import pandas as pd

import numpy as np

import sqlite3

from datetime import datetime

from io import BytesIO

from plotnine import *

from mizani.formatters import comma_format, percent_format3 Dữ liệu Datacore

Chương này giới thiệu Datacore, nền tảng dữ liệu của Việt Nam dành cho nghiên cứu học thuật, doanh nghiệp và chính phủ. Datacore cung cấp các bộ dữ liệu tài chính và kinