import pandas as pd

import numpy as np

import sqlite3

from datetime import datetime

from itertools import product

from plotnine import *

from mizani.formatters import comma_format, percent_format

from scipy import stats18 Momentum Strategies

Momentum is one of the most robust and pervasive anomalies in financial economics. Stocks that have performed well over the past three to twelve months tend to continue performing well over the subsequent three to twelve months, and stocks that have performed poorly tend to continue underperforming. This pattern, first documented by Jegadeesh and Titman (1993), has been replicated across virtually every equity market, asset class, and time period examined, earning it a central place in the canon of empirical asset pricing.

In this chapter, we provide an implementation of momentum strategies following the methodology of Jegadeesh and Titman (1993). We construct momentum portfolios based on past cumulative returns, evaluate their performance across different formation and holding period combinations, and examine whether the momentum premium exists in the Vietnamese equity market..

18.1 Theoretical Background

18.1.1 The Momentum Effect

The momentum effect refers to the tendency of assets with high recent returns to continue generating high returns, and assets with low recent returns to continue generating low returns. More formally, if we define the cumulative return of stock \(i\) over the past \(J\) months as

\[ R_{i,t-J:t-1} = \prod_{s=t-J}^{t-1} (1 + r_{i,s}) - 1 \tag{18.1}\]

then momentum predicts a positive cross-sectional relationship between \(R_{i,t-J:t-1}\) and future returns \(r_{i,t}\). That is, stocks in the top decile of past returns (winners) should outperform stocks in the bottom decile (losers) in subsequent months.

The Jegadeesh and Titman (1993) framework parameterizes momentum strategies by two key dimensions:

- Formation period (\(J\)): The number of months over which past returns are computed to rank stocks. Typical values range from 3 to 12 months.

- Holding period (\(K\)): The number of months for which the momentum portfolios are held after formation. Typical values also range from 3 to 12 months.

A strategy is therefore characterized by the pair \((J, K)\). For example, a \((6, 6)\) strategy ranks stocks based on their cumulative returns over the past 6 months and holds the resulting portfolios for 6 months.

18.1.2 Overlapping Portfolios and Calendar-Time Returns

A critical implementation detail in Jegadeesh and Titman (1993) is the use of overlapping portfolios. In each month \(t\), a new set of portfolios is formed based on the most recent \(J\)-month returns. However, portfolios formed in months \(t-1\), \(t-2\), \(\ldots\), \(t-K+1\) are still within their holding periods and therefore remain active. The return of the momentum strategy in month \(t\) is thus the equally weighted average across all \(K\) active cohorts:

\[ r_{p,t} = \frac{1}{K} \sum_{k=0}^{K-1} r_{p,t}^{(t-k)} \tag{18.2}\]

where \(r_{p,t}^{(t-k)}\) denotes the return in month \(t\) of the portfolio formed in month \(t-k\). This overlapping portfolio approach serves two purposes. First, it reduces the impact of any single formation date on the strategy’s performance. Second, it produces a monthly return series that can be analyzed using standard time-series methods, even when the holding period \(K\) exceeds one month.

18.1.3 Theoretical Explanations

The academic literature offers two broad classes of explanations for the momentum effect.

- Behavioral explanations attribute momentum to systematic cognitive biases among investors. Daniel, Hirshleifer, and Subrahmanyam (1998) propose a model based on investor overconfidence and biased self-attribution: investors overweight private signals and attribute confirming outcomes to their own skill, leading to initial underreaction followed by delayed overreaction. Hong and Stein (1999) develop a model in which information diffuses gradually across heterogeneous investors, generating underreaction to firm-specific news. Barberis, Shleifer, and Vishny (1998) formalize a model combining conservatism bias (slow updating of beliefs in response to new evidence) and representativeness heuristic (extrapolation of recent trends).

- Risk-based explanations argue that momentum profits represent compensation for systematic risk that varies over time. Johnson (2002) show that momentum can arise in a rational framework if expected returns are stochastic and time-varying. Grundy and Martin (2001) document that momentum portfolios have substantial time-varying factor exposures, suggesting that at least part of the momentum premium reflects dynamic risk. However, standard risk models such as the Fama-French three-factor model have generally struggled to explain momentum returns, which motivated the development of explicit momentum factors such as the Winners-Minus-Losers (WML) factor in Carhart (1997).

18.1.4 Momentum in Emerging Markets

The behavior of momentum in emerging markets differs substantially from developed markets, and understanding these differences is essential for interpreting our Vietnamese market results.

Rouwenhorst (1998) provides early evidence that momentum profits exist in European markets. Chan, Hameed, and Tong (2000) extend the analysis to international equity markets and find that momentum profits are present in most developed markets but are weaker or absent in several Asian markets. Chui, Titman, and Wei (2010) offer a cultural explanation, documenting that momentum profits are positively related to a country’s degree of individualism as measured by Hofstede (2001). Countries with collectivist cultures, including many in East and Southeast Asia, tend to exhibit weaker momentum effects.

Several market microstructure features common in emerging markets may attenuate momentum:

- Trading band limits constrain daily price movements, potentially slowing the adjustment process that generates momentum. Vietnam’s HOSE imposes a \(\pm 7\%\) daily limit, while HNX allows \(\pm 10\%\).

- Lower liquidity and higher transaction costs can erode momentum profits, as documented by Lesmond, Schill, and Zhou (2004).

- Foreign ownership limits segment the investor base, potentially altering the information diffusion dynamics that underlie momentum.

- Shorter market history limits the statistical power available to detect the effect.

These considerations motivate our careful empirical analysis of whether, and to what extent, momentum manifests in Vietnamese equities.

18.2 Setting Up the Environment

We begin by loading the necessary Python packages. The core packages include pandas for data manipulation, numpy for numerical operations, and sqlite3 for database connectivity. We also import plotnine for creating publication-quality figures and scipy for statistical tests.

We connect to our SQLite database, which stores the cleaned datasets prepared previous chapters.

tidy_finance = sqlite3.connect(

database="data/tidy_finance_python.sqlite"

)18.3 Data Preparation

18.3.1 Loading Monthly Stock Returns

We load the monthly stock price data from our database. The prices_monthly table contains adjusted returns, market capitalizations, and other variables for all stocks listed on HOSE and HNX.

prices_monthly = pd.read_sql_query(

# can add "exchange" variable

sql="""

SELECT symbol, date, ret, ret_excess, mktcap, mktcap_lag, risk_free

FROM prices_monthly

""",

con=tidy_finance,

parse_dates={"date"}

).dropna()

print(f"Total monthly observations: {len(prices_monthly):,}")

print(f"Unique stocks: {prices_monthly['symbol'].nunique():,}")

print(f"Date range: {prices_monthly['date'].min().date()} "

f"to {prices_monthly['date'].max().date()}")Total monthly observations: 165,499

Unique stocks: 1,457

Date range: 2010-02-28 to 2023-12-3118.3.2 Inspecting the Data

Before proceeding with portfolio construction, we examine the key variables in our dataset. Table 18.1 presents the summary statistics for the main variables used in momentum portfolio construction.

summary_stats = (prices_monthly

[["ret", "ret_excess", "mktcap"]]

.describe()

.T

.round(4)

)

summary_stats| count | mean | std | min | 25% | 50% | 75% | max | |

|---|---|---|---|---|---|---|---|---|

| ret | 165499.0 | 0.0042 | 0.1862 | -0.9900 | -0.0703 | 0.0000 | 0.0553 | 12.7500 |

| ret_excess | 165499.0 | 0.0008 | 0.1862 | -0.9933 | -0.0736 | -0.0033 | 0.0519 | 12.7467 |

| mktcap | 165499.0 | 2183.1646 | 13983.9977 | 0.3536 | 60.3728 | 180.6224 | 660.0000 | 463886.6454 |

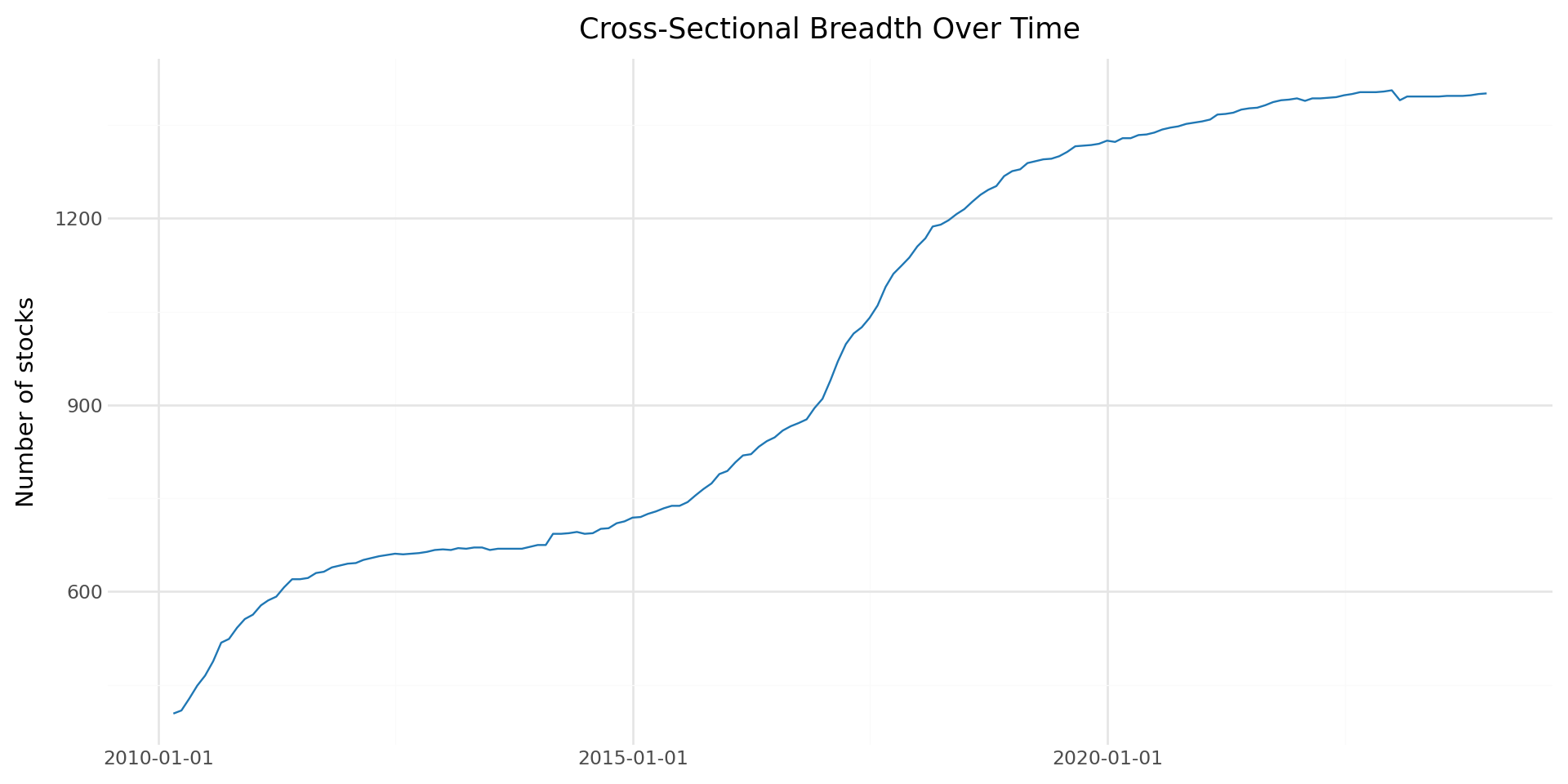

We also examine the cross-sectional distribution of stocks over time, which is important for understanding whether we have sufficient breadth for decile portfolio construction.

stock_counts = (prices_monthly

.groupby("date")["symbol"]

.nunique()

.reset_index()

.rename(columns={"symbol": "n_stocks"})

)

plot_stock_counts = (

ggplot(stock_counts, aes(x="date", y="n_stocks")) +

geom_line(color="#1f77b4") +

labs(

x="", y="Number of stocks",

title="Cross-Sectional Breadth Over Time"

) +

theme_minimal() +

theme(figure_size=(10, 5))

)

plot_stock_counts

18.3.3 Loading Factor Data

We also load the Fama-French factor returns for risk-adjusted performance evaluation. These factors were constructed in previous chapters.

factors_ff3_monthly = pd.read_sql_query(

sql="SELECT date, mkt_excess, smb, hml, risk_free FROM factors_ff3_monthly",

con=tidy_finance,

parse_dates={"date"}

)

print(f"Factor observations: {len(factors_ff3_monthly):,}")

print(f"Date range: {factors_ff3_monthly['date'].min().date()} "

f"to {factors_ff3_monthly['date'].max().date()}")Factor observations: 150

Date range: 2011-07-31 to 2023-12-3118.3.4 Data Quality Filters

Momentum strategies require continuous return histories for the formation period. We apply several filters to ensure data quality:

- Minimum price filter: We exclude penny stocks with prices below 1,000 VND, which are subject to extreme microstructure noise.

- Return availability: We require non-missing returns for the entire formation period.

- Market capitalization: We require positive lagged market capitalization for portfolio weighting.

# Filter for stocks with positive market cap and non-missing returns

prices_clean = (prices_monthly

.dropna(subset=["ret", "mktcap"])

.query("mktcap > 0")

.sort_values(["symbol", "date"])

.reset_index(drop=True)

)

print(f"Observations after filtering: {len(prices_clean):,}")

print(f"Stocks after filtering: {prices_clean['symbol'].nunique():,}")Observations after filtering: 165,499

Stocks after filtering: 1,45718.4 Momentum Portfolio Construction

18.4.1 Computing Formation Period Returns

The first step in constructing momentum portfolios is to compute cumulative returns over the formation period. For a formation period of \(J\) months, we compute the cumulative return for each stock \(i\) at the end of month \(t\) as specified in Equation 35.7.

