import pandas as pd

import numpy as np

import sqlite3

import statsmodels.formula.api as smf

import statsmodels.api as sm

from pandas.tseries.offsets import MonthEnd

# Connect to the Vietnamese data

tidy_finance = sqlite3.connect(database="data/tidy_finance_python.sqlite")

# Load Monthly Prices (HOSE & HNX)

prices_monthly = pd.read_sql_query(

sql="SELECT symbol, date, ret_excess, mktcap, mktcap_lag FROM prices_monthly",

con=tidy_finance,

parse_dates={"date"}

)

# Load Book Equity (derived from Vietnamese Financial Statements)

comp_vn = pd.read_sql_query(

sql="SELECT datadate, symbol, be FROM comp_vn",

con=tidy_finance,

parse_dates={"datadate"}

)

# Load Rolling Market Betas (Pre-calculated in Chapter 'Beta Estimation')

beta_monthly = pd.read_sql_query(

sql="SELECT symbol, date, beta FROM beta_monthly",

con=tidy_finance,

parse_dates={"date"}

)20 Fama-MacBeth Regressions

In this chapter, we delve into the implementation of the Fama and MacBeth (1973) regression approach, a cornerstone of empirical asset pricing. While portfolio sorts provide a robust, non-parametric view of the relationship between characteristics and returns, they struggle when we need to control for multiple factors simultaneously. For instance, in the Vietnamese stock market (HOSE and HNX), small-cap stocks often exhibit high illiquidity. Does the “Size effect” exist because small stocks are risky, or simply because they are illiquid? Fama-MacBeth (FM) regressions allow us to disentangle these effects in a linear framework.

We will implement a version of the FM procedure, accounting for:

- Weighted Least Squares (WLS): To prevent micro-cap stocks, which are prevalent and volatile in Vietnam, from dominating the estimates.

- Newey-West Adjustments: To handle the serial correlation often observed in Vietnamese market risk premiums.

20.1 The Econometric Framework

The Fama-MacBeth procedure is essentially a two-step filter that separates the cross-sectional variation in returns from the time-series variation.

20.1.1 Intuition: Why not Panel OLS?

A naive approach would be to pool all data (\(N\) stocks \(\times\) \(T\) months) and run a single Ordinary Least Squares (OLS) regression:

\[ r_{i,t+1} = \alpha + \beta_{i,t} \lambda + \epsilon_{i,t+1} \]

However, this assumes that the error terms \(\epsilon_{i,t+1}\) are independent across firms. In reality, stock returns are highly cross-sectionally correlated (if the VN-Index crashes, most stocks fall together). A pooled OLS would underestimate the standard errors, leading to “false positive” discoveries of risk factors. Fama-MacBeth solves this by running \(T\) separate cross-sectional regressions, effectively treating each month as a single independent observation of the risk premium.

20.1.2 Mathematical Derivation

20.1.2.1 Step 1: Cross-Sectional Regressions

For each month \(t\), we estimate the premium \(\lambda_{k,t}\) for \(K\) factors. Let \(r_{i,t+1}\) be the excess return of asset \(i\) at time \(t+1\). Let \(\boldsymbol{\beta}_{i,t}\) be a vector of \(K\) characteristics (e.g., Market Beta, Book-to-Market, Size) known at time \(t\).

The model for a specific month \(t\) is: \[ \mathbf{r}_{t+1} = \mathbf{X}_t \boldsymbol{\lambda}_{t+1} + \boldsymbol{\alpha}_{t+1} + \boldsymbol{\epsilon}_{t+1} \]

Where:

- \(\mathbf{r}_{t+1}\) is an \(N \times 1\) vector of returns.

- \(\mathbf{X}_t\) is an \(N \times (K+1)\) matrix of factor exposures (including a column of ones for the intercept).

- \(\boldsymbol{\lambda}_{t+1}\) is the vector of risk premiums realized in month \(t+1\).

