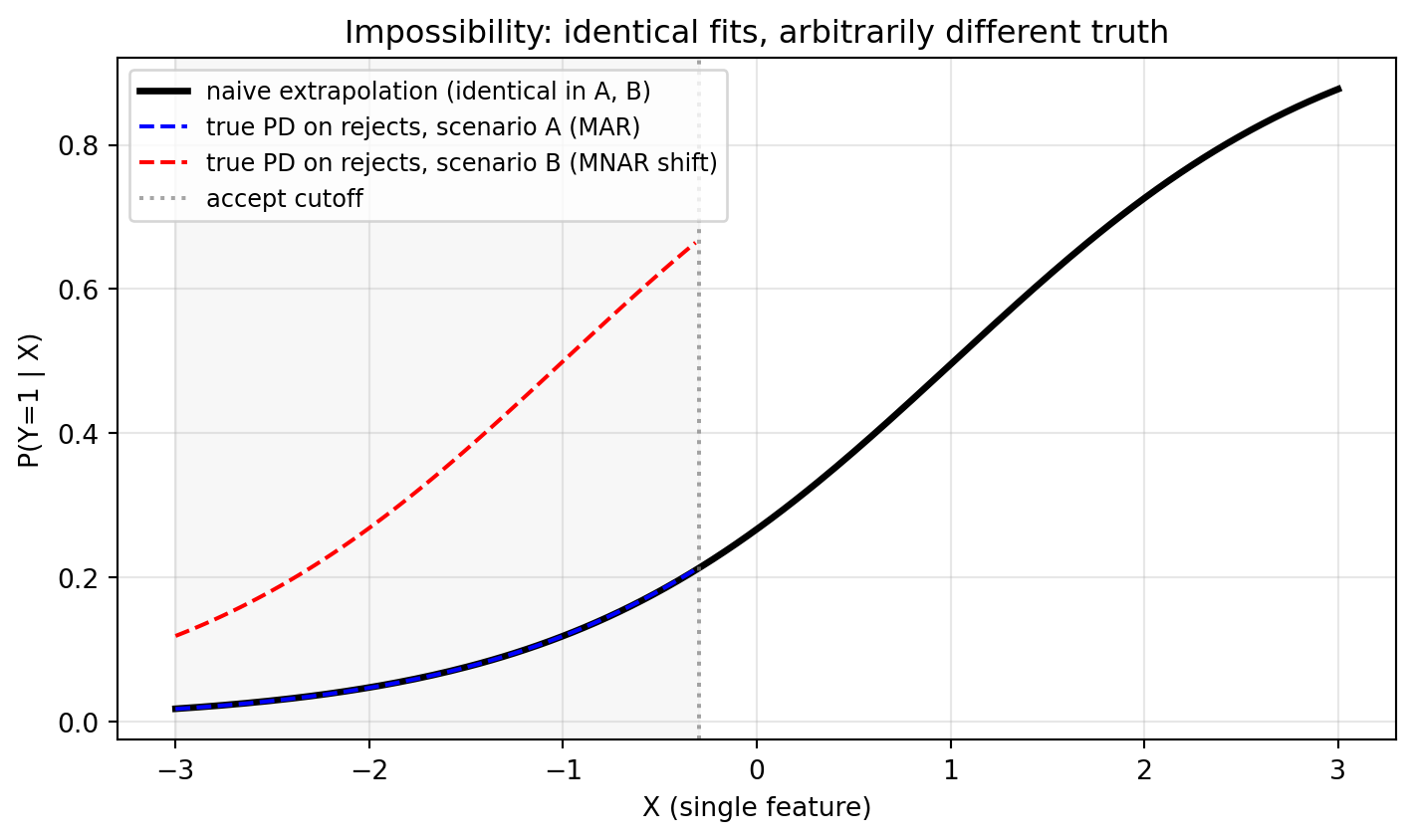

### Visualizing the impossibility

```{python}

cutoff = -0.3

grid = np.linspace(-3, 3, 200)

pred_A = modelA.predict_proba(grid.reshape(-1,1))[:, 1]

pred_B = modelB.predict_proba(grid.reshape(-1,1))[:, 1]

# pred_A and pred_B are numerically identical: same accepted-only fit.

# Truth differs only on the rejected side (grid < cutoff). On the accepted

# side the DGP is identical across scenarios by construction, so true_A and

# true_B both coincide with the naive curve there. Mask the truth curves to

# the rejected region to avoid implying a divergence where there is none.

rej = grid < cutoff

true_A_rej = stable_sigmoid(1.0 * grid[rej] - 1.0)

true_B_rej = stable_sigmoid((1.0 * grid[rej] - 1.0) + 2.0)

fig, ax = plt.subplots(figsize=(7.5, 4.5))

ax.plot(grid, pred_A, "k-", lw=2.5, label="naive extrapolation (identical in A, B)")

ax.plot(grid[rej], true_A_rej, "b--", lw=1.5,

label="true PD on rejects, scenario A (MAR)")

ax.plot(grid[rej], true_B_rej, "r--", lw=1.5,

label="true PD on rejects, scenario B (MNAR shift)")

ax.axvline(cutoff, color="gray", ls=":", alpha=0.7, label="accept cutoff")

ax.axvspan(grid.min(), cutoff, color="gray", alpha=0.06)

ax.set_xlabel("X (single feature)")

ax.set_ylabel("P(Y=1 | X)")

ax.set_title("Impossibility: identical fits, arbitrarily different truth")

ax.legend(loc="upper left", fontsize=9)

ax.grid(alpha=0.3)

plt.tight_layout()

plt.show()

```

Read the figure in two regions. Right of the accept cutoff (the observed-data region) the naive fit, the scenario-A truth, and the scenario-B truth all coincide; the figure plots only the black line there because the two truths are identical to it by construction. Left of the cutoff (the rejected region) the black line is the unique extrapolation the accepted-only data can support, and the blue and red dashed curves are both consistent with that same observed data: they share an identical $P(Y \mid X, S=1)$, so the accepted-only likelihood cannot distinguish them. Reject inference methods that claim to discriminate between A and B are using a parametric assumption ($\rho$ being well-constrained in Heckman under bivariate normality, say) or an auxiliary data source (bureau outcomes). Neither is free.