We implement this using a rolling product of gross returns. A key detail is that we require non-missing returns for all \(J\) months in the formation window. If any monthly return is missing, the cumulative return is set to missing, and the stock is excluded from portfolio formation in that month.

def compute_formation_returns(data, J):

"""

Compute J-month cumulative returns for momentum portfolio formation.

Parameters

----------

data : pd.DataFrame

Panel data with columns 'symbol', 'date', 'ret'.

J : int

Formation period length in months (typically 3-12).

Returns

-------

pd.DataFrame

Original data augmented with 'cum_return' column.

"""

df = data.sort_values(["symbol", "date"]).copy()

# Compute rolling J-month cumulative return

# Using gross returns: (1+r1)*(1+r2)*...*(1+rJ) - 1

df["gross_ret"] = 1 + df["ret"]

df["cum_return"] = (

df.groupby("symbol")["gross_ret"]

.rolling(window=J, min_periods=J)

.apply(np.prod, raw=True)

.reset_index(level=0, drop=True)

- 1

)

df = df.drop(columns=["gross_ret"])

return dfLet us apply this function for our baseline case with \(J = 6\) months:

J = 6 # Formation period: 6 months

prices_with_cumret = compute_formation_returns(prices_clean, J)

# Check the result

print(f"Observations with valid {J}-month cumulative returns: "

f"{prices_with_cumret['cum_return'].notna().sum():,}")

print(f"\nCumulative return distribution:")

print(prices_with_cumret["cum_return"].describe().round(4))Observations with valid 6-month cumulative returns: 158,227

Cumulative return distribution:

count 158227.0000

mean 0.0171

std 0.5053

min -0.9999

25% -0.2196

50% -0.0400

75% 0.1404

max 35.7136

Name: cum_return, dtype: float6418.4.2 Assigning Momentum Decile Portfolios

Each month, we sort all stocks with valid cumulative returns into decile portfolios based on their past \(J\)-month performance. Portfolio 1 contains the bottom decile (losers) and portfolio 10 contains the top decile (winners).

def assign_momentum_portfolios(data, n_portfolios=10):

"""

Assign stocks to momentum portfolios based on formation-period returns.

For each cross-section (month), stocks are sorted into

n_portfolios quantile groups according to their cumulative return.

Portfolio 1 = lowest past returns (Losers)

Portfolio n_portfolios = highest past returns (Winners)

This implementation uses `groupby().transform()` rather than

`groupby().apply()` to preserve the original DataFrame structure

and avoid index mutation issues.

Parameters

----------

data : pd.DataFrame

Panel data containing at minimum:

- 'symbol' : stock identifier

- 'date' : formation month

- 'cum_return' : cumulative return over formation window

n_portfolios : int, optional

Number of portfolios to form (default = 10 for deciles).

Returns

-------

pd.DataFrame

Original data augmented with:

- 'momr' : integer momentum rank (1 to n_portfolios)

"""

# Drop observations without formation-period returns

# These cannot be ranked into portfolios

df = data.dropna(subset=["cum_return"]).copy()

def safe_qcut(x):

"""

Assign quantile portfolio labels within a single cross-section.

Uses pd.qcut to create approximately equal-sized portfolios.

If too few unique return values exist (which can happen in

small markets or illiquid samples), fall back to rank-based

binning to ensure portfolios are still formed.

"""

try:

# Standard quantile sorting

return pd.qcut(

x,

q=n_portfolios,

labels=range(1, n_portfolios + 1),

duplicates="drop" # prevents crash if quantile edges duplicate

)

except ValueError:

# Fallback: rank then evenly cut into bins

return pd.cut(

x.rank(method="first"),

bins=n_portfolios,

labels=range(1, n_portfolios + 1)

)

# Cross-sectional portfolio assignment:

# For each month, compute portfolio ranks based on cum_return.

# transform ensures:

# - original row order preserved

# - no index mutation

# - no loss of 'date' column

df["momr"] = (

df.groupby("date")["cum_return"]

.transform(safe_qcut)

.astype(int)

)

return dfportfolios = assign_momentum_portfolios(prices_with_cumret)

print(f"Stocks assigned to portfolios: {len(portfolios):,}")

print(f"\nPortfolio distribution (should be approximately equal):")

print(portfolios.groupby("momr")["symbol"].count().to_frame("count"))Stocks assigned to portfolios: 158,227

Portfolio distribution (should be approximately equal):

count

momr

1 15894

2 15815

3 16021

4 15759

5 15738

6 16568

7 15288

8 15582

9 15697

10 1586518.4.3 Defining Holding Period Dates

After forming portfolios at the end of month \(t\), we hold them from the beginning of month \(t+1\) through the end of month \(t+K\). This one-month gap between the formation period and the start of the holding period is standard in the literature and avoids the well-documented short-term reversal effect at the one-month horizon (Jegadeesh 1990).

K = 6 # Holding period: 6 months

portfolios_with_dates = portfolios.copy()

portfolios_with_dates = portfolios_with_dates.rename(

columns={"date": "form_date"}

)

# Define holding period start and end dates

portfolios_with_dates["hdate1"] = (

portfolios_with_dates["form_date"] + pd.offsets.MonthBegin(1)

)

portfolios_with_dates["hdate2"] = (

portfolios_with_dates["form_date"] + pd.offsets.MonthEnd(K)

)

print(portfolios_with_dates[

["symbol", "form_date", "cum_return", "momr", "hdate1", "hdate2"]

].head(10)) symbol form_date cum_return momr hdate1 hdate2

5 A32 2019-04-30 -0.061599 4 2019-05-01 2019-10-31

6 A32 2019-05-31 -0.213675 2 2019-06-01 2019-11-30

7 A32 2019-06-30 -0.308720 2 2019-07-01 2019-12-31

8 A32 2019-07-31 -0.249936 2 2019-08-01 2020-01-31

9 A32 2019-08-31 0.061986 8 2019-09-01 2020-02-29

10 A32 2019-09-30 0.030751 8 2019-10-01 2020-03-31

11 A32 2019-10-31 0.030751 8 2019-11-01 2020-04-30

12 A32 2019-11-30 0.032486 8 2019-12-01 2020-05-31

13 A32 2019-12-31 0.180073 9 2020-01-01 2020-06-30

14 A32 2020-01-31 0.412322 10 2020-02-01 2020-07-3118.4.4 Computing Portfolio Holding Period Returns

We now compute the returns of each portfolio during its holding period. For each stock-formation date combination, we merge in the actual returns realized during the holding window. This produces a panel of stock returns indexed by formation date, holding date, and momentum portfolio rank.

# Merge: for each portfolio assignment, get all returns during holding period

portfolio_returns = portfolios_with_dates.merge(

prices_clean[["symbol", "date", "ret"]].rename(

columns={"ret": "hret", "date": "hdate"}

),

on="symbol",

how="inner"

)

# Keep only returns within the holding period

portfolio_returns = portfolio_returns.query(

"hdate >= hdate1 and hdate <= hdate2"

)

print(f"Portfolio-holding period observations: {len(portfolio_returns):,}")Portfolio-holding period observations: 918,07218.4.5 Computing Equally Weighted Portfolio Returns

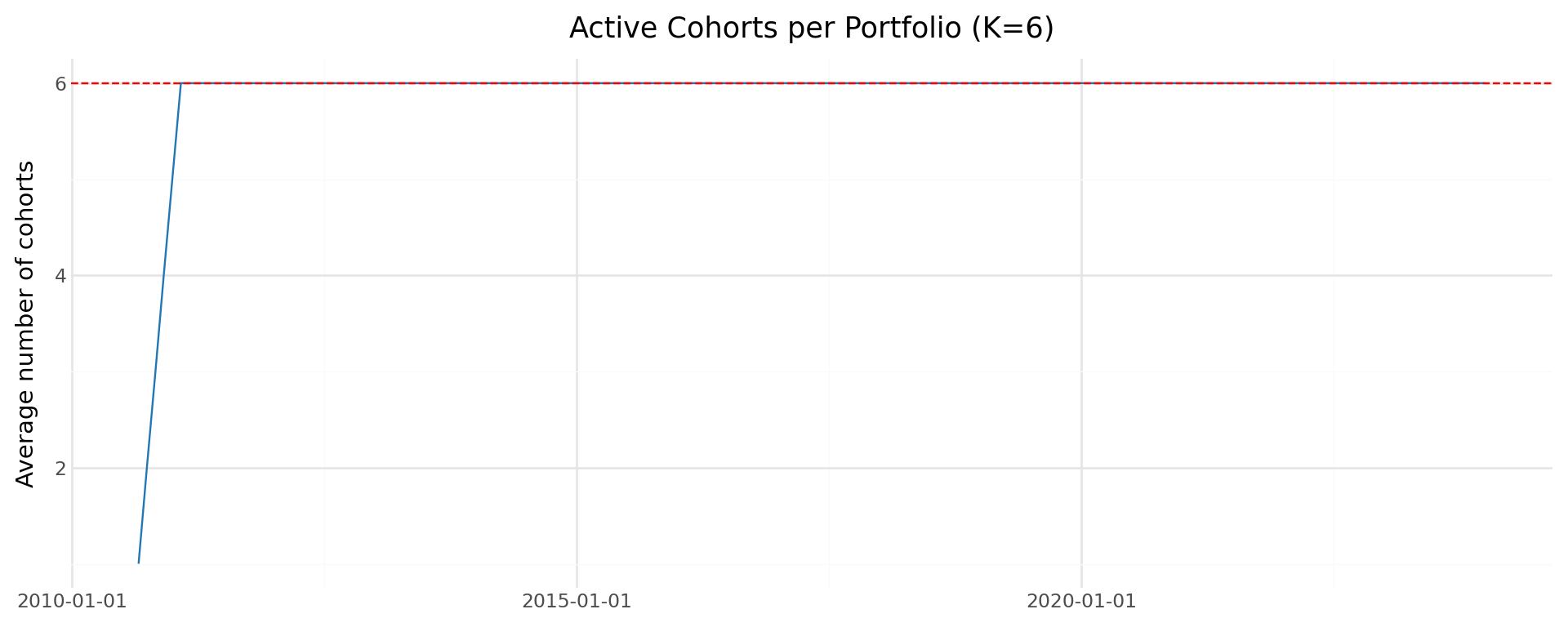

The Jegadeesh and Titman (1993) methodology uses equally weighted portfolios. For each holding month, each momentum decile has \(K\) active cohorts (one formed in each of the past \(K\) months). We first compute the equally weighted return within each cohort, then average across cohorts to get the final monthly portfolio return.

# Step 1: Average return within each cohort (form_date × momr × hdate)

cohort_returns = (portfolio_returns

.groupby(["hdate", "momr", "form_date"])

.agg(cohort_ret=("hret", "mean"))

.reset_index()

)

# Step 2: Average across cohorts for each momentum portfolio × month

ewret = (cohort_returns

.groupby(["hdate", "momr"])

.agg(

ewret=("cohort_ret", "mean"),

ewret_std=("cohort_ret", "std"),

n_cohorts=("cohort_ret", "count")

)

.reset_index()

.rename(columns={"hdate": "date"})

)

print(f"Monthly portfolio return observations: {len(ewret):,}")

print(f"Date range: {ewret['date'].min().date()} to {ewret['date'].max().date()}")Monthly portfolio return observations: 1,610

Date range: 2010-08-31 to 2023-12-31We should verify that we have the expected number of active cohorts per month. Once the strategy has been running for at least \(K\) months, each momentum decile should have exactly \(K\) active cohorts.

cohort_check = (ewret

.groupby("date")["n_cohorts"]

.mean()

.reset_index()

.rename(columns={"n_cohorts": "avg_cohorts"})

)

plot_cohorts = (

ggplot(cohort_check, aes(x="date", y="avg_cohorts")) +

geom_line(color="#1f77b4") +

geom_hline(yintercept=K, linetype="dashed", color="red") +

labs(

x="", y="Average number of cohorts",

title=f"Active Cohorts per Portfolio (K={K})"

) +

theme_minimal() +

theme(figure_size=(10, 4))

)

plot_cohorts

18.5 Baseline Results: J=6, K=6 Strategy

18.5.1 Summary Statistics by Momentum Decile

We now examine the average monthly returns for each momentum decile portfolio. Table 18.2 presents the mean, \(t\)-statistic, and \(p\)-value for each of the ten portfolios.

def compute_portfolio_stats(group):

"""Compute mean, t-stat, and p-value for a return series."""

n = len(group)

mean_ret = group.mean()

std_ret = group.std()

t_stat = mean_ret / (std_ret / np.sqrt(n)) if std_ret > 0 else np.nan

p_val = 2 * (1 - stats.t.cdf(abs(t_stat), df=n-1)) if not np.isnan(t_stat) else np.nan

return pd.Series({

"N": n,

"Mean (%)": mean_ret * 100,

"Std (%)": std_ret * 100,

"t-stat": t_stat,

"p-value": p_val

})

momentum_stats = (ewret

.groupby("momr")["ewret"]

.apply(compute_portfolio_stats)

.unstack()

.round(4)

)

momentum_stats| N | Mean (%) | Std (%) | t-stat | p-value | |

|---|---|---|---|---|---|

| momr | |||||

| 1 | 161.0 | 1.4190 | 6.5319 | 2.7565 | 0.0065 |

| 2 | 161.0 | 0.6602 | 5.9895 | 1.3985 | 0.1639 |

| 3 | 161.0 | 0.3658 | 5.5080 | 0.8427 | 0.4007 |

| 4 | 161.0 | 0.1623 | 5.0085 | 0.4112 | 0.6815 |

| 5 | 161.0 | 0.0111 | 4.7561 | 0.0297 | 0.9763 |

| 6 | 161.0 | 0.0408 | 4.6864 | 0.1104 | 0.9122 |

| 7 | 161.0 | -0.0674 | 4.8881 | -0.1749 | 0.8614 |

| 8 | 161.0 | -0.2066 | 4.9208 | -0.5329 | 0.5949 |

| 9 | 161.0 | -0.2228 | 5.3013 | -0.5332 | 0.5946 |

| 10 | 161.0 | -0.6812 | 5.7131 | -1.5130 | 0.1323 |

18.5.2 The Long-Short Momentum Portfolio

The key test of the momentum effect is whether the spread between winners and losers—the long-short momentum portfolio—generates statistically significant positive returns. We construct this spread portfolio by going long the top decile (portfolio 10) and short the bottom decile (portfolio 1).