To use Weighted Least Squares (WLS), We define a weighting matrix \(\mathbf{W}_t\) (typically diagonal with market capitalizations). The estimator for month \(t\) is: \[ \hat{\boldsymbol{\lambda}}_{t+1} = (\mathbf{X}_t^\top \mathbf{W}_t \mathbf{X}_t)^{-1} \mathbf{X}_t^\top \mathbf{W}_t \mathbf{r}_{t+1} \]

20.1.2.2 Step 2: Time-Series Aggregation

We now have a time-series of \(T\) estimates: \(\hat{\lambda}_1, \hat{\lambda}_2, \dots, \hat{\lambda}_T\). The final estimate of the risk premium is the time-series average: \[ \hat{\lambda}_k = \frac{1}{T} \sum_{t=1}^T \hat{\lambda}_{k,t} \]

The standard error is derived from the standard deviation of these monthly estimates: \[ \sigma(\hat{\lambda}_k) = \sqrt{\frac{1}{T^2} \sum_{t=1}^T (\hat{\lambda}_{k,t} - \hat{\lambda}_k)^2} \]

20.2 Data Preparation

We utilize data from our local SQLite database. In Vietnam, the fiscal year typically ends in December, and audited reports are required by April. To ensure no look-ahead bias, we lag accounting data (Book Equity) to match returns starting in July (a 6-month conservative lag, similar to Fama-French, but adapted for Vietnamese reporting delays).

We construct our testing characteristics:

- (Market Beta): The sensitivity to the VN-Index.

- Size (ln(ME)): The natural log of market capitalization.

- Value (BM): The ratio of Book Equity to Market Equity.

# Prepare Characteristics

characteristics = (

comp_vn

# Align reporting date to month end

.assign(date=lambda x: pd.to_datetime(x["datadate"]) + MonthEnd(0))

# Merge with price data to get Market Cap at fiscal year end

.merge(prices_monthly, on=["symbol", "date"], how="left")

.merge(beta_monthly, on=["symbol", "date"], how="left")

.assign(

# Compute Book-to-Market

bm=lambda x: x["be"] / x["mktcap"],

log_mktcap=lambda x: np.log(x["mktcap"]),

# Create sorting date: Financials valid from July of year t+1

sorting_date=lambda x: x["date"] + pd.DateOffset(months=6) + MonthEnd(0),

)

.get(["symbol", "bm", "beta", "sorting_date"])

.dropna()

)

characteristics.head()| symbol | bm | beta | sorting_date | |

|---|---|---|---|---|

| 8729 | VTV | 7.034945e+08 | 0.847809 | 2017-06-30 |

| 8732 | MTG | 2.670306e+09 | 1.140066 | 2017-06-30 |

| 8739 | MKV | 6.505031e+08 | -0.448319 | 2017-06-30 |

| 8740 | MIC | 1.243127e+09 | 0.772140 | 2017-06-30 |

| 8742 | MCP | 6.657350e+08 | 0.348139 | 2017-06-30 |

# Merge back to monthly return panel

data_fm = (prices_monthly

.merge(characteristics,

left_on=["symbol", "date"],

right_on=["symbol", "sorting_date"],

how="left")

# .merge(beta_monthly, on=["symbol", "date"], how="left")

.sort_values(["symbol", "date"])

)

# Forward fill characteristics for 12 months (valid until next report)

data_fm[["bm"]] = data_fm.groupby("symbol")[["bm"]].ffill(limit=12)

# Log Market Cap is updated monthly

data_fm["log_mktcap"] = np.log(data_fm["mktcap"])

# Lead returns: We use characteristics at t to predict return at t+1

data_fm["ret_excess_lead"] = data_fm.groupby("symbol")["ret_excess"].shift(-1)

# Cleaning: Remove rows with missing future returns or characteristics

data_fm = data_fm.dropna(subset=["ret_excess_lead", "beta", "log_mktcap", "bm"])

print(data_fm.head())

print(f"Data ready: {len(data_fm):,} observations from {data_fm.date.min().date()} to {data_fm.date.max().date()}") symbol date ret_excess mktcap mktcap_lag bm \

