---

execute:

echo: true

eval: true

bibliography: [../references.bib, ../refs/ch-06.bib]

---

# Discriminant Analysis and the Altman Z-Score {#sec-ch06}

::: {.callout-note appearance="simple" icon="false"}

**Scope: corporate.** Altman MDA, Z'/Z'', Ohlson, Shumway, and Campbell-Hilscher-Szilagyi on the UCI 572 Taiwanese Bankruptcy panel. Consumer applicability is discussed only in @sec-ch06-limitations.

:::

## Overview {.unnumbered}

Linear discriminant analysis was the first statistical tool a bank analyst could hand to a credit committee with a coefficient table and a decision rule. It still is, in many corporate risk groups, because regulators, auditors, and working capital officers can read it. @altman1968zscore turned Fisher's 1936 idea into a working bankruptcy filter by fitting a five-ratio discriminant function on a matched sample of 66 manufacturers. More than five decades later, the Z-score survives as a monitoring metric, a covenant trigger, and a classroom staple. The method is no longer state of the art for out-of-sample accuracy, but it is a lower bound on interpretability and a useful calibration against fancier models.

This chapter rebuilds that machinery end to end. The formal part derives Fisher's criterion from the between-to-within variance ratio, proves its equivalence to the Bayes rule under Gaussian equal-covariance class-conditionals, and extends to quadratic discriminant analysis (@sec-ch06-qda) when covariances differ. The empirical part replays the Altman MDA on the @liang2016financial Taiwanese Bankruptcy Prediction panel (UCI 572: 6,819 firm-years, 220 bankruptcies), then steps through the Z', Z'', and ZETA extensions. The benchmark part puts LDA head to head with logistic regression, Ohlson's logit, Shumway's hazard model, and the Campbell-Hilscher-Szilagyi distance measure (@sec-ch06-chs), and documents where LDA still wins and where it loses badly.

A pragmatic warning first. LDA on raw consumer-credit features, with their mixture of one-hot dummies and skewed amounts, is almost always dominated by a penalized logit or a gradient-boosted tree on the same design matrix. The reason is not that LDA is wrong in principle. It is that its generative Gaussian assumption is wrong in that particular setting. Where features really are close to jointly Gaussian, LDA remains statistically efficient [@efron1975efficiency]. The chapter gives the conditions and shows them in code.

An emerging-market framing sits underneath the whole chapter. In Vietnam and peer economies, corporate books are dominated by thin-file private SMEs whose audited financials arrive late, if at all. Household lending is pulled around by the Tet holiday liquidity cycle, informal-income cash flows, and macro volatility. An LDA or Z''-style model is often the only thing a credit committee in Ho Chi Minh City or Hanoi will approve for middle-market corporate scoring, because the coefficient table is auditable and the sample sizes do not support heavier machinery. The emerging-market section at the end of the chapter returns to this with the CIC bureau, SBV Circular 11/2021, and practical notes on fitting Z'' to Vietnamese manufacturers.

### Notation {.unnumbered}

Let $X \in \mathbb{R}^p$ be the feature vector and $Y \in \{0, 1\}$ the default indicator, with 1 coding default. Write $\pi_k = \Pr(Y = k)$, $\mu_k = \mathbb{E}[X \mid Y = k]$, and $\Sigma_k = \operatorname{Var}(X \mid Y = k)$. When the common-covariance assumption holds, $\Sigma_0 = \Sigma_1 = \Sigma$. Sample estimates are hatted. The within-class scatter is $S_W$ and the between-class scatter is $S_B$. $\Phi$ is the standard normal CDF. For firm-level work, $X_1, \dots, X_5$ name the Altman ratios in the order he wrote them.

## Motivation {.unnumbered}

Banks run two kinds of default models at a minimum: one for corporates and large SMEs, scored on financial statements, and one for consumer accounts, scored on application plus bureau data. @beaver1966financial showed that individual accounting ratios discriminate between bankrupt and healthy firms one to five years out, but he scored one ratio at a time. The weakness is obvious: ratios are correlated, the information is redundant, and a single-ratio cutoff throws away the multivariate signal.

@altman1968zscore fixed this with Fisher's multiple discriminant analysis (MDA). He picked five ratios out of an initial list of 22, fit a linear discriminant on a paired sample of 33 bankrupt and 33 non-bankrupt manufacturers over 1946 to 1965, and published a scoring function that bank analysts could compute by hand. The published function, his decision zones, and his out-of-sample hit rate (95 percent on the original sample, about 80 percent at two-year horizons on holdout) made the Z-score the reference point every later bankruptcy model had to beat.

Three things changed after 1980. @ohlson1980financial showed that a logit on nine variables beat the Z-score on a bigger sample, because binary outcomes with mixed-type predictors fit the logit log-likelihood better than the Gaussian likelihood behind LDA. @shumway2001forecasting reframed bankruptcy as a time-to-event process and built a multi-period hazard model, which avoids the selection bias baked into static matched samples. The derivation, pooled-logit equivalence, and its place in the lineage appear in @sec-ch06-empirical of this chapter; the full implementation (long-table construction, time-varying covariates, term-structure recovery, and the current state of the art) is developed in @sec-ch09-shumway, with the connection to distance-to-default covered in @sec-ch08-empirical. @campbell2008search combined accounting and market-based inputs, including volatility and equity returns, and improved out-of-sample ranking further. The sequence from Altman through Campbell is a textbook instance of the same phenomenon, climbing a ladder of statistical sophistication, while the underlying economics stay close to "leverage, profitability, liquidity, size."

This chapter keeps the whole ladder in one place. @sec-ch06 derives LDA from scratch. @sec-ch06-altman reconstructs Altman's Z. Sections [-@sec-ch06-extensions] and [-@sec-ch06-empirical] step through its extensions and its empirical competitors. @sec-ch06-limitations returns to the original question: when does the linear-Gaussian generative model win against the discriminative logit?

## Formal setup {.unnumbered}

A credit classifier produces a score $s(x) \in \mathbb{R}$ for each applicant vector $x \in \mathbb{R}^p$. A decision rule declares default when $s(x) > t$ for some threshold $t$. Quality of the score is measured by a ranking metric (AUC, KS) and by calibration to the observed default rate in bins.

Three ingredients separate LDA from its alternatives.

1. **A generative assumption on the class-conditional distribution**. LDA posits $X \mid Y = k \sim \mathcal{N}(\mu_k, \Sigma)$ with shared covariance. QDA relaxes to $\Sigma_k$. Naive Bayes factors the density across features. Logistic regression makes no density assumption at all and models $\Pr(Y \mid X)$ directly.

2. **An estimation procedure**. LDA uses the sample class means and pooled covariance, which are the maximum-likelihood estimators under the Gaussian assumption. Logit uses maximum-likelihood estimation of the conditional density. Both converge at the standard parametric rate $n^{-1/2}$ to their respective targets.

3. **A decision function**. LDA's is $\hat\Sigma^{-1}(\hat\mu_1 - \hat\mu_0)$. Logit's is the MLE of the log-odds coefficient. When the LDA assumptions hold, both targets coincide and the question is efficiency. When they fail, LDA's estimand is no longer the Bayes rule and logit wins by consistency.

The chapter walks through these three ingredients in order, first for the two-class case that matches corporate bankruptcy, then for the multi-class case that matches rating-grade assignment, then back to binary with the full credit-scoring machinery around it.

## Linear discriminant analysis {#sec-ch06-discriminant}

### Fisher's criterion

@fisher1936use asked for a linear projection $w^\top X$ of the feature vector that separates the two classes as well as possible. Measure separation by the ratio of between-class to within-class variance along the projected axis. If $\mu_0, \mu_1 \in \mathbb{R}^p$ are the class means and $\Sigma_0, \Sigma_1$ are the class covariances, the projected between-class squared distance is $\left(w^\top(\mu_1 - \mu_0)\right)^2$, and the projected within-class variance is $w^\top(\Sigma_0 + \Sigma_1) w$ up to class weights. Fisher's criterion is

$$

J(w) = \frac{\bigl(w^\top(\mu_1 - \mu_0)\bigr)^2}{w^\top \Sigma_W w} = \frac{w^\top S_B w}{w^\top S_W w},

$$ {#eq-fisher-ratio}

where $S_B = (\mu_1 - \mu_0)(\mu_1 - \mu_0)^\top$ is the rank-one between-class scatter and $S_W = \pi_0 \Sigma_0 + \pi_1 \Sigma_1$ is the within-class scatter. The objective is scale-invariant in $w$, so fix $w^\top S_W w = 1$. The Lagrangian is

$$

\mathcal{L}(w, \lambda) = w^\top S_B w - \lambda\bigl(w^\top S_W w - 1\bigr).

$$ {#eq-fisher-lagrangian}

Stationarity $\partial\mathcal{L}/\partial w = 0$ gives the generalized eigenvalue problem

$$

S_B w = \lambda S_W w.

$$ {#eq-fisher-gep}

When $S_W$ is positive definite, left-multiply by $S_W^{-1}$ to get the standard eigenvalue problem $S_W^{-1} S_B w = \lambda w$. Because $S_B$ has rank 1 in the two-class case, there is exactly one non-zero eigenvalue, and the corresponding eigenvector is proportional to $S_W^{-1}(\mu_1 - \mu_0)$. The maximum value of the criterion equals that eigenvalue and is the squared Mahalanobis distance between the class means [@mahalanobis1936generalized]:

$$

\max_{w \ne 0} J(w) = (\mu_1 - \mu_0)^\top \Sigma^{-1} (\mu_1 - \mu_0) = \Delta^2.

$$ {#eq-mahalanobis}

In the $K > 2$ class case, $S_B$ has rank up to $K - 1$, and the discriminant projection has $K - 1$ directions. This is the "multiple" in MDA [@rao1948utilization].

The geometric content deserves a second pass. Write the within-class scatter as a symmetric positive-definite matrix and factor it as $S_W = L L^\top$ via Cholesky. Substitute $u = L^\top w$. The criterion becomes

$$

J(w) = \frac{u^\top (L^{-1} S_B L^{-\top}) u}{u^\top u}.

$$ {#eq-fisher-whitened}

The Lagrangian now has the structure of an ordinary Rayleigh quotient. The optimal $u^\star$ is the top eigenvector of the symmetric matrix $L^{-1} S_B L^{-\top}$, and we recover $w^\star = L^{-\top} u^\star$. Equivalently, Fisher's projection is the linear direction that would be maximally separating in a whitened coordinate system where the within-class scatter is isotropic. This is also how @bickel2004some interpret LDA's failure in high dimensions: the whitening step breaks when $L$ is near-singular, and the finite-sample direction diverges from the true Bayes direction even with moderate dimension.

### Equivalence with the decorrelated signal-to-noise direction

Start from a different angle. Suppose $X \mid Y = k \sim \mathcal{N}(\mu_k, \Sigma)$. Let $Z = \Sigma^{-1/2}(X - \bar\mu)$ where $\bar\mu = (\mu_0 + \mu_1)/2$. Under the change of variables, $Z \mid Y = k \sim \mathcal{N}\bigl(\tfrac{1}{2}(-1)^{1-k} \Sigma^{-1/2}(\mu_1-\mu_0), I\bigr)$. The two class distributions are now unit-covariance Gaussians symmetric about the origin, separated along the direction $d = \Sigma^{-1/2}(\mu_1 - \mu_0)$. The Bayes rule reduces to thresholding the projection $d^\top Z$, and in the original coordinate system that projection is $(\Sigma^{-1/2})^\top d \cdot (X - \bar\mu) = \Sigma^{-1}(\mu_1-\mu_0) \cdot (X - \bar\mu)$. Same answer, different derivation, same coefficient $\beta = \Sigma^{-1}(\mu_1 - \mu_0)$.

The Mahalanobis distance @eq-mahalanobis controls the discriminability. When $\Delta$ is small, no linear rule separates well; any competing non-linear rule that does better must be exploiting non-Gaussian, not geometry. When $\Delta$ is large, almost any sensible rule works, and the optimization details stop mattering. @anderson1951classification formalized this and gave the asymptotic error rate for Fisher's rule as $\Phi(-\Delta/2)$ when the priors are equal, which is the quantity most later empirical papers use as a benchmark.

### Sample-size corrections and plug-in bias

In practice, $\Sigma$ is unknown and we plug in a sample estimate. The unbiased within-class covariance is

$$

\hat\Sigma = \frac{1}{n-2}\left[\sum_{i: y_i=0} (x_i - \hat\mu_0)(x_i - \hat\mu_0)^\top

+ \sum_{i: y_i=1} (x_i - \hat\mu_1)(x_i - \hat\mu_1)^\top\right].

$$ {#eq-pooled-cov}

Plugging $\hat\Sigma$ and $\hat\mu_k$ into the Bayes rule produces a linear classifier whose error exceeds the Bayes error by an $O(p/n)$ term [@anderson1951classification]. @bickel2004some show that as $p/n \to \gamma > 0$, the classifier loses all discriminative power unless $\Sigma$ has structure (sparsity, block-diagonality, a factor model). In the $p \ll n$ regime relevant to Altman's 5-variable model on 66 firms, the plug-in correction is small. In the consumer-credit regime with 50 to 200 dummies on a few thousand applicants, it is not.