# Pivot to wide format

ewret_wide = ewret.pivot(

index="date", columns="momr", values="ewret"

).reset_index()

ewret_wide.columns = ["date"] + [f"port{i}" for i in range(1, 11)]

# Compute long-short return

ewret_wide["winners"] = ewret_wide["port10"]

ewret_wide["losers"] = ewret_wide["port1"]

ewret_wide["long_short"] = ewret_wide["winners"] - ewret_wide["losers"]ls_stats = pd.DataFrame()

for col in ["winners", "losers", "long_short"]:

series = ewret_wide[col].dropna()

n = len(series)

mean_val = series.mean()

std_val = series.std()

t_val = mean_val / (std_val / np.sqrt(n))

p_val = 2 * (1 - stats.t.cdf(abs(t_val), df=n-1))

ls_stats[col] = [n, mean_val * 100, std_val * 100, t_val, p_val]

ls_stats.index = ["N", "Mean (%)", "Std (%)", "t-stat", "p-value"]

ls_stats.columns = ["Winners", "Losers", "Long-Short"]

ls_stats = ls_stats.round(4)

ls_stats| Winners | Losers | Long-Short | |

|---|---|---|---|

| N | 161.0000 | 161.0000 | 161.0000 |

| Mean (%) | -0.6812 | 1.4190 | -2.1002 |

| Std (%) | 5.7131 | 6.5319 | 4.8969 |

| t-stat | -1.5130 | 2.7565 | -5.4420 |

| p-value | 0.1323 | 0.0065 | 0.0000 |

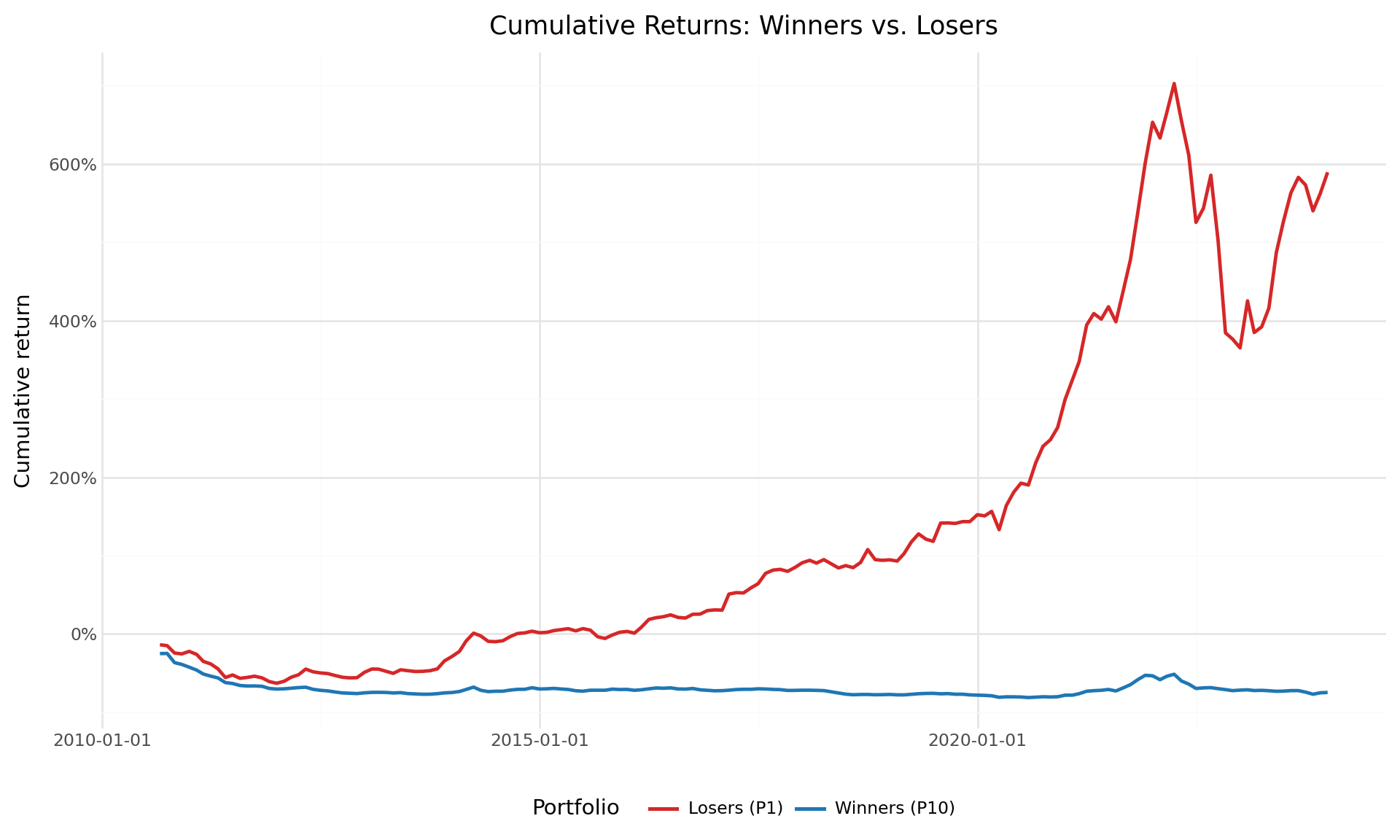

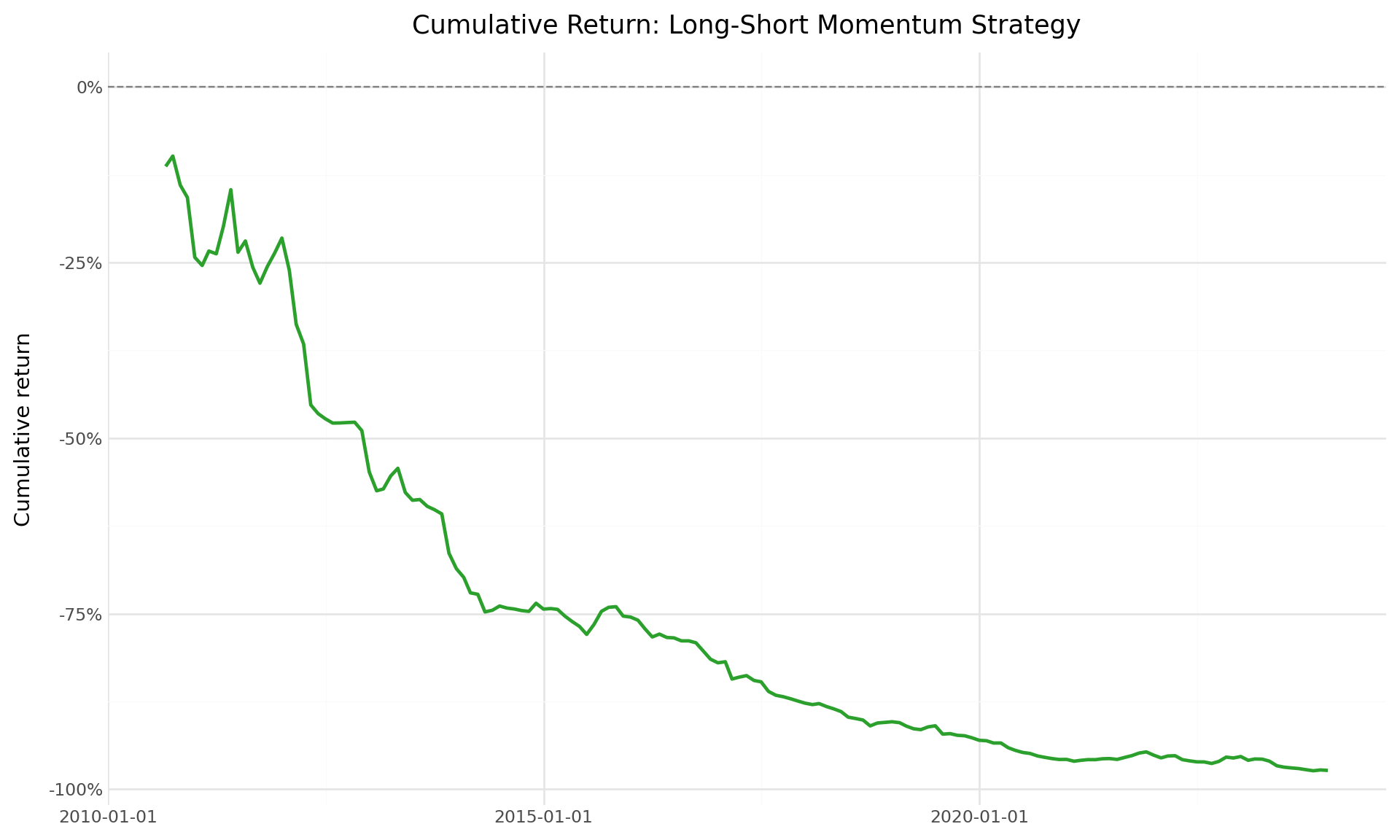

18.5.3 Cumulative Returns

The time-series evolution of cumulative returns provides visual evidence of the momentum strategy’s performance. Figure 18.3 shows the cumulative returns of the winner and loser portfolios, while Figure 18.4 shows the cumulative return of the long-short momentum strategy.

# Compute cumulative returns

ewret_wide = ewret_wide.sort_values("date").reset_index(drop=True)

for col in ["winners", "losers", "long_short"]:

ewret_wide[f"cumret_{col}"] = (1 + ewret_wide[col]).cumprod() - 1cumret_plot_data = (ewret_wide

[["date", "cumret_winners", "cumret_losers"]]

.melt(id_vars="date", var_name="portfolio", value_name="cumret")

)

cumret_plot_data["portfolio"] = cumret_plot_data["portfolio"].map({

"cumret_winners": "Winners (P10)",

"cumret_losers": "Losers (P1)"

})

plot_cumret = (

ggplot(cumret_plot_data,

aes(x="date", y="cumret", color="portfolio")) +

geom_line(size=1) +

scale_y_continuous(labels=percent_format()) +

scale_color_manual(values=["#d62728", "#1f77b4"]) +

labs(

x="", y="Cumulative return",

color="Portfolio",

title="Cumulative Returns: Winners vs. Losers"

) +

theme_minimal() +

theme(

figure_size=(10, 6),

legend_position="bottom"

)

)

plot_cumret

plot_ls = (

ggplot(ewret_wide, aes(x="date", y="cumret_long_short")) +

geom_line(size=1, color="#2ca02c") +

geom_hline(yintercept=0, linetype="dashed", color="gray") +

scale_y_continuous(labels=percent_format()) +

labs(

x="", y="Cumulative return",

title="Cumulative Return: Long-Short Momentum Strategy"

) +

theme_minimal() +

theme(figure_size=(10, 6))

