---

bibliography:

- ../references.bib

- ../refs/ch-08.bib

execute:

echo: true

eval: true

warning: false

---

# Structural Models: Merton and the KMV Framework {#sec-ch08}

::: {.callout-note appearance="simple" icon="false"}

**Scope: corporate.** Merton structural model, Black-Cox extensions, and the KMV distance-to-default. Inputs are firm-level (asset volatility, leverage, equity), so the framework does not transfer to consumer credit.

:::

## Overview {.unnumbered}

A firm defaults when it cannot pay. That sentence sounds like an accounting identity but it is really a statement about two random variables. One is the value of the firm's assets, which drifts and fluctuates as markets reprice the business. The other is the face value of the firm's obligations, which is a fixed claim written into debt indentures. Default is what happens when the first variable falls below the second on a date that matters. Everything in this chapter follows from taking that picture seriously.

Structural models make the identity operational by embedding the firm inside a no-arbitrage asset-pricing framework. Starting from the balance-sheet identity $V = E + D$, they cast equity as a call option on the firm's assets and debt as a risky bond written on the same underlying. The probability of default is then the probability that the call finishes out of the money. That idea is due to @merton1974pricing, built directly on the Black-Scholes option-pricing framework of @black1973pricing, and it remains the single most influential piece of corporate credit theory a half-century later.

The engineering version lives inside KMV (named for its founders Kealhofer, McQuown, and Vasicek), the commercial platform that Moody's bought in 2002 and turned into the public Expected Default Frequency (EDF) model. KMV translates Merton's formula into a workflow: observe equity and its volatility, back out asset value and asset volatility, compute a distance-to-default in standard deviations, map that distance into a PD using a proprietary historical table. The framework is still deployed at every major bank for wholesale and middle-market corporates, and its metric, DD, has become a standard covariate in reduced-form and accounting-based default models as well.

This chapter builds the structural model from first principles, derives distance-to-default and the PD map (@sec-ch08-dd), codes the KMV iterative solver from scratch (@sec-ch08-kmv), and compares its output to Altman Z on a simulated Compustat-like panel (@sec-ch08-compare-altman). It then develops the reduced-form alternative of @jarrow1995pricing (@sec-ch08-reduced-form), contrasts the two philosophies, and ends with a tour of the empirical horse-race literature (@sec-ch08-empirical) that led from Merton to the hybrid frailty models of @duffie2009frailty.

### Notation {.unnumbered}

Throughout this chapter: $V_t$ is the market value of the firm's assets at time $t$, $E_t$ its equity, $D$ the face value of a zero-coupon debt maturing at $T$, $\mu$ the physical drift of assets, $r$ the risk-free rate, $\sigma_V$ the asset volatility, and $\sigma_E$ the equity volatility. $\Phi$ is the standard normal CDF, $\phi$ its density. PD is real-world probability of default on the physical measure $\mathbb{P}$; PD$^Q$ is the risk-neutral counterpart on $\mathbb{Q}$. EDF is the KMV map of DD to PD. Hazard rate is $\lambda_t$, cumulative hazard $\Lambda_t = \int_0^t \lambda_s ds$.

Two pieces of that notation deserve a fuller gloss before they show up inside derivations.

#### Physical measure $\mathbb{P}$ versus risk-neutral measure $\mathbb{Q}$ {.unnumbered}

A probability measure is just a rule that assigns probabilities to events. In a structural model the relevant event is "the firm's asset value at time $T$ is below $D$". Two different rules can be applied to that same event, and the textbook calls them $\mathbb{P}$ and $\mathbb{Q}$.

The physical measure $\mathbb{P}$, also called the real-world measure, the historical measure, or the data-generating measure, is the law that actually governs the world. If you could rerun history a million times and tabulate how often each firm defaulted, the limiting frequency would be its $\mathbb{P}$ probability. Every empirical default frequency you ever read in a Moody's cohort study, an S&P transition matrix, or a Basel IRB pillar-3 disclosure is a sample estimate of a $\mathbb{P}$ probability. Under $\mathbb{P}$ the asset value drifts at the rate investors actually expect, $\mu$, which equals the risk-free rate plus a risk premium that compensates for bearing equity-like volatility: $$

dV_t = \mu V_t \, dt + \sigma_V V_t \, dW_t^{\mathbb{P}}.

$$ {#eq-asset-sde-P}

The risk-neutral measure $\mathbb{Q}$ is a different probability law on the same sample space, constructed so that every traded asset earns the risk-free rate in expectation. It is a calculational device, not a description of reality: nobody believes stocks really drift at $r$. By Girsanov's theorem $\mathbb{Q}$ replaces the physical drift with $r$ while leaving the volatility unchanged, $$

dV_t = r V_t \, dt + \sigma_V V_t \, dW_t^{\mathbb{Q}},

$$ {#eq-asset-sde-Q} and the two measures are linked by an explicit Radon-Nikodym derivative whose log involves the Sharpe ratio $(\mu - r)/\sigma_V$. The reason $\mathbb{Q}$ exists at all is the fundamental theorem of asset pricing: in a frictionless arbitrage-free market, today's price of any payoff is the discounted $\mathbb{Q}$-expectation of that payoff. Bond and CDS prices therefore embed $\mathbb{Q}$-probabilities of default by construction.

Two consequences follow. First, the same firm has two PDs, not one. The physical PD answers "how often does this firm default in the real world?" and the risk-neutral PD$^{Q}$ answers "what default probability is consistent with the price the market is charging for default protection?". Second, PD$^{Q}$ is mechanically larger than PD for any firm with a positive risk premium, because shifting the drift from $\mu$ down to $r$ pushes more probability mass below the default barrier. The wedge $\text{PD}^{Q} - \text{PD}$ is the credit risk premium, the same object that makes investment-grade bond spreads systematically wider than realized losses would justify [@huang2012how].

Concretely, plug $\mu = 0.10$, $r = 0.03$, $\sigma_V = 0.25$, $T = 1$, $V_0/D = 1.5$ into the Merton formula. The physical PD is about $0.4\%$. Replacing $\mu$ with $r$ for the risk-neutral version raises it to roughly $2.4\%$. Same firm, same balance sheet, same volatility, six times the probability, all driven by the change of measure.

The pair PD and PD$^Q$ refers to the same event (the firm defaults by time $T$) measured under two different probability laws. PD on the physical measure $\mathbb{P}$ is the actual frequency you would expect to see if you could replay history many times: it uses the physical asset drift $\mu$, which contains the equity risk premium, and it is the right number for risk management, capital, expected loss, and forecasting. PD$^Q$ on the risk-neutral measure $\mathbb{Q}$ replaces $\mu$ with the risk-free rate $r$ and is the number embedded in market prices of bonds, CDS, and other credit derivatives. Because investors demand compensation for bearing default risk, PD$^Q$ is mechanically larger than PD for the same firm; the wedge between them is the credit risk premium. Practically: use PD for loss forecasting and Basel IRB inputs, use PD$^Q$ for pricing and hedging, and never mix the two inside a single calculation.

EDF (Expected Default Frequency) is KMV's empirical replacement for the textbook formula PD $= \Phi(-\text{DD})$. The textbook formula is exact only if asset returns are truly lognormal, which they are not, so it badly understates default risk in the tails. KMV instead pools a large proprietary default database, sorts firms into DD buckets, computes the realized one-year default rate inside each bucket, and fits a smooth monotone curve through those bucket-level rates. The resulting function $\text{EDF}(\text{DD})$ is what gets shipped to clients. It is still a one-to-one map from distance-to-default to a probability, but the shape is calibrated to data rather than assumed from a Gaussian. The empirical-map step is built out in detail in @sec-ch08-dd.

## Motivation: why equity can be a call option on the firm {#sec-ch08-structural}

Consider a firm with a single zero-coupon debt contract. The firm promises to pay the creditor $D$ dollars at maturity $T$ and is financed in part by equity. Shareholders control the firm until $T$, at which point two states of the world matter.

1. Either the assets $V_T$ exceed $D$, the creditors are paid in full, and shareholders keep the residual $V_T - D$.

2. Or $V_T < D$, in which case limited liability kicks in, shareholders walk away with nothing, and creditors seize the assets worth $V_T$.

The payoff at $T$ to shareholders is therefore $$

E_T = \max(V_T - D, 0).

$$ {#eq-equity-payoff}

That is the payoff of a European call option on $V$ struck at $D$ with expiry $T$. The payoff to creditors is $$

\text{Debt}_T = \min(V_T, D) = D - \max(D - V_T, 0),

$$ {#eq-debt-payoff} which is a risk-free bond minus a European put on $V$ struck at $D$. @merton1974pricing turned these two identities into the foundation of structural credit risk by pricing them under the Black-Scholes assumptions.

The intellectual leap is that once equity is a call on assets, equity trading contains information about firm-asset volatility and firm-asset value. Equity is observed daily in liquid markets; asset value and asset volatility are not. The structural model lets you back them out. Everything KMV ships is built on that inversion.

Two warnings are worth stating before the derivations. First, this is a model. Real firms have coupon debt, senior and junior tranches, callable provisions, cross-default clauses, pension obligations, lease liabilities, and revolvers. Compressing all of that into a single zero-coupon face value is a first approximation and the extensions literature ([@black1976valuing; @geske1977valuation; @longstaff1995simple; @leland1994corporate; @leland1996optimal]) exists precisely to relax those assumptions. Second, default in the classical Merton setup only happens at $T$. In real life, covenants, rating triggers, and liquidity crises can force default earlier. Barrier versions such as @black1976valuing address that.

The emerging-market framing matters here more than in any other chapter. Merton-KMV needs a liquid equity price and an estimate of equity volatility. Vietnam has fewer than 800 listings across HOSE, HNX, and UPCoM, with thin free float at many names, and the vast majority of corporate borrowers are private SMEs with no equity price at all [@worldbank2022vietnamfinance; @adb2022vnfin]. Macro volatility amplifies the asset-drift uncertainty that already plagues Merton in developed markets. The closing emerging-market section returns to this with practical hybrids: Z'' plus CIC ratings, and Merton on the listed subset only.

### Why bother with a structural model at all

A purely statistical model of corporate default, say a logistic regression on financial ratios, can deliver competitive AUC numbers without invoking any option pricing. Why incur the cost of an option-theoretic derivation to solve a classification problem? Four reasons.