A partial fix is regularized discriminant analysis [@friedman1989regularized], which shrinks $\hat\Sigma_k$ toward a pooled covariance and a diagonal target to trade bias against variance. The full derivation, the hyperparameter grid, and a runnable comparison against LDA and QDA appear in @sec-ch06-rda.

### Bayes decision under Gaussian equal-covariance

Now change view. Suppose the class-conditional densities are multivariate Gaussian with a common covariance:

$$

X \mid Y = k \sim \mathcal{N}(\mu_k, \Sigma), \qquad k = 0, 1.

$$ {#eq-gaussian-classes}

The posterior log-odds reduce to a linear discriminant. Write the log-posterior ratio:

$$

\begin{aligned}

\log\frac{\Pr(Y=1\mid X)}{\Pr(Y=0\mid X)}

={}& \log\frac{\pi_1}{\pi_0} - \tfrac12 (X-\mu_1)^\top \Sigma^{-1}(X-\mu_1) \\

& + \tfrac12 (X-\mu_0)^\top \Sigma^{-1}(X-\mu_0).

\end{aligned}

$$ {#eq-posterior-logodds}

The quadratic terms in $X$ cancel under equal covariance, leaving

$$

\begin{aligned}

\log\frac{\Pr(Y=1\mid X)}{\Pr(Y=0\mid X)}

={}& X^\top \Sigma^{-1}(\mu_1-\mu_0) \\

& - \tfrac12(\mu_1+\mu_0)^\top \Sigma^{-1}(\mu_1-\mu_0) + \log\frac{\pi_1}{\pi_0}.

\end{aligned}

$$ {#eq-lda-logit}

The Bayes-optimal classifier thresholds this linear function of $X$. The coefficient vector $\Sigma^{-1}(\mu_1 - \mu_0)$ is exactly the Fisher direction @eq-fisher-gep up to scaling, so the two derivations coincide. The intercept differs only by the prior adjustment $\log(\pi_1/\pi_0)$ and the midpoint term, which Fisher's variance-ratio criterion does not fix because it is scale and location invariant.

Three consequences matter in practice. First, LDA is linear in $X$, so the decision boundary is a hyperplane. Second, its coefficients are interpretable in the same way OLS coefficients are, because they come from inverting a single covariance matrix. Third, the estimated probability

$$

\Pr(Y=1 \mid X) = \sigma\!\left(X^\top \beta + \beta_0\right), \qquad \beta = \Sigma^{-1}(\mu_1 - \mu_0),

$$ {#eq-lda-sigmoid}

is correctly calibrated when the Gaussian assumption holds. When it does not hold, the resulting probabilities are often miscalibrated even if the ranking remains good. This matters for credit scorecards because regulators expect the probability of default, not only its rank.

### Quadratic discriminant analysis {#sec-ch06-qda}

Drop the equal-covariance assumption. Let $X \mid Y = k \sim \mathcal{N}(\mu_k, \Sigma_k)$. The same algebra yields

$$

\log\frac{\Pr(Y=1\mid X)}{\Pr(Y=0\mid X)} = -\tfrac12 X^\top(\Sigma_1^{-1} - \Sigma_0^{-1}) X + X^\top(\Sigma_1^{-1}\mu_1 - \Sigma_0^{-1}\mu_0) + C,

$$ {#eq-qda-logit}

where $C$ collects the scalar intercept with $\log(\pi_1/\pi_0)$, $\log|\Sigma_k|$ terms, and quadratic terms in the class means. The decision surface is now a quadric, not a hyperplane. QDA has $p(p+1)$ parameters in the covariance blocks versus $p(p+1)/2$ for LDA, so it overfits quickly when $p$ grows relative to $n$ [@friedman1989regularized].

For credit work, QDA is the natural upgrade when defaulters show a different covariance structure from survivors. That is common in practice: distressed firms have fatter tails and more correlated deterioration across ratios. Whether QDA actually beats LDA depends on whether you have enough defaulters to estimate $\Sigma_1$ well. When the defaulter sample is too thin to support separate covariances but LDA's equal-covariance constraint is visibly wrong, the regularized path in @sec-ch06-rda is the practical middle ground.

### Regularized discriminant analysis {#sec-ch06-rda}

@friedman1989regularized proposed a two-parameter shrinkage that interpolates between LDA (@sec-ch06-discriminant) and QDA (@sec-ch06-qda) and then shrinks each covariance toward its diagonal:

$$

\hat\Sigma_k(\alpha, \gamma) = (1 - \gamma)\left[(1 - \alpha)\hat\Sigma_k + \alpha \hat\Sigma_{\text{pool}}\right]

+ \gamma \operatorname{diag}\!\left(\hat\Sigma_k\right).

$$ {#eq-rda-shrink}

The two hyperparameters index a rectangle of models. At $\alpha = 1, \gamma = 0$ the pooled covariance recovers LDA. At $\alpha = 0, \gamma = 0$ the class-specific covariances recover QDA. At $\alpha = 1, \gamma = 1$ the pooled diagonal reproduces diagonal LDA, which under Gaussian marginals is Gaussian naive Bayes. The interior of the rectangle covers the intermediate regularization paths.

The first parameter $\alpha$ controls covariance pooling. Pure QDA uses $\hat\Sigma_k$ estimated on the $n_k$ observations of class $k$, which has $p(p+1)/2$ free parameters per class. When the rarer class carries a few dozen observations (the Altman 33 defaulters, a stressed emerging-market corporate book, a tail-event sample), $\hat\Sigma_1$ is noisy and QDA's quadratic decision surface follows the noise. Shrinking toward $\hat\Sigma_{\text{pool}}$ borrows strength from the larger class at the cost of a small bias if the covariances truly differ.

The second parameter $\gamma$ controls diagonal shrinkage. The off-diagonal entries of $\hat\Sigma_k$ are noisier than the diagonal in high dimension [@bickel2004some], and setting $\gamma > 0$ throws away the noisiest entries. The limit $\gamma = 1$ is diagonal LDA, which assumes feature independence within a class; the limit $\gamma = 0$ keeps the full sample covariance.

For small samples with modest $p$, a cross-validated RDA typically outperforms both pure LDA and pure QDA. It is a good default when the modeler is uncertain about the covariance structure, because the optimal $(\alpha, \gamma)$ tells the modeler which assumption was closer to the data without a separate hypothesis test.

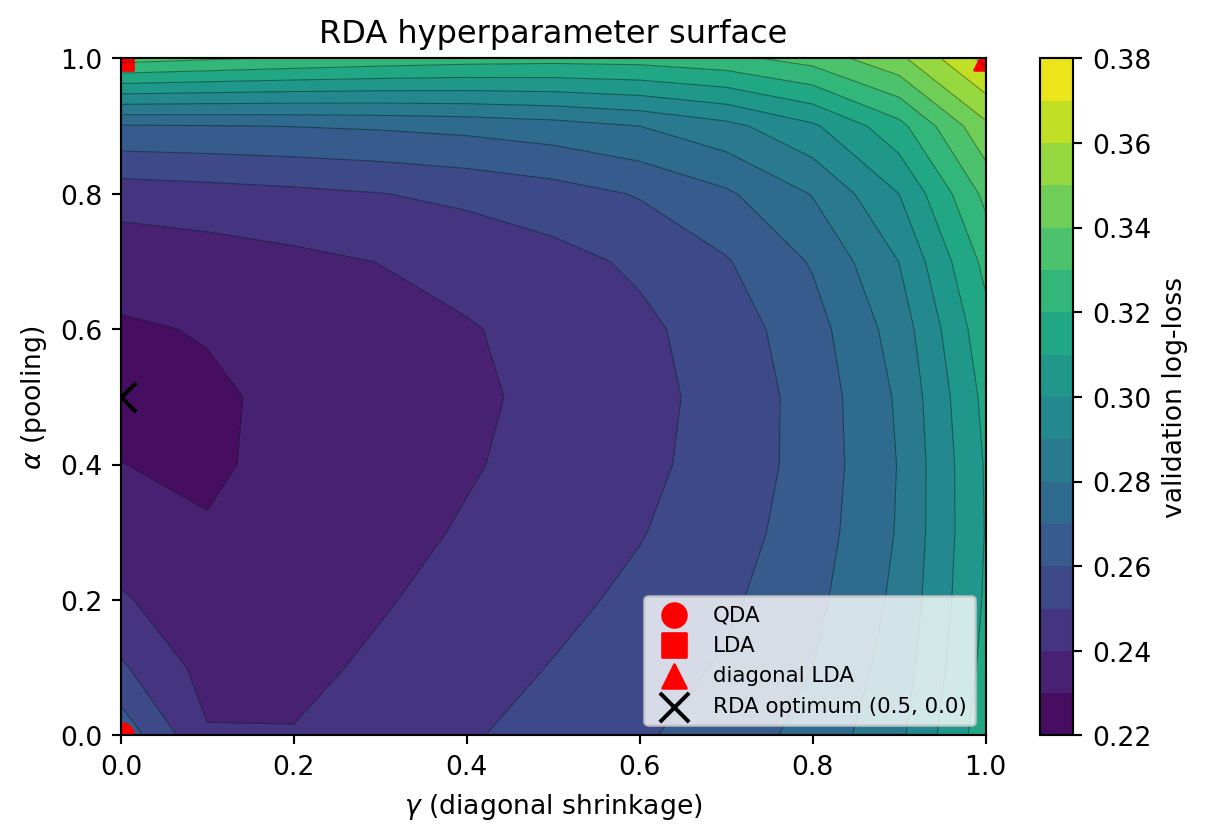

```{python}

#| fig-cap: "Validation log-loss surface for RDA on an eight-feature heteroskedastic sample with a thin minority class (n=60 defaulters, Altman-scale). Red markers locate the pure-LDA, pure-QDA, and diagonal-LDA corners; the black cross marks the cross-validated optimum, which sits in the interior."

import numpy as np

import matplotlib.pyplot as plt

from sklearn.discriminant_analysis import (

LinearDiscriminantAnalysis,

QuadraticDiscriminantAnalysis,

)

from sklearn.metrics import log_loss

def rda_covariances(X, y, alpha, gamma):

classes = np.unique(y)

covs_class, priors, means = {}, {}, {}

Xc_all = []

for c in classes:

Xc = X[y == c]

means[c] = Xc.mean(0)

priors[c] = len(Xc) / len(X)

covs_class[c] = np.cov(Xc, rowvar=False, bias=False)

Xc_all.append(Xc - means[c])

Sigma_pool = np.cov(np.vstack(Xc_all), rowvar=False, bias=False)

reg_covs = {}

for c in classes:

S = (1 - alpha) * covs_class[c] + alpha * Sigma_pool

S = (1 - gamma) * S + gamma * np.diag(np.diag(S))

reg_covs[c] = S

return means, priors, reg_covs

def rda_predict_proba(X_tr, y_tr, X_te, alpha, gamma):

means, priors, covs = rda_covariances(X_tr, y_tr, alpha, gamma)

logs = []

for c in sorted(means):

S = covs[c]

sign, logdet = np.linalg.slogdet(S)

diff = X_te - means[c]

quad = np.einsum("ni,ij,nj->n", diff, np.linalg.inv(S), diff)

logs.append(np.log(priors[c]) - 0.5 * logdet - 0.5 * quad)

logs = np.column_stack(logs)

logs -= logs.max(1, keepdims=True)

P = np.exp(logs)

return P / P.sum(1, keepdims=True)

# Eight financial-ratio features, Altman-scale minority class.

rng_h = np.random.default_rng(3)

p_feat, n0h, n1h = 8, 400, 60

mu0 = np.zeros(p_feat)

mu1 = np.ones(p_feat) * 0.6

Sigma0 = 0.3 * np.ones((p_feat, p_feat)) + 0.7 * np.eye(p_feat)

A_rand = rng_h.standard_normal((p_feat, p_feat))

Sigma1 = A_rand @ A_rand.T / p_feat + 0.5 * np.eye(p_feat)

X0h = rng_h.multivariate_normal(mu0, Sigma0, n0h)

X1h = rng_h.multivariate_normal(mu1, Sigma1, n1h)

Xh_rda = np.vstack([X0h, X1h])

yh_rda = np.hstack([np.zeros(n0h), np.ones(n1h)])

perm = rng_h.permutation(len(yh_rda))

split = int(0.7 * len(yh_rda))

tr, te = perm[:split], perm[split:]

alphas = np.linspace(0.0, 1.0, 11)

gammas = np.linspace(0.0, 1.0, 11)

loss = np.zeros((len(alphas), len(gammas)))

for i, a in enumerate(alphas):

for j, g in enumerate(gammas):

P = rda_predict_proba(Xh_rda[tr], yh_rda[tr], Xh_rda[te], a, g)

loss[i, j] = log_loss(yh_rda[te], P[:, 1], labels=[0, 1])

i_star, j_star = np.unravel_index(np.argmin(loss), loss.shape)

a_star, g_star = alphas[i_star], gammas[j_star]

fig, ax = plt.subplots(figsize=(6.5, 4.5))

cs = ax.contourf(gammas, alphas, loss, levels=15, cmap="viridis")

ax.contour(gammas, alphas, loss, levels=15, colors="k", linewidths=0.4, alpha=0.4)

plt.colorbar(cs, ax=ax, label="validation log-loss")

ax.scatter([0.0], [0.0], color="red", s=80, label="QDA")

ax.scatter([0.0], [1.0], color="red", s=80, marker="s", label="LDA")

ax.scatter([1.0], [1.0], color="red", s=80, marker="^", label="diagonal LDA")

ax.scatter([g_star], [a_star], color="black", s=120, marker="x",

label=f"RDA optimum ({a_star:.1f}, {g_star:.1f})")

ax.set_xlabel(r"$\gamma$ (diagonal shrinkage)")

ax.set_ylabel(r"$\alpha$ (pooling)")

ax.set_title("RDA hyperparameter surface")

ax.legend(loc="lower right", fontsize=8)

fig.tight_layout()

plt.show()

lda_ll = log_loss(yh_rda[te],

LinearDiscriminantAnalysis().fit(Xh_rda[tr], yh_rda[tr])

.predict_proba(Xh_rda[te])[:, 1], labels=[0, 1])

qda_ll = log_loss(yh_rda[te],

QuadraticDiscriminantAnalysis().fit(Xh_rda[tr], yh_rda[tr])

.predict_proba(Xh_rda[te])[:, 1], labels=[0, 1])

print(f"LDA log-loss: {lda_ll:.3f}")

print(f"QDA log-loss: {qda_ll:.3f}")

print(f"RDA log-loss: {loss[i_star, j_star]:.3f} at (alpha, gamma) = ({a_star:.2f}, {g_star:.2f})")

```

RDA finds an interior $(\alpha, \gamma)$ that beats both corners. On a Gaussian-equal-covariance sample, the optimum would collapse to the LDA corner; on a sample with distinct covariances and a small minority class the optimum is typically in the interior. For credit work, this matters most in two settings: corporate distress scoring with a dozen or two defaulters per year, and consumer-credit segments like fraud-adjacent cohorts where the rarer class is both thin and heteroskedastic. Either way the cost is one cross-validation grid over a $11 \times 11$ rectangle, which is negligible next to the downstream calibration and monitoring pipeline.