)

plot_ls

18.5.4 Monthly Return Distribution

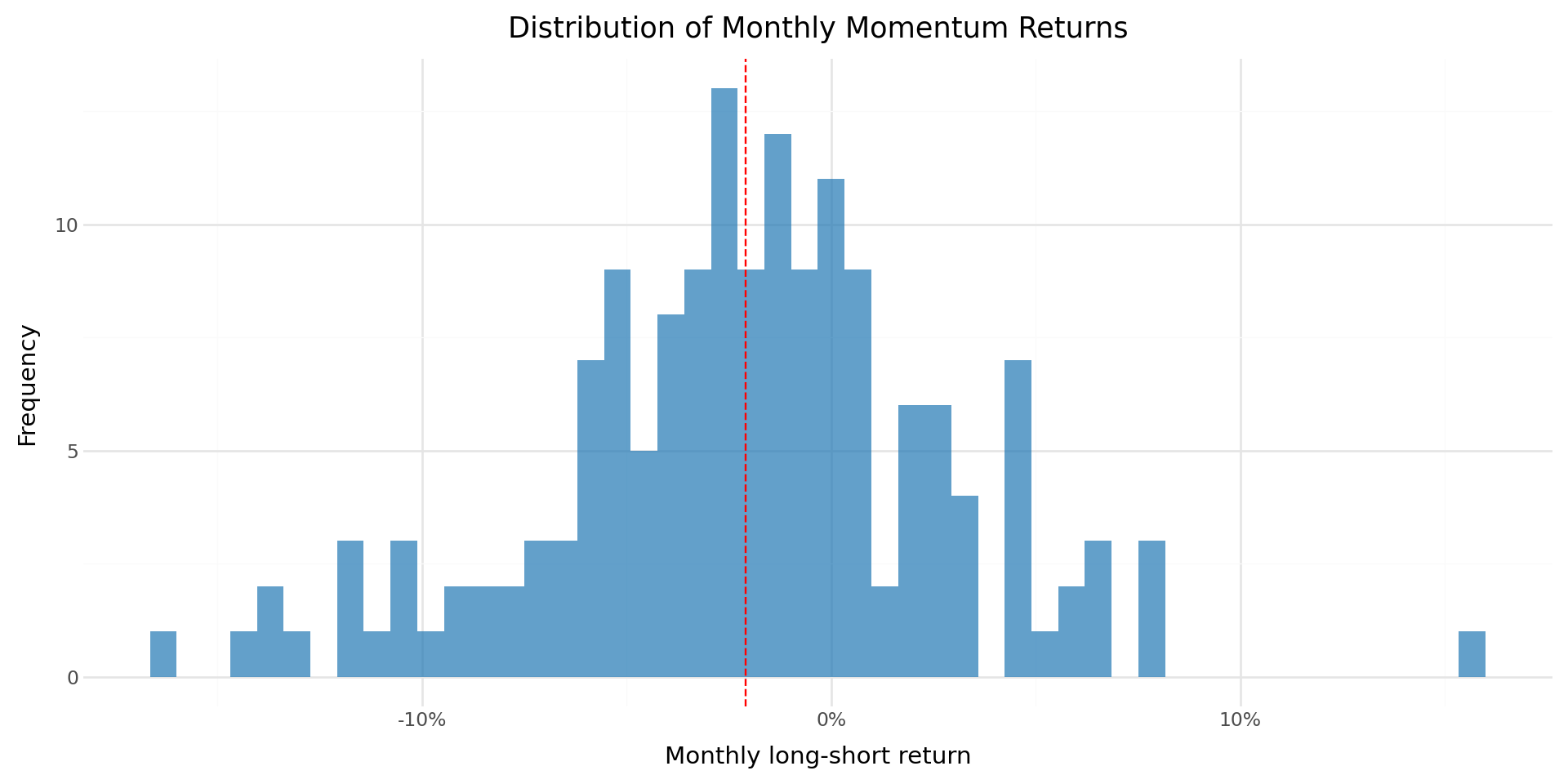

Beyond the mean, the full distribution of monthly long-short returns provides insight into the risk profile of the momentum strategy. Figure 39.1 shows the histogram of monthly returns.

mean_ls = ewret_wide["long_short"].mean()

plot_dist = (

ggplot(ewret_wide, aes(x="long_short")) +

geom_histogram(bins=50, fill="#1f77b4", alpha=0.7) +

geom_vline(xintercept=mean_ls, linetype="dashed", color="red") +

scale_x_continuous(labels=percent_format()) +

labs(

x="Monthly long-short return",

y="Frequency",

title="Distribution of Monthly Momentum Returns"

) +

theme_minimal() +

theme(figure_size=(10, 5))

)

plot_dist

18.6 Extending to Multiple Formation and Holding Periods

18.6.1 The J × K Grid

Jegadeesh and Titman (1993) evaluate momentum strategies across a comprehensive grid of formation periods \(J \in \{3, 6, 9, 12\}\) and holding periods \(K \in \{3, 6, 9, 12\}\). This produces 16 different strategy specifications, allowing us to assess the robustness of the momentum effect across different horizons.

We now implement a function that computes the full momentum strategy for any given \((J, K)\) pair, wrapping the steps developed above into a single reusable pipeline.

from joblib import Parallel, delayed

import time

def momentum_strategy(data, J, K, n_portfolios=10):

"""

Implement the full Jegadeesh-Titman momentum strategy.

Parameters

----------

data : pd.DataFrame

Panel of stock returns with columns: symbol, date, ret.

J : int

Formation period in months.

K : int

Holding period in months.

n_portfolios : int

Number of portfolios (default: 10 for deciles).

Returns

-------

pd.DataFrame

Monthly returns for each momentum portfolio and the long-short spread.

"""

# Step 1: Compute formation period cumulative returns

df = data.sort_values(["symbol", "date"]).copy()

df["gross_ret"] = 1 + df["ret"]

df["cum_return"] = (

df.groupby("symbol")["gross_ret"]

.rolling(window=J, min_periods=J)

.apply(np.prod, raw=True)

.reset_index(level=0, drop=True)

- 1

)

df = df.drop(columns=["gross_ret"]).dropna(subset=["cum_return"])

# Step 2: Assign to momentum portfolios using transform

df["momr"] = df.groupby("date", observed=True)["cum_return"].transform(

lambda x: pd.qcut(

x,

q=n_portfolios,

labels=range(1, n_portfolios + 1),

duplicates="drop"

)

).astype('Int64')

# If any NaNs in momr, fill with rank-based assignment

mask = df["momr"].isna()

if mask.any():

df.loc[mask, "momr"] = df.loc[mask].groupby("date")["cum_return"].transform(

lambda x: pd.qcut(

x.rank(method="first"),

q=min(n_portfolios, len(x.unique())),

labels=False,

duplicates="drop"

)

).astype('Int64') + 1

# Step 3: Define holding period dates

df = df.rename(columns={"date": "form_date"})

df["hdate1"] = df["form_date"] + pd.offsets.MonthBegin(1)

df["hdate2"] = df["form_date"] + pd.offsets.MonthEnd(K)

# Step 4: Merge with holding period returns

port_ret = df[["symbol", "form_date", "momr", "hdate1", "hdate2"]].merge(

data[["symbol", "date", "ret"]].rename(

columns={"ret": "hret", "date": "hdate"}

),

on="symbol",

how="inner"

)

# Use boolean indexing

port_ret = port_ret[

(port_ret["hdate"] >= port_ret["hdate1"]) &

(port_ret["hdate"] <= port_ret["hdate2"])

]

# Step 5: Compute equally weighted returns (two-stage averaging)

cohort_ret = (port_ret

.groupby(["hdate", "momr", "form_date"])

.agg(cohort_ret=("hret", "mean"))

.reset_index()

)

monthly_ret = (cohort_ret

.groupby(["hdate", "momr"])

.agg(ewret=("cohort_ret", "mean"))

.reset_index()

.rename(columns={"hdate": "date"})

)

# Step 6: Compute long-short spread

wide = monthly_ret.pivot(

index="date", columns="momr", values="ewret"

).reset_index()

# Handle variable number of portfolios

n_cols = len(wide.columns) - 1

wide.columns = ["date"] + [f"port{i}" for i in range(1, n_cols + 1)]

wide["winners"] = wide[f"port{n_cols}"]

wide["losers"] = wide["port1"]

wide["long_short"] = wide["winners"] - wide["losers"]

return monthly_ret, wide18.6.2 Running the Full Grid

We now run the momentum strategy for all 16 \((J, K)\) combinations. This is computationally intensive, so we store the key summary statistics for each specification.

18.6.2.1 Sequential Calculation

J_values = [3, 6, 9, 12]

K_values = [3, 6, 9, 12]

results_grid = []

for J_val, K_val in product(J_values, K_values):

print(f"Computing J={J_val}, K={K_val}...", end=" ")

try:

_, wide_result = momentum_strategy(prices_clean, J_val, K_val)

for portfolio_name in ["winners", "losers", "long_short"]:

series = wide_result[portfolio_name].dropna()

n = len(series)

mean_ret = series.mean()

std_ret = series.std()

t_stat = mean_ret / (std_ret / np.sqrt(n)) if std_ret > 0 else np.nan

p_val = (2 * (1 - stats.t.cdf(abs(t_stat), df=n-1))

if not np.isnan(t_stat) else np.nan)

results_grid.append({

"J": J_val,

"K": K_val,

"portfolio": portfolio_name,

"n_months": n,

"mean_ret": mean_ret,

"std_ret": std_ret,

"t_stat": t_stat,

"p_value": p_val

})

print("Done.")

except Exception as e:

print(f"Error: {e}")

results_df = pd.DataFrame(results_grid)18.6.2.2 Parallel Calculation

def compute_single_strategy(data, J, K):

"""

Compute statistics for a single (J, K) strategy.

Returns a list of result dicts, one per portfolio.

"""

try:

_, wide_result = momentum_strategy(data, J, K)

results = []

for portfolio_name in ["winners", "losers", "long_short"]:

series = wide_result[portfolio_name].dropna()

n = len(series)

mean_ret = series.mean()

std_ret = series.std()

t_stat = mean_ret / (std_ret / np.sqrt(n)) if std_ret > 0 else np.nan

p_val = (2 * (1 - stats.t.cdf(abs(t_stat), df=n-1))

if not np.isnan(t_stat) else np.nan)

results.append({

"J": J,

"K": K,

"portfolio": portfolio_name,

"n_months": n,

"mean_ret": mean_ret,

"std_ret": std_ret,

"t_stat": t_stat,

"p_value": p_val

})

return results

except Exception as e:

print(f"Error in J={J}, K={K}: {e}")

return []J_values = [3, 6, 9, 12]

K_values = [3, 6, 9, 12]

# Create list of (J, K) pairs

params = list(product(J_values, K_values))

print(f"Running {len(params)} momentum strategies in parallel with 4 cores...")

start_time = time.time()

# Parallel execution with 4 workers

results_list = Parallel(n_jobs=4, verbose=10)(

delayed(compute_single_strategy)(prices_clean, J, K)

for J, K in params

)

# Flatten results

results_grid = [item for sublist in results_list for item in sublist]

results_df = pd.DataFrame(results_grid)

elapsed = time.time() - start_time

print(f"\nCompleted in {elapsed:.2f} seconds")Running 16 momentum strategies in parallel with 4 cores...[Parallel(n_jobs=4)]: Using backend LokyBackend with 4 concurrent workers.

[Parallel(n_jobs=4)]: Done 5 tasks | elapsed: 8.4s

[Parallel(n_jobs=4)]: Done 11 out of 16 | elapsed: 14.4s remaining: 6.5s

[Parallel(n_jobs=4)]: Done 13 out of 16 | elapsed: 18.7s remaining: 4.3s

Completed in 19.68 seconds[Parallel(n_jobs=4)]: Done 16 out of 16 | elapsed: 19.6s finished# Summary statistics

print("\nResults Summary by Formation Period:")

print(results_df.groupby("J").agg({

"mean_ret": "mean",

"std_ret": "mean",

"t_stat": ["mean", lambda x: (x.abs() > 1.96).sum()],

"n_months": "first"

}).round(6))

Results Summary by Formation Period:

mean_ret std_ret t_stat n_months

mean mean mean <lambda_0> first

J

6 -0.004661 0.055672 -1.517507 9 161

9 -0.003265 0.056520 -1.071904 9 158

12 -0.002759 0.058194 -0.931273 9 15518.6.3 Winners Portfolio Returns

Table 18.4 presents the average monthly returns of the winner portfolio (portfolio 10) across all \((J, K)\) combinations.

winners_grid = (results_df

.query("portfolio == 'winners'")

.assign(

display=lambda x: (

x["mean_ret"].apply(lambda v: f"{v*100:.2f}") +

"\n(" + x["t_stat"].apply(lambda v: f"{v:.2f}") + ")"

)

)

.pivot(index="J", columns="K", values="display")

)

winners_grid.columns = [f"K={k}" for k in winners_grid.columns]

winners_grid.index = [f"J={j}" for j in winners_grid.index]

winners_grid| K=3 | K=6 | K=9 | K=12 | |

|---|---|---|---|---|

| J=6 | -1.18\n(-2.65) | -0.68\n(-1.51) | -0.55\n(-1.23) | -0.39\n(-0.87) |

| J=9 | -1.00\n(-2.36) | -0.51\n(-1.22) | -0.28\n(-0.68) | -0.16\n(-0.39) |

| J=12 | -0.88\n(-2.09) | -0.39\n(-0.91) | -0.24\n(-0.56) | -0.14\n(-0.34) |

18.6.4 Losers Portfolio Returns

Table 18.5 presents the corresponding results for the loser portfolio.

losers_grid = (results_df

.query("portfolio == 'losers'")

.assign(

display=lambda x: (

x["mean_ret"].apply(lambda v: f"{v*100:.2f}") +

"\n(" + x["t_stat"].apply(lambda v: f"{v:.2f}") + ")"

)

)

.pivot(index="J", columns="K", values="display")

)

losers_grid.columns = [f"K={k}" for k in losers_grid.columns]

losers_grid.index = [f"J={j}" for j in losers_grid.index]

losers_grid| K=3 | K=6 | K=9 | K=12 | |

|---|---|---|---|---|

| J=6 | 1.87\n(3.49) | 1.42\n(2.76) | 1.10\n(2.19) | 0.99\n(1.99) |

| J=9 | 1.94\n(3.51) | 1.38\n(2.56) | 1.21\n(2.31) | 1.15\n(2.22) |

| J=12 | 1.57\n(2.71) | 1.29\n(2.28) | 1.19\n(2.13) | 1.15\n(2.09) |

18.6.5 Long-Short Momentum Returns

Table 18.6 presents the most important results: the average monthly returns of the long-short momentum portfolio across all specifications.

ls_grid = (results_df

.query("portfolio == 'long_short'")

.assign(

display=lambda x: (

x["mean_ret"].apply(lambda v: f"{v*100:.2f}") +

"\n(" + x["t_stat"].apply(lambda v: f"{v:.2f}") + ")"

)

)

.pivot(index="J", columns="K", values="display")

)

ls_grid.columns = [f"K={k}" for k in ls_grid.columns]

ls_grid.index = [f"J={j}" for j in ls_grid.index]

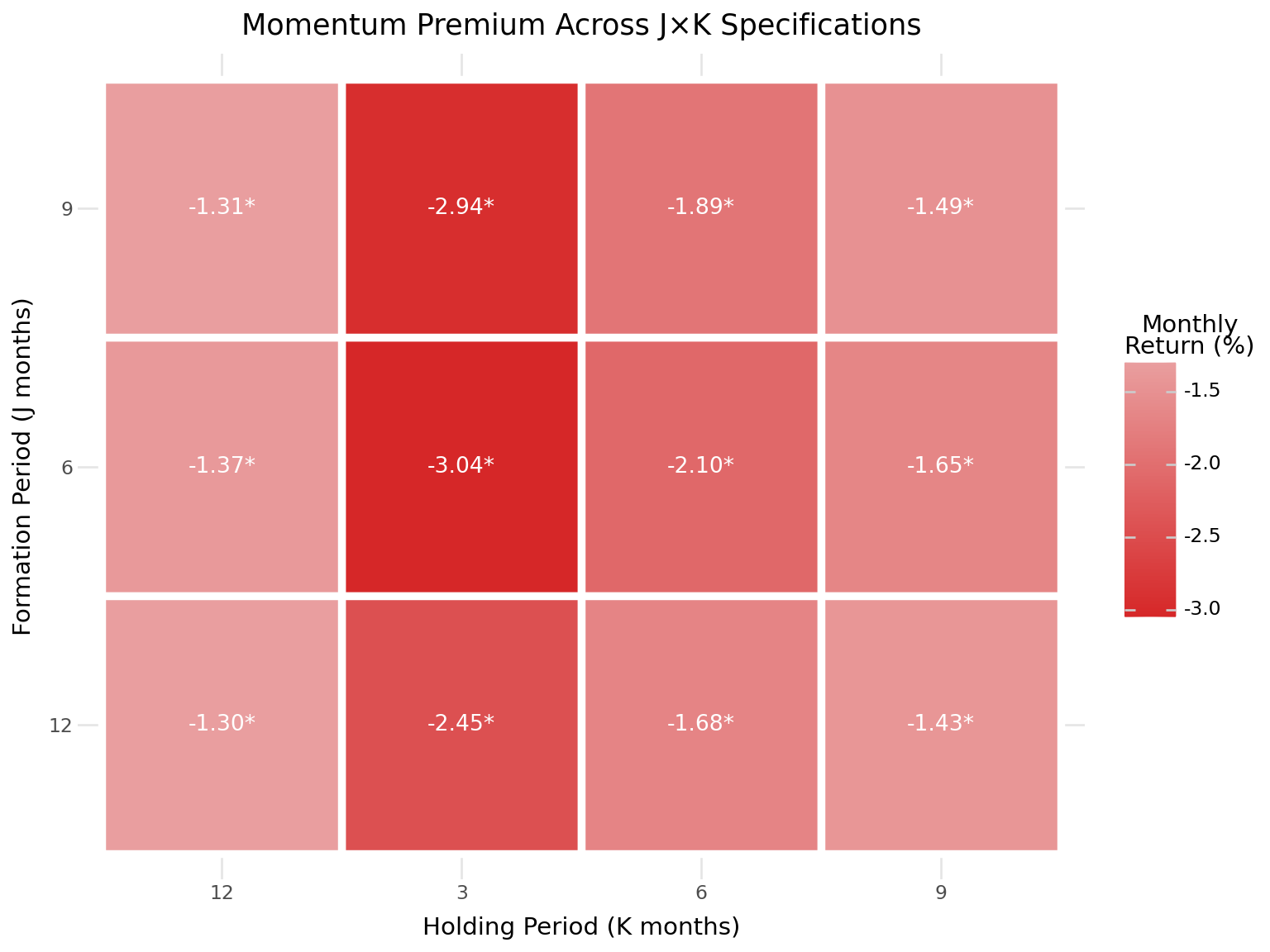

ls_grid| K=3 | K=6 | K=9 | K=12 | |

|---|---|---|---|---|

| J=6 | -3.04\n(-7.38) | -2.10\n(-5.44) | -1.65\n(-4.94) | -1.37\n(-4.61) |

| J=9 | -2.94\n(-6.41) | -1.89\n(-4.55) | -1.49\n(-3.98) | -1.31\n(-3.87) |

| J=12 | -2.45\n(-5.42) | -1.68\n(-3.92) | -1.43\n(-3.60) | -1.30\n(-3.55) |

18.6.6 Visualizing the Momentum Premium Across Specifications

Figure 18.6 provides a visual summary of the long-short momentum premium across all \((J, K)\) combinations.

ls_heatmap_data = (results_df

.query("portfolio == 'long_short'")

.assign(

mean_pct=lambda x: x["mean_ret"] * 100,

significant=lambda x: x["p_value"] < 0.05,

label=lambda x: x.apply(

lambda row: f"{row['mean_ret']*100:.2f}{'*' if row['p_value'] < 0.05 else ''}",

axis=1

)

)

)

plot_heatmap = (

ggplot(ls_heatmap_data,

aes(x="K.astype(str)", y="J.astype(str)", fill="mean_pct")) +

geom_tile(color="white", size=2) +

geom_text(aes(label="label"), size=10, color="white") +

scale_fill_gradient2(

low="#d62728", mid="#f7f7f7", high="#1f77b4", midpoint=0,

name="Monthly\nReturn (%)"

) +

labs(

x="Holding Period (K months)",

y="Formation Period (J months)",

title="Momentum Premium Across J×K Specifications"

) +

theme_minimal() +

theme(figure_size=(8, 6))

)

plot_heatmap

18.7 Risk-Adjusted Performance

18.7.1 CAPM Alpha

A natural question is whether the momentum premium is explained by exposure to the market factor. We estimate the CAPM alpha of the long-short momentum portfolio by regressing its returns on the market excess return:

\[ r_{\text{WML},t} = \alpha + \beta \cdot r_{\text{MKT},t} + \epsilon_t \tag{18.3}\]

# Merge momentum returns with factor data (baseline J=6, K=6)

ewret_factors = (ewret_wide

[["date", "winners", "losers", "long_short"]]

.merge(factors_ff3_monthly, on="date", how="inner")

)

# CAPM regression for long-short portfolio

from statsmodels.formula.api import ols as ols_formula

import statsmodels.api as sm

X_capm = sm.add_constant(ewret_factors["mkt_excess"])

y_ls = ewret_factors["long_short"]

capm_model = sm.OLS(y_ls, X_capm).fit(cov_type="HAC", cov_kwds={"maxlags": 6})

print("CAPM Regression: Long-Short Momentum Returns")

print("=" * 60)

print(f"Alpha (monthly): {capm_model.params['const']*100:.4f}% "

f"(t={capm_model.tvalues['const']:.2f})")

print(f"Market Beta: {capm_model.params['mkt_excess']:.4f} "

f"(t={capm_model.tvalues['mkt_excess']:.2f})")

print(f"R-squared: {capm_model.rsquared:.4f}")

print(f"N observations: {capm_model.nobs:.0f}")CAPM Regression: Long-Short Momentum Returns

============================================================

Alpha (monthly): -2.2703% (t=-5.05)

Market Beta: -0.1779 (t=-1.75)

R-squared: 0.0470

N observations: 15018.7.2 Fama-French Three-Factor Alpha

We extend the risk adjustment to the Fama-French three-factor model, which includes the size (SMB) and value (HML) factors in addition to the market factor:

\[ r_{\text{WML},t} = \alpha + \beta_1 \cdot r_{\text{MKT},t} + \beta_2 \cdot \text{SMB}_t + \beta_3 \cdot \text{HML}_t + \epsilon_t \tag{18.4}\]

X_ff3 = sm.add_constant(

ewret_factors[["mkt_excess", "smb", "hml"]]

)

y_ls = ewret_factors["long_short"]

ff3_model = sm.OLS(y_ls, X_ff3).fit(cov_type="HAC", cov_kwds={"maxlags": 6})

# Display results as a clean table

ff3_results = pd.DataFrame({

"Coefficient": ff3_model.params,

"Std Error": ff3_model.bse,

"t-stat": ff3_model.tvalues,

"p-value": ff3_model.pvalues

}).round(4)

ff3_results.index = ["Alpha", "MKT", "SMB", "HML"]

ff3_results| Coefficient | Std Error | t-stat | p-value | |

|---|---|---|---|---|

| Alpha | -0.0234 | 0.0041 | -5.7189 | 0.0000 |

| MKT | -0.1269 | 0.1558 | -0.8145 | 0.4154 |

| SMB | 0.1123 | 0.1882 | 0.5969 | 0.5506 |

| HML | 0.0716 | 0.1414 | 0.5065 | 0.6125 |

print(f"\nR-squared: {ff3_model.rsquared:.4f}")

print(f"Adjusted R-squared: {ff3_model.rsquared_adj:.4f}")

print(f"Alpha (annualized): {ff3_model.params['const'] * 12 * 100:.2f}%")

R-squared: 0.0553

Adjusted R-squared: 0.0359

Alpha (annualized): -28.02%18.7.3 Interpretation of Risk Exposures

The factor loadings from the three-factor regression reveal the risk characteristics of the momentum strategy in the Vietnamese market. Several patterns are commonly observed:

Market beta: Momentum portfolios typically have moderate market exposure. In the U.S., Grundy and Martin (2001) document that the market beta of the long-short portfolio is close to zero on average but highly time-varying, spiking during market reversals.

Size exposure (SMB): Momentum strategies often load positively on the size factor, reflecting the tendency for smaller stocks to exhibit stronger momentum patterns.

Value exposure (HML): The long-short momentum portfolio typically loads negatively on HML, indicating that winners tend to be growth stocks while losers tend to be value stocks. This creates a natural tension between momentum and value strategies.

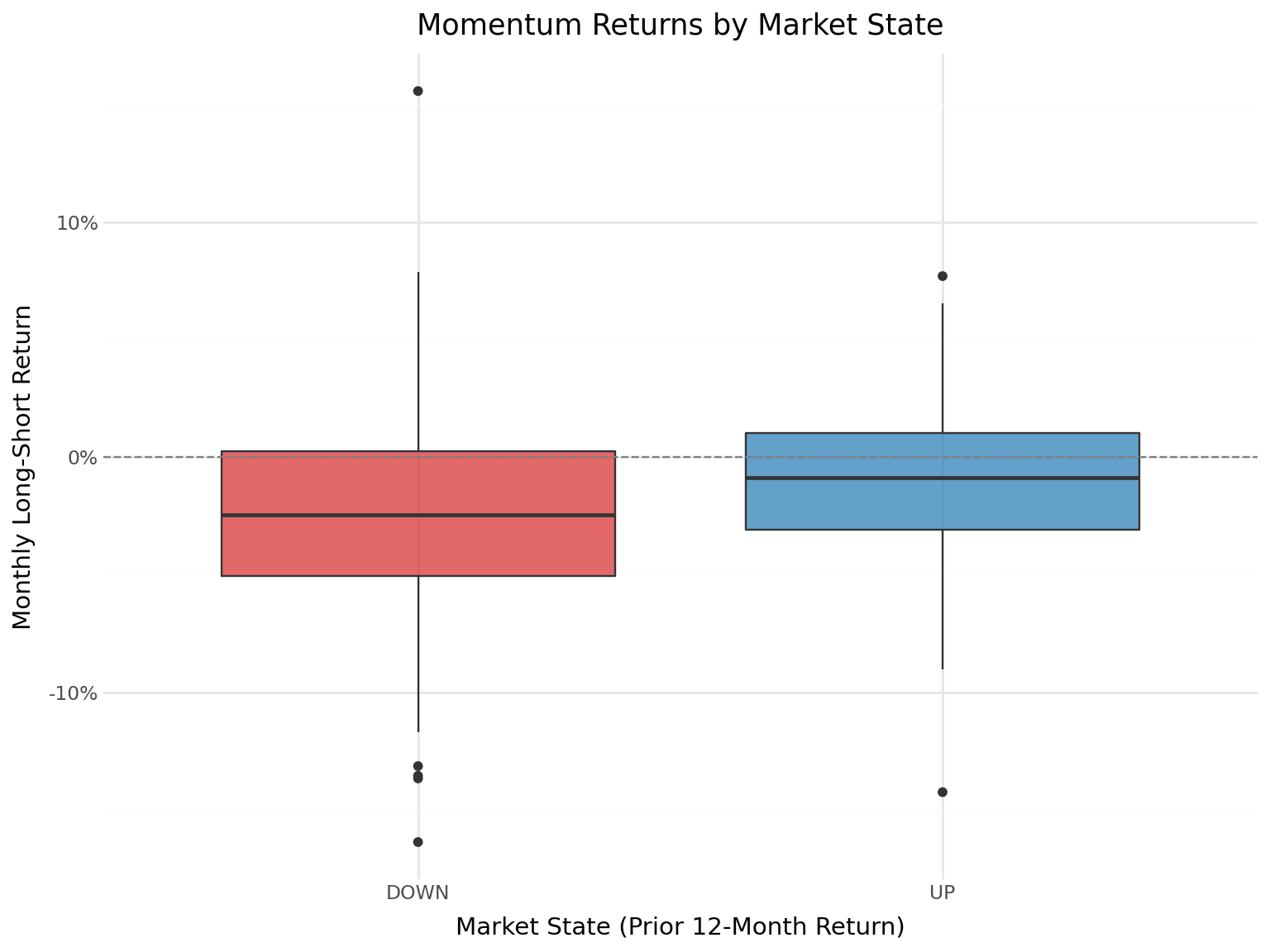

18.8 Momentum and Market States

18.8.1 Conditional Performance

An important finding in the momentum literature is that momentum profits vary with market conditions. Cooper, Gutierrez Jr, and Hameed (2004) document that momentum strategies perform well following market gains (UP markets) but experience severe losses following market declines (DOWN markets). This asymmetry is particularly relevant for emerging markets, which experience more extreme market states.

We define market states based on the cumulative market return over the prior 12 months:

\[ \text{Market State}_t = \begin{cases} \text{UP} & \text{if } \prod_{s=t-12}^{t-1}(1 + r_{m,s}) - 1 > 0 \\ \text{DOWN} & \text{otherwise} \end{cases} \tag{18.5}\]

# Compute 12-month lagged market return

market_returns = factors_ff3_monthly[["date", "mkt_excess"]].copy()

market_returns = market_returns.sort_values("date")

market_returns["mkt_cum_12m"] = (

(1 + market_returns["mkt_excess"])

.rolling(window=12, min_periods=12)

.apply(np.prod, raw=True)

- 1

)

market_returns["market_state"] = np.where(

market_returns["mkt_cum_12m"] > 0, "UP", "DOWN"

)

# Merge with momentum returns

ewret_states = ewret_wide[["date", "long_short"]].merge(

market_returns[["date", "market_state"]], on="date", how="inner"

).dropna()state_stats = []

for state in ["UP", "DOWN"]:

subset = ewret_states.query(f"market_state == '{state}'")["long_short"]

n = len(subset)

mean_ret = subset.mean()

std_ret = subset.std()

t_stat = mean_ret / (std_ret / np.sqrt(n)) if std_ret > 0 else np.nan

p_val = 2 * (1 - stats.t.cdf(abs(t_stat), df=n-1)) if not np.isnan(t_stat) else np.nan

state_stats.append({

"Market State": state,

"N Months": n,

"Mean (%)": mean_ret * 100,

"Std (%)": std_ret * 100,

"t-stat": t_stat,

"p-value": p_val

})

state_stats_df = pd.DataFrame(state_stats).round(4)

state_stats_df| Market State | N Months | Mean (%) | Std (%) | t-stat | p-value | |

|---|---|---|---|---|---|---|

| 0 | UP | 39 | -1.1972 | 4.5814 | -1.6320 | 0.1109 |

| 1 | DOWN | 111 | -2.4050 | 4.8669 | -5.2063 | 0.0000 |

plot_states = (

ggplot(ewret_states, aes(x="market_state", y="long_short",

fill="market_state")) +

geom_boxplot(alpha=0.7) +

geom_hline(yintercept=0, linetype="dashed", color="gray") +

scale_y_continuous(labels=percent_format()) +

scale_fill_manual(values={"UP": "#1f77b4", "DOWN": "#d62728"}) +

labs(

x="Market State (Prior 12-Month Return)",

y="Monthly Long-Short Return",

title="Momentum Returns by Market State"

) +

theme_minimal() +

theme(

figure_size=(8, 6),

legend_position="none"

)

)

plot_states

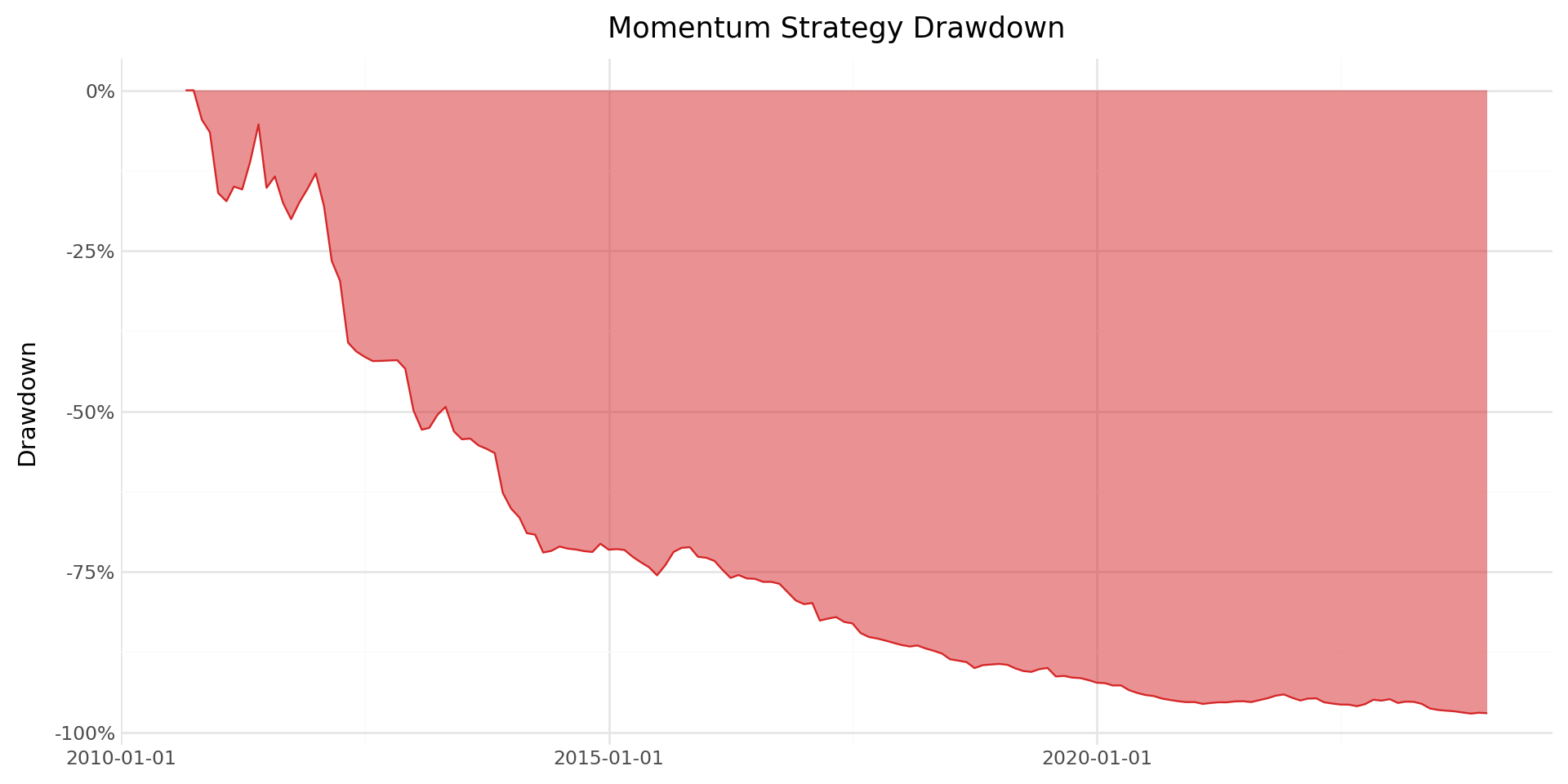

18.9 Momentum Crashes

18.9.1 Understanding Momentum Drawdowns

One of the most important risk characteristics of momentum strategies is their susceptibility to sudden, severe losses—known as momentum crashes. Daniel and Moskowitz (2016) document that momentum strategies experience infrequent but extreme losses, typically during market rebounds following bear markets. These crashes occur because the loser portfolio, which has been short, is heavily loaded with high-beta stocks that surge when markets reverse.

We identify the worst drawdowns of the momentum strategy and examine their market context.

worst_months = (ewret_wide

[["date", "long_short", "winners", "losers"]]

.merge(factors_ff3_monthly[["date", "mkt_excess"]], on="date", how="left")

.sort_values("long_short")

.head(10)

.assign(

long_short_pct=lambda x: (x["long_short"] * 100).round(2),

winners_pct=lambda x: (x["winners"] * 100).round(2),

losers_pct=lambda x: (x["losers"] * 100).round(2),

mkt_pct=lambda x: (x["mkt_excess"] * 100).round(2)

)

[["date", "long_short_pct", "winners_pct", "losers_pct", "mkt_pct"]]

.rename(columns={

"date": "Date",

"long_short_pct": "L/S (%)",

"winners_pct": "Winners (%)",

"losers_pct": "Losers (%)",

"mkt_pct": "Market (%)"

})

)

worst_months| Date | L/S (%) | Winners (%) | Losers (%) | Market (%) | |

|---|---|---|---|---|---|

| 153 | 2023-05-31 | -16.39 | -2.69 | 13.70 | 2.78 |

| 39 | 2013-11-30 | -14.26 | 4.24 | 18.50 | 2.57 |

| 20 | 2012-04-30 | -13.68 | 1.51 | 15.19 | 4.88 |

| 78 | 2017-02-28 | -13.56 | 2.10 | 15.67 | 1.49 |

| 107 | 2019-07-31 | -13.15 | -2.46 | 10.69 | 1.61 |

| 140 | 2022-04-30 | -11.71 | -17.57 | -5.87 | -11.19 |

| 149 | 2023-01-31 | -11.53 | 1.37 | 12.90 | 6.96 |

| 28 | 2012-12-31 | -11.52 | 4.03 | 15.54 | -1.61 |

| 0 | 2010-08-31 | -11.31 | -25.03 | -13.72 | NaN |

| 10 | 2011-06-30 | -10.44 | -3.15 | 7.29 | NaN |

18.9.2 Maximum Drawdown Analysis

The maximum drawdown provides a measure of the worst peak-to-trough decline experienced by the strategy. This metric is particularly relevant for practitioners evaluating the risk of momentum strategies.

# Compute running maximum and drawdown

ewret_wide["cum_wealth"] = (1 + ewret_wide["long_short"]).cumprod()

ewret_wide["running_max"] = ewret_wide["cum_wealth"].cummax()

ewret_wide["drawdown"] = (

ewret_wide["cum_wealth"] / ewret_wide["running_max"] - 1

)

max_dd = ewret_wide["drawdown"].min()

max_dd_date = ewret_wide.loc[ewret_wide["drawdown"].idxmin(), "date"]

print(f"Maximum drawdown: {max_dd*100:.2f}%")

print(f"Date of maximum drawdown: {max_dd_date.date()}")Maximum drawdown: -97.08%

Date of maximum drawdown: 2023-10-31plot_dd = (

ggplot(ewret_wide, aes(x="date", y="drawdown")) +

geom_area(fill="#d62728", alpha=0.5) +

geom_line(color="#d62728", size=0.5) +

scale_y_continuous(labels=percent_format()) +

labs(

x="", y="Drawdown",

title="Momentum Strategy Drawdown"

) +

theme_minimal() +

theme(figure_size=(10, 5))

)

plot_dd

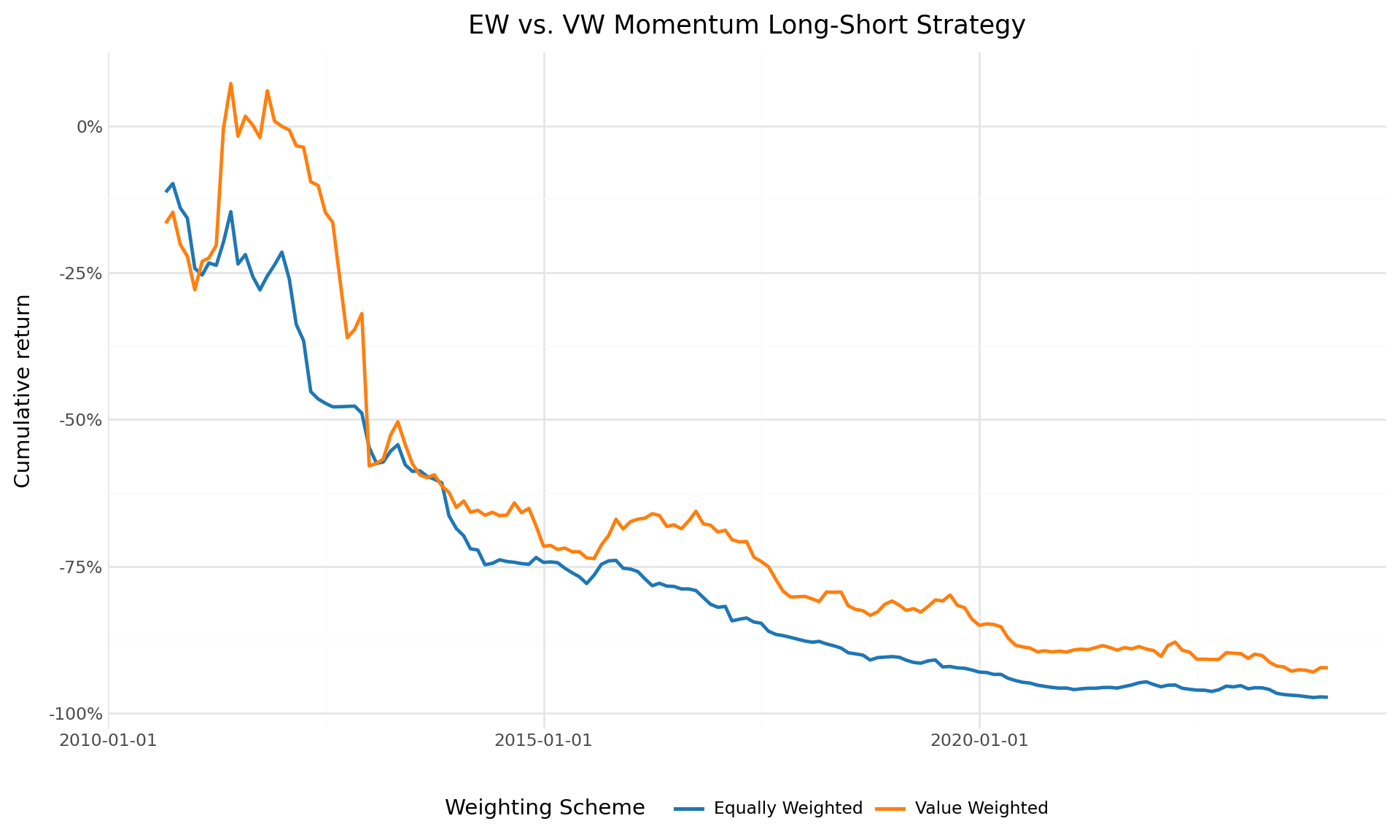

18.10 Value-Weighted Momentum Portfolios

The baseline Jegadeesh and Titman (1993) implementation uses equally weighted portfolios. However, equally weighted returns can be dominated by small, illiquid stocks that may be difficult to trade in practice. Value-weighted portfolios, where each stock’s contribution is proportional to its market capitalization, provide a more investable benchmark and are more representative of the returns that large investors could actually achieve.

def momentum_strategy_vw(data, J, K, n_portfolios=10):

"""

Value-weighted momentum strategy implementation.