## Augmentation: Hsia's parceling and its fuzzy variant {#sec-ch10-augmentation-hsias-parceling-and-its-fuz}

### The procedure

@hsia1978credit proposed the first systematic reject inference method in a regulatory-compliance context. The idea is elementary: fit a PD model on accepted loans, score the rejected applicants, split the rejected into score bands, assign each band a bad rate using the accepted bad rate in that band, and refit on the augmented sample. "Parceling" refers to the score-band partition. "Fuzzy augmentation" softens the assignment: instead of a 0/1 label per rejected applicant, each rejected applicant contributes a fractional weight for $Y=1$ equal to the assigned bad rate and a fractional weight for $Y=0$ equal to its complement.

#### Algorithm: Hsia parceling with fuzzy augmentation {#sec-ch10-parceling-algorithm .unnumbered}

**Inputs.** Training rows $(X_i, S_i, Y_i)$ for $i = 1, \ldots, n$, with $Y_i$ observed only when $S_i = 1$. Number of bands $K$ (industry default 5 to 10). Scaling factor $\tau \geq 1$ ($\tau = 1$ is the MAR baseline; $\tau > 1$ encodes a belief that rejects are riskier than accepteds at the same score).

**Output.** Refit PD model $\hat p_{\text{aug}}(\cdot)$.

1. **Fit accepted-only PD.** Estimate $\hat p_A$ by maximum likelihood on $\{(X_i, Y_i) : S_i = 1\}$.

2. **Score everyone.** Compute $s_i = \hat p_A(X_i)$ for all applicants, accepted and rejected.

3. **Cut bands.** Set band edges $q_0 < q_1 < \cdots < q_K$ as $K$-quantiles of $\{s_i : S_i = 1\}$; let $B_b = [q_{b-1}, q_b)$ for $b = 1, \ldots, K$.

4. **Compute band bad rates.** For each band, $\displaystyle \bar\pi_b = \frac{\sum_{i: S_i=1, s_i \in B_b} Y_i}{\sum_{i: S_i=1, s_i \in B_b} 1}$.

5. **Assign rejects to bands.** For each $j$ with $S_j = 0$, set $b(j) = b$ such that $s_j \in B_b$.