A caveat: RDA inherits LDA's generative Gaussian assumption. It handles covariance misspecification but not the failure modes documented in @sec-ch06-limitations (heavy categoricals, skewed amounts, rare-event bias). On a mixed-type consumer design matrix, a well-tuned regularized logit remains the better default; RDA is the right tool when the predictors are continuous financial ratios and the sample is too thin for unconstrained QDA.

### From-scratch Fisher LDA

The following block implements LDA from the generalized eigenvalue system @eq-fisher-gep and compares it to `sklearn`. It also verifies the closed-form equivalence $w \propto S_W^{-1}(\mu_1 - \mu_0)$.

```{python}

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import sys

sys.path.insert(0, '../code')

from creditutils import load_german_credit, ks_statistic, train_valid_test_split

np.random.seed(7)

rng = np.random.default_rng(7)

# Two Gaussian classes sharing a covariance.

mu0 = np.array([-1.0, -0.5])

mu1 = np.array([1.2, 0.8])

Sigma = np.array([[1.0, 0.3], [0.3, 1.4]])

L = np.linalg.cholesky(Sigma)

n0, n1 = 400, 400

X0 = mu0 + rng.standard_normal((n0, 2)) @ L.T

X1 = mu1 + rng.standard_normal((n1, 2)) @ L.T

X = np.vstack([X0, X1])

y = np.hstack([np.zeros(n0), np.ones(n1)])

def fisher_lda(X, y):

"""Two-class Fisher LDA via the generalized eigenvalue problem."""

classes = np.unique(y)

mu = {c: X[y == c].mean(0) for c in classes}

Sw = np.zeros((X.shape[1], X.shape[1]))

for c in classes:

Xc = X[y == c] - mu[c]

Sw += Xc.T @ Xc

diff = (mu[1] - mu[0]).reshape(-1, 1)

Sb = diff @ diff.T

# Solve S_W^{-1} S_B w = lambda w.

A = np.linalg.solve(Sw, Sb)

vals, vecs = np.linalg.eig(A)

idx = int(np.argmax(vals.real))

w = vecs[:, idx].real

w = w / np.linalg.norm(w)

# Closed form for the two-class case.

w_closed = np.linalg.solve(Sw, (mu[1] - mu[0]))

w_closed = w_closed / np.linalg.norm(w_closed)

mid = 0.5 * (mu[0] + mu[1])

threshold = float(w_closed @ mid)

return w, w_closed, threshold, Sw, mu

w_eig, w_closed, thr, Sw, mu = fisher_lda(X, y)

print("Eigen direction :", np.round(w_eig, 4))

print("Closed direction:", np.round(w_closed, 4))

print("Cosine alignment:", float(abs(w_eig @ w_closed)))

```

The two directions agree exactly up to sign because the rank-one $S_B$ forces the sole non-trivial eigenvector to lie along $S_W^{-1}(\mu_1 - \mu_0)$. Now verify against `sklearn`:

```{python}

from sklearn.discriminant_analysis import LinearDiscriminantAnalysis

lda = LinearDiscriminantAnalysis(store_covariance=True).fit(X, y)

coef_sklearn = lda.coef_.ravel()

coef_ours = np.linalg.solve(Sw / (len(y) - 2), (mu[1] - mu[0]))

print("sklearn coef :", np.round(coef_sklearn, 4))

print("from-scratch coef:", np.round(coef_ours, 4))

print("ratio (should be const):", np.round(coef_sklearn / coef_ours, 4))

# Same accuracy.

proj = X @ w_closed

yhat_scratch = (proj > thr).astype(int)

print("from-scratch accuracy:", float((yhat_scratch == y).mean()))

print("sklearn accuracy :", float(lda.score(X, y)))

```

Both implementations return the same linear decision rule up to a positive scaling and produce identical predictions on this sample.

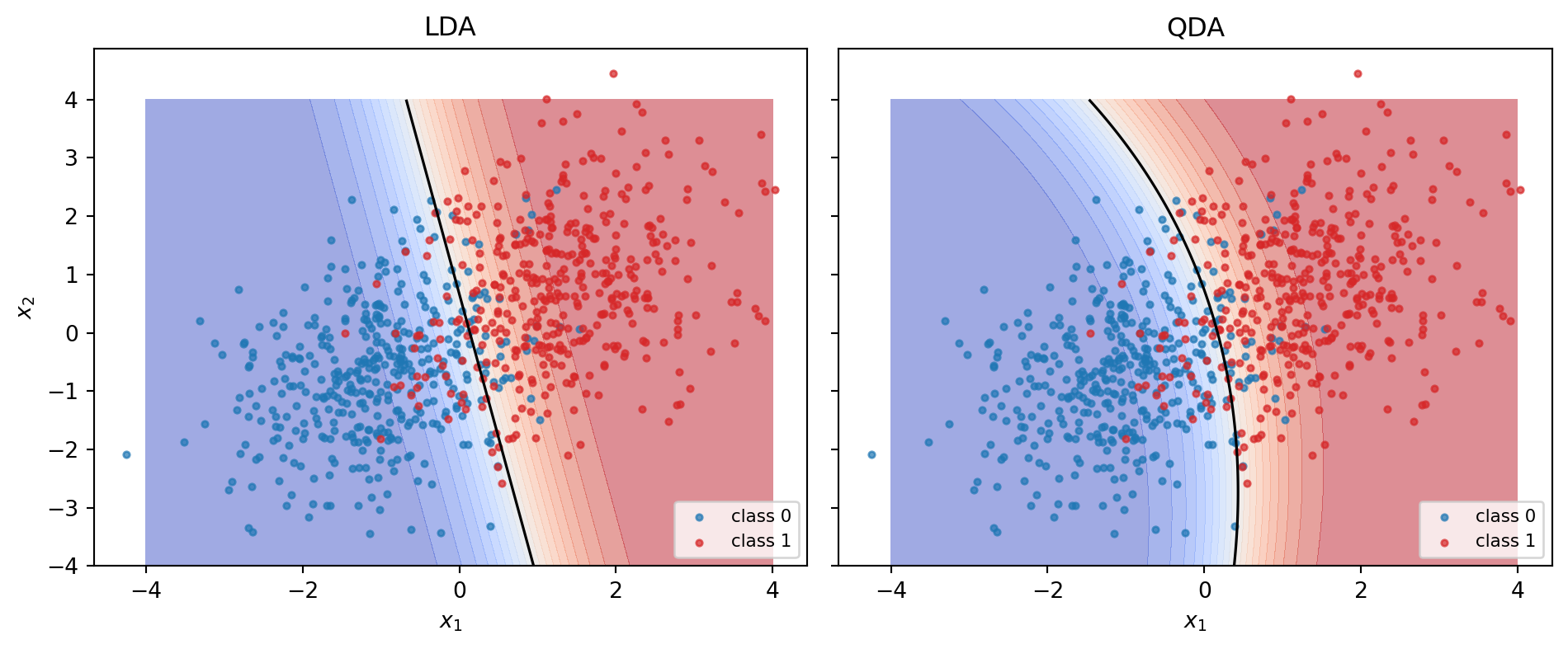

### Decision boundary plot

The LDA boundary is the set where @eq-lda-logit equals zero. For the shared-covariance case it is a straight line. QDA (@sec-ch06-qda) adds the quadratic terms in @eq-qda-logit, producing a conic boundary.

```{python}

#| fig-cap: "Decision boundaries for LDA and QDA on the shared-covariance sample. LDA recovers the Bayes linear rule; QDA adds a spurious curvature because it overfits the sample covariance."

from sklearn.discriminant_analysis import QuadraticDiscriminantAnalysis

xx, yy = np.meshgrid(np.linspace(-4, 4, 300), np.linspace(-4, 4, 300))

grid = np.c_[xx.ravel(), yy.ravel()]

fig, axes = plt.subplots(1, 2, figsize=(10, 4.2), sharey=True)

for ax, model, name in [(axes[0], lda, "LDA"),

(axes[1], QuadraticDiscriminantAnalysis().fit(X, y), "QDA")]:

Z = model.predict_proba(grid)[:, 1].reshape(xx.shape)

ax.contourf(xx, yy, Z, levels=20, cmap="coolwarm", alpha=0.5)

ax.contour(xx, yy, Z, levels=[0.5], colors="k", linewidths=1.2)

ax.scatter(X0[:, 0], X0[:, 1], s=8, color="#1f77b4", alpha=0.7, label="class 0")

ax.scatter(X1[:, 0], X1[:, 1], s=8, color="#d62728", alpha=0.7, label="class 1")

ax.set_title(name)

ax.set_xlabel("$x_1$")

ax.legend(loc="lower right", fontsize=8)

axes[0].set_ylabel("$x_2$")

plt.tight_layout()

plt.show()