Same as the equally-weighted version but uses lagged market

capitalization as weights when computing portfolio returns.

Parameters

----------

data : pd.DataFrame

Panel with columns: symbol, date, ret, mktcap_lag.

J : int

Formation period in months.

K : int

Holding period in months.

n_portfolios : int

Number of portfolios.

Returns

-------

pd.DataFrame

Monthly value-weighted portfolio returns.

"""

# Step 1: Formation period returns

df = data.sort_values(["symbol", "date"]).copy()

df["gross_ret"] = 1 + df["ret"]

df["cum_return"] = (

df.groupby("symbol")["gross_ret"]

.rolling(window=J, min_periods=J)

.apply(np.prod, raw=True)

.reset_index(level=0, drop=True)

- 1

)

df = df.drop(columns=["gross_ret"]).dropna(subset=["cum_return"])

# Step 2: Portfolio assignment using transform (fast)

df["momr"] = df.groupby("date", observed=True)["cum_return"].transform(

lambda x: pd.qcut(

x,

q=n_portfolios,

labels=range(1, n_portfolios + 1),

duplicates="drop"

)

).astype('Int64')

# Fill NaNs with rank-based assignment

mask = df["momr"].isna()

if mask.any():

df.loc[mask, "momr"] = df.loc[mask].groupby("date")["cum_return"].transform(

lambda x: pd.qcut(

x.rank(method="first"),

q=min(n_portfolios, len(x.unique())),

labels=False,

duplicates="drop"

)

).astype('Int64') + 1

# Step 3: Holding period

df = df.rename(columns={"date": "form_date"})

df["hdate1"] = df["form_date"] + pd.offsets.MonthBegin(1)

df["hdate2"] = df["form_date"] + pd.offsets.MonthEnd(K)

# Step 4: Merge with holding period returns AND weights

port_ret = df[

["symbol", "form_date", "momr", "hdate1", "hdate2"]

].merge(

data[["symbol", "date", "ret", "mktcap_lag"]].rename(

columns={"ret": "hret", "date": "hdate"}

),

on="symbol",

how="inner"

)

# Use boolean indexing instead of query (faster)

port_ret = port_ret[

(port_ret["hdate"] >= port_ret["hdate1"]) &

(port_ret["hdate"] <= port_ret["hdate2"])

]

port_ret = port_ret.dropna(subset=["mktcap_lag"])

port_ret = port_ret[port_ret["mktcap_lag"] > 0]

# Step 5: Value-weighted returns within each cohort

def vw_mean(group):

weights = group["mktcap_lag"]

if weights.sum() == 0:

return np.nan

return np.average(group["hret"], weights=weights)

cohort_ret = (port_ret

.groupby(["hdate", "momr", "form_date"])

.apply(vw_mean, include_groups=False)

.reset_index(name="cohort_ret")

)

monthly_ret = (cohort_ret

.groupby(["hdate", "momr"])

.agg(vwret=("cohort_ret", "mean"))

.reset_index()

.rename(columns={"hdate": "date"})

)

# Step 6: Long-short

wide = monthly_ret.pivot(

index="date", columns="momr", values="vwret"

).reset_index()

# Handle variable number of portfolios

n_cols = len(wide.columns) - 1

wide.columns = ["date"] + [f"port{i}" for i in range(1, n_cols + 1)]

wide["winners"] = wide[f"port{n_cols}"]

wide["losers"] = wide["port1"]

wide["long_short"] = wide["winners"] - wide["losers"]

return monthly_ret, wide# Run value-weighted J=6, K=6 strategy

_, vw_results = momentum_strategy_vw(prices_clean, J=6, K=6)

print("Value-Weighted Momentum Strategy (J=6, K=6)")

print("=" * 50)

print("\nPortfolio Statistics:")

print(vw_results[["winners", "losers", "long_short"]].describe().round(4))Value-Weighted Momentum Strategy (J=6, K=6)

==================================================

Portfolio Statistics:

winners losers long_short

count 161.0000 161.0000 161.0000

mean -0.0129 0.0006 -0.0135

std 0.0763 0.0713 0.0653

min -0.2519 -0.2178 -0.3813

25% -0.0540 -0.0397 -0.0465

50% -0.0067 0.0010 -0.0126

75% 0.0354 0.0443 0.0173

max 0.1765 0.2498 0.2498comparison = []

for scheme, df in [("EW", ewret_wide), ("VW", vw_results)]:

for col in ["winners", "losers", "long_short"]:

series = df[col].dropna()

n = len(series)

mean_ret = series.mean()

std_ret = series.std()

t_stat = mean_ret / (std_ret / np.sqrt(n))

p_val = 2 * (1 - stats.t.cdf(abs(t_stat), df=n-1))

comparison.append({

"Weighting": scheme,

"Portfolio": col.replace("_", " ").title(),

"Mean (%)": round(mean_ret * 100, 4),

"Std (%)": round(std_ret * 100, 4),

"t-stat": round(t_stat, 2),

"p-value": round(p_val, 4)

})

pd.DataFrame(comparison)| Weighting | Portfolio | Mean (%) | Std (%) | t-stat | p-value | |

|---|---|---|---|---|---|---|

| 0 | EW | Winners | -0.6812 | 5.7131 | -1.51 | 0.1323 |

| 1 | EW | Losers | 1.4190 | 6.5319 | 2.76 | 0.0065 |

| 2 | EW | Long Short | -2.1002 | 4.8969 | -5.44 | 0.0000 |

| 3 | VW | Winners | -1.2943 | 7.6274 | -2.15 | 0.0328 |

| 4 | VW | Losers | 0.0589 | 7.1275 | 0.10 | 0.9166 |

| 5 | VW | Long Short | -1.3533 | 6.5312 | -2.63 | 0.0094 |

vw_results = vw_results.sort_values("date")

vw_results["cumret_ls_vw"] = (1 + vw_results["long_short"]).cumprod() - 1

ew_data = (ewret_wide[["date", "long_short"]]

.rename(columns={"long_short": "cumret"})

.assign(scheme="Equally Weighted")

)

ew_data["cumret"] = (1 + ew_data["cumret"]).cumprod() - 1

vw_data = (vw_results[["date", "cumret_ls_vw"]]

.rename(columns={"cumret_ls_vw": "cumret"})

.assign(scheme="Value Weighted")

)

ew_vs_vw = pd.concat([ew_data, vw_data], ignore_index=True)

plot_ew_vw = (

ggplot(ew_vs_vw, aes(x="date", y="cumret", color="scheme")) +

geom_line(size=1) +

scale_y_continuous(labels=percent_format()) +

scale_color_manual(values=["#1f77b4", "#ff7f0e"]) +

labs(

x="", y="Cumulative return",

color="Weighting Scheme",

title="EW vs. VW Momentum Long-Short Strategy"

) +

theme_minimal() +

theme(

figure_size=(10, 6),

legend_position="bottom"

)

)

plot_ew_vw

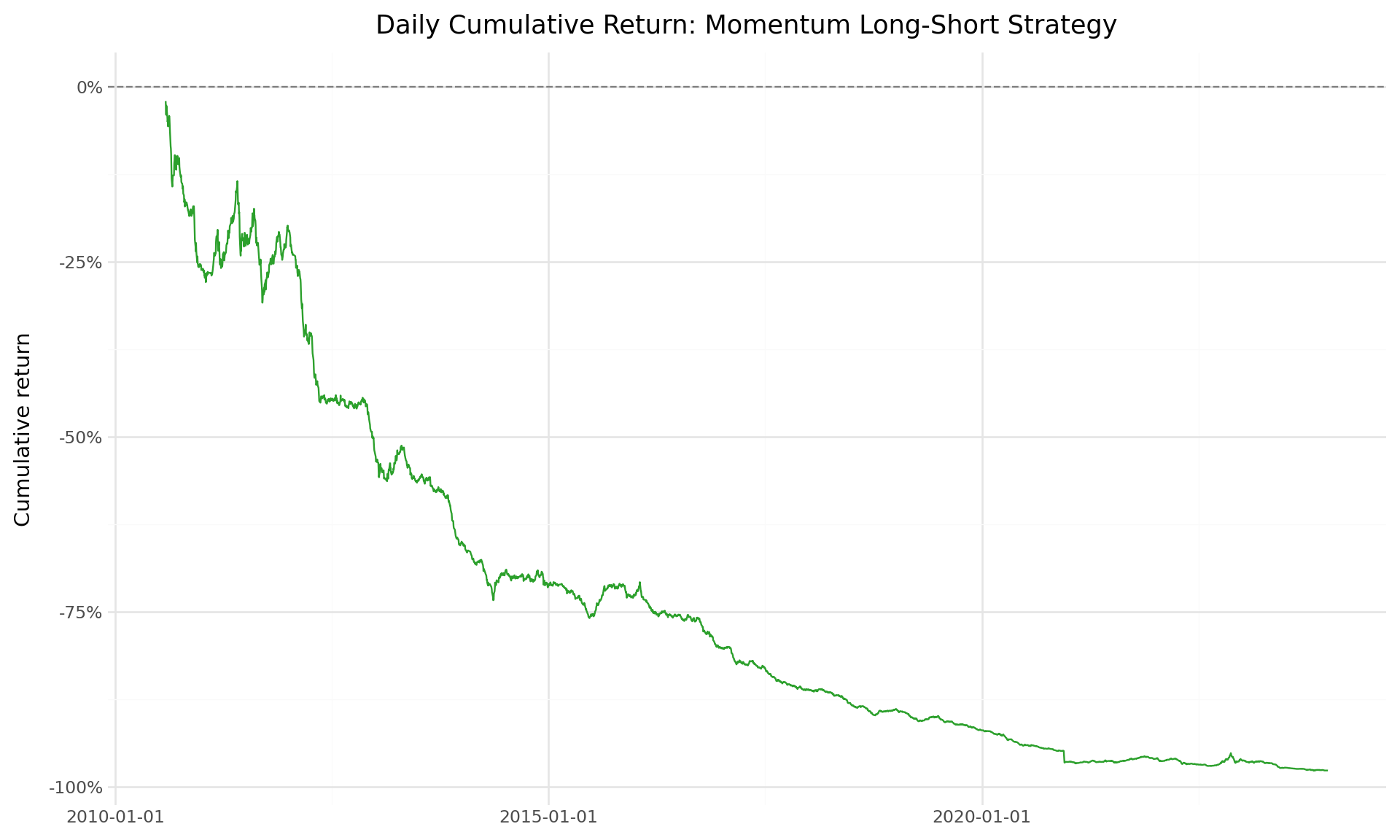

18.11 Daily Momentum Analysis

While momentum strategies are typically evaluated at the monthly frequency following Jegadeesh and Titman (1993), analyzing daily return patterns provides additional insights into the dynamics of momentum profits. Daily data allows us to examine how momentum profits accrue within the holding period, measure intra-month volatility of the strategy, and compute more precise risk measures.

18.11.1 Loading Daily Data

prices_daily = pd.read_sql_query(

sql=("SELECT symbol, date, ret, ret_excess, mktcap_lag "

"FROM prices_daily"),

con=tidy_finance,

parse_dates={"date"}

)

print(f"Daily observations: {len(prices_daily):,}")

print(f"Unique stocks: {prices_daily['symbol'].nunique():,}")

print(f"Date range: {prices_daily['date'].min().date()} "

f"to {prices_daily['date'].max().date()}")Daily observations: 3,462,157

Unique stocks: 1,459

Date range: 2010-01-05 to 2023-12-2918.11.2 Daily Returns of Monthly Momentum Portfolios

Rather than forming momentum portfolios at the daily frequency (which would require daily rebalancing and is impractical), we use the monthly portfolio assignments and track their daily returns. This gives us the daily return series of the monthly momentum strategy.