6. **Build the soft label weight.** $w_j = \min(1, \tau \cdot \bar\pi_{b(j)})$ for each reject; $\tau = 1$ recovers the band rate exactly.

7. **Refit.** Solve the weighted maximum-likelihood problem in @eq-fuzzy-augmentation with rows: $(X_i, Y_i, 1)$ for each accepted, and the pair $(X_j, 1, w_j),\; (X_j, 0, 1 - w_j)$ for each reject.

The convention is that each rejected applicant contributes total weight 1 across the two augmented rows, so the refit treats accepteds and rejects on equal footing per applicant. Increasing $\tau$ shifts mass from the $Y=0$ row to the $Y=1$ row but does not create a new applicant.

Formally, let $\hat p_0(x) = P(Y=1 \mid X=x, S=1)$ be the accepted-only PD model. Let $\tau(x)$ be a scaling factor that inflates the PD for rejected applicants relative to accepted applicants at the same $x$, reflecting the belief that the incumbent policy correctly identified higher risk in rejects. Fuzzy augmentation solves

$$

\begin{aligned}

\hat \beta_{\text{fuzzy}} = \arg\max_\beta\;\;

& \sum_{i: S_i=1} \log P(Y_i \mid X_i; \beta) \\

& + \sum_{i: S_i=0} \Big[ w_i \log P(1 \mid X_i; \beta) + (1 - w_i) \log P(0 \mid X_i; \beta) \Big],

\end{aligned}

$$ {#eq-fuzzy-augmentation}

where $w_i = \tau(X_i) \hat p_0(X_i)$ is the soft-label weight.

Setting $\tau \equiv 1$ is the MAR assumption in disguise: the accepted PD curve, extrapolated to the rejected region, is the true PD curve. Setting $\tau > 1$ is a hand-tuned adjustment. Industry lore uses $\tau \in [2, 5]$, with higher values for riskier product segments. The *policy*-accepted sample alone cannot pin $\tau$, because every applicant in it survived a selection rule that depends on $(U, V)$; the conditional default rate it reveals is $P(Y \mid X, S=1)$, not $P(Y \mid X)$. To identify $\tau(x)$ data-driven, the modeller needs a sample whose acceptance was assigned independently of the policy decision. Two such sources exist in production: a bureau pull on rejected applicants (@sec-ch10-bureau-extrapolation), or a champion-challenger random-accept holdout where a small fraction of applicants is approved regardless of policy score (@sec-ch10-design-based, D1). The latter delivers a banded estimator $\hat\tau(x)$ with bootstrap confidence intervals; we work it out end-to-end on the synthetic lender in @sec-ch10-tau-from-holdout.

### A pen-and-paper trace {#sec-ch10-parceling-pen-paper}

Before scaling to the simulation in @sec-ch10-parceling-worked-example, we walk every step of the algorithm on a 12-applicant accepted sample with three rejects and $K = 3$ bands. The numbers are small enough to verify by hand and large enough to show non-degenerate band rates.

| $i$ | $X_i$ | $S_i$ | $Y_i$ | $\hat p_A(X_i)$ | band |

|----:|:------:|:-----:|:--------:|:---------------:|:----:|

| 1 | $-1.5$ | 1 | 0 | 0.05 | 1 |

| 2 | $-1.0$ | 1 | 0 | 0.10 | 1 |

| 3 | $-0.7$ | 1 | 0 | 0.15 | 1 |

| 4 | $-0.4$ | 1 | 1 | 0.20 | 1 |

| 5 | $-0.1$ | 1 | 0 | 0.30 | 2 |

| 6 | $0.2$ | 1 | 0 | 0.40 | 2 |

| 7 | $0.5$ | 1 | 1 | 0.50 | 2 |

| 8 | $0.7$ | 1 | 1 | 0.55 | 2 |

| 9 | $0.9$ | 1 | 0 | 0.65 | 3 |

| 10 | $1.1$ | 1 | 1 | 0.75 | 3 |

| 11 | $1.3$ | 1 | 1 | 0.82 | 3 |

| 12 | $1.5$ | 1 | 1 | 0.88 | 3 |

| R1 | $-0.3$ | 0 | (unobs.) | 0.18 | 1 |

| R2 | $0.3$ | 0 | (unobs.) | 0.45 | 2 |

| R3 | $1.2$ | 0 | (unobs.) | 0.80 | 3 |

**Steps 1 to 3.** $\hat p_A$ is fit on rows 1 to 12 (the accepteds). The score column $\hat p_A(X_i)$ ranks applicants by predicted PD. Cutting at the tertiles of the 12 accepted scores produces three bands of size 4: $B_1 = [0, 0.25]$, $B_2 = (0.25, 0.60]$, $B_3 = (0.60, 1]$. Each reject is dropped into the band whose interval contains its score.