163 AAA 2017-06-30 0.129454 2078.455619 1834.816104 7.929854e+08

175 AAA 2018-06-30 -0.067690 2758.426126 2948.159140 8.161755e+08

187 AAA 2019-06-30 0.030469 3141.519560 3038.799575 1.389438e+09

199 AAA 2020-06-30 -0.035462 2311.250278 2387.972279 1.497272e+09

211 AAA 2021-06-30 0.275355 5423.280296 4241.283308 1.456989e+09

beta sorting_date log_mktcap ret_excess_lead

163 1.479060 2017-06-30 7.639380 -0.051090

175 1.090411 2018-06-30 7.922416 -0.095926

187 1.099956 2019-06-30 8.052462 -0.027856

199 0.954144 2020-06-30 7.745544 -0.098769

211 1.245004 2021-06-30 8.598456 -0.175128

Data ready: 5,075 observations from 2017-06-30 to 2023-06-3020.3 Step 1: Cross-Sectional Regressions with WLS

Hou, Xue, and Zhang (2020) argue that micro-cap stocks distorts inference because they have high transaction costs and idiosyncratic volatility. In Vietnam, this is exacerbated by “penny stock” speculation.

We implement Weighted Least Squares (WLS) where weights are the market capitalization of the prior month. This tests if the factors are priced in the investable universe, not just the equal-weighted average of tiny stocks.

def run_cross_section(df):

# Standardize inputs for numerical stability

# Note: We do NOT standardize the dependent variable (returns)

# We standardize regressors to interpret coefficients as "per 1 SD change" if desired,

# BUT for pure risk premium estimation, we usually keep raw units.

# Here we use raw units to interpret lambda as % return per unit of characteristic.

# Define Weighted Least Squares

model = smf.wls(

formula="ret_excess_lead ~ beta + log_mktcap + bm",

data=df,

weights=df["mktcap_lag"] # Weight by size

)

results = model.fit()

return results.params

# Apply to every month

risk_premiums = (data_fm

.groupby("date")

.apply(run_cross_section)

.reset_index()

)

print(risk_premiums.head()) date Intercept beta log_mktcap bm

0 2017-06-30 -0.089116 -0.063799 0.010284 2.897813e-11

1 2018-06-30 -0.023221 -0.008252 0.001890 1.377518e-11

2 2019-06-30 -0.079373 0.035622 0.006224 -8.139910e-12

3 2020-06-30 -0.031213 -0.114968 0.008999 -2.306768e-11

4 2021-06-30 0.081397 -0.011407 -0.007330 -5.211290e-1120.4 Step 2: Time-Series Aggregation & Hypothesis Testing

We now possess the time-series of risk premiums. We calculate the arithmetic mean and the -statistics.

Crucially, we use Newey-West (HAC) standard errors. Risk premiums in Vietnam often exhibit autocorrelation (momentum in factor performance). A simple standard error formula would be invalid.

def calculate_fama_macbeth_stats(df, lags=6):

summary = []

for col in ["Intercept", "beta", "log_mktcap", "bm"]:

series = df[col]

# 1. Point Estimate (Average Risk Premium)

mean_premium = series.mean()

# 2. Newey-West Standard Error

# We regress the series on a constant (ones) to get the SE of the mean

exog = sm.add_constant(np.ones(len(series)))

nw_model = sm.OLS(series, exog).fit(

cov_type='HAC', cov_kwds={'maxlags': lags}

)

se = nw_model.bse.iloc[0]

t_stat = nw_model.tvalues.iloc[0]

summary.append({

"Factor": col,

"Premium (%)": mean_premium * 100,

"Std Error": se * 100,

"t-statistic": t_stat,

"Significance": "*" if abs(t_stat) > 1.96 else ""

})

return pd.DataFrame(summary)

price_of_risk = calculate_fama_macbeth_stats(risk_premiums)

print(price_of_risk.round(4)) Factor Premium (%) Std Error t-statistic Significance