First, the structural model forces the analyst to confront the joint distribution of asset value and debt face value in a coherent way. Accounting ratios are noisy proxies for this joint distribution. The structural model is a generative story that ties them together. That generative story is what lets the framework extrapolate outside the historical sample. A logistic regression fit on 1985-2005 US data has no mechanism to think about what a sudden asset-volatility shock of the kind seen in March 2020 does to PD; the Merton model does, through $\sigma_V$.

Second, the structural framework produces PDs that are internally consistent with bond and equity prices at the same time. An accounting-only model might predict a 1% PD for a firm whose bond yield implies 4%. Either the accounting model is wrong, the bond price is wrong, or the recovery assumption is wrong. The structural model at least gives a disciplined way to choose between these hypotheses.

Third, the framework extends cleanly to more complex capital structures. The seniority ranking of debt tranches can be modeled as a waterfall of call options with progressively higher strikes. The priority of bank debt versus bond debt shows up as the strike ordering. Collateral and covenants show up as barrier features. These extensions preserve the option-theoretic skeleton and let a wholesale credit desk price instruments that a logistic regression would have no way to approach.

Fourth, structural models are forward-looking by construction. Equity prices aggregate market expectations over all future states. An accounting-based score is backward-looking: it uses last quarter's balance sheet, which reflects last quarter's performance. In fast-moving distressed situations, the backward lag of accounting data can be fatal. @vassalou2004default shows that the structural DD has information content about equity returns beyond book-to-market and size, and @bharath2008forecasting shows that DD dominates accounting ratios at short forecast horizons.

## Formal setup

### The firm under Black-Scholes dynamics

Assume a frictionless market, continuous trading, no taxes or dividends, a flat risk-free rate $r$, and a single risky firm. Firm assets evolve as a geometric Brownian motion under the physical measure $\mathbb{P}$: $$

dV_t = \mu V_t dt + \sigma_V V_t dW_t,

$$ {#eq-asset-gbm} where $W_t$ is a standard Brownian motion, $\mu$ the expected asset return, and $\sigma_V$ the asset volatility. The SDE in @eq-asset-gbm is not solved by ordinary calculus, because $W_t$ has unbounded variation and a non-vanishing quadratic variation $d\langle W \rangle_t = dt$. Ito's lemma is the chain rule that fixes this: for a twice-differentiable function $f(t, V_t)$ of an Ito process, $$

df(t, V_t) = \frac{\partial f}{\partial t}\,dt + \frac{\partial f}{\partial V}\,dV_t + \tfrac{1}{2}\frac{\partial^2 f}{\partial V^2}\,d\langle V \rangle_t,

$$ {#eq-ito-general} the only difference from the deterministic chain rule being the second-order term $\tfrac{1}{2} f_{VV}\, d\langle V \rangle_t$. That extra term is non-negligible because $(dW_t)^2 = dt$ rather than $0$.

Apply @eq-ito-general to $f(V) = \ln V$, whose derivatives are $f_V = 1/V$ and $f_{VV} = -1/V^2$. The quadratic variation of $V$ from @eq-asset-gbm is $d\langle V \rangle_t = \sigma_V^2 V_t^2\, dt$, so $$

d \ln V_t = \frac{1}{V_t}\, dV_t - \frac{1}{2}\,\frac{1}{V_t^2}\,\sigma_V^2 V_t^2\, dt

= \left(\mu - \tfrac{1}{2}\sigma_V^2\right) dt + \sigma_V\, dW_t.

$$ {#eq-ito-logV} The drift of $\ln V_t$ is therefore $\mu - \tfrac{1}{2}\sigma_V^2$, not $\mu$. The $-\tfrac{1}{2}\sigma_V^2$ piece is the Ito correction (or convexity correction): even with a fair coin, log-returns drift down because $\ln$ is concave and Jensen's inequality penalizes volatility. This is the same mechanism behind the volatility drag in geometric returns and behind the half-variance term in the Black-Scholes formula.

Integrating @eq-ito-logV from $0$ to $T$ is now ordinary calculus on a deterministic drift plus a Wiener integral, $$

\ln V_T - \ln V_0 = \left(\mu - \tfrac{1}{2}\sigma_V^2\right) T + \sigma_V\, (W_T - W_0),

$$ {#eq-logV-integrated} and exponentiating, with $W_T - W_0 \sim \mathcal{N}(0, T)$ written as $\sqrt{T}\, Z$ for a standard normal $Z$, gives the closed-form solution $$

V_T = V_0 \exp\!\left[(\mu - \tfrac{1}{2}\sigma_V^2)T + \sigma_V \sqrt{T} Z\right],\qquad Z \sim \mathcal{N}(0,1).

$$ {#eq-VT-solution} So $\ln V_T$ is normal with mean $\ln V_0 + (\mu - \tfrac{1}{2}\sigma_V^2)T$ and variance $\sigma_V^2 T$, i.e. $V_T$ is lognormal. Every PD formula in this chapter, including $\Phi(-\text{DD})$ and the Black-Scholes call price for equity, ultimately rides on @eq-VT-solution.

The firm's capital structure consists of equity $E$ and a single zero-coupon bond with face $D$ maturing at $T$. The balance sheet identity holds at every date, $$

V_t = E_t + B_t,

$$ {#eq-balance} where $B_t$ is the market value of the debt at $t$.

### The information structure: incomplete accounting information {#sec-ch08-filtration}

An important subtlety in the Merton setup is the information set. The model assumes that $V_t$ and $\sigma_V$ are known at time $t$. In practice neither is observed. What is observed is $E_t$ and a noisy proxy for $\sigma_E$ estimated from equity returns. The textbook structural model papers over this by assuming that markets can see through equity to asset value via the Black-Scholes inversion. That is a strong assumption, and relaxing it changes the model in ways large enough to deserve their own subsection.

@duffielando2001 is the canonical treatment. Their setup is worth walking through because it is the cleanest bridge from structural to reduced-form models, and it underlies several of the extensions discussed later in the chapter (jumps in @sec-ch08-dd, the structural-reduced contrast in @sec-ch08-reduced-form, and the hybrid frailty work in @sec-ch08-empirical).

#### Setup: manager's filtration versus market's filtration {.unnumbered}

The manager observes the asset path $V_t$ continuously and therefore works on the natural filtration $\mathcal{F}_t^M = \sigma(V_s : s \le t)$. The market does not. Investors see the equity price (which under Merton is a deterministic function of $V$ but in the Duffie-Lando setup is observed only at the accounting-report frequency) and a sequence of noisy accounting reports $$

y_n = \ln V_{t_n} + \varepsilon_n,\qquad \varepsilon_n \sim \mathcal{N}(0, u^2),

$$ {#eq-accounting-noise} released at dates $t_1 < t_2 < \cdots$. The market filtration is $\mathcal{F}_t^I = \sigma(y_n : t_n \le t) \vee \sigma(\mathbf{1}\{\tau \le s\} : s \le t)$, i.e. the noisy reports plus knowledge of whether the firm has already defaulted. Crucially $\mathcal{F}_t^I \subsetneq \mathcal{F}_t^M$.

Default is the first passage of $V$ to a barrier $V_B$ (the Merton special case is $V_B = D$ at $t = T$ only), $$

\tau = \inf\{t \ge 0 : V_t \le V_B\}.

$$ {#eq-tau-firstpassage}

#### The key result: predictable under $\mathcal{F}^M$, totally inaccessible under $\mathcal{F}^I$ {.unnumbered}

A stopping time is *predictable* if it can be announced by an increasing sequence of stopping times: there exist $\tau_n \uparrow \tau$ with $\tau_n < \tau$. Diffusions do not jump, so on the manager's filtration the first-passage time $\tau$ is predictable: as $V_t$ approaches $V_B$ the manager sees disaster coming. The Doob-Meyer compensator of the indicator $\mathbf{1}\{\tau \le t\}$ in this filtration is degenerate, the conditional hazard at $t = 0$ is zero, and short-horizon credit spreads collapse to zero. This is the well-known short-spread defect of the pure Merton model, which the empirical literature documents repeatedly [@huang2012how; @eom2004structural].

Project the same default time onto the smaller filtration $\mathcal{F}^I$. Because $V_t$ is now itself a random variable conditional on the noisy reports, the market does not see $V_t$ approaching $V_B$ in a deterministic way. @duffielando2001 prove that under mild regularity $\tau$ is *totally inaccessible* with respect to $\mathcal{F}^I$: it cannot be announced. The Doob-Meyer decomposition then yields a positive intensity $$

\lambda_t^I = \lim_{h \downarrow 0} \frac{1}{h}\, \Pr[\tau \le t+h \mid \mathcal{F}_t^I,\, \tau > t],

$$ {#eq-lambda-filtration} which has a closed-form expression in terms of the conditional density $g(v \mid \mathcal{F}_t^I)$ of $\ln V_t$ given the market's information, $$

\lambda_t^I = \tfrac{1}{2}\sigma_V^2\, \frac{\partial g}{\partial v}\bigg|_{v = \ln V_B}.

$$ {#eq-lambda-density} Equation @eq-lambda-density is the bridge between the structural and reduced-form worlds: a structural model with incomplete information *generates* a reduced-form intensity endogenously, rather than postulating one as in @jarrow1995pricing.

#### Why short-end spreads stop collapsing {.unnumbered}

Under full information, $\Pr[\tau \le h]$ for small $h$ behaves like $\exp(-c/h)$ near a non-zero distance to the barrier: vanishingly small. Under incomplete information, the conditional density $g$ has positive mass arbitrarily close to $\ln V_B$ even when the point estimate $\hat V_t \gg V_B$, simply because the posterior over $V_t$ is diffuse. The spread at short maturity inherits this density and becomes $O(1)$ rather than exponentially small. Numerically, with realistic accounting noise $u \in [0.10, 0.25]$ and posting frequencies of one quarter, @duffielando2001 close roughly half of the short-end credit-spread puzzle without invoking jumps or stochastic volatility.

#### Implications for the rest of the chapter {.unnumbered}

The filtration argument has three downstream consequences that recur in later sections.

1. **Empirical EDF beats theoretical** $\Phi(-\text{DD})$. The KMV calibration in @sec-ch08-dd folds the incomplete-information distortion into the bucket-wise default-rate map. That is one of the three reasons the Gaussian formula undershoots; the other two (jumps and strategic default) are listed alongside in @sec-ch08-dd.

2. **Structural-reduced hybrids are not a hack**. Because the Duffie-Lando intensity $\lambda_t^I$ is itself a structural object (a derivative of a structural posterior), running a hazard model whose intensity depends on DD plus accounting and macro covariates is consistent with the underlying theory rather than an ad-hoc patch. This is the philosophical justification for the hybrid models in @sec-ch08-reduced-form and @sec-ch08-empirical.

3. **Filtering is unavoidable in EM markets**. Vietnamese listed firms publish quarterly reports with material noise (accounting standard transition, related-party transactions, undisclosed contingent liabilities); private SMEs report annually with even larger $u$. The filtration problem is not a textbook curiosity in this setting, it is the modal case, and the practical hybrids in @sec-ch08-empirical handle it explicitly.

### Default event and default probability

Default occurs if and only if $V_T < D$. Under the physical measure $\mathbb{P}$, $$

\text{PD}^{\mathbb{P}} = \Pr[V_T < D] = \Pr\!\left[\ln V_T < \ln D\right].

$$ {#eq-pd-def} Using (@eq-VT-solution), $$

\ln V_T = \ln V_0 + (\mu - \tfrac{1}{2}\sigma_V^2)T + \sigma_V \sqrt{T} Z,

$$ {#eq-lnVT} so $$

\text{PD}^{\mathbb{P}} = \Pr\!\left[Z < \frac{\ln(D/V_0) - (\mu - \tfrac{1}{2}\sigma_V^2)T}{\sigma_V \sqrt{T}}\right] = \Phi(-\text{DD}),

$$ {#eq-pd-phi} with $$

\text{DD} = \frac{\ln(V_0/D) + (\mu - \tfrac{1}{2}\sigma_V^2)T}{\sigma_V \sqrt{T}}.

$$ {#eq-dd}

That is the definition of distance-to-default. It measures, in asset-volatility units, how many standard deviations the log asset value sits above the log default barrier after accounting for drift. The larger the DD, the smaller the PD, and the mapping is purely the normal CDF when the model is literally correct. KMV replaces $\Phi(-\text{DD})$ with an empirical map estimated from historical defaults; that calibration is developed in @sec-ch08-pd-routes, the reasons the lognormal map fails are dissected in @sec-ch08-undershoot, and a runnable empirical PD map on simulated data is built in @sec-ch08-empirical-pd-map.

## Derivation: equity as a call and debt as face value minus a put

### Step 1: translate the problem to a call option

By @eq-equity-payoff, the terminal payoff of equity is that of a European call on $V_T$ struck at $D$. The Merton claim is that everything we know about pricing Black-Scholes calls transfers directly to corporate equity. The argument runs as follows.

Under the risk-neutral measure $\mathbb{Q}$ the drift of $V$ is $r$, not $\mu$, because a self-financing hedging portfolio in $V$ must earn the risk-free rate. @harrison1979martingales and @harrison1981martingales provide the measure-theoretic machinery: in a complete arbitrage-free market there is a unique equivalent martingale measure under which discounted traded-asset prices are martingales. Asset value, as the underlying of a tradable claim, has drift $r$ under $\mathbb{Q}$, so $$

dV_t = r V_t dt + \sigma_V V_t dW_t^{\mathbb{Q}}.

$$ {#eq-V-Q}

By no-arbitrage, $E_0 = e^{-rT} \mathbb{E}^{\mathbb{Q}}[\max(V_T - D, 0)]$. Substituting the lognormal distribution of $V_T$ under $\mathbb{Q}$ and integrating yields the Black-Scholes formula, $$

E_0 = V_0 \Phi(d_1) - D e^{-rT} \Phi(d_2),

$$ {#eq-merton-equity} with $$

d_1 = \frac{\ln(V_0/D) + (r + \tfrac{1}{2}\sigma_V^2)T}{\sigma_V \sqrt{T}}, \quad d_2 = d_1 - \sigma_V \sqrt{T}.

$$ {#eq-d1d2}

### Step 2: the Black-Scholes derivation step by step

The derivation of (@eq-merton-equity) from (@eq-V-Q) and (@eq-equity-payoff) is textbook but worth spelling out because every symbol here has a credit-risk meaning.

**Step 2.1: law of the terminal asset value.** Under $\mathbb{Q}$, $V_T = V_0 \exp[(r - \tfrac{1}{2}\sigma_V^2)T + \sigma_V \sqrt{T} Z^{\mathbb{Q}}]$ with $Z^{\mathbb{Q}} \sim \mathcal{N}(0,1)$ under $\mathbb{Q}$. Equivalently, $\ln(V_T/V_0) \sim \mathcal{N}((r - \tfrac{1}{2}\sigma_V^2)T, \sigma_V^2 T)$.

**Step 2.2: split the expected payoff.** Write $$

\mathbb{E}^{\mathbb{Q}}[\max(V_T - D, 0)] = \mathbb{E}^{\mathbb{Q}}[V_T \mathbf{1}\{V_T > D\}] - D \cdot \Pr^{\mathbb{Q}}[V_T > D].

$$

**Step 2.3: the risk-neutral survival probability.** Because $\ln V_T$ is normal, $$

\Pr^{\mathbb{Q}}[V_T > D] = \Pr^{\mathbb{Q}}[\ln V_T > \ln D] = \Phi(d_2),

$$ where $d_2$ comes from standardizing $\ln V_T$ under $\mathbb{Q}$ and noticing $d_2 = \frac{\ln(V_0/D) + (r - \tfrac{1}{2}\sigma_V^2)T}{\sigma_V \sqrt{T}}$.

**Step 2.4: the expectation** $\mathbb{E}^{\mathbb{Q}}[V_T \mathbf{1}\{V_T > D\}]$. This is a standard "partial expectation of a lognormal." Change variables to $u = \ln(V_T/V_0)$, so $V_T = V_0 e^u$, and condition on $u > \ln(D/V_0)$: $$

\mathbb{E}^{\mathbb{Q}}[V_T \mathbf{1}\{V_T > D\}]

= V_0 \int_{\ln(D/V_0)}^{\infty} e^u f_u(u) du,

$$ with $f_u$ the normal density of $u$ with mean $m = (r - \tfrac{1}{2}\sigma_V^2)T$ and variance $s^2 = \sigma_V^2 T$. Completing the square, $$

\begin{aligned}

e^u f_u(u) &= \frac{1}{\sqrt{2\pi s^2}} \exp\!\left[-\frac{(u - m)^2}{2 s^2} + u\right] \\

&= e^{m + s^2/2} \cdot \frac{1}{\sqrt{2\pi s^2}} \exp\!\left[-\frac{(u - m - s^2)^2}{2 s^2}\right].

\end{aligned}

$$ The factor $e^{m + s^2/2} = e^{rT}$ because $m + s^2/2 = rT$. The remaining integral is the tail of a normal with mean $m + s^2$: $$

\int_{\ln(D/V_0)}^{\infty} e^u f_u(u) du = e^{rT} \Phi(d_1),

$$ with $d_1 = \frac{\ln(V_0/D) + (r + \tfrac{1}{2}\sigma_V^2)T}{\sigma_V \sqrt{T}}$, by direct standardization.

**Step 2.5: assemble.** Combine the two pieces and discount: $$

E_0 = e^{-rT} \left[V_0 e^{rT} \Phi(d_1) - D \Phi(d_2)\right] = V_0 \Phi(d_1) - D e^{-rT} \Phi(d_2),

$$ which is (@eq-merton-equity). Debt follows from the balance-sheet identity $B_0 = V_0 - E_0$: $$

B_0 = V_0 \Phi(-d_1) + D e^{-rT} \Phi(d_2).

$$ {#eq-merton-debt}

### Step 3: risk-neutral PD

The risk-neutral probability of default is $$

\text{PD}^{\mathbb{Q}} = 1 - \Pr^{\mathbb{Q}}[V_T > D] = 1 - \Phi(d_2) = \Phi(-d_2).

$$ {#eq-pd-Q} The only difference between $\text{PD}^{\mathbb{Q}}$ and $\text{PD}^{\mathbb{P}}$ is the drift: $r$ versus $\mu$. That difference is first-order; it is why KMV uses the physical drift and why quants pricing credit derivatives use the risk-neutral one. @vassalou2004default shows that Merton-implied default probabilities using the physical drift have genuine forecasting power for equity returns, which would not be true of the risk-neutral construct.

### Step 4: credit spread

From (@eq-merton-debt), the continuously compounded yield on the zero-coupon defaultable bond is $y = -\frac{1}{T} \ln(B_0 / D)$, so the credit spread is $$

s = y - r = -\frac{1}{T} \ln\!\left[\Phi(d_2) + \frac{V_0}{D e^{-rT}} \Phi(-d_1)\right].

$$ {#eq-spread} Merton's empirical miss is well known: plugging observed leverage, volatility, and recovery into (@eq-spread) generates spreads that are too small relative to observed investment-grade spreads, the so-called credit-spread puzzle ([@huang2012how; @collin2001determinants; @chen2010macroeconomic; @eom2004structural]). Structural models with taxes, jumps, stochastic volatility, and stochastic interest rates close some of the gap but not all.

### Numerical check: Black-Scholes and put-call parity

```{python}

import sys

sys.path.insert(0, '../code')

import numpy as np

from scipy.stats import norm

def bs_call(S, K, r, sigma, T):

"""Black-Scholes call price."""

d1 = (np.log(S/K) + (r + 0.5 * sigma**2) * T) / (sigma * np.sqrt(T))

d2 = d1 - sigma * np.sqrt(T)

return S * norm.cdf(d1) - K * np.exp(-r * T) * norm.cdf(d2)

def bs_put(S, K, r, sigma, T):

d1 = (np.log(S/K) + (r + 0.5 * sigma**2) * T) / (sigma * np.sqrt(T))

d2 = d1 - sigma * np.sqrt(T)

return K * np.exp(-r * T) * norm.cdf(-d2) - S * norm.cdf(-d1)

S, K, r, sigma, T = 100.0, 100.0, 0.05, 0.25, 1.0

call = bs_call(S, K, r, sigma, T)

put = bs_put(S, K, r, sigma, T)

parity_lhs = call - put

parity_rhs = S - K * np.exp(-r * T)

print(f"Call = {call:8.5f}")

print(f"Put = {put:8.5f}")

print(f"C - P = {parity_lhs:8.5f} S - K e^-rT = {parity_rhs:8.5f}")

```

Put-call parity is satisfied to machine precision, which confirms the equity-as-call and debt-as-face-minus-put decompositions agree. The same two functions will be reused throughout the chapter, with $V$ playing the role of $S$ and $D$ the role of $K$.