**Step 4 (band bad rates).** Band 1: 1 bad among 4 accepteds, $\bar\pi_1 = 0.25$. Band 2: 2 bads among 4, $\bar\pi_2 = 0.50$. Band 3: 3 bads among 4, $\bar\pi_3 = 0.75$. The bad rate increases monotonically with band, which is the regularity condition every implementation should check (a non-monotone column is a sign of too many bands or too small a sample).

**Steps 5 to 6 (assign and weight,** $\tau = 1$).

| reject | band | $w_j = \bar\pi_{b(j)}$ | $1 - w_j$ |

|:------:|:----:|:----------------------:|:---------:|

| R1 | 1 | $0.25$ | $0.75$ |

| R2 | 2 | $0.50$ | $0.50$ |

| R3 | 3 | $0.75$ | $0.25$ |

**Step 7 (augmented training set).** Each reject becomes two weighted rows; the combined set has 12 accepted rows (weight 1, real label) and $3 \times 2 = 6$ reject rows for a total of 18 rows that go into a `LogisticRegression(...).fit(X, y, sample_weight=w)` call.

| row | $X$ | $Y$ | weight | source |

|:---:|:--------:|:---:|:------:|:-------------------------------:|

| ... | ... | ... | $1$ | accepteds 1 to 12 (real labels) |

| 13 | $X_{R1}$ | $1$ | $0.25$ | R1 fuzzy bad |

| 14 | $X_{R1}$ | $0$ | $0.75$ | R1 fuzzy good |

| 15 | $X_{R2}$ | $1$ | $0.50$ | R2 fuzzy bad |

| 16 | $X_{R2}$ | $0$ | $0.50$ | R2 fuzzy good |

| 17 | $X_{R3}$ | $1$ | $0.75$ | R3 fuzzy bad |

| 18 | $X_{R3}$ | $0$ | $0.25$ | R3 fuzzy good |

**Reading R1's contribution.** R1 contributes

$$

0.25 \log p(X_{R1}; \beta) + 0.75 \log\big(1 - p(X_{R1}; \beta)\big)

$$

to the augmented log-likelihood, where $p(\cdot; \beta)$ is the refit PD. Treated as a free probability, this expression is maximized at $p(X_{R1}; \beta) = 0.25$ (the cross-entropy minimum of a $\mathrm{Bernoulli}(0.25)$ target). The refit therefore pulls the fitted PD curve at $X_{R1} = -0.3$ toward $0.25$, the band-1 accepted bad rate, exactly as the prose intuition predicted.

**Effect of** $\tau > 1$. Set $\tau = 2$. Then $w_{R1} = \min(1, 2 \cdot 0.25) = 0.50$, $w_{R2} = \min(1, 1.00) = 1.00$, $w_{R3} = \min(1, 1.50) = 1.00$. Rejects in bands 2 and 3 now contribute as known bads (the $Y=0$ row carries weight 0), and R1 contributes as a coin flip. The refit PD curve in the upper score region is dragged sharply upward because every reject above band 1 is treated as a guaranteed default. This is the level shift that $\tau$ produces, and it is also why $\tau > 1$ without a bureau anchor is the hand-tuned guess that the simulation in @sec-ch10-parceling-worked-example flags as an over-correction.

### What parceling estimates

When $\tau \equiv 1$, @eq-fuzzy-augmentation is a pseudo-likelihood that treats the rejected applicants as contributing the expected log-likelihood under the accepted PD curve. The fitted $\beta$ is the maximizer of

$$

\mathbb{E}_{(X, S)} \Big[ \mathbb{E}_{Y \mid X, S=1} \log P(Y \mid X; \beta) \Big],

$$ {#eq-fuzzy-target}

which is the weighted average of the accepted-conditional log-likelihood over the full marginal of $X$. When selection is MAR (that is, $P(Y \mid X, S=1) = P(Y \mid X)$) this coincides with the through-the-door target. When selection is MNAR, @eq-fuzzy-target is biased in exactly the way a naive fit would be, because the conditional PD the augmentation uses is itself biased. Fuzzy augmentation cannot out-run the MAR assumption it is built on; it can only match the marginal of $X$.