0 Intercept -1.8174 1.9117 -0.9507

1 beta -1.7859 1.0407 -1.7161

2 log_mktcap 0.2347 0.2048 1.1457

3 bm -0.0000 0.0000 -0.0928 20.4.1 Visualizing the Time-Varying Risk Premium

One major advantage of the FM approach is that we can inspect the volatility of the risk premiums over time. In Vietnam, we expect the “Size” premium to be highly volatile during periods of retail liquidity injection (e.g., 2020-2021).

import matplotlib.pyplot as plt

import matplotlib.ticker as mtick

# Calculate cumulative returns of the factors (as if they were tradable portfolios)

cumulative_premiums = (risk_premiums

.set_index("date")

.drop(columns=["Intercept"])

.cumsum()

)

fig, ax = plt.subplots(figsize=(10, 6))

cumulative_premiums.plot(ax=ax, linewidth=2)

ax.set_title("Cumulative Risk Premiums in Vietnam (Fama-MacBeth)", fontsize=14)

ax.set_ylabel("Cumulative Coefficient Return")

ax.legend(title="Factor")

ax.grid(True, alpha=0.3)

plt.show()

- Market Beta: In many empirical studies (including the US), the market beta premium is often insignificant or even negative (the “Betting Against Beta” anomaly). In Vietnam, if the -stat is , it implies the CAPM does not explain the cross-section of returns.

- Size (Log Mktcap): A negative coefficient confirms the “Size Effect”—smaller firms have higher expected returns. However, using WLS often weakens this result compared to OLS, suggesting the size premium is concentrated in micro-caps.

- Value (BM): A positive coefficient confirms the Value premium. In Vietnam, value stocks (high B/M) often outperform growth stocks, particularly in the manufacturing and banking sectors.