### Extensions that actually ship

The classical Merton model has well-known weaknesses and four extensions have become standard in practice.

**Barrier default.** @black1976valuing allow default to happen any time the asset value crosses a lower threshold $K < D$, capturing covenants and early-trigger clauses. The equity payoff is a down-and-out call struck at $D$ with barrier $K$. The closed form is messier but still analytic, and for moderate leverage the resulting DD is lower than the classical DD by an amount that reflects the probability of passing through the barrier before $T$. @longstaff1995simple extend to a constant barrier with exogenous recovery and a stochastic interest rate, producing term-structure fits that are materially better than pure Merton.

**Endogenous default.** @leland1994corporate and @leland1996optimal treat the default barrier as an equilibrium choice of shareholders, who compare the option value of continuing to service debt against the option of defaulting immediately. The equilibrium barrier rises with leverage and falls with asset volatility, capturing the strategic dimension of default that Merton's exogenous barrier misses. The Leland framework also delivers endogenous term-structure of credit spreads and an optimal capital structure that roughly matches observed leverage ratios in investment-grade corporates.

**Compound options.** @geske1977valuation treats equity as a compound option in the presence of multiple debt maturities. Each coupon date is itself an option on the post-coupon firm. The resulting formula is a multivariate normal integral and provides a more realistic pricing of long-dated debt with intermediate coupon payments. The compound-option correction is what KMV uses internally to deal with firms that have revolving debt maturities.

**Stochastic interest rates and jumps.** Adding Vasicek or CIR dynamics to $r$ lets the model capture the interest-rate-spread interaction that @collin2001determinants highlight. Adding jumps in $V$ raises short-horizon PD to realistic levels and closes the short end of the credit-spread puzzle. @chen2010macroeconomic embeds the whole thing inside a consumption-based asset-pricing framework with time-varying risk premia and produces a structural model that matches both the level and the cyclicality of observed credit spreads.

None of these extensions have displaced Merton as the workhorse. KMV EDF ships a compound-option variant; academic researchers still benchmark on pure Merton DD because its estimation is unambiguous and its inputs are public. The practical compromise is to use Merton DD as a feature and let a downstream logistic or tree model pick up the residual structure that the extensions would have captured analytically.

## Distance-to-default and the PD map {#sec-ch08-dd}

### Defining DD inside the model

The quantity DD from (@eq-dd) sits at the center of the whole structural edifice. It has three useful interpretations.

**Reading 1: standardized log leverage.** Rewrite $\text{DD} = \frac{\ln(V_0/D) + (\mu - \sigma_V^2/2)T}{\sigma_V \sqrt{T}}$ as the number of one-year asset-volatility units separating log asset value (drifted by $(\mu - \sigma_V^2/2)T$) from log default barrier $\ln D$. Because the numerator is the mean of $\ln V_T - \ln D$ under the physical measure and the denominator is its standard deviation, DD is literally the $z$-score of log survival.

**Reading 2:** $d_2$ under the physical drift. Compare to (@eq-d1d2): $d_2 = (\ln(V_0/D) + (r - \sigma_V^2/2)T)/(\sigma_V \sqrt{T})$. So DD and $d_2$ differ only in that DD uses $\mu$ and $d_2$ uses $r$. Under the risk-neutral measure, DD collapses to $d_2$. Structural PD under $\mathbb{Q}$ is $\Phi(-d_2)$; under $\mathbb{P}$ it is $\Phi(-\text{DD})$.

**Reading 3: standardized log-moneyness.** The call-option analogy: DD is how far in the money the implicit call $\max(V_T - D, 0)$ is expected to finish, measured in asset-return standard deviations. Very in-the-money calls correspond to very distant-to-default firms.

### From DD to PD: two routes {#sec-ch08-pd-routes}

The theoretical route maps DD to PD through the normal CDF, $$

\widehat{\text{PD}} = \Phi(-\text{DD}).

$$ {#eq-pd-phi-rn}

This is exactly right if the asset-return distribution really is lognormal. It is badly wrong in the tails of real data. Empirically, actual default rates at high DD are nowhere near as small as the normal CDF predicts. The fix in KMV is to replace $\Phi$ with an empirical map built from a large proprietary default database: group firms by DD bucket, compute the realized one-year default rate in each bucket, and smooth the bucket-level hazard to get a monotone decreasing function $\text{EDF}(\text{DD})$.

A useful stylized fact: for investment-grade firms the empirical EDF at a given DD sits roughly one to two orders of magnitude above $\Phi(-\text{DD})$. For a firm with DD equal to 4, the lognormal formula gives PD of about 3 bps; Moody's KMV EDF puts the same firm closer to 30 bps to 50 bps. This gap is one reason structural PDs cannot be used as-is for capital under a regulatory IRB model.

### Why the normal CDF undershoots {#sec-ch08-undershoot}

The discrepancy between theoretical $\Phi(-\text{DD})$ and empirical EDF is not a minor calibration bug. It reflects a deep problem with the structural model's distributional assumption. Three mechanisms conspire to produce fatter tails than the lognormal allows.

**Jumps.** Asset values do jump. Fraud disclosures, litigation surprises, adverse regulatory rulings, commodity price shocks, and pandemic-level events are not drawn from a lognormal distribution. Even a small Poisson jump component with intensity 2% per year and expected jump size -20% raises DD-implied PDs by 30-80% at low DDs. @duffie1999modeling and subsequent work in the structural literature quantify the jump contribution to observed spreads.

**Incomplete information.** The filtration problem from @sec-ch08-filtration produces a positive short-end hazard that the diffusion model lacks. Investors do not observe $V_t$ exactly; they infer it from noisy accounting and market signals. The inferred distribution of $V_t$ has fatter tails than the underlying $V_t$, and the implied PD at any given point estimate is larger. The Duffie-Lando intensity in @eq-lambda-density is precisely the contribution this channel makes to the empirical PD map.

**Strategic default.** Under limited liability, shareholders may walk away from a firm whose $V_T$ exceeds $D$ if the cost of equity injection exceeds the option value of continuing. This behavior is documented in sovereign and municipal debt (the "willingness to pay" problem) and in private equity-held firms with aggressive dividend recap structures. The Merton model does not capture strategic default because it assumes shareholders always pay if $V_T > D$.

The empirical EDF calibration absorbs all three effects by construction. If you fit a smooth map from DD to realized default rates, the map folds in the jump, information, and strategic contributions automatically. The disadvantage is that the resulting PD is not a PD in any rigorous no-arbitrage sense; it is a conditional expectation of a default indicator given a model-implied covariate. For capital purposes that is usually good enough; for exotic-derivative pricing it is not.

### Numerical implementation

```{python}

from scipy.stats import norm

import numpy as np

from creditutils import stable_sigmoid

def merton_dd_pd(V, D, sigma_V, mu, T):

"""Return (DD, PD^P) under the physical measure.

Parameters

----------

V, D : asset value and face value of debt.

sigma_V : asset volatility (annualised).

mu : physical asset drift.

T : horizon in years.

"""

denom = sigma_V * np.sqrt(T)

dd = (np.log(V / D) + (mu - 0.5 * sigma_V**2) * T) / denom

pd = norm.cdf(-dd)

return dd, pd

def merton_debt_equity(V, D, sigma_V, r, T):

"""Risk-neutral prices of debt and equity at t=0 under Merton."""

d1 = (np.log(V / D) + (r + 0.5 * sigma_V**2) * T) / (sigma_V * np.sqrt(T))

d2 = d1 - sigma_V * np.sqrt(T)

equity = V * norm.cdf(d1) - D * np.exp(-r * T) * norm.cdf(d2)

debt = V - equity

return debt, equity

V, D, sigma_V, mu, r, T = 120.0, 100.0, 0.30, 0.08, 0.03, 1.0

dd, pd_p = merton_dd_pd(V, D, sigma_V, mu, T)

debt, equity = merton_debt_equity(V, D, sigma_V, r, T)

pd_q = norm.cdf(-((np.log(V/D) + (r - 0.5*sigma_V**2)*T)/(sigma_V*np.sqrt(T))))

print(f"DD = {dd:8.4f}")

print(f"PD (phys.) = {pd_p:8.6f}")

print(f"PD (risk-n) = {pd_q:8.6f}")

print(f"Equity = {equity:8.4f}")

print(f"Debt = {debt:8.4f}")

print(f"Debt + Eq = {debt + equity:8.4f} (should equal V = {V:.4f})")

```

The risk-neutral PD is larger than the physical PD because the drift under $\mathbb{Q}$ is the risk-free rate, and any firm with $\mu > r$ is riskier in the risk-neutral world than in the real world. That wedge is the basis of the credit risk premium.

### A simple empirical PD map {#sec-ch08-empirical-pd-map}

If you have your own default database, you can build a KMV-style map in a dozen lines. The recipe is to bucket DD, compute the realized one-year default rate per bucket, and regress a logit of the default rate on DD to smooth. @bharath2008forecasting gives an influential comparison between the full structural DD and a naive approximation that skips the iterative solver; the naive version retains nearly all of the predictive power.

```{python}

# Simulated default database: 50,000 firm-years, true EDF = Phi(-DD + epsilon)

rng = np.random.default_rng(20260416)

n = 50_000

dd = rng.normal(loc=4.0, scale=2.0, size=n)

# True map: empirical EDF fatter than normal by a factor

epsilon = rng.normal(scale=0.4, size=n)

p_true = stable_sigmoid(-(1.4 * dd - 3.5 + epsilon))

y = (rng.uniform(size=n) < p_true).astype(int)

# Bucket DD into 20 quantile buckets

q = np.quantile(dd, np.linspace(0, 1, 21))

buckets = np.digitize(dd, q, right=True) - 1

buckets = np.clip(buckets, 0, 19)

import pandas as pd

tab = (pd.DataFrame({"DD": dd, "default": y, "bucket": buckets})

.groupby("bucket")

.agg(DD_mid=("DD", "mean"), default_rate=("default", "mean"), n=("DD", "size")))

print(tab.head(10).round(4))

```

That table is the empirical skeleton of EDF. KMV fits a smooth monotone curve through the `DD_mid`-to-`default_rate` mapping using a log-link-style GLM; the specific functional form is proprietary but the idea is exactly what the code above produces.