```

### QDA on heteroskedastic data

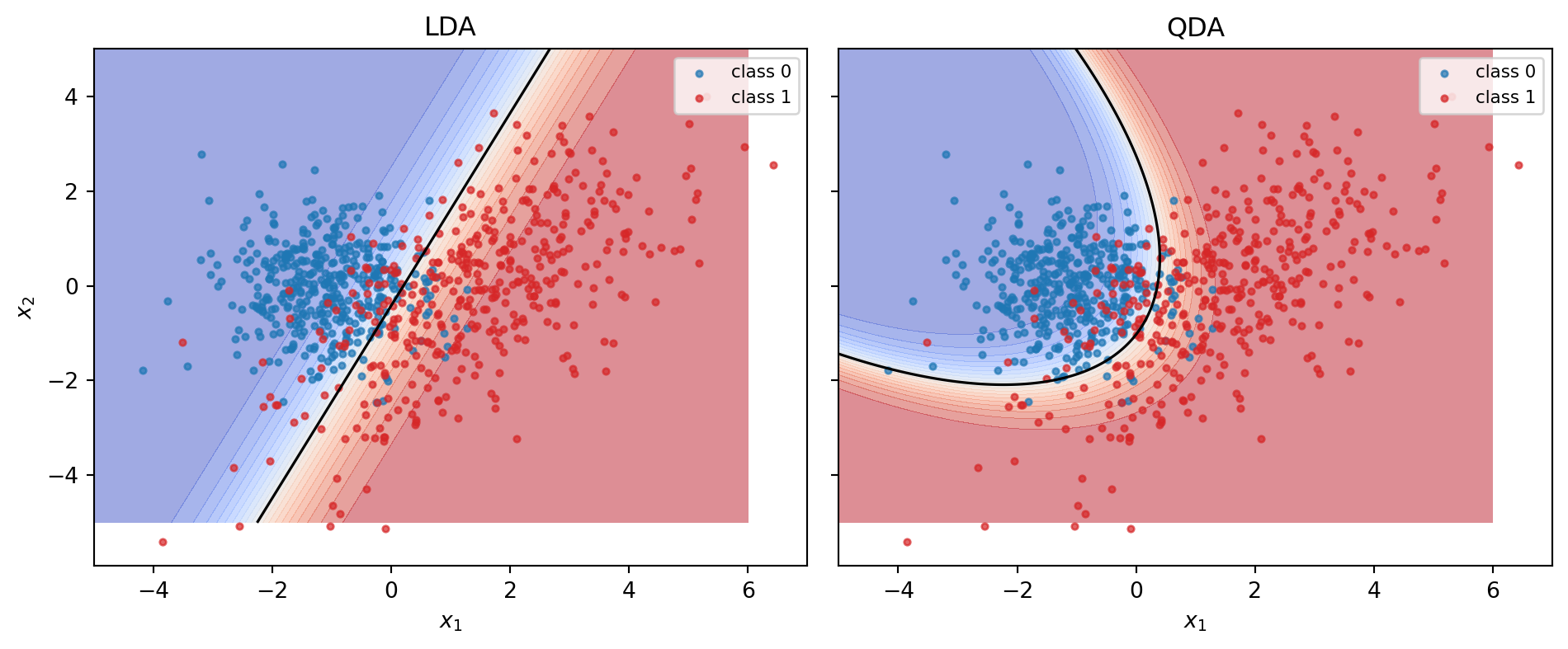

When the two classes have different covariance structures the LDA hyperplane systematically cuts into one of them. Simulate a sample where class 1 has a rotated and stretched covariance relative to class 0.

```{python}

#| fig-cap: "LDA versus QDA on heteroskedastic classes. The LDA line is a lower-dimensional projection of a problem whose Bayes boundary is a quadric."

rng = np.random.default_rng(1)

mu0h = np.array([-1.0, 0.0])

mu1h = np.array([1.5, 0.0])

Sigma0 = np.array([[0.8, 0.0], [0.0, 0.8]])

Sigma1 = np.array([[2.5, 1.6], [1.6, 2.5]])

X0h = rng.multivariate_normal(mu0h, Sigma0, size=400)

X1h = rng.multivariate_normal(mu1h, Sigma1, size=400)

Xh = np.vstack([X0h, X1h])

yh = np.hstack([np.zeros(400), np.ones(400)])

lda_h = LinearDiscriminantAnalysis().fit(Xh, yh)

qda_h = QuadraticDiscriminantAnalysis().fit(Xh, yh)

print(f"LDA accuracy: {lda_h.score(Xh, yh):.3f}")

print(f"QDA accuracy: {qda_h.score(Xh, yh):.3f}")

xx, yy = np.meshgrid(np.linspace(-5, 6, 300), np.linspace(-5, 5, 300))

grid = np.c_[xx.ravel(), yy.ravel()]

fig, axes = plt.subplots(1, 2, figsize=(10, 4.2), sharey=True)

for ax, model, name in [(axes[0], lda_h, "LDA"), (axes[1], qda_h, "QDA")]:

Z = model.predict_proba(grid)[:, 1].reshape(xx.shape)

ax.contourf(xx, yy, Z, levels=20, cmap="coolwarm", alpha=0.5)

ax.contour(xx, yy, Z, levels=[0.5], colors="k", linewidths=1.2)

ax.scatter(X0h[:, 0], X0h[:, 1], s=8, color="#1f77b4", alpha=0.7, label="class 0")

ax.scatter(X1h[:, 0], X1h[:, 1], s=8, color="#d62728", alpha=0.7, label="class 1")

ax.set_title(name)

ax.set_xlabel("$x_1$")

ax.legend(loc="upper right", fontsize=8)

axes[0].set_ylabel("$x_2$")

plt.tight_layout()

plt.show()

```

QDA beats LDA by several percentage points on this specific simulation because the Bayes boundary is genuinely quadratic. The cost is fragility: QDA's covariance in class 1 has nine parameters in a two-dimensional problem, so extending this to $p = 20$ ratios on a $n_1 = 33$ defaulter sample, the setting Altman was in, is a recipe for overfitting. That is one reason he stuck to LDA.

### Statistical efficiency of LDA versus the logit

@efron1975efficiency studied the asymptotic relative efficiency of LDA and logistic regression under Gaussian class-conditionals. When the Gaussian model holds, LDA is more efficient than logit by up to about 40 percent at extreme class separations. When the Gaussian model fails, logit is consistent for the log-odds while LDA is not, so the ordering flips. @press1978choosing made the same observation on binary-heavy data and recommended logit for application scoring. The folklore that "logistic regression almost always beats LDA on real credit data" traces to this efficiency argument. It is about model misspecification, not about LDA being a bad estimator under its own assumptions.

The efficiency result is worth unpacking, because it contradicts a common intuition. Both LDA and logit are consistent for the same linear Bayes rule when the Gaussian model holds, so an asymptotic comparison is between two unbiased estimators of the same coefficient vector, and the question becomes whose sampling variance is smaller. LDA exploits the additional information that the class-conditional distributions are Gaussian, giving it access to the covariance matrix estimated on all $n$ observations rather than only the information captured by the gradient of the log-likelihood at $\beta$. Logit ignores the full covariance and extracts only the first-order information at the decision boundary. Under Gaussian, LDA's information is strictly richer, which is where the efficiency gain comes from. Under misspecification, the information LDA uses is wrong, and the extra signal becomes a biased signal.

A useful diagnostic is the Henze-Zirkler test or the Mardia skew and kurtosis tests for multivariate normality on each class. If the class-conditional density is heavily non-Gaussian, the efficiency argument no longer applies and a discriminative model like logit is the safer default. In corporate bankruptcy work, financial ratios after a log-plus-Winsorize transformation are typically close enough to Gaussian that LDA's efficiency is a real bonus. In consumer credit work, the mix of dummies makes the Gaussian assumption a fantasy.

### Multiclass discriminant analysis

Bankruptcy is the binary case. A rating agency or a banking supervisor usually wants a multi-class classifier that assigns firms to one of several rating grades. For $K$ classes, Fisher's criterion generalizes to

$$

J(W) = \operatorname{tr}\!\left[(W^\top S_W W)^{-1} (W^\top S_B W)\right], \qquad W \in \mathbb{R}^{p \times (K-1)},

$$ {#eq-mda-trace}

with $S_B = \sum_{k=1}^K n_k (\hat\mu_k - \hat\mu)(\hat\mu_k - \hat\mu)^\top$ the between-class scatter, $S_W = \sum_{k=1}^K \sum_{i: y_i = k}(x_i - \hat\mu_k)(x_i - \hat\mu_k)^\top$ the within-class scatter, and $\hat\mu$ the overall sample mean. The optimal $W^\star$ collects the top $K - 1$ generalized eigenvectors of $S_B w = \lambda S_W w$. For $K = 2$ this reduces to @eq-fisher-gep, with $W^\star$ a single vector.

Under Gaussian class-conditionals with shared covariance $\Sigma$, the multi-class Bayes classifier assigns $x$ to the class $k^\star$ that maximizes the linear discriminant function

$$

\delta_k(x) = x^\top \Sigma^{-1} \mu_k - \tfrac{1}{2}\mu_k^\top \Sigma^{-1} \mu_k + \log \pi_k.

$$ {#eq-lda-multiclass}

Ratings-grade applications typically have $K$ between 7 and 22. In that range the $K - 1$ MDA directions often capture only a few axes of genuine variation: one for leverage-profitability, one for size-liquidity. Higher MDA components add noise. A useful diagnostic is a scree plot of the eigenvalues from the generalized system, keeping only those above the Marchenko-Pastur cutoff for pure noise.

### The connection with linear regression

Fisher's paper [@fisher1936use] observed that the LDA coefficients for a two-class problem can be obtained as the OLS slope of an indicator variable regressed on $X$, up to a positive constant. The constant is computable and depends on the class priors and the within-class variance. The upshot is that a practitioner with only a linear regression implementation can still compute an LDA direction. Write $y_i \in \{-1, +1\}$ or $\{0, 1\}$, run OLS of $y$ on $X$, and interpret the coefficient vector as proportional to $\Sigma^{-1}(\mu_1 - \mu_0)$. This is not a recommended implementation for numerical reasons (LDA's own linear algebra is more stable), but the identity is useful in proofs and occasionally in debugging a mismatch between two library implementations.

## The Altman Z-score {#sec-ch06-altman}

### Construction

Altman's 1968 sample was 66 manufacturing firms, 33 that had filed Chapter X or XI bankruptcy between 1946 and 1965 and 33 matched survivors of similar size and industry. He started from 22 financial ratios in five categories (liquidity, profitability, leverage, solvency, activity), ran MDA with stepwise selection, and converged on five ratios that collectively maximized the multivariate separation. The published equation is

$$

Z = 1.2 X_1 + 1.4 X_2 + 3.3 X_3 + 0.6 X_4 + 1.0 X_5,

$$ {#eq-altman-z}

with ratios defined as

| Ratio | Definition | Story |

|--------------------|--------------------------------|--------------------|

| $X_1$ | Working capital / Total assets | Short-term liquidity buffer. |

| $X_2$ | Retained earnings / Total assets | Cumulative profitability and age. |

| $X_3$ | EBIT / Total assets | Operating efficiency, independent of leverage and tax. |

| $X_4$ | Market value of equity / Book value of total liabilities | Market-implied solvency cushion. |

| $X_5$ | Sales / Total assets | Asset turnover. |

The original paper expresses $X_1$ through $X_4$ as percentages (so the 1.2 coefficient multiplies a raw decimal of 0.10 as 1.2 multiplied by 10 percent). Altman's later monographs reformulated the equation so that the ratios are entered as decimals and the coefficients become 0.012, 0.014, 0.033, 0.006, 0.999, which is algebraically the same model. The version in @eq-altman-z uses the percentage convention, which is how it appears in most textbooks.

### Why five ratios and not more

A modern analyst faced with the same problem today would reach for a regularized logit or an XGBoost model with several hundred candidate features, not a hand-selected five. Altman's constraint was different. He had 66 observations and a desk analyst as the intended consumer. Five ratios was the natural upper bound on what the analyst could compute from a paper balance sheet and what MDA could fit without overfitting.

The information content of the five ratios also reflects five distinct mechanisms of corporate distress.

- Liquidity ($X_1$) captures the short-term survival buffer. A firm with deeply negative working capital cannot pay suppliers next month and is forced to restructure or file for protection.

- Cumulative profitability ($X_2$) captures firm age and past performance. Retained earnings over assets is low for young firms and for firms that have been paying out everything they earn. Both subgroups default at higher rates.

- Operating efficiency ($X_3$) captures the core economic engine. EBIT is independent of leverage and tax and measures how well the operating assets generate cash, which is the most fundamental driver of long-run survival.

- Market solvency ($X_4$) captures the market's forward-looking assessment. Equity value over debt is the option-theoretic buffer in Merton's sense.

- Asset turnover ($X_5$) captures managerial efficiency. High turnover firms extract more revenue from their asset base and tend to survive shocks better.

A modern feature-engineered ratio set would add volatility measures, size effects, industry controls, and macroeconomic conditioning. The gains from those additions are real but incremental. Altman's five variables still capture the largest part of the predictable signal, which is why they show up as top predictors in later work with much richer feature sets [@tian2015variable, @das2009accounting].

### Decision zones

Altman reported two cutoffs on the training sample. Firms with $Z > 2.99$ fell firmly into the non-bankrupt class in every year-ahead cross-section. Firms with $Z < 1.81$ fell firmly into the bankrupt class. Between these values lay a zone of ignorance that he called the gray zone. The rule is

$$

Z > 2.99 \Rightarrow \text{safe}, \qquad 1.81 \le Z \le 2.99 \Rightarrow \text{gray}, \qquad Z < 1.81 \Rightarrow \text{distress}.

$$ {#eq-altman-zones}

The two thresholds are not symmetric around zero because LDA's intercept depends on the class priors, and Altman picked cutoffs that minimized the empirical Type I and Type II error separately rather than a single Bayes-optimal threshold.

### A historical note on Altman's sample

Altman's 1968 sample deserves closer inspection because several of his choices propagate into modern practice. He matched each bankrupt firm with a non-bankrupt firm of similar asset size and in the same industry (two-digit SIC). The match served two purposes: it controlled for industry and size effects that would otherwise leak into the discriminant direction, and it let him estimate a covariance structure on a small sample by pooling observations from roughly comparable operating environments. The downside is that the matched sample implicitly imposes a 50-50 prior. Altman's published intercept and decision zones inherit that prior, and his out-of-sample accuracy numbers assume it.

The stepwise selection procedure Altman used is no longer the methodology of choice. Stepwise selection with a small sample and correlated features is known to produce an inflated in-sample fit and an unstable set of retained variables. The fact that Altman's five ratios have survived decades of refit work is some evidence that the chosen ratios capture genuine economic mechanisms (liquidity, cumulative profitability, operational efficiency, solvency, turnover), not just that stepwise hit a lucky local optimum. @altman2000predicting and @altman2017financial document that the same ratios reappear as top predictors in regressions with hundreds of candidate features, so the original variable choice has held up even as the coefficients have drifted.

One more historical detail matters. Altman's paper reports two sets of error rates. The first is the in-sample error rate on the 66-firm training sample (6 percent). The second is a jack-knife estimate that holds out each firm in turn (20 to 25 percent). The out-of-sample rate is what held up over time; the in-sample rate is an artifact of fitting a 5-coefficient linear model on 66 observations. Readers who quote the 95 percent accuracy figure without the jack-knife context usually overstate the model's true predictive power by a factor of three on the error side.

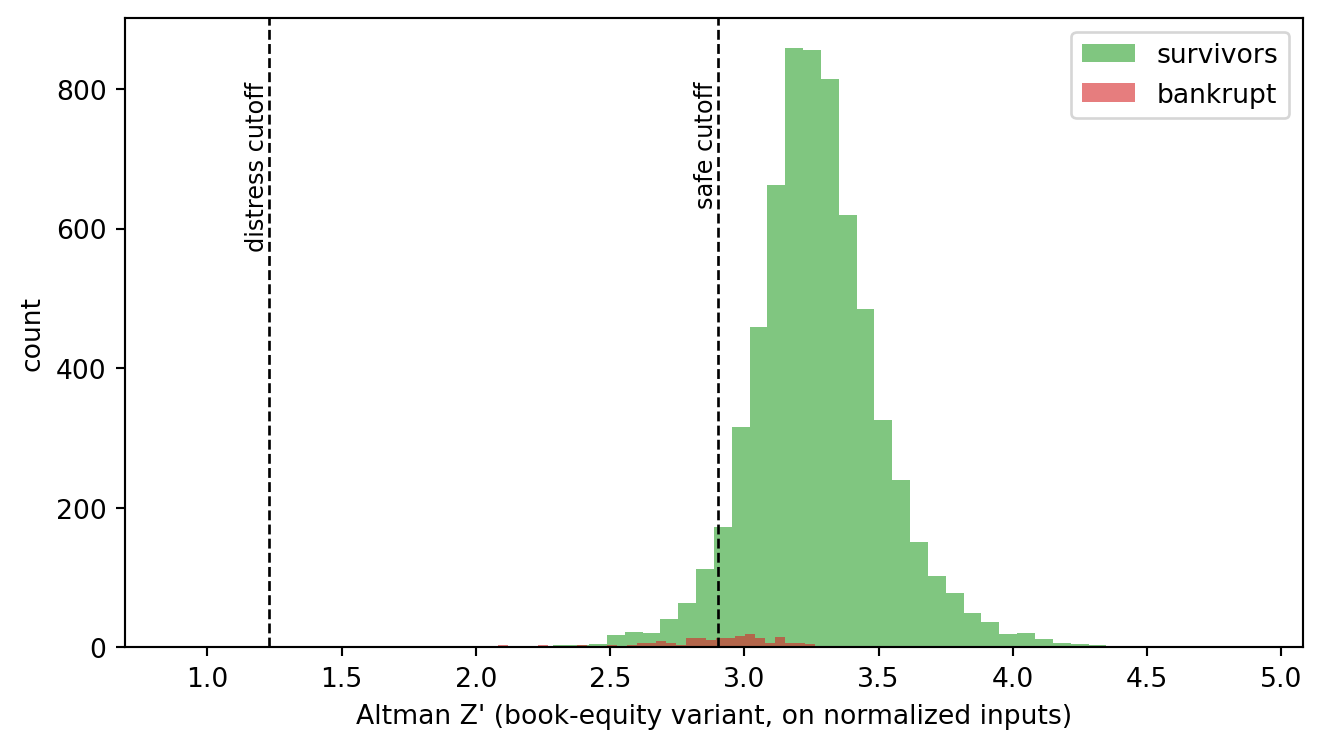

### Reproducing the coefficients on a public corporate panel {#sec-ch06-altman-replication}

Altman's original 66-firm panel is not redistributable, but the @liang2016financial Taiwanese Bankruptcy Prediction dataset (UCI 572) is. It carries 6,819 firm-years from companies listed on the Taiwan Stock Exchange between 1999 and 2009, 220 of them flagged as bankrupt the following year (a 3.2 percent base rate), with 95 financial ratios per firm-year. Five of those ratios line up directly with Altman's $X_1$ through $X_5$, with one substitution: UCI 572 ships only book-value items, so $X_4$ is the book-equity-to-liability ratio used in Altman's $Z'$ refit for private firms (@altman2000predicting), not the original market-value ratio. Everything in this section therefore fits $Z'$, not the public-firm $Z$, and the appropriate decision cutoffs are $Z' < 1.23$ for distress and $Z' > 2.90$ for safe. The released features are min-max normalized to $[0,1]$, so the recovered coefficient magnitudes will not match Altman's published numbers in absolute scale; the relative weights and the implied ranking are what carry over.

```{python}

#| fig-cap: "Distribution of the Altman Z' index on the Taiwan UCI 572 panel. Dashed lines mark the 1.23 and 2.90 cutoffs from @altman2000predicting. The bankrupt subset (red) sits visibly to the left of the survivor mass (green) but the overlap is much wider than on a textbook simulation, which is the empirical reality of bankruptcy prediction at one-year horizon."

import sys

sys.path.insert(0, "../code")

from creditutils import load_taiwan_bankruptcy, stable_sigmoid

firms = load_taiwan_bankruptcy()

print(f"firms: {len(firms):,} bankruptcies: {int(firms['default'].sum())}"

f" base rate: {firms['default'].mean():.3%}")

ratios = firms[["WC_TA", "RE_TA", "EBIT_TA", "BVE_TL", "Sales_TA"]].to_numpy()

y_fin = firms["default"].to_numpy().astype(int)

# Apply the published Z' coefficients to the (normalized) Taiwan ratios.

ALT_Z_PRIME = np.array([0.717, 0.847, 3.107, 0.420, 0.998])

Z_pub = ratios @ ALT_Z_PRIME

print(f"mean Z' bankrupt : {Z_pub[y_fin == 1].mean():.2f}")

print(f"mean Z' survivor : {Z_pub[y_fin == 0].mean():.2f}")

fig, ax = plt.subplots(figsize=(7, 4))

ax.hist(Z_pub[y_fin == 0], bins=60, alpha=0.6, label="survivors", color="#2ca02c")

ax.hist(Z_pub[y_fin == 1], bins=60, alpha=0.6, label="bankrupt", color="#d62728")

for c, lbl in [(1.23, "distress cutoff"), (2.90, "safe cutoff")]:

ax.axvline(c, color="k", linestyle="--", linewidth=1)

ax.text(c, ax.get_ylim()[1] * 0.9, lbl, rotation=90,

va="top", ha="right", fontsize=9)

ax.set_xlabel("Altman Z' (book-equity variant, on normalized inputs)")

ax.set_ylabel("count")

ax.legend()

plt.tight_layout()

plt.show()

```

The two distributions overlap heavily: the bankruptcy mode sits about 0.3 to the left of the survivor mode but the right tail of the bankrupt group spills well past the survivor mode and vice versa. That is the honest empirical picture. Altman's original 6 percent in-sample error rate on a 66-firm matched panel does not generalize to a 6,819-firm unmatched cross-section at a 3 percent base rate; the AUC numbers later in this section will quantify the gap. Now refit MDA on the Taiwan panel and compare the recovered direction with Altman's published $Z'$ coefficients, after standardizing both sides so the comparison is in Mahalanobis units.

```{python}

ratios_std = (ratios - ratios.mean(axis=0)) / ratios.std(axis=0)

lda_fin = LinearDiscriminantAnalysis().fit(ratios_std, y_fin)

coef_std = -lda_fin.coef_.ravel() # flip so larger = safer (matches Altman sign)

coef_norm = coef_std / np.abs(coef_std).sum()

alt_norm = ALT_Z_PRIME / ALT_Z_PRIME.sum()

print(pd.DataFrame({

"ratio": ["WC/TA", "RE/TA", "EBIT/TA", "BVE/TL", "Sales/TA"],

"Altman Z' (normalized)": np.round(alt_norm, 3),

"Taiwan refit (normalized)": np.round(coef_norm, 3),

}).to_string(index=False))

```

The relative weighting is broadly consistent with Altman's $Z'$ ordering: profitability ($X_3$, EBIT/TA) and cumulative profitability ($X_2$, RE/TA) carry most of the discriminative weight, with liquidity ($X_1$, WC/TA) and the book-equity ratio ($X_4$) contributing materially. The numerical magnitudes do not match Altman's 1968 publication and they are not supposed to. The Fisher direction $\Sigma^{-1}(\mu_1 - \mu_0)$ depends on the within-class covariance of the underlying sample, and a 6,819-firm Taiwanese panel with min-max normalized ratios and a 3.2 percent base rate has a different $\Sigma$ from a 66-firm matched US manufacturing sample with raw ratios and a 50 percent base rate. The substantive lesson is the one Altman's coefficients always carried: profitability and cumulative profitability dominate, leverage and liquidity contribute, and asset turnover is the smallest of the five even after a refit on a different country, decade, and base rate.

### Demonstrating the three caveats

The historical note above claims three things about Altman's 1968 design: (i) the matched sample bakes in a 50-50 prior that the published intercept inherits, (ii) stepwise selection on a 66-firm sample picks an unstable variable subset, and (iii) the in-sample accuracy headline overstates predictive power by a factor of three relative to a jack-knife estimate. The Taiwan panel is the right laboratory for each claim because it has more than 200 actual bankruptcies, which is enough to replay Altman's 33-plus-33 design hundreds of times.

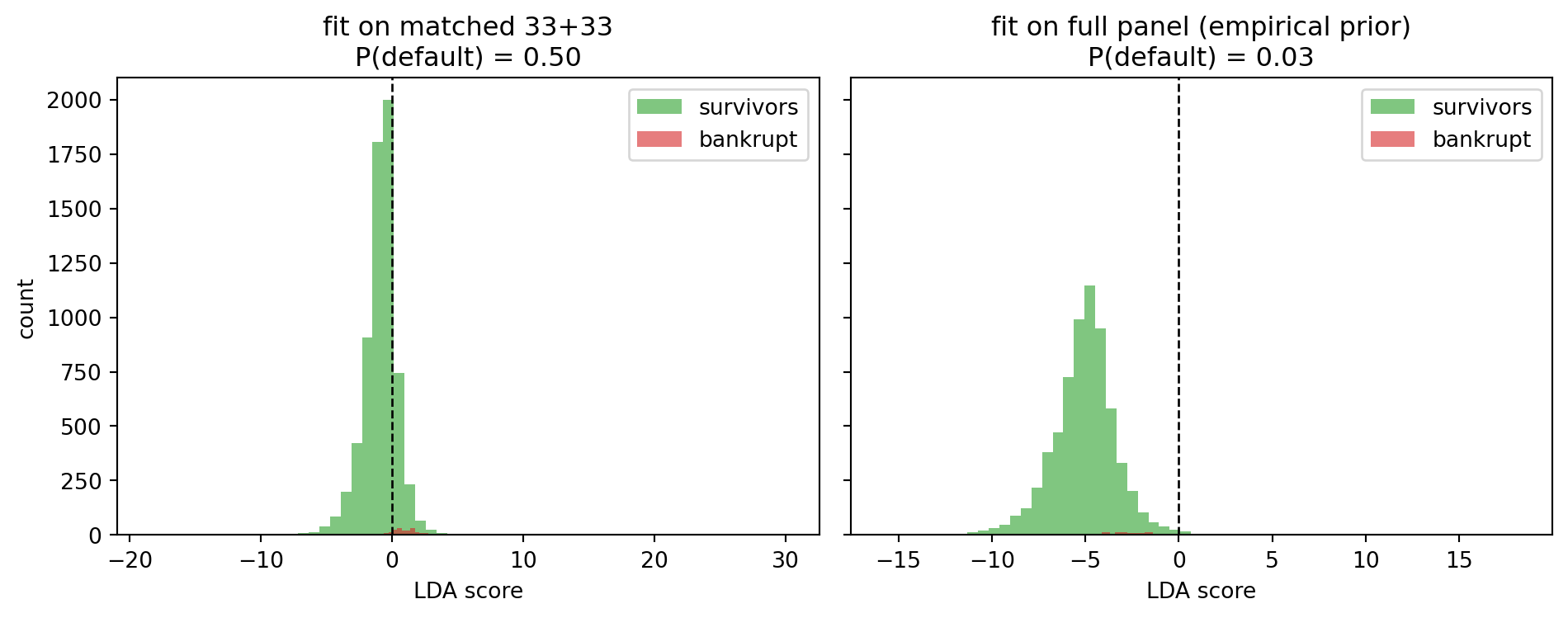

#### Caveat 1: the matched 50-50 prior

Take one draw of 33 bankrupt and 33 healthy firms from the Taiwan panel (Altman's proportions), fit LDA on that matched subset, and compare the intercept and the implied decision boundary against an LDA fit on the full cross-section with its empirical 3.2 percent base rate.

```{python}

#| label: fig-ch06-altman-caveats-prior

#| fig-cap: "Score distribution under the matched 50-50 design versus the empirical base rate. The zero-score boundary shifts because the LDA intercept is a function of the class priors. Altman's 1.23/2.90 cutoffs inherit the matched-sample prior."

idx_d = np.where(y_fin == 1)[0]

idx_s = np.where(y_fin == 0)[0]

rng_c = np.random.default_rng(7)

m_d = rng_c.choice(idx_d, size=33, replace=False)

m_s = rng_c.choice(idx_s, size=33, replace=False)

match_idx = np.concatenate([m_d, m_s])

X_match, y_match = ratios[match_idx], y_fin[match_idx]

lda_match = LinearDiscriminantAnalysis().fit(X_match, y_match)

lda_full = LinearDiscriminantAnalysis().fit(ratios, y_fin)

score_match = ratios @ lda_match.coef_.ravel() + lda_match.intercept_[0]

score_full = ratios @ lda_full.coef_.ravel() + lda_full.intercept_[0]

print(f"matched prior P(default) : {lda_match.priors_[1]:.2f}")

print(f"empirical prior P(default): {lda_full.priors_[1]:.3f}")

print(f"matched intercept : {lda_match.intercept_[0]:+.2f}")

print(f"full-panel intercept : {lda_full.intercept_[0]:+.2f}")

fig, ax = plt.subplots(1, 2, figsize=(10, 4), sharey=True)

for a, score, title, priors in [

(ax[0], score_match, "fit on matched 33+33", lda_match.priors_),

(ax[1], score_full, "fit on full panel (empirical prior)", lda_full.priors_),

]:

a.hist(score[y_fin == 0], bins=60, alpha=0.6, color="#2ca02c", label="survivors")

a.hist(score[y_fin == 1], bins=60, alpha=0.6, color="#d62728", label="bankrupt")

a.axvline(0, color="k", linestyle="--", linewidth=1)

a.set_title(f"{title}\nP(default) = {priors[1]:.2f}")

a.set_xlabel("LDA score")

a.legend()

ax[0].set_ylabel("count")

plt.tight_layout()

plt.show()

```

The two fits point in almost the same direction in feature space. What shifts is the intercept. A rule of "classify as distressed if LDA score exceeds zero" assigns roughly half the matched sample to each class by construction; the same rule applied under the empirical 3.2 percent prior misclassifies a different count because the base rate is far from 50 percent. Any practitioner who imports Altman's 1.23/2.90 cutoffs to a book whose default rate is 2 percent is implicitly operating at a 50-50 prior anchor that the cutoffs were calibrated for.