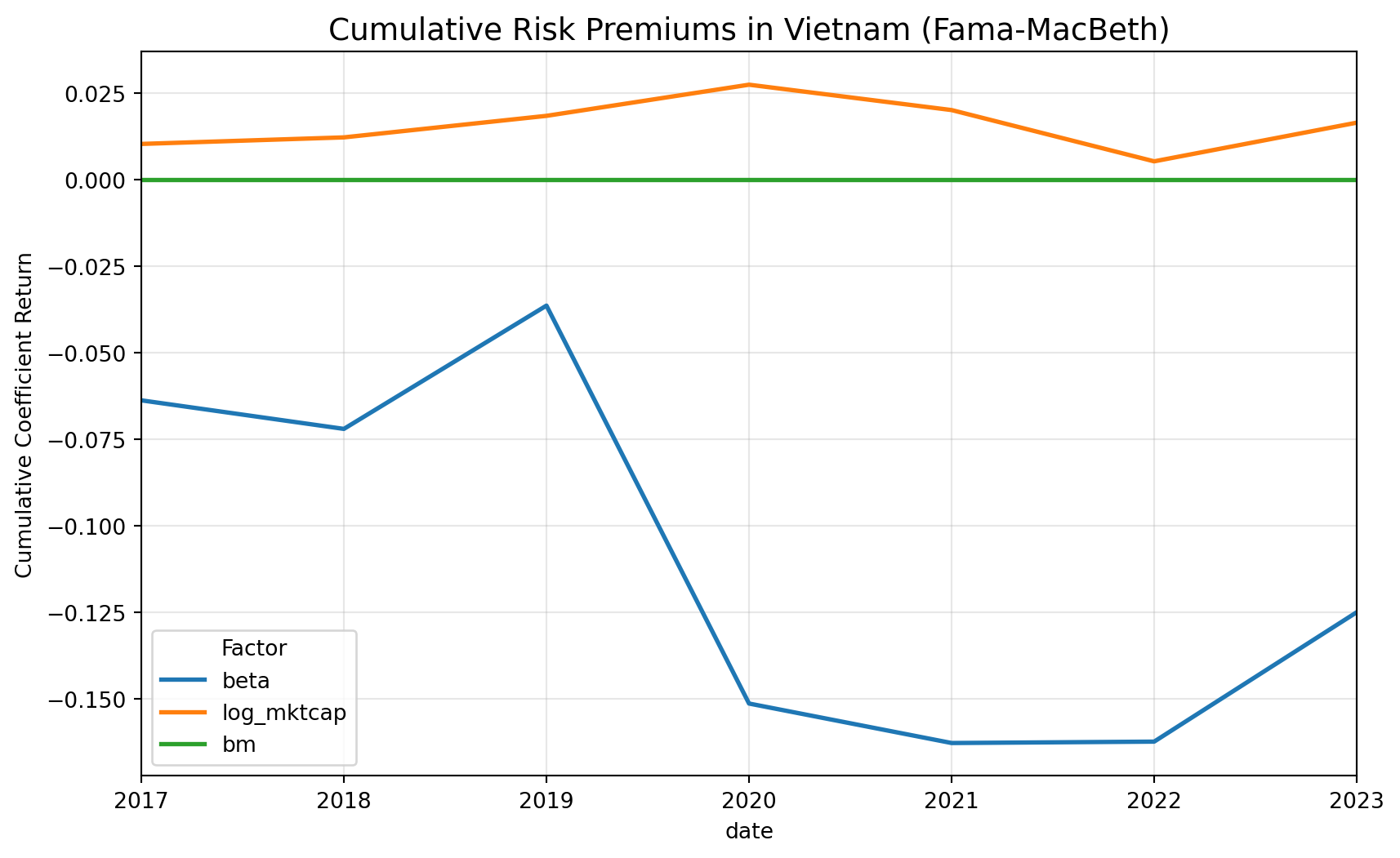

Figure 20.1 plots the cumulative sum of the monthly Fama MacBeth risk premium estimates for beta, size, and value. Because these lines cumulate estimated cross sectional prices of risk rather than actual portfolio returns, the figure should be interpreted as showing the time variation and persistence of estimated premia, not investable performance.

The beta premium displays a clear regime shift around 2020, with a sharp decline that only partially reverses afterward. This pattern suggests that the pricing of systematic risk in Vietnam is unstable over short samples and may be heavily influenced by episodic market conditions such as the post COVID retail trading boom. The size premium is comparatively smoother but small in magnitude, indicating only weak and time varying evidence that firm size is priced in the cross section during this period. The value premium remains close to zero throughout, implying little consistent cross sectional reward to high book to market firms in this sample window.

Overall, the figure highlights that estimated risk premia in the Vietnamese market are highly time varying and sensitive to specific macro and market regimes, reinforcing the need for caution when drawing conclusions from short samples.