## The KMV implementation: inverting equity to recover asset value and volatility {#sec-ch08-kmv}

### The identification problem

Everything in the structural model is written in terms of unobservable inputs: $V_t$ and $\sigma_V$. Only $E_t$ is observed directly, and $\sigma_E$ can be estimated from its time series. We need a way to back out $V_t$ and $\sigma_V$ from $(E_t, \sigma_E, D, r, T)$.

Two equations pin down the two unknowns. The first is (@eq-merton-equity) relating $E$ to $V$: $$

E = V \Phi(d_1) - D e^{-rT} \Phi(d_2).

$$

The second is Ito's lemma applied to $E$ as a function of $V$. Since $E = f(V)$ with $f$ the BS call function, the instantaneous volatility of $\ln E$ satisfies $$

\sigma_E = \frac{V}{E} \frac{\partial E}{\partial V} \sigma_V = \frac{V}{E} \Phi(d_1) \sigma_V.

$$ {#eq-sigma-e-vega}

Here $\partial E / \partial V = \Phi(d_1)$ is the Black-Scholes delta of equity with respect to assets. Multiplying by $V/E$ rescales to log-returns. Equation (@eq-sigma-e-vega) is the structural-model hedge ratio.

@jones1984contingent and early KMV memos solved the system by simultaneous nonlinear root-finding on $(V, \sigma_V)$ given a single observation of $(E, \sigma_E)$. The modern KMV approach instead uses an iterative fixed-point algorithm on an observed equity time series.

### The iterative KMV algorithm

The standard KMV procedure, popularized by @vassalou2004default, is:

1. Initialize $\sigma_V^{(0)} = \sigma_E \cdot E_t/(E_t + D)$ (the naive leverage adjustment) and $V_t^{(0)} = E_t + D$.

2. Holding $\sigma_V^{(k)}$ fixed, invert (@eq-merton-equity) pointwise across the equity time series to get $V_t^{(k+1)}$ for every $t$.

3. Compute $\sigma_V^{(k+1)}$ as the annualized standard deviation of $\log V_t^{(k+1)} - \log V_{t-1}^{(k+1)}$.

4. Repeat 2-3 until $|\sigma_V^{(k+1)} - \sigma_V^{(k)}| < \epsilon$.

There are two subtleties that matter for numerical stability.

**Jensen-style correction.** Equation (@eq-sigma-e-vega) holds instantaneously but is a nonlinear transformation of $V$, so any finite-sample estimator of $\sigma_E$ implies a non-trivial $\sigma_V$. Using (@eq-sigma-e-vega) directly as a one-step estimator gives $\sigma_V \approx \sigma_E / (\Phi(d_1) V/E)$, but $\Phi(d_1)$ itself depends on $\sigma_V$. Iterating closes the loop. @duan1994maximum and @duan2004structural show that the KMV fixed-point estimator is closely related to the maximum-likelihood estimator for the transformed GBM and is consistent for $\sigma_V$ under the structural model, with the same asymptotic distribution up to a boundary correction.

**Fixed-point monotonicity.** The map $\sigma_V \mapsto \sigma_V^{(k+1)}(\sigma_V)$ is a contraction in reasonable regions of parameter space, which is why Picard iteration converges. When the firm is deeply in the money ($V \gg D$), the map is almost linear with slope near one; when the firm is near default ($V \approx D$), the map can temporarily become non-contractive and produce oscillations. Practical implementations add damping $\sigma_V^{(k+1)} = (1 - \alpha) \sigma_V^{(k)} + \alpha \sigma_V^{(k+1)}(\sigma_V^{(k)})$ with $\alpha \in (0, 1)$.

### KMV solver implementation

```{python}

from scipy.stats import norm

from scipy.optimize import brentq

import numpy as np

def equity_from_V(V_path, D, sigma_V, r, T):

"""Merton equity call as a function of V."""

V_path = np.asarray(V_path)

d1 = (np.log(V_path / D) + (r + 0.5 * sigma_V**2) * T) / (sigma_V * np.sqrt(T))

d2 = d1 - sigma_V * np.sqrt(T)

return V_path * norm.cdf(d1) - D * np.exp(-r * T) * norm.cdf(d2)

def kmv_solve(E_series, D, r, T, max_iter=100, tol=1e-6, damping=0.5):

"""Iterative KMV-style solver.

Returns

-------

V_path : recovered asset value series.

sigma_V : recovered annualised asset volatility.

n_iter : number of iterations used.

"""

E_series = np.asarray(E_series, dtype=float)

# Naive initialization

sigma_E_hat = np.std(np.diff(np.log(E_series))) * np.sqrt(252)

V = E_series + D

sigma_V = sigma_E_hat * np.mean(E_series) / (np.mean(E_series) + D)

for it in range(max_iter):

V_new = np.empty_like(V)

for i, Ei in enumerate(E_series):

f = lambda Vi: equity_from_V(np.array([Vi]), D, sigma_V, r, T)[0] - Ei

V_new[i] = brentq(f, 1e-8, 1e12)

sigma_V_new = np.std(np.diff(np.log(V_new))) * np.sqrt(252)

# Damped update

sigma_V_next = (1 - damping) * sigma_V + damping * sigma_V_new

if abs(sigma_V_next - sigma_V) < tol:

return V_new, sigma_V_next, it + 1

V, sigma_V = V_new, sigma_V_next

return V, sigma_V, max_iter

```

The loop is not vectorized inside `brentq` because the bracketing root-finder needs a scalar objective. For a 252-observation equity time series, this runs in roughly 100 milliseconds per iteration on a laptop. Production KMV systems run the same idea on millions of firm-year observations by replacing `brentq` with a vectorized Newton step on $\ln V$ since the BS call is monotone in $V$.

### Testing the solver on a simulated Compustat-like sample

```{python}

rng = np.random.default_rng(20260416)

# Ground truth asset process

n_days = 252

T_h = 1.0

D_face = 100.0

r_free = 0.03

mu_A = 0.08

sigma_A_true = 0.25

V0 = 150.0

dt = 1 / 252

z = rng.standard_normal(n_days)

V_true = np.empty(n_days)

V_true[0] = V0

for t in range(1, n_days):

V_true[t] = V_true[t-1] * np.exp((mu_A - 0.5 * sigma_A_true**2) * dt

+ sigma_A_true * np.sqrt(dt) * z[t])

# Observed equity under Merton

E_obs = equity_from_V(V_true, D_face, sigma_A_true, r_free, T_h)

# Recover V and sigma_V from E alone

V_hat, sigma_V_hat, n_iter = kmv_solve(E_obs, D_face, r_free, T_h)

print(f"True sigma_V = {sigma_A_true:.4f}")

print(f"Recovered = {sigma_V_hat:.4f}")

print(f"Error = {abs(sigma_V_hat - sigma_A_true):.4f}")

print(f"Iterations = {n_iter}")

print(f"True V[end] = {V_true[-1]:.4f}")

print(f"Recovered = {V_hat[-1]:.4f}")

print(f"Mean abs err = {np.mean(np.abs(V_hat - V_true)):.4f}")

```

Recovery is accurate to a fraction of a percent. With 252 daily observations, the limiting factor is not bias but the finite-sample variance of the log-asset-return standard deviation estimator, which equals $\sigma_V / \sqrt{2n}$ times familiar factors. That is why KMV uses rolling windows of one or two years and shrinks to a sector mean.

### Why the naive BS-implied asset volatility breaks

A common error in applied work is to compute $\sigma_V = \sigma_E \cdot E/(E + D)$, often called "leverage-adjusted" equity volatility. This is the starting point of the KMV iteration, not its output. The error scales like the difference between $\Phi(d_1) V / E$ and $E/(E + D)$, which can be large when leverage is high or when the firm is close to default. @bharath2008forecasting points out that even this naive quantity, when plugged back into the DD formula, retains most of the predictive power of the full iterative DD, but the predicted level of PD can be off by a factor of two or three.

```{python}

sigma_V_naive = np.std(np.diff(np.log(E_obs))) * np.sqrt(252) \

* np.mean(E_obs) / (np.mean(E_obs) + D_face)

print(f"Naive sigma_V = {sigma_V_naive:.4f}")

print(f"Iterative sigma_V = {sigma_V_hat:.4f}")

print(f"Truth = {sigma_A_true:.4f}")

```

The naive estimate is biased low because $\Phi(d_1)$ is generally larger than $E/(E+D)$ for firms with positive drift. The iterative solver corrects the bias.

### Common implementation gotchas

A production KMV pipeline hits several non-obvious pitfalls that take years to surface.

**Face value definition.** Merton's $D$ is the face of a single zero-coupon bond. Real firms have short-term debt, long-term debt, off-balance-sheet commitments, and operating leases. @vassalou2004default uses $D = \text{short-term debt} + \tfrac{1}{2} \cdot \text{long-term debt}$ as a pragmatic approximation. The factor $\tfrac{1}{2}$ reflects the average time to maturity of long-term debt and the coupons that will be paid before the notional. @bharath2008forecasting show that the choice of $D$ definition matters less than the KMV literature's own emphasis would suggest; several alternative definitions produce DDs that are rank-correlated at 0.95 or higher.

**Horizon** $T$. KMV uses $T = 1$ year. For capital purposes this matches the Basel one-year PD horizon. For bond pricing and credit-derivative applications, the horizon should match the instrument's maturity. The DD at $T = 5$ years and $T = 1$ year can differ substantially because the drift term $(\mu - \sigma_V^2/2) T$ scales linearly with $T$ while the noise scales with $\sqrt{T}$; for high-drift firms, longer horizons produce higher DDs.

**Dividends.** A firm that pays dividends has an effective negative drift of size equal to the dividend yield, because assets drain out of the firm. The standard fix is to use $\mu - q$ in the DD formula, where $q$ is the dividend yield. Ignoring dividends for mature blue-chip firms with 2-4% dividend yields biases DD upward by 10-20%.