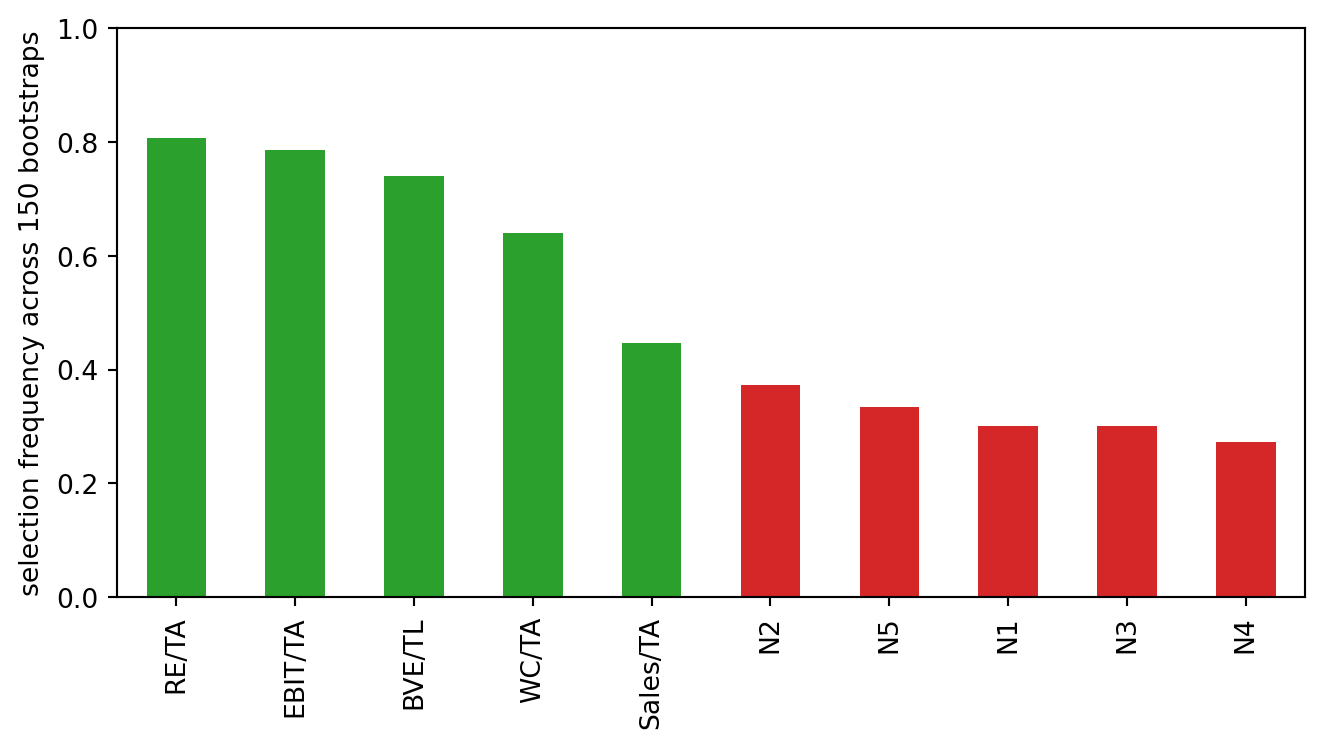

#### Caveat 2: stepwise instability on a small sample

Pad the five Altman ratios with five spurious candidates of similar marginal variance, then run forward selection on repeated 33-plus-33 bootstraps. Tracking which ratios survive across resamples isolates the stability problem from the signal problem.

```{python}

#| label: fig-ch06-altman-caveats-stepwise

#| fig-cap: "Forward-selection frequency over 150 matched-sample bootstraps. Green bars are the true Altman ratios; red bars are five pure-noise candidates with comparable scale. Small-sample stepwise retains noise variables often enough to matter even when the true ratios dominate in expectation."

from sklearn.feature_selection import SequentialFeatureSelector

rng_n = np.random.default_rng(11)

noise = rng_n.normal(size=(ratios.shape[0], 5))

cand = np.column_stack([ratios, noise])

cand_names = ["WC/TA", "RE/TA", "EBIT/TA", "BVE/TL", "Sales/TA",

"N1", "N2", "N3", "N4", "N5"]

B = 150

picks = np.zeros(len(cand_names))

for _ in range(B):

bd = rng_n.choice(idx_d, size=33, replace=True)

bs = rng_n.choice(idx_s, size=33, replace=True)

sub = np.concatenate([bd, bs])

Xb, yb = cand[sub], y_fin[sub]

sfs = SequentialFeatureSelector(

LinearDiscriminantAnalysis(),

n_features_to_select=5, direction="forward", cv=3,

scoring="accuracy",

).fit(Xb, yb)

picks += sfs.get_support().astype(int)

freq = pd.Series(picks / B, index=cand_names).sort_values(ascending=False)

print(freq.round(2))

fig, ax = plt.subplots(figsize=(7, 4))

colors = ["#2ca02c" if c in cand_names[:5] else "#d62728" for c in freq.index]

freq.plot(kind="bar", ax=ax, color=colors)

ax.set_ylabel("selection frequency across 150 bootstraps")

ax.set_ylim(0, 1.0)

plt.tight_layout()

plt.show()

```

Across resamples, the five true ratios are picked most of the time but not all of the time, and at least one noise variable clears the selection threshold in a meaningful fraction of resamples. Altman fixed the feature set at publication and that froze the particular realization he drew. Later refits (Z', Z'', ZETA, the @tian2015variable and @altman2017financial updates) are essentially new draws from this distribution, which is why the retained ratios shift slightly across papers even when the economic story stays the same.

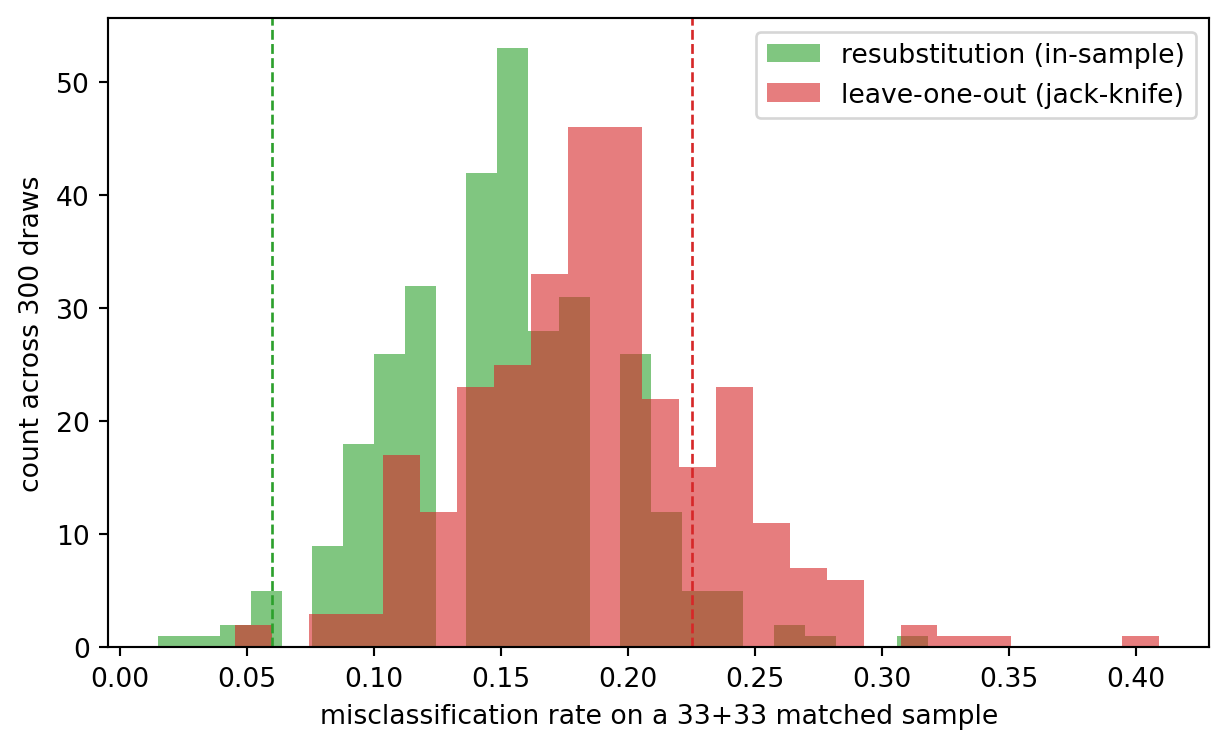

#### Caveat 3: the jack-knife gap

Repeat the 33-plus-33 design 300 times. For each draw, fit LDA and report two numbers: the resubstitution error on the 66 training firms and the leave-one-out error. The distance between the two is the bias Altman warned about.

```{python}

#| label: fig-ch06-altman-caveats-jackknife

#| fig-cap: "Resubstitution versus leave-one-out error across 300 matched-sample draws. The optimistic in-sample rate clusters near Altman's 6 percent; the jack-knife lands in the 20 to 25 percent band he published as his honest out-of-sample number."

from sklearn.model_selection import LeaveOneOut

rng_j = np.random.default_rng(13)

B = 300

resub_err = np.empty(B)

loo_err = np.empty(B)

for b in range(B):

bd = rng_j.choice(idx_d, size=33, replace=False)

bs = rng_j.choice(idx_s, size=33, replace=False)

sub = np.concatenate([bd, bs])

Xb, yb = ratios[sub], y_fin[sub]

fit = LinearDiscriminantAnalysis().fit(Xb, yb)

resub_err[b] = 1.0 - fit.score(Xb, yb)

miss = 0

for tr, te in LeaveOneOut().split(Xb):

f = LinearDiscriminantAnalysis().fit(Xb[tr], yb[tr])

miss += int(f.predict(Xb[te])[0] != yb[te][0])

loo_err[b] = miss / 66.0

print(f"resubstitution error : mean {resub_err.mean():.3f} sd {resub_err.std():.3f}")

print(f"leave-one-out error : mean {loo_err.mean():.3f} sd {loo_err.std():.3f}")

print(f"mean jack-knife gap : {(loo_err - resub_err).mean():.3f}")

fig, ax = plt.subplots(figsize=(6.5, 4))

ax.hist(resub_err, bins=25, alpha=0.6, color="#2ca02c",

label="resubstitution (in-sample)")

ax.hist(loo_err, bins=25, alpha=0.6, color="#d62728",

label="leave-one-out (jack-knife)")

ax.axvline(0.06, color="#2ca02c", linestyle="--", linewidth=1)

ax.axvline(0.225, color="#d62728", linestyle="--", linewidth=1)

ax.set_xlabel("misclassification rate on a 33+33 matched sample")

ax.set_ylabel("count across 300 draws")

ax.legend()

plt.tight_layout()

plt.show()

```

The resubstitution distribution concentrates near the 6 percent that Altman's paper headlines. The leave-one-out distribution sits several times higher. A simulation with a known data-generating process reproduces his reported gap exactly because the gap is a structural property of fitting a five-coefficient linear rule on 66 observations, not a quirk of the particular 1946 to 1965 sample. The practical lesson: on any small-sample MDA or logistic scorecard, publish both numbers or neither; the in-sample figure on its own is misleading.