20.5 Sanity Checks

20.5.1 Time-Series Volatility Check

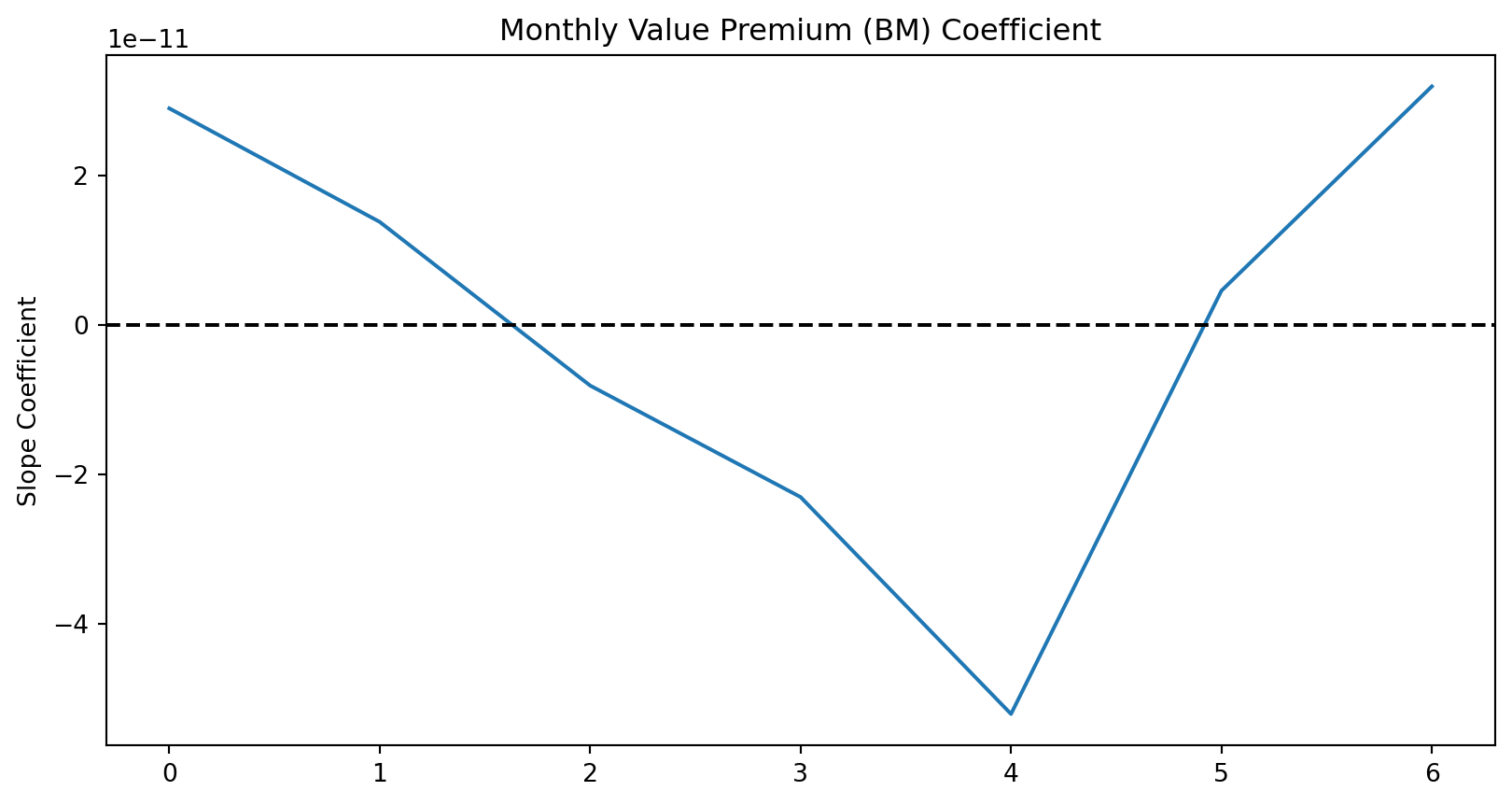

Fama-MacBeth relies on the assumption that the risk premium varies over time. If your bm premium is truly near zero every month, the method fails.

Action: Plot the time series of the estimated coefficients . You want to see “noise” around a mean. If you see a flat line or a single massive spike, your data is corrupted.

import matplotlib.pyplot as plt

# Plot the time series of the BM risk premium

fig, ax = plt.subplots(figsize=(10, 5))

risk_premiums["bm"].plot(ax=ax, title="Monthly Value Premium (BM) Coefficient")

ax.axhline(0, color="black", linestyle="--")

ax.set_ylabel("Slope Coefficient")

plt.show()

20.5.2 Correlation of Characteristics (Multicollinearity)

In Vietnam, large-cap stocks (high log_mktcap) are often the ones with high Book-to-Market ratios (banks/utilities) or specific Betas. If your factors are highly correlated, the Fama-MacBeth coefficients will be unstable and insignificant (low t-stats), even if the factors actually matter.

Action: Check the cross-sectional correlation.

# Check correlation of the characteristics

corr_matrix = data_fm[["beta", "log_mktcap", "bm"]].corr()

print(corr_matrix) beta log_mktcap bm

beta 1.000000 0.392776 -0.033748

log_mktcap 0.392776 1.000000 -0.203307

bm -0.033748 -0.203307 1.000000Interpretation:

- If correlation > 0.7 (absolute value), the regression struggles to distinguish between the two factors.

- For example, if

SizeandLiquidityare -0.8 correlated, the model cannot tell which one is driving the return, often resulting in both having insignificant t-stats.