**Stock splits and corporate actions.** Equity price history must be adjusted for splits, reverse splits, and spin-offs before the KMV iteration runs. Splits are easy; spin-offs change the asset base mid-sample and require a segment-by-segment reconstruction of $V$. A standard validation step is to compare implied $V_t$ against quarterly book-value-of-assets from Compustat; a persistent large gap usually indicates an unhandled corporate action.

**Delisting.** Firms that delist for reasons other than default (going private, merging into another entity) must be censored at the delisting date, not treated as survivors. The delisting indicator in CRSP (DLSTCD codes 200-699) is the standard source; @shumway2001forecasting provides the conventional mapping.

**Survivorship bias.** The KMV panel must include firms that have already defaulted, not just currently listed firms. A backtest on currently listed Compustat firms will overstate the model's accuracy by 20-40% because the most informative data points (realized defaults) are missing. The correct panel comes from the CRSP-Compustat merged database with all historical firm-years included.

**Convergence failures.** The iterative solver occasionally fails to converge for firms with extreme leverage or near-zero equity. The symptom is $\sigma_V$ oscillating between two attractors. The standard fix is damping (as in the code above) plus a fallback to the naive estimator when damping does not settle. A production pipeline logs convergence diagnostics and flags firms with non-convergence for manual review.

## Comparing structural DD to Altman Z on a simulated Compustat sample {#sec-ch08-compare-altman}

### Setup

@altman1968zscore derived Z as a discriminant-analysis score on a small US bankruptcy sample. The formula is $$

Z = 1.2 X_1 + 1.4 X_2 + 3.3 X_3 + 0.6 X_4 + 1.0 X_5,

$$ {#eq-altman-z} where \$X_1 = \$ working capital / total assets, \$X_2 = \$ retained earnings / total assets, \$X_3 = \$ EBIT / total assets, \$X_4 = \$ market value of equity / book value of total liabilities, \$X_5 = \$ sales / total assets. Higher Z means safer. The classical thresholds are Z above 2.99 (safe), between 1.81 and 2.99 (gray), below 1.81 (distress).

@altman1977zeta updated the coefficients to ZETA, and subsequent work [@ohlson1980financial; @shumway2001forecasting; @campbell2008search] generalized the approach to logistic, hazard, and multi-period frameworks. Structural DD and Altman Z are conceptually different: DD is a forward-looking, market-implied distance to the default barrier; Z is a backward-looking, accounting-implied discriminant. The natural question is whether one dominates the other on the same sample.

### A synthetic Compustat panel

Public data note: a structural KMV demonstration needs the joint distribution of equity time series, book leverage, and a default label. The accounting side is in the @liang2016financial Taiwanese Bankruptcy Prediction panel (UCI 572) used in @sec-ch06-altman-replication, but UCI 572 ships no daily equity prices, no market capitalization series, and no firm identifiers that would let one join external market data; this rules it out for distance-to-default. Free firm-month equity data (Yahoo Finance via `yfinance`, AlphaVantage) cover only currently-listed firms and so suffer from survivorship bias, which is precisely the bias that would inflate any out-of-sample KMV result. Compustat-CRSP (paywalled) is the production data source. The synthetic panel below preserves the joint dependence between accounting health and asset volatility that makes the DD-versus-Z comparison meaningful, without distributing licensed data.

```{python}

rng = np.random.default_rng(20260416)

def simulate_firm(rng):

latent = rng.normal() # positive = healthy

ta = np.exp(4.0 + 0.5 * rng.normal()) # total assets in $m

lev = float(np.clip(0.30 + 0.20 * rng.normal() - 0.10 * latent, 0.05, 0.95))

D = lev * ta

V = ta # book = market at t=0 for simplicity

sigma_V = float(np.clip(0.25 - 0.05 * latent + 0.05 * rng.normal(), 0.08, 0.80))

mu = 0.05 + 0.02 * latent

wc = ta * (0.15 + 0.10 * latent + 0.05 * rng.normal())

re = ta * (0.25 + 0.15 * latent + 0.05 * rng.normal())

ebit = ta * (0.08 + 0.06 * latent + 0.03 * rng.normal())

mve = (1 - lev) * ta * np.exp(0.10 * latent)

sales = ta * (0.90 + 0.20 * rng.normal())

return dict(V=V, D=D, sigma_V=sigma_V, mu=mu,

wc=wc, re=re, ebit=ebit, mve=mve, sales=sales,

total_liab=D, total_assets=ta, latent=latent)

firms = [simulate_firm(rng) for _ in range(400)]

```

Each firm has a latent "health" variable that drives leverage, asset volatility, asset drift, and accounting inputs jointly. Default risk is therefore cross-correlated through `latent`, which gives both DD and Z a signal to pick up.

### Compute DD, PD, Altman Z

```{python}

def altman_z(wc, re, ebit, mve, total_liab, sales, total_assets):

x1 = wc / total_assets

x2 = re / total_assets

x3 = ebit / total_assets

x4 = mve / total_liab

x5 = sales / total_assets

return 1.2 * x1 + 1.4 * x2 + 3.3 * x3 + 0.6 * x4 + 1.0 * x5

rows = []

for f in firms:

dd, pd_p = merton_dd_pd(f['V'], f['D'], f['sigma_V'], f['mu'], 1.0)

z = altman_z(f['wc'], f['re'], f['ebit'], f['mve'],

f['total_liab'], f['sales'], f['total_assets'])

rows.append(dict(DD=dd, PD=pd_p, Z=z, latent=f['latent']))

df = pd.DataFrame(rows)

print(df.describe().round(4))

```

### Rank-correlation and discrimination

```{python}

from sklearn.metrics import roc_auc_score

# Default label proxy: top decile of PD

thr = df['PD'].quantile(0.90)

df['default_proxy'] = (df['PD'] > thr).astype(int)

auc_dd = roc_auc_score(df['default_proxy'], -df['DD'])

auc_z = roc_auc_score(df['default_proxy'], -df['Z'])

corr = df[['DD', 'Z']].corr().iloc[0, 1]

print(f"Rank corr DD vs Z = {corr:.3f}")

print(f"AUC of -DD for label = {auc_dd:.3f}")

print(f"AUC of -Z for label = {auc_z:.3f}")

```

The structural DD dominates here because the label was generated from PD. That is a tautology. The more honest comparison uses an independent default signal.

```{python}

# Independent default proxy: threshold on latent health

df['default_alt'] = (df['latent'] < df['latent'].quantile(0.15)).astype(int)

auc_dd2 = roc_auc_score(df['default_alt'], -df['DD'])

auc_z2 = roc_auc_score(df['default_alt'], -df['Z'])

print(f"AUC vs latent: DD = {auc_dd2:.3f}, Z = {auc_z2:.3f}")

```

Now Z, which loads on multiple accounting variables correlated with the latent health, catches up. The empirical literature [@bharath2008forecasting; @campbell2008search] reports exactly this pattern on real data: DD and Z have correlated but not redundant information, and hybrid models that include both dominate either alone.

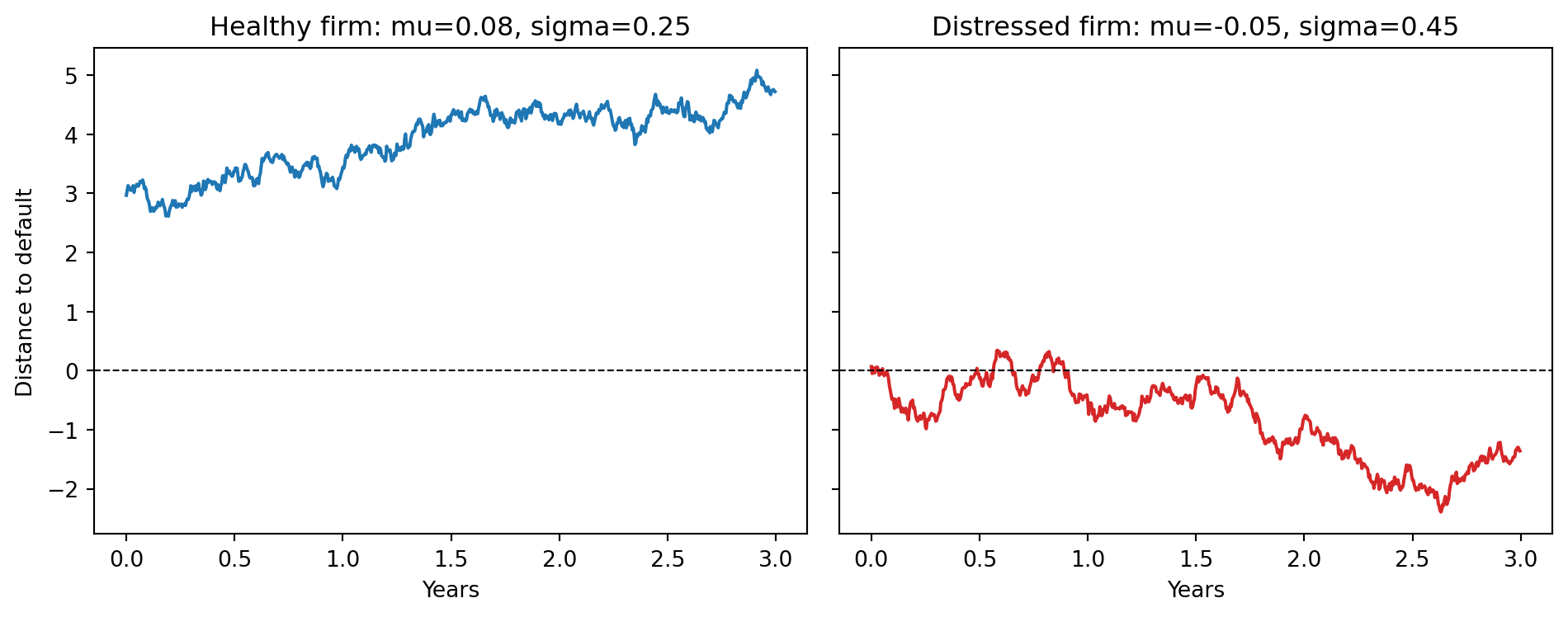

### Plotting DD over time for healthy and distressed firms

```{python}

import matplotlib.pyplot as plt

# Simulate two firms over 3 years

def simulate_V_path(V0, mu, sigma, n_days, rng):

dt = 1 / 252

z = rng.standard_normal(n_days)

V = np.empty(n_days); V[0] = V0

for t in range(1, n_days):

V[t] = V[t-1] * np.exp((mu - 0.5 * sigma**2) * dt + sigma * np.sqrt(dt) * z[t])

return V

rng = np.random.default_rng(11)

n_days = 3 * 252

V_healthy = simulate_V_path(200.0, 0.08, 0.25, n_days, rng)

V_distress = simulate_V_path(120.0, -0.05, 0.45, n_days, rng)

D_face = 100.0

def rolling_dd(V_path, D, mu, sigma_V, T=1.0):

dd = (np.log(V_path / D) + (mu - 0.5 * sigma_V**2) * T) / (sigma_V * np.sqrt(T))

return dd

dd_healthy = rolling_dd(V_healthy, D_face, 0.08, 0.25)

dd_distress = rolling_dd(V_distress, D_face, -0.05, 0.45)

fig, ax = plt.subplots(1, 2, figsize=(10, 4), sharey=True)

t = np.arange(n_days) / 252

ax[0].plot(t, dd_healthy, color="#1f77b4", lw=1.5)

ax[0].axhline(0, color="k", ls="--", lw=0.8)

ax[0].set_title("Healthy firm: mu=0.08, sigma=0.25")

ax[0].set_xlabel("Years"); ax[0].set_ylabel("Distance to default")

ax[1].plot(t, dd_distress, color="#d62728", lw=1.5)

ax[1].axhline(0, color="k", ls="--", lw=0.8)

ax[1].set_title("Distressed firm: mu=-0.05, sigma=0.45")

ax[1].set_xlabel("Years")

fig.tight_layout()

plt.show()

```

The DD trajectory of the distressed firm grinds toward zero over three years while the healthy firm drifts up. In practice, a DD below about 2 is a strong warning signal; below 1 is typically an investment-grade-to-junk migration; below 0 means the model implies the firm is already default-likely at the horizon.

### What DD tells you that a bond yield does not

There is a tempting shortcut in credit analysis: read the bond yield, subtract the risk-free rate, call the result the implied PD (after dividing by one minus recovery). This gets you to a risk-neutral PD that the market has already priced. Why bother with Merton-DD at all?

Three reasons, in order of importance.

First, bond yields incorporate a credit risk premium that is a multiple of the physical PD. The typical long-run wedge between risk-neutral and physical PD for investment-grade corporates is 4x to 8x; for high-yield it narrows to 2x to 4x. A 200 bp spread does not mean a 200 bp physical PD. @huang2012how decomposes observed spreads into expected loss, credit risk premium, tax effects, and liquidity effects, and finds that in the investment-grade segment less than a third of the spread is expected loss.

Second, not all firms have liquid bond markets. Middle-market corporates, private firms, and emerging-market issuers rarely have traded bonds with clean yields. Equity-based DD is available for any publicly listed firm and for many private firms through comparable-company adjustments. KMV's private-firm model uses sector regressions of public-firm DD on accounting ratios to produce DDs for private firms with no market data.

Third, structural DD has forward-looking content that bond yields miss at moderate horizons. Bond yields are dominated by near-term default risk; Merton DD at a one-year horizon blends near-term volatility and longer-horizon drift, which is often what a through-the-cycle risk manager wants.

The practical compromise is to use all three signals: KMV EDF from equity, market-implied PD from bonds and CDS, and a logistic-hazard model on accounting and macro covariates. Each provides a different slice of the information set, and a wholesale credit desk that watches all three detects regime shifts that a single signal would miss.

## Reduced-form models: Jarrow-Turnbull {#sec-ch08-reduced-form}

### The reduced-form idea

Structural models tie default to the firm's capital structure and asset process. Reduced-form models do the opposite. They treat the default time $\tau$ as an exogenous random variable with a hazard-rate process $\lambda_t$, and they calibrate $\lambda_t$ to market prices of defaultable bonds or CDS without modeling why default happens. The cost is that you cannot inspect the driver of $\lambda_t$ from fundamentals; the benefit is that you get exact calibration to any observed term structure and clean machinery for pricing exotic credit derivatives.

@jarrow1995pricing is the canonical paper. The two-state model posits that default is a Poisson event with intensity $\lambda$, independent of interest rates in the simplest case and correlated in extensions. @jarrow1997markov generalizes to a Markov rating-migration structure; @lando1998cox develops the Cox-process framework with stochastic $\lambda_t$; @duffie1999modeling recasts the price of a defaultable cash flow as a discounted expectation with a default-adjusted discount rate.

### Hazard rates and survival probabilities

Define the hazard rate $$

\lambda_t = \lim_{h \to 0^+} \frac{1}{h} \Pr[t \leq \tau < t + h \mid \tau \geq t].

$$ {#eq-ch08-hazard}

Cumulative hazard is $$

\Lambda(t) = \int_0^t \lambda_s ds.

$$ {#eq-cumhaz}

Survival probability: $$

S(t) = \Pr[\tau > t] = \exp\!\left[-\Lambda(t)\right] = \exp\!\left[-\int_0^t \lambda_s ds\right].

$$ {#eq-survival}

In the homogeneous case with constant $\lambda$, $\tau \sim \text{Exp}(\lambda)$ and $S(t) = e^{-\lambda t}$. In the inhomogeneous case, $\lambda_t$ is a deterministic or stochastic function of time and possibly covariates; the Cox-process case of @lando1998cox makes $\lambda_t$ itself a stochastic process.

### Pricing a zero-coupon defaultable bond

Consider a bond with face value 1 maturing at $T$, no coupons, and a recovery rate $R$ paid at $T$ in the event of default before $T$ (the "recovery-of-face-value" convention). Under the risk-neutral measure with deterministic $\lambda$ and $r$: $$

P(0, T) = \mathbb{E}^{\mathbb{Q}}\!\left[e^{-rT} \mathbf{1}\{\tau > T\}\right] + R \cdot \mathbb{E}^{\mathbb{Q}}\!\left[e^{-rT} \mathbf{1}\{\tau \leq T\}\right].

$$ {#eq-bond-general}

Independence of $\tau$ and $r$ (the simplest Jarrow-Turnbull case) gives $$

P(0, T) = e^{-rT}\left[S(T) + R(1 - S(T))\right] = e^{-rT}\left[e^{-\Lambda(T)} + R(1 - e^{-\Lambda(T)})\right].

$$ {#eq-jt-bond}

Take logs and compare to the risk-free price $e^{-rT}$ to get the implied credit spread $$

s(T) = -\frac{1}{T} \ln\!\left[S(T) + R(1 - S(T))\right].

$$ {#eq-jt-spread}

For small $\lambda T$ and $S(T) \approx 1 - \lambda T$, $$

s(T) \approx \lambda (1 - R),

$$ {#eq-jt-approx} which is the celebrated "spread is hazard times loss-given-default" approximation that industry CDS desks use every day.

### Contrasting structural and reduced-form

Structural models derive PD from the capital structure. The advantage is interpretability and a tight link to fundamentals. The disadvantage is that they miss short-horizon default risk because diffusion processes do not jump: with $V$ following a GBM, $\Pr[V_T < D]$ at short $T$ goes to zero like $\Phi(-\text{DD}) \sim e^{-\text{DD}^2/2}$, which undershoots observed short-maturity spreads badly. The fixes split into two families. The first keeps the structural skeleton and adds either jumps, stochastic volatility, or unobserved asset value (the incomplete-information route formalized by @duffielando2001 and developed in @sec-ch08-filtration). The second switches to reduced-form altogether, as @duffie1999modeling and @sundaresan2013review survey.

Reduced-form models bypass the mechanism and match spreads by construction. The advantage is calibration and tractability for exotics. The disadvantage is that $\lambda_t$ is a data-fit object with no causal story; macroeconomic stress tests must bolt on an external model for $\lambda_t$.

Hybrid approaches combine the two: DD becomes an input to a logistic or hazard model alongside accounting ratios and macro variables. @campbell2008search is the best-known hybrid, using DD together with accounting ratios in a dynamic logit to forecast bankruptcies and delistings. @duffie2009frailty adds a latent frailty factor that explains the bunching of defaults in crises beyond what DD and accounting can capture. The frailty factor is effectively a reduced-form random intensity common to many firms, and it improves out-of-sample calibration in stress periods.

### Jarrow-Turnbull simulation and MLE

```{python}

rng = np.random.default_rng(20260416)

def simulate_default_time(lam, T_max, rng):

"""Simulate tau ~ Exp(lam), censored at T_max."""

u = rng.uniform()

tau = -np.log(u) / lam

return (min(tau, T_max), 1 if tau < T_max else 0)

# Panel of 800 firms, true lambda = 0.04 per year, observation window = 5 years

n_firms = 800

true_lambda = 0.04

T_obs = 5.0

times = np.empty(n_firms); events = np.empty(n_firms, dtype=int)

for i in range(n_firms):

times[i], events[i] = simulate_default_time(true_lambda, T_obs, rng)

# Exponential MLE: lambda_hat = d / sum(t_i)

lam_hat = events.sum() / times.sum()

se_lam = lam_hat / np.sqrt(events.sum()) # approx standard error

print(f"True lambda = {true_lambda:.4f}")

print(f"MLE lambda = {lam_hat:.4f} (SE = {se_lam:.4f})")

print(f"Defaults = {events.sum():d} / {n_firms}")

```

The exponential MLE is the simplest Jarrow-Turnbull fit. When intensity varies over time, one can fit a piecewise-constant $\lambda_t$ by maximum likelihood across the hazard segments, or fit a Cox partial likelihood with covariates; both reduce to the same exponential MLE in the piecewise-constant case without covariates.

```{python}

def jt_bond_price(face, r, lam, R, T):

"""Zero-coupon defaultable bond price with recovery of face value."""

return face * np.exp(-r * T) * (np.exp(-lam * T) + R * (1 - np.exp(-lam * T)))

face = 100.0

r_free = 0.03

R_rec = 0.40

prices = np.array([jt_bond_price(face, r_free, lam_hat, R_rec, T)

for T in [1, 2, 3, 5, 10]])

print("Maturities 1-10y, prices:", np.round(prices, 4))

# Implied credit spreads

def jt_spread(lam, R, T):

return -1/T * np.log(np.exp(-lam*T) + R*(1 - np.exp(-lam*T)))

spreads = np.array([jt_spread(lam_hat, R_rec, T) for T in [1, 2, 3, 5, 10]])

print("Implied spreads (bps):", np.round(spreads * 1e4, 1))

approx = lam_hat * (1 - R_rec)

print(f"Approx (lam * LGD) = {approx * 1e4:.1f} bps")

```

The implied term structure is almost flat because $\lambda$ is constant. Non-flat term structures in practice reflect either $\lambda_t$ varying with $t$ or rating migrations in the @jarrow1997markov extension.