This is why the method is most defensible when the lender's acceptance rule is largely a function of observed features with little residual variation from unobservables. A rule-based approve-all-above-score scorecard is closer to this regime than a relationship-manager judgmental decision.

To make the regime concrete, the question to ask of any portfolio is: "if I exactly reproduced the recorded features for a rejected applicant, would the system have produced the same accept-or-reject answer?" Where the answer is yes (or close to yes) the unobserved $V$ is small relative to the observed selection score, $\rho$ is mechanically near zero, and fuzzy augmentation with $\tau \approx 1$ is a defensible MAR estimator. Where the answer is no, $V$ is doing the work and the impossibility result of @sec-ch10-impossibility takes over.

In Vietnam, the regime split is unusually clean because the same lender often runs both kinds of book. Three families where the MAR-within-band assumption is approximately defensible:

1. **Mass-market consumer finance.** The unsecured cash-loan and credit-card books at FE Credit, Home Credit Vietnam, MCredit, Mirae Asset Finance, and Shinhan Finance run on automated underwriting against a bureau pull from CIC plus a thin alternative-data layer (telco tenure, e-wallet history, GPS-stable address). Decisions take minutes, with a hard score cut and a small set of policy rules ("CIC nhóm $\geq 3$ in last 24 months $\to$ decline"). Loan officers see only a green/yellow/red flag. Reject inference here is a candidate for fuzzy augmentation with $\tau$ in the lower industry range, because the recorded features carry most of the decision and the residual $V$ is small.

2. **POS and BNPL installment lending.** Home Credit point-of-sale loans at electronics retailers, FPT Shop and Pico co-branded credit, Shopee SPayLater, and the MoMo / ZaloPay BNPL stacks all run pure rule engines against a bureau-light feature vector (phone tenure, prior wallet balance, basic KYC). The merchant cashier sees an accept/decline only and cannot override. The acceptance rule is essentially a deterministic function of the observed inputs.

3. **Auto and motorbike finance with hard LTV/DTI rules.** Toyota Financial Services Vietnam, Honda VietFinance, VPBank Auto, and Techcombank's vehicle loan book gate decisions on loan-to-value, debt-to-income, and bureau bands. Sales staff cannot relax these gates without escalation, and escalations are rare on the mass-affluent segment.

Three families where the assumption breaks and parceling should not be the headline method:

1. **SME and corporate lending at relationship banks.** Vietcombank, BIDV, Agribank, and VietinBank route SME files through a relationship manager who weighs unrecorded soft signals (factory walkthrough, supplier-letter quality, owner's family standing, Tet-season inventory turn). The recorded features capture a fraction of the decision and $\rho$ is large in absolute value.

2. **Microfinance and group-lending books.** TYM and CEP underwrite via village-level group sponsorship and commune-officer references. The accept decision is almost entirely a function of unrecorded social-collateral variables. Fuzzy augmentation on this book would borrow accepted bad rates that reflect a heavily pre-screened sub-population and project them onto a rejected pool dominated by group-rejected applicants whose risk profile is structurally different.

3. **Mortgage and high-ticket secured lending with manual valuation.** Property valuation, source-of-funds review, and committee approval at Techcombank, VPBank, and Sacombank introduce judgmental layers that the application-time feature vector does not encode. Even with a strong observable scorecard, the binding constraint at the margin is often the valuation negotiation, which is a rich source of unobservables.

Even within a single institution the regime can flip across products. A Techcombank cash card on Techcombank Mobile can be a clean rule-based decision while a Techcombank business overdraft to the same customer at the same branch is a relationship-manager call. The right operating discipline is to gate fuzzy augmentation per-product, not per-institution, and to record at decision time which path the file took (`auto`, `auto with override`, `manual review`, `committee`); the override and manual-review tags are then used as conditioning variables in a Heckman-style or copula-based extension when the product mix is mixed.