# # # Use the monthly portfolio assignments from the J=6 baseline

monthly_assignments = portfolios_with_dates[

["symbol", "form_date", "momr", "hdate1", "hdate2"]

].copy()

# Merge with daily returns

daily_mom_returns = monthly_assignments.merge(

prices_daily[["symbol", "date", "ret"]].rename(

columns={"ret": "dret", "date": "ddate"}

),

on="symbol",

how="inner"

)

# Use boolean indexing instead of query

daily_mom_returns = daily_mom_returns[

(daily_mom_returns["ddate"] >= daily_mom_returns["hdate1"]) &

(daily_mom_returns["ddate"] <= daily_mom_returns["hdate2"])

]

print(f"Daily portfolio return observations: {len(daily_mom_returns):,}")Daily portfolio return observations: 19,112,536# Compute daily equally weighted portfolio returns

# Stage 1: Average within each cohort

daily_cohort_ret = (daily_mom_returns

.groupby(["ddate", "momr", "form_date"])

.agg(cohort_ret=("dret", "mean"))

.reset_index()

)

# Stage 2: Average across cohorts

daily_ewret = (daily_cohort_ret

.groupby(["ddate", "momr"])

.agg(ewret=("cohort_ret", "mean"))

.reset_index()

.rename(columns={"ddate": "date"})

)

# Compute daily long-short returns

daily_wide = daily_ewret.pivot(

index="date", columns="momr", values="ewret"

).reset_index()

daily_wide.columns = ["date"] + [f"port{i}" for i in range(1, 11)]

daily_wide["winners"] = daily_wide["port10"]

daily_wide["losers"] = daily_wide["port1"]

daily_wide["long_short"] = daily_wide["winners"] - daily_wide["losers"]

print(f"Daily long-short return observations: {len(daily_wide):,}")Daily long-short return observations: 3,35218.11.3 Daily Cumulative Returns

daily_wide = daily_wide.sort_values("date")

daily_wide["cumret_ls"] = (1 + daily_wide["long_short"]).cumprod() - 1

plot_daily_cumret = (

ggplot(daily_wide, aes(x="date", y="cumret_ls")) +

geom_line(size=0.5, color="#2ca02c") +

geom_hline(yintercept=0, linetype="dashed", color="gray") +

scale_y_continuous(labels=percent_format()) +

labs(

x="", y="Cumulative return",

title="Daily Cumulative Return: Momentum Long-Short Strategy"

) +

theme_minimal() +

theme(figure_size=(10, 6))

)

plot_daily_cumret

18.11.4 Annualized Risk Metrics from Daily Data

Daily data enables more precise estimation of risk metrics through higher-frequency sampling.

daily_ls = daily_wide["long_short"].dropna()

# Annualized metrics

ann_mean = daily_ls.mean() * 252

ann_vol = daily_ls.std() * np.sqrt(252)

sharpe = ann_mean / ann_vol if ann_vol > 0 else np.nan

# Drawdown

daily_wealth = (1 + daily_ls).cumprod()

daily_running_max = daily_wealth.cummax()

daily_dd = (daily_wealth / daily_running_max - 1).min()

# Higher moments

skew = daily_ls.skew()

kurt = daily_ls.kurtosis()

# VaR and CVaR

var_95 = daily_ls.quantile(0.05)

cvar_95 = daily_ls[daily_ls <= var_95].mean()

risk_metrics = pd.DataFrame({

"Metric": [

"Annualized Mean Return",

"Annualized Volatility",

"Sharpe Ratio",

"Maximum Drawdown",

"Skewness",

"Excess Kurtosis",

"Daily VaR (5%)",

"Daily CVaR (5%)"

],

"Value": [

f"{ann_mean*100:.2f}%",

f"{ann_vol*100:.2f}%",

f"{sharpe:.2f}",

f"{daily_dd*100:.2f}%",

f"{skew:.2f}",

f"{kurt:.2f}",

f"{var_95*100:.2f}%",

f"{cvar_95*100:.2f}%"

]

})

risk_metrics| Metric | Value | |

|---|---|---|

| 0 | Annualized Mean Return | -26.90% |

| 1 | Annualized Volatility | 15.01% |

| 2 | Sharpe Ratio | -1.79 |

| 3 | Maximum Drawdown | -97.62% |

| 4 | Skewness | -11.23 |

| 5 | Excess Kurtosis | 378.11 |

| 6 | Daily VaR (5%) | -1.33% |

| 7 | Daily CVaR (5%) | -2.10% |

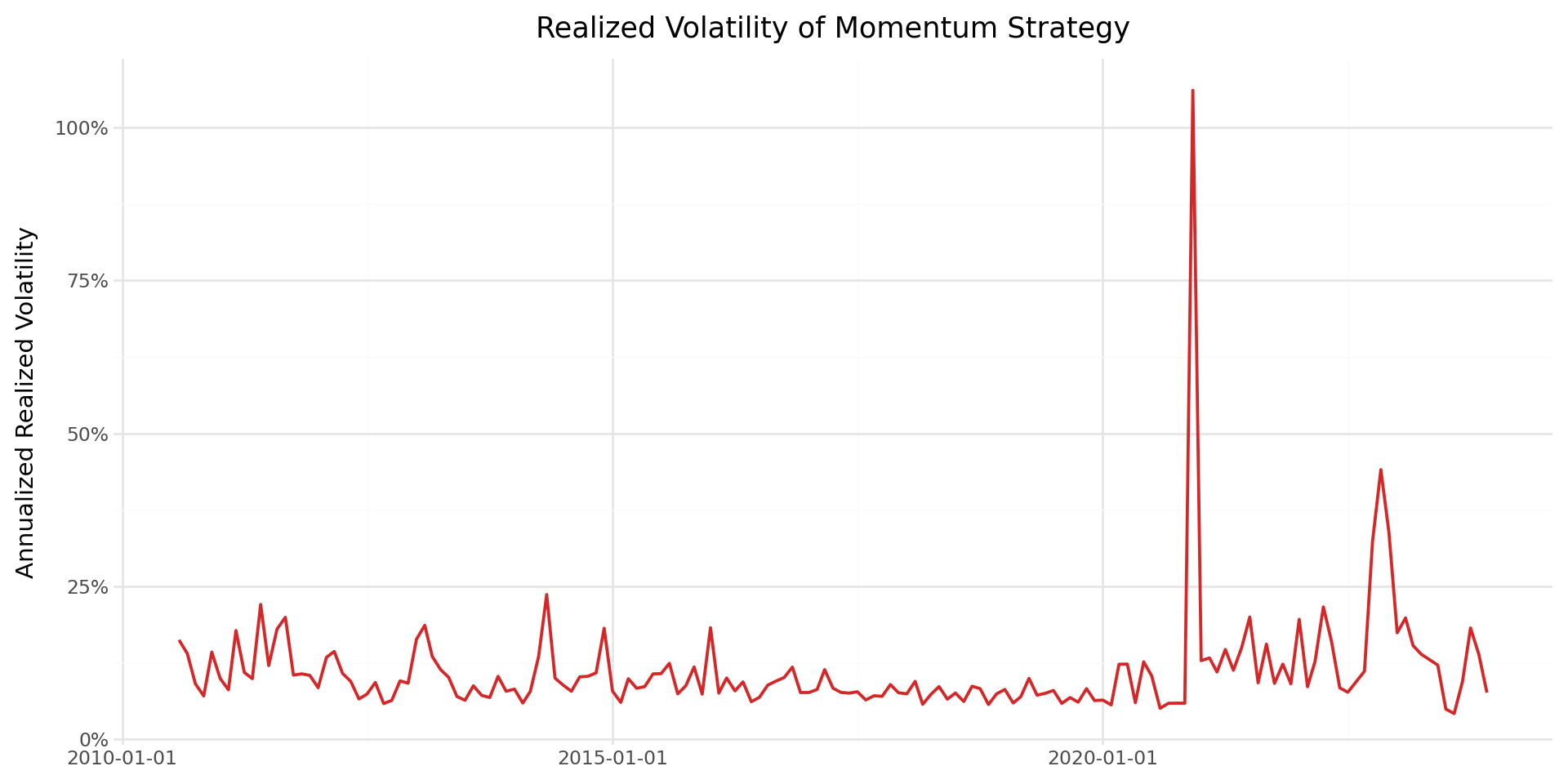

18.11.5 Realized Volatility of Momentum Returns

Using daily returns, we can compute the monthly realized volatility of the momentum strategy and examine how it varies over time.

daily_wide["year_month"] = daily_wide["date"].dt.to_period("M")

realized_vol = (daily_wide

.groupby("year_month")["long_short"]

.std()

.reset_index()

.rename(columns={"long_short": "realized_vol"})

)

realized_vol["date"] = realized_vol["year_month"].dt.to_timestamp()

realized_vol["realized_vol_ann"] = realized_vol["realized_vol"] * np.sqrt(252)

plot_rvol = (

ggplot(realized_vol, aes(x="date", y="realized_vol_ann")) +

geom_line(color="#d62728", size=0.8) +

scale_y_continuous(labels=percent_format()) +

labs(

x="", y="Annualized Realized Volatility",

title="Realized Volatility of Momentum Strategy"

) +

theme_minimal() +

theme(figure_size=(10, 5))

)

plot_rvol

18.12 Saving Results to the Database

We save the momentum portfolio returns to our database for use in subsequent chapters, including factor model construction and portfolio optimization.

# Save monthly equally weighted momentum portfolio returns

ewret_to_save = ewret[["date", "momr", "ewret"]].copy()

ewret_to_save.to_sql(

name="momentum_portfolios_monthly",

con=tidy_finance,

if_exists="replace",

index=False

)

print(f"Saved {len(ewret_to_save):,} monthly momentum portfolio observations.")

# Save the long-short return series

momentum_factor = ewret_wide[["date", "long_short"]].dropna().copy()

momentum_factor = momentum_factor.rename(columns={"long_short": "wml"})

momentum_factor.to_sql(

name="momentum_factor_monthly",

con=tidy_finance,

if_exists="replace",

index=False

)

print(f"Saved {len(momentum_factor):,} monthly WML factor observations.")

# Save the daily long-short return series

daily_momentum_factor = daily_wide[["date", "long_short"]].dropna().copy()

daily_momentum_factor = daily_momentum_factor.rename(

columns={"long_short": "wml"}

)

daily_momentum_factor.to_sql(

name="momentum_factor_daily",

con=tidy_finance,

if_exists="replace",

index=False

)

print(f"Saved {len(daily_momentum_factor):,} daily WML factor observations.")Saved 1,610 monthly momentum portfolio observations.

Saved 161 monthly WML factor observations.

Saved 3,352 daily WML factor observations.18.13 Practical Considerations

18.13.1 Transaction Costs

Momentum strategies involve substantial portfolio turnover, as stocks enter and exit the extreme decile portfolios each month. Korajczyk and Sadka (2004) examine whether momentum profits survive transaction costs and find that profitability declines significantly for large institutional investors, though smaller portfolios can still capture meaningful returns.

In the Vietnamese market, transaction costs include:

- Brokerage commissions: Typically 0.15%–0.25% of transaction value for institutional investors.

- Exchange fees: Approximately 0.03% per trade.

- Market impact: Particularly relevant for smaller, less liquid stocks that dominate the extreme momentum portfolios. Vietnam’s lower liquidity compared to developed markets may amplify this cost.

- Trading band limits: The \(\pm 7\%\) daily price limit on HOSE can prevent immediate execution of trades, introducing tracking error relative to the theoretical portfolio.

18.13.2 Implementation Lag

Our baseline implementation assumes that portfolios can be formed and rebalanced instantaneously at the end of each month. In practice, there is a lag between observing the formation period returns and executing the portfolio trades. The one-month gap between the formation period and the start of the holding period (Jegadeesh (1990)) partially addresses this concern, but practitioners should consider additional implementation delays.

18.13.3 Survivorship Bias

Our dataset from DataCore includes both active and delisted stocks, which mitigates survivorship bias. However, the treatment of delisted stocks can affect momentum results. Stocks that are delisted during the holding period may generate extreme returns (both positive for acquisitions and negative for failures). We retain delisted returns as reported in the database, which is consistent with the treatment in Jegadeesh and Titman (1993).

18.13.4 Small Sample Considerations

The Vietnamese stock market has a relatively short history compared to the U.S. market studied in Jegadeesh and Titman (1993). Our sample spans approximately two decades, compared to the nearly three decades in the original study. This shorter sample period implies wider confidence intervals and greater sensitivity to specific episodes (such as the 2007–2009 financial crisis, which had a severe impact on Vietnamese equities). Results should be interpreted with this caveat in mind.

18.14 Key Takeaways

This chapter has provided an implementation and analysis of momentum strategies in the Vietnamese equity market, following the methodology of Jegadeesh and Titman (1993). The main findings and methodological contributions are:

Methodology: We implemented the full Jegadeesh and Titman (1993) overlapping portfolio methodology, including the two-stage averaging procedure (within-cohort, then across-cohort) that handles the \(K\) active portfolios in each month.

Baseline results: The \(J=6\), \(K=6\) strategy provides a natural benchmark. The spread between winner and loser portfolios reveals whether cross-sectional momentum exists in Vietnamese equities.

Robustness across horizons: By computing the full \(J \times K\) grid with \(J, K \in \{3, 6, 9, 12\}\), we assessed whether the momentum premium is robust to the choice of formation and holding periods, following the approach in Jegadeesh and Titman (1993) Table 1.

Risk adjustment: CAPM and Fama-French three-factor alphas measure whether the momentum premium is explained by standard risk factors, building on the analysis in Fama and French (1996) who show that their three-factor model fails to explain momentum.

Market state dependence: Following Cooper, Gutierrez Jr, and Hameed (2004), we examined whether momentum profits vary with market conditions, which is particularly relevant in emerging markets with pronounced boom-bust cycles.

Value weighting: The comparison of equally weighted and value-weighted strategies addresses practical implementability and isolates the role of firm size in driving momentum profits.

Daily analysis: By tracking momentum portfolios at the daily frequency, we computed precise risk metrics including realized volatility, maximum drawdown, VaR, and CVaR, providing a complete risk profile of the strategy.

Emerging market context: Throughout the analysis, we have highlighted features specific to the Vietnamese market—trading band limits, foreign ownership restrictions, shorter sample history, and higher transaction costs—that affect the interpretation and practical viability of momentum strategies.