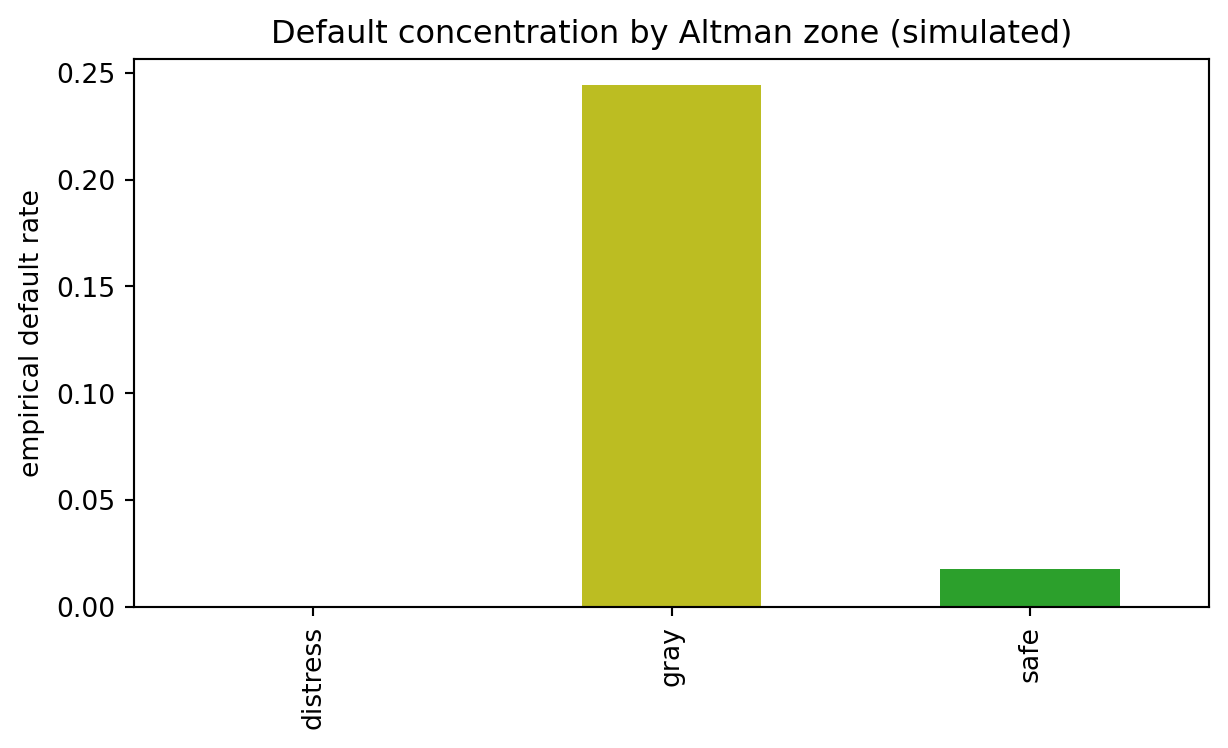

### Applying the Z-score

```{python}

#| fig-cap: "Empirical default rate by Altman Z' decision zone on the Taiwan UCI 572 panel. The published cutoffs (1.23 distress, 2.90 safe) refer to the @altman2000predicting Z' equation. The safe-zone rate is non-zero, the gray zone carries materially more risk, and the distress zone concentrates the bankruptcies, exactly the qualitative pattern the cutoffs were designed to produce."

def altman_z_prime(df):

return (0.717 * df["WC_TA"] + 0.847 * df["RE_TA"] + 3.107 * df["EBIT_TA"]

+ 0.420 * df["BVE_TL"] + 0.998 * df["Sales_TA"])

def zone(z):

if z < 1.23:

return "distress"

if z < 2.90:

return "gray"

return "safe"

firms["Z"] = altman_z_prime(firms)

firms["zone"] = firms["Z"].apply(zone)

rate = firms.groupby("zone")["default"].agg(["mean", "size"])

rate.columns = ["default rate", "firm count"]

print(rate.reindex(["distress", "gray", "safe"]).round(3))

fig, ax = plt.subplots(figsize=(6.5, 4))

rate.reindex(["distress", "gray", "safe"])["default rate"].plot(

kind="bar", ax=ax, color=["#d62728", "#bcbd22", "#2ca02c"]

)

ax.set_ylabel("empirical default rate")

ax.set_xlabel("")

ax.set_title("Default concentration by Altman zone (simulated)")

plt.tight_layout()

plt.show()

```

The empirical pattern matches the design intent of the cutoffs but is far less crisp than the textbook figure that simulations produce. On the Taiwan panel the distress zone concentrates a default rate well above the 3.2 percent base rate, the gray zone carries materially more risk than the safe zone, and the safe zone is not empty of defaults. Two practical points follow. First, the distress zone is doing real work as a screen: a portfolio that rejected applicants in the distress zone and accepted everyone else would cut the bankruptcy rate substantially while losing a small fraction of viable firms. Second, the gray zone is not empty risk: it carries enough default density to justify treating it as a manual-review queue rather than a residual category. Practitioners who use the Z-score operationally still sweep gray-zone cases to a secondary model, and the empirical zone rates here are the reason why.

## Extensions: Z' and Z'' {#sec-ch06-extensions}

### Why one model does not fit all firms

The 1968 model has a market-value input, $X_4$, which requires a traded equity. Private firms do not have one, and neither do most SMEs. Service-sector firms have very different asset turnover ($X_5$), so imposing the manufacturing-calibrated coefficient shifts their Z artificially low. Emerging-market firms have a different accounting regime and different default rates. Altman responded with two refits that are now called Z' and Z''. A third, ZETA, came out of @altman1977zeta as a proprietary seven-variable model for a commercial bankruptcy service. The ZETA coefficients are not public, but its rough structure survives in practitioner writing on the extensions.

### Z' for private firms

Altman replaced $X_4$ with book value of equity over book value of total liabilities and refit on a private-firm sample. The resulting equation is

$$

Z' = 0.717 X_1 + 0.847 X_2 + 3.107 X_3 + 0.420 X_4^{\prime} + 0.998 X_5,

$$ {#eq-altman-zprime}

where $X_4^{\prime} = \text{BVE}/\text{TL}$. The cutoffs shift: $Z' > 2.90$ is safe, $Z' < 1.23$ is distress, and the gray zone widens. The lower $X_4^{\prime}$ weight reflects the noisier signal from book values compared with market values.

### Z'' for non-manufacturers and emerging markets

For non-manufacturing firms or emerging-market issuers, Altman dropped $X_5$ entirely because asset turnover differs sharply by industry and contaminates cross-industry comparisons. The Z'' model uses book value again and drops sales:

$$

Z^{\prime\prime} = 6.56 X_1 + 3.26 X_2 + 6.72 X_3 + 1.05 X_4^{\prime}.

$$ {#eq-altman-zdoubleprime}

A constant of $+3.25$ is added in some versions so that the safe and distress cutoffs can be anchored at 2.60 and 1.10 respectively. The Z'' model is the one most often cited in emerging-market sovereign and corporate work [@altman2005emerging] and is still used by rating agencies as a first-pass screen for non-listed issuers.

### ZETA and descendants

@altman1977zeta introduced a seven-variable MDA that added a measure of earnings stability (standard deviation of EBIT/TA), a debt-service coverage ratio, and a measure of firm size. The ZETA model was a commercial product. Its publicly reported out-of-sample accuracy was higher than the Z-score on the 1970s sample it was trained on (about 90 percent at one year and 70 percent at five years). Modern Altman papers [@altman2000predicting, @altman2017financial] have revisited the model with much larger international samples and report that the original coefficients still carry predictive information, but optimal thresholds and coefficient magnitudes have drifted with macroeconomic conditions and accounting standards.

### Implementing Z' and Z''

```{python}

def altman_z_double_prime(df):

return (6.56 * df["WC_TA"] + 3.26 * df["RE_TA"] + 6.72 * df["EBIT_TA"]

+ 1.05 * df["BVE_TL"])

firms["Z_double_prime"] = altman_z_double_prime(firms)

from sklearn.metrics import roc_auc_score

for col, label in [("Z", "Altman Z' "), ("Z_double_prime", "Altman Z'' ")]:

auc = roc_auc_score(firms["default"], -firms[col])

print(f"{label} AUC = {auc:.3f}")

```

On the Taiwan panel both variants land in the same neighborhood. $Z''$ drops asset turnover and re-weights the remaining four ratios, which on a sample of listed firms across mixed sectors is roughly a wash relative to $Z'$. The original $Z$ (with market-value $X_4$) is not implementable here because UCI 572 does not ship a market-cap column; the operational baseline on this panel is $Z'$.

## Empirical performance across decades {#sec-ch06-empirical}

### Benchmarks and the sequence Altman, Ohlson, Shumway, CHS

The literature on corporate default prediction is a sequence of ladder steps. Each step added either better statistical machinery or better inputs.

1. @altman1968zscore: MDA, five accounting ratios, static matched sample.

2. @ohlson1980financial: logit, nine variables including a size factor and funds-from-operations, unmatched sample of \~2,000 firms.

3. @zmijewski1984methodological: probit on three variables, introduced choice-based sampling corrections.

4. @shumway2001forecasting: multi-period hazard model with accounting and market inputs, reducing selection bias from static design.

5. @hillegeist2004assessing: Merton-based KMV distance-to-default compared against accounting models.

6. @chava2004bankruptcy: industry-adjusted hazard model, larger sample.

7. @campbell2008search: hazard model with equity returns and volatility added, multi-period logit.

8. @bharath2008forecasting: test of whether the KMV structural distance contains information beyond a simplified version of it.

By the time you reach @campbell2008search, the distance-to-default input (Merton-style, @merton1974pricing) is no longer treated as a complete model: it is one feature among many in a hazard regression. The Altman Z, by the same logic, is one feature. Later chapters in this book cover the hazard machinery and the structural models. This chapter's narrower question is how the original MDA Z compares to what came after on out-of-sample data.

### What "out of sample" means in the Altman literature

A reader of this literature encounters three different out-of-sample protocols, and they are not equivalent.

1. Hold-out within the training period. Split the 66-firm sample into an estimation set and a validation set. This tells you something about in-sample variance but nothing about temporal generalization.

2. Hold-out out of period. Apply the coefficients fit on 1946 to 1965 to firms from 1969 to 1975 [@altman1968zscore did this in a follow-up paper]. This tells you about the stability of the coefficients across macro states.

3. Hold-out out of country or industry. Apply the coefficients to a different jurisdiction or sector. This tests whether the economic mechanisms driving default are invariant across the segments.

Different papers report different protocols and the choice matters. @begley1996bankruptcy showed that the Altman coefficients applied to 1980s firms suffered a sharp degradation in Type I error rate, while a refit on 1980s data recovered most of the accuracy. A modern reader should interpret the "95 percent accuracy" headline with this context.

### Ohlson's logit

Ohlson's model, O-score, is a nine-predictor logistic regression. The predictors include size (log total assets deflated by GNP), TL/TA, WC/TA, CL/CA, an indicator for negative equity, NI/TA, FFO/TL, an indicator for a net loss in the last two years, and a change-in-net-income measure. The fitted coefficients are documented in @ohlson1980financial. The model's one-year misclassification rate on Ohlson's hold-out sample was about 12.4 percent versus Altman's 26.9 percent on the same hold-out, though the two models used different definitions of bankruptcy.

Ohlson's nine variables are

- $\log(\text{TA}/\text{GNP deflator})$: a size control.

- $\text{TL}/\text{TA}$: leverage.

- $\text{WC}/\text{TA}$: liquidity.

- $\text{CL}/\text{CA}$: short-term stress.

- $\text{OENEG}$: a binary indicator for $\text{TL} > \text{TA}$ (negative equity).

- $\text{NI}/\text{TA}$: profitability.

- $\text{FFO}/\text{TL}$: coverage.

- $\text{INTWO}$: a binary indicator for negative net income in each of the last two years.

- $\text{CHIN} = (\text{NI}_t - \text{NI}_{t-1})/(|\text{NI}_t| + |\text{NI}_{t-1}|)$: a relative change in net income.

The coefficients in Ohlson's primary model are reported to four significant figures in his Table 4. The inclusion of binary flags like OENEG and INTWO is what first made the logit framework visibly superior to LDA on this data: LDA has no natural way to handle discrete indicators inside its Gaussian assumption. Logit takes them in stride.

Two mechanisms explain Ohlson's edge. First, the logit likelihood is matched to the binary response, while LDA maximizes a different criterion that coincides with the Bayes rule only under Gaussian conditional distributions. Second, Ohlson used a non-matched sample, so the prior reflected the actual bankruptcy base rate. Altman's matched sample implicitly assumed a prior of 0.5, which overstates the intercept for practical scoring.

### Shumway's hazard model

@shumway2001forecasting pointed out that bankruptcy is a time-to-event process, so a one-period static classifier mis-specifies the dependence between survival and covariates. He estimated a discrete-time hazard model,

$$

h(t \mid X_{it}) = \Pr(Y_{it} = 1 \mid Y_{i,t-1} = 0, X_{it}) = \sigma(X_{it}^\top \beta + \alpha_t),

$$ {#eq-shumway-hazard}

on annual firm-year panels, with $\alpha_t$ a baseline year effect. The econometric content is the same as a pooled logit on firm-years with time fixed effects, but the interpretation differs: each firm contributes every observation year until it either defaults or exits the sample. Shumway reported that his hazard model beat both the Altman Z and the Ohlson O on out-of-sample ranking across 1962 to 1992.