### A worked numeric example {#sec-ch10-parceling-worked-example}

We trace each step of @eq-fuzzy-augmentation on a deliberately small simulation so the reader can watch every quantity move. The logic is identical to the production-grade run in @sec-ch10-implementation-from-scratch; the only change is that we shrink the sample to 2000 applicants with a single feature so the band table fits on a page. Imports and seed are local to this code chunk so it can be read in isolation from the larger end-to-end script.

```{python}

import numpy as np

import pandas as pd

from sklearn.linear_model import LogisticRegression

from scipy.stats import norm, logistic

rng = np.random.default_rng(2026)

n = 2000

x = rng.standard_normal(n)

z = rng.standard_normal(n)

rho = 0.4

u_n = rng.standard_normal(n)

v = rho * u_n + np.sqrt(1 - rho**2) * rng.standard_normal(n)

u = logistic.ppf(norm.cdf(u_n)) # standard logistic, copula-coupled to v

beta_true = (-0.6, 1.2)

y_lin = beta_true[0] + beta_true[1] * x + u

y = (y_lin > 0).astype(int) # equivalently: y ~ Bernoulli(sigma(beta0 + beta1 x))

gamma_true = (0.3, -1.0, 0.9)

s_star = gamma_true[0] + gamma_true[1] * x + gamma_true[2] * z + v

s = (s_star > 0).astype(int)

print(f"through-the-door default rate : {y.mean():.3f}")

print(f"accept rate : {s.mean():.3f}")

print(f"accepted bad rate : {y[s==1].mean():.3f}")

print(f"rejected bad rate (oracle) : {y[s==0].mean():.3f}")

```

The data-generating process is logistic by construction so that the population coefficients $(\beta_0, \beta_1) = (-0.6, 1.2)$ are directly comparable to a logistic-regression fit. The unobserved outcome shock $u$ is standard logistic, drawn through a Gaussian copula on a normal pair $(u_n, v)$ with $\mathrm{Corr}(u_n, v) = \rho = 0.4$; this preserves the MNAR mechanism (rank dependence between the outcome and selection shocks) while making the marginal default model exactly $P(Y=1 \mid X) = \sigma(\beta_0 + \beta_1 x)$. The accepted bad rate (around 0.35) sits below the through-the-door rate (around 0.39), and the rejected slice (around 0.44) is roughly 8 percentage points riskier than the accepted slice. That gap is the reject-inference target.

::: {.callout-note appearance="simple" icon="false"}

**Two reference rows: truth versus oracle.** Every comparison table in this chapter prints two reference rows alongside the candidate estimators. They are not the same object and the distinction matters.

- **truth (**$\beta^{\star}$). The population DGP coefficient vector $(\beta_0, \beta_1) = (-0.6, 1.2)$. This is what the lender would recover with an infinite labeled sample drawn from the through-the-door distribution. It is a fixed parameter, not an estimator. No method in the chapter targets the truth directly; methods target the oracle, which targets the truth.

- **oracle (**$\hat\beta_{\text{full}}$). The maximum-likelihood logistic fit on the full $n = 2{,}000$ through-the-door labels $(X, Y)$, observable only because this is a simulation. It is a finite-sample estimator that is consistent for $\beta^{\star}$ when the model class matches the DGP. Its gap from truth is finite-sample sampling noise plus sklearn's default L2 ridge ($C = 1.0$); on this seed the slope sits at about 1.28 versus a truth of 1.20.

The reject-inference target is the oracle, not the truth. A method that lands on oracle has solved the selection problem; the residual oracle-versus-truth gap is the same Monte Carlo noise the oracle itself carries. When you read a row like `naive (acc only)` against the two reference rows, the comparison that scores the method is `naive` versus `oracle`. The `truth` row is there to confirm that the oracle is itself unbiased on this DGP.[^10-reject-inference-1]

:::

[^10-reject-inference-1]: An earlier draft of this chapter used a probit-style threshold DGP with a normal $u$, which is why a previous render showed the oracle row drifted from the truth row by the logit-versus-probit scale factor of $\pi/\sqrt 3 \approx 1.81$ (truth slope 1.2, oracle slope around 2.09). The bias story for naive, fuzzy, and bureau is identical under either link; only the numerical alignment of the oracle row against the truth row changes.

**Step 1: fit a PD model on accepteds only.**

```{python}