### Rating migrations: Jarrow-Lando-Turnbull

The single-hazard model cannot reproduce the empirical pattern of transitions between rating categories. @jarrow1997markov extend the reduced-form framework by treating the credit rating as a continuous-time Markov chain over states $\{1, 2, \dots, K, \text{default}\}$, where state $K$ is the default-absorbing state. The generator matrix $\mathbf{Q}$ collects the transition intensities; the transition probability matrix over horizon $T$ is $$

\mathbf{P}(T) = \exp(\mathbf{Q} T),

$$ {#eq-rating-transition} using the matrix exponential. Calibrating $\mathbf{Q}$ from observed one-year transition matrices published by Moody's and S&P is standard practice.

Under risk-neutral dynamics the generator $\mathbf{Q}^{\mathbb{Q}}$ may differ from the physical generator $\mathbf{Q}^{\mathbb{P}}$ through a "credit risk premium adjustment" that scales transitions toward default by a factor greater than one. @jarrow1997markov derive the adjustment from observed bond prices, and empirical estimates for investment-grade corporates put the adjustment factor in the 2 to 4 range.

The rating-migration model solves the practical problem of pricing instruments whose payoff depends on rating, not just default: corporate bonds with rating-linked coupon step-ups, credit-default swaps with rating-triggered knockouts, and structured products with rating-based waterfall tranches. It also provides a natural framework for downgrade-risk management: the probability of downgrading from BBB to BB in the next year is directly computable from $\mathbf{P}(1)$.

### Correlated defaults

Both structural and reduced-form models in their single-firm forms fail to capture the correlation in defaults across firms. Observed defaults are clustered in time: 2001, 2008, and 2020 each produced unusual bunching relative to what an independent-default model would predict.

Two mechanisms generate default correlation in the structural framework. The first is a common asset-return factor: all firms' $V_t$ respond to a common market factor, so joint downturns push multiple firms below their barriers simultaneously. This is the idea underlying the @vasicek2002distribution and @gordy2003risk one-factor models used in the Basel IRB formula. The second is a common jump factor: systemic events like financial crises deliver simultaneous jumps to many firms' asset values, which a diffusion-only model cannot capture.

@duffie2009frailty document a third mechanism: a latent "frailty" factor that is not captured by observed covariates. Even after controlling for DD, accounting ratios, and macro variables, US corporate defaults cluster more than the hazard model predicts. Adding a filtered unobserved factor improves out-of-sample calibration materially, especially in crisis periods. The frailty factor can be interpreted as capturing common information that market participants have but modelers do not.

@das2007common test whether the bunching of defaults is consistent with a doubly stochastic hazard model (the Cox-process of @lando1998cox) and reject the independence hypothesis: conditional on observed covariates, defaults are still correlated. This has become the empirical motivation for portfolio credit risk models that go beyond independent-firm PDs.

### Jarrow-Turnbull with covariates: the proportional hazards form

```{python}

from scipy.optimize import minimize

def jt_cox_nll(params, X, times, events):

"""Negative log-likelihood of a proportional-hazards exponential model.

lambda_i = exp(X_i @ beta), Exp distribution conditional on covariates.

"""

beta = params

eta = X @ beta

lam_i = np.exp(eta)

# log-lik = sum_i [events_i * log(lam_i) - lam_i * times_i]

ll = np.sum(events * eta - lam_i * times)

return -ll

# Simulate with covariates

rng = np.random.default_rng(42)

n = 1500

X = np.column_stack([

np.ones(n),

rng.normal(size=n), # DD-like covariate

rng.normal(size=n), # leverage

])

beta_true = np.array([-3.5, -0.6, 0.4])

lam_i = np.exp(X @ beta_true)

T_obs = 5.0

times = np.empty(n); events = np.empty(n, dtype=int)

u = rng.uniform(size=n)

tau = -np.log(u) / lam_i

times = np.minimum(tau, T_obs)

events = (tau < T_obs).astype(int)

res = minimize(jt_cox_nll, x0=np.zeros(3), args=(X, times, events),

method="L-BFGS-B")

print("True beta: ", np.round(beta_true, 3))

print("Estimated beta:", np.round(res.x, 3))

print("Converged: ", res.success)

```

The estimator recovers the true coefficients to two decimal places. This is the workhorse of the @duffie2007multi multi-period default-prediction literature: hazard-rate models with DD as one of the covariates among firm financial ratios and macro factors.

### Dynamic hazard versus static logistic

@shumway2001forecasting makes an important methodological point that applies directly to credit scoring: a static logit treating each firm-year as an independent observation, when the underlying data-generating process is a multi-period hazard, produces biased coefficients and inefficient use of the data. The fix is to use a discrete-time hazard specification that acknowledges the within-firm repeated observations.

The Shumway setup writes the conditional probability of default in year $t$ given survival to year $t-1$ as $$

\Pr[\tau = t \mid \tau \geq t, X_{t-1}] = \frac{1}{1 + \exp(-X_{t-1}^\top \beta - \alpha_t)},

$$ {#eq-shumway} with $\alpha_t$ a baseline-hazard term. The likelihood contribution of a firm that defaults in year $t$ is $$

L_i = \left[\prod_{s=1}^{t-1} \Pr[\tau \neq s \mid \tau \geq s, X_{i, s-1}]\right] \cdot \Pr[\tau = t \mid \tau \geq t, X_{i, t-1}],

$$ {#eq-shumway-l} while a firm censored at $t^*$ contributes the product of survival probabilities only. @shumway2001forecasting shows this likelihood is identical to a pooled logit on the firm-year panel with each firm contributing one observation per year until default or censoring, which is why the approach is sometimes called "pooled logit with risk-set sampling." The key insight is that this pooling is statistically valid only if one treats each firm-year-observation as a distinct draw, which changes the standard errors and coefficient estimates relative to the naive cross-sectional logit.

@campbell2008search build on the Shumway framework with an expanded covariate set: DD from a KMV-style solver, equity volatility from recent returns, profitability, leverage, cash holdings, market-to-book, and relative price performance. Their preferred specification puts DD and equity volatility in the same model, which is mildly redundant by construction; both contain information about asset volatility. The empirical coefficient on DD remains large and significant even with volatility in the model, which suggests that the drift component of DD ($\mu - \sigma_V^2/2$) is adding something over and above pure volatility.

### CDS and market-implied PD

A liquid credit-default-swap market exists for a few thousand corporate reference entities. CDS spreads imply risk-neutral default probabilities directly, without needing a structural inversion. The standard bootstrap procedure is:

1. Observe par CDS spreads at maturities 1y, 3y, 5y, 7y, 10y.

2. Assume a recovery rate, typically 40% for senior unsecured corporate bonds.

3. Solve for a piecewise-constant hazard rate $\lambda_t$ that reprices the CDS term structure exactly.

The resulting $\lambda_t$ is a risk-neutral intensity. Converting to physical hazard requires a credit risk premium assumption, which in practice is calibrated from the historical ratio of observed default rates to CDS-implied rates, typically 0.25 to 0.5 for investment grade.

For firms with liquid CDS, the CDS-implied PD is usually the preferred input for short-horizon trading decisions: CDS updates in real time, reflects credit market consensus, and is arbitrage-consistent with bond prices. For firms without liquid CDS (the vast majority of corporates by count), the KMV-style structural PD remains the standard. A sophisticated credit desk runs both and reconciles discrepancies as potential trading signals.

## Empirical comparison: structural, accounting, hybrid {#sec-ch08-empirical}

### What the literature has settled

Three families of corporate-default models compete in the empirical literature.

**Structural.** DD from @merton1974pricing and its commercial implementation in KMV. Inputs: equity price, equity volatility, leverage. Output: PD as $\Phi(-\text{DD})$ or a proprietary EDF map.

**Accounting-based.** @altman1968zscore (linear discriminant, @sec-ch06-discriminant), @ohlson1980financial (static logit), @shumway2001forecasting (hazard logit). Inputs: balance-sheet ratios. Output: default score, interpretable as log-odds of default.

**Hybrid/dynamic.** @campbell2008search, @duffie2007multi, @duffie2009frailty. Inputs: DD plus accounting ratios plus macro/industry factors, fit via dynamic hazard model, often with latent frailty.

The empirical verdict, across multiple studies on US data, is reasonably consistent:

1. @bharath2008forecasting show that a naive DD, computed without the iterative KMV solver, has nearly the same forecasting accuracy as the full DD. They also show that DD enters significantly in a hazard model with accounting ratios but does not dominate Altman Z.

2. @campbell2008search report an AUC near 0.94 for one-year bankruptcy prediction using a dynamic logit with twelve accounting and market covariates; DD by itself reaches about 0.87. The incremental contribution of DD after controlling for profitability, leverage, and equity volatility is modest but significant.

3. @hillegeist2004assessing compare Merton-based BSM probabilities to Altman Z and Ohlson O on US bankruptcies 1980-2000 and find BSM dominates accounting-only models but is dominated by the hybrid.

4. @duffie2009frailty document that a common frailty factor, on top of DD and accounting variables, is necessary to explain the clustering of defaults in 2001 and 2008.

The practical implication is that structural DD is a useful covariate but not a sufficient statistic for corporate PD. Wholesale IRB models at large banks typically blend DD, accounting ratios, and industry/macro overlays, with ratings benchmarks from Moody's EDF and S&P as external anchors.

### Benchmark code

We reuse the simulated panel from earlier, compute DD, Z, and an Ohlson-style logit, and compare discrimination on a held-out default label that mixes DD and accounting information.

```{python}

from sklearn.linear_model import LogisticRegression