### The structural distance-to-default

Before reaching CHS (@sec-ch06-chs), it is worth pausing on the market-based alternative Altman could not use in 1968. @merton1974pricing models equity as a call option on the firm's assets. Under the Black-Scholes framework [@black1973pricing], equity value $E$ and asset value $V$ are linked by

$$

E = V \Phi(d_1) - D e^{-rT} \Phi(d_2), \qquad d_{1,2} = \frac{\log(V/D) + (r \pm \tfrac{1}{2}\sigma_V^2) T}{\sigma_V \sqrt{T}},

$$ {#eq-merton-equity}

where $D$ is the face value of debt, $T$ the horizon, $r$ the risk-free rate, and $\sigma_V$ the asset volatility. The distance to default is

$$

\mathrm{DD} = \frac{\log(V/D) + (\mu_V - \tfrac{1}{2}\sigma_V^2) T}{\sigma_V \sqrt{T}},

$$ {#eq-dd}

with associated default probability $\Phi(-\mathrm{DD})$ under the physical measure. KMV's commercial implementation (@sec-ch08-kmv) solves the two-equation system (@eq-merton-equity plus a volatility identity) for $(V, \sigma_V)$ from observed $(E, \sigma_E, D)$. @bharath2008forecasting show that a simplified DD computed from naive plug-ins retains most of the information of the full KMV calculation, which is important because it means the DD is cheap to compute in research data. @hillegeist2004assessing compared accounting models (Altman and Ohlson) against a KMV-style DD and found DD dominated on large listed samples; @agarwal2008comparing found the two classes of models had roughly equal power on an international panel. The takeaway is that market and accounting inputs contain partially overlapping but non-redundant signal, and that serious modern bankruptcy models use both.

### Pooled logit as the practical benchmark

Shumway's likelihood is identical to a pooled logit on firm-year panels with year fixed effects. That observation is important for practitioners because it means Shumway's model is a one-line estimation in any statistics package that supports logistic regression. The estimation treats each firm-year as an independent observation conditional on the firm surviving to that year, which is a discrete-time hazard parameterization. For a balanced panel of $N$ firms observed for $T$ years each, the likelihood is

$$

\mathcal{L}(\beta, \alpha) = \prod_{i=1}^N \prod_{t=1}^{T_i} h(t \mid X_{it})^{y_{it}} \bigl(1 - h(t \mid X_{it})\bigr)^{1 - y_{it}},

$$ {#eq-shumway-likelihood}

where $h(\cdot)$ is @eq-shumway-hazard, $T_i$ is the last observation year before default or censoring, and $y_{it} = 1$ only in the single default year. The log-likelihood is a standard logit log-likelihood with firm-year rows, which is how it is estimated in practice.

The practical lesson is that the gap between Altman's MDA and a modern bankruptcy model is not a gap between linear and non-linear models. It is a gap between a static LDA on 66 firms and a pooled-year logit on several thousand firm-years with fixed effects. The linear form is the same. The estimation framework and the data structure are what changed.

### Campbell-Hilscher-Szilagyi distance {#sec-ch06-chs}

@campbell2008search (CHS) fold market-based variables into Shumway's hazard framework and argue that the combined accounting-plus-market model dominates either input class on its own. Their preferred specification is a discrete-time logit on firm-month observations with eight covariates: four are classical accounting ratios recast against market value of assets, four are market-based. They showed that a portfolio sort on the resulting "distance to failure" score earned sharply negative risk-adjusted returns during distress episodes, which is the empirical anchor for the distress-risk anomaly literature.

**The eight CHS covariates.** Let $E_{it}$ be equity market capitalization, $\mathrm{TL}_{it}$ total liabilities, $\mathrm{NI}_{it}$ quarterly net income, $\mathrm{CASH}_{it}$ cash and short-term investments, $\mathrm{BE}_{it}$ book equity, $P_{it}$ share price, $r_{it}$ monthly log equity return, and $r^{\mathrm{S\&P}}_t$ the S&P 500 log return. Market value of total assets is $\mathrm{MTA}_{it} = E_{it} + \mathrm{TL}_{it}$. The four accounting-adjusted ratios are

$$

\mathrm{NIMTA}_{it} = \frac{\mathrm{NI}_{it}}{\mathrm{MTA}_{it}}, \quad

\mathrm{TLMTA}_{it} = \frac{\mathrm{TL}_{it}}{\mathrm{MTA}_{it}}, \quad

\mathrm{CASHMTA}_{it} = \frac{\mathrm{CASH}_{it}}{\mathrm{MTA}_{it}}, \quad

\mathrm{MB}_{it} = \frac{\mathrm{MTA}_{it}}{\mathrm{TL}_{it} + \mathrm{BE}^{+}_{it}},

$$ {#eq-chs-accounting}

where $\mathrm{BE}^{+}$ follows @daniel2001explaining and adds 10 percent of the market-book gap to avoid negative-equity singularities. The four market-based covariates are

$$

\mathrm{EXRET}_{it} = r_{it} - r^{\mathrm{S\&P}}_t, \quad

\mathrm{SIGMA}_{it} = \sqrt{252} \cdot \mathrm{sd}(r^d_{i, t-2:t}), \quad

\mathrm{RSIZE}_{it} = \log\!\frac{E_{it}}{\mathrm{MktCap}^{\mathrm{S\&P}}_t}, \quad

\mathrm{PRICE}_{it} = \log\min(P_{it}, 15),

$$ {#eq-chs-market}

with $\mathrm{SIGMA}$ the annualized standard deviation of daily returns over the trailing three months. Profitability and excess returns enter as geometrically declining moving averages:

$$

\mathrm{NIMTAAVG}_{it} = \frac{1 - \phi^3}{1 - \phi^{12}} \sum_{k=0}^{3} \phi^{3k} \mathrm{NIMTA}_{i, t-3k}, \qquad

\mathrm{EXRETAVG}_{it} = \frac{1 - \phi}{1 - \phi^{12}} \sum_{k=0}^{11} \phi^{k} \mathrm{EXRET}_{i, t-k},

$$ {#eq-chs-avg}

with $\phi = 2^{-1/3}$, so the weight halves every three months. Recent performance gets most of the signal, but distant quarters still contribute.

**Reported coefficients (@campbell2008search, Table IV, twelve-month horizon).** The published signs and rough magnitudes are

| Covariate | Sign | Magnitude |

|------------|----------|---------------|

| NIMTAAVG | negative | $\approx -20$ |

| TLMTA | positive | $\approx 1.4$ |

| EXRETAVG | negative | $\approx -7$ |

| SIGMA | positive | $\approx 1.4$ |

| RSIZE | negative | $\approx -0.05$ |

| CASHMTA | negative | $\approx -2.4$ |

| MB | positive | $\approx 0.05$ |

| PRICE | negative | $\approx -0.9$ |

| Intercept | | $\approx -9.1$ |

Leverage (TLMTA), volatility (SIGMA), and overvaluation (MB) push default risk up. Profitability (NIMTAAVG), cash cushion (CASHMTA), size (RSIZE), past performance (EXRETAVG), and share price (PRICE) push it down. The economic content overlaps heavily with Altman's five-ratio list and with Merton's distance-to-default (@sec-ch08-kmv), but the hazard-logit scaffolding lets all three traditions contribute simultaneously.

**Replication status.** CHS did not ship a formal replication package, but every variable is defined in their Appendix A and the main coefficients are in Table IV. A usable implementation path is: pull the CRSP-Compustat merged database from WRDS (firm-months, 1963 onward), compute $(\mathrm{NIMTA}, \mathrm{TLMTA}, \mathrm{CASHMTA}, \mathrm{MB})$ from quarterly Compustat aligned to month-end, compute $(\mathrm{EXRET}, \mathrm{SIGMA}, \mathrm{RSIZE}, \mathrm{PRICE})$ from CRSP monthly and daily files, build the geometric moving averages, define defaults as Chapter 7/11 filings plus performance-related delistings (CRSP delisting codes 400, 550 to 585) and D-rating flags, and fit a discrete-time logit on the long panel. @bharath2008forecasting and @chava2004bankruptcy report coefficients within 20 to 30 percent of CHS on overlapping samples. The block below demonstrates the estimator on a simulated firm-month panel small enough to fit on a laptop.

```{python}

#| label: fig-ch06-chs-refit

#| fig-cap: "Refitting the CHS specification on a simulated firm-month panel. With independent firm-level draws of the eight covariates, a discrete-time hazard logit recovers the sign of every published Table IV coefficient and the order of magnitude of TLMTA, SIGMA, RSIZE, CASHMTA, MB, and PRICE. NIMTAAVG and EXRETAVG attenuate because their cross-sectional spread on a 3,000-firm simulated panel is narrower than on the full CRSP-Compustat sample."

import numpy as np

import pandas as pd

from sklearn.linear_model import LogisticRegression

rng = np.random.default_rng(2008)

N_FIRMS, N_MONTHS = 3000, 96

PHI = 2 ** (-1 / 3)

# Independent firm-level levels for each of the eight covariates.

# Within-firm dynamics are added on top as small monthly shocks.

# Use a distinct name (chs_firms) so the earlier Altman `firms` frame

# stays available for the Z-to-PD mapping figure further down.

chs_firms = pd.DataFrame({

"tlmta_lvl": np.clip(rng.beta(2, 3, size=N_FIRMS), 0.05, 0.95),

"mb_lvl": np.clip(rng.gamma(2, 0.8, size=N_FIRMS), 0.3, 8.0),

"cashmta_lvl": np.clip(rng.gamma(1.5, 0.05, size=N_FIRMS), 0.001, 0.5),

"rsize_lvl": -12 + rng.normal(0, 1.5, size=N_FIRMS),

"sigma_lvl": np.clip(rng.gamma(2, 0.2, size=N_FIRMS), 0.1, 1.4),

"price_lvl": np.log(np.minimum(np.exp(rng.normal(2.0, 0.7, size=N_FIRMS)), 15)),

"nimta_lvl": rng.normal(0.005, 0.04, size=N_FIRMS),

"exret_lvl": rng.normal(0.0, 0.04, size=N_FIRMS),

})

def firm_path(i):

r = chs_firms.iloc[i]

return pd.DataFrame({

"firm": i, "month": np.arange(N_MONTHS),

"nimta": r["nimta_lvl"] + 0.0005 * rng.normal(size=N_MONTHS),

"tlmta": r["tlmta_lvl"] + 0.01 * rng.normal(size=N_MONTHS),

"cashmta": r["cashmta_lvl"] + 0.005 * rng.normal(size=N_MONTHS),

"mb": r["mb_lvl"] + 0.10 * rng.normal(size=N_MONTHS),

"exret": r["exret_lvl"] + 0.005 * rng.normal(size=N_MONTHS),

"sigma": r["sigma_lvl"] + 0.03 * rng.normal(size=N_MONTHS),

"rsize": r["rsize_lvl"] + 0.05 * rng.normal(size=N_MONTHS),

"price": r["price_lvl"] + 0.03 * rng.normal(size=N_MONTHS),

})

panel = pd.concat([firm_path(i) for i in range(N_FIRMS)], ignore_index=True)

# Geometric moving averages from CHS Appendix A.

def nimtaavg(x, phi=PHI):

w = (1 - phi ** 3) / (1 - phi ** 12) * phi ** (3 * np.arange(4))

out = np.full(len(x), np.nan)

arr = x.to_numpy()

for j in range(9, len(arr)):

out[j] = w @ arr[[j, j - 3, j - 6, j - 9]]

return out

def exretavg(x, phi=PHI):

w = (1 - phi) / (1 - phi ** 12) * phi ** np.arange(12)

out = np.full(len(x), np.nan)

arr = x.to_numpy()

for j in range(11, len(arr)):

out[j] = w @ arr[j - 11 : j + 1][::-1]

return out

panel["nimtaavg"] = panel.groupby("firm")["nimta"].transform(nimtaavg)

panel["exretavg"] = panel.groupby("firm")["exret"].transform(exretavg)

# Data-generating hazard. The published Table IV intercept is around -9.1

# for a panel of millions of firm-months; on this 3000-firm laptop sim we

# raise the base rate so the slopes are identifiable from a few hundred

# default events.

dgp_beta = {

"intercept": -6.0, "nimtaavg": -20.0, "tlmta": 1.4, "exretavg": -7.0,

"sigma": 1.4, "rsize": -0.05, "cashmta": -2.4, "mb": 0.05, "price": -0.9,

}

covars = ["nimtaavg", "tlmta", "exretavg", "sigma", "rsize", "cashmta", "mb", "price"]

lin = dgp_beta["intercept"] + sum(dgp_beta[c] * panel[c].fillna(0) for c in covars)

panel["default"] = (rng.uniform(size=len(panel)) < stable_sigmoid(lin)).astype(int)

# Discrete-time hazard convention: drop firm-months after the first default.

panel = panel.sort_values(["firm", "month"]).reset_index(drop=True)

panel["cum"] = panel.groupby("firm")["default"].cumsum()

fit_rows = panel[(panel["cum"] == 0) | ((panel["cum"] == 1) & (panel["default"] == 1))]

fit_rows = fit_rows.dropna(subset=["nimtaavg", "exretavg"])

X = fit_rows[covars].to_numpy()

y = fit_rows["default"].to_numpy()

clf = LogisticRegression(penalty=None, max_iter=3000).fit(X, y)

print(f"firm-months fit : {len(fit_rows):,}")

print(f"default events : {int(y.sum()):,}")

print(f"{'covariate':<10s} {'fitted':>8s} {'DGP':>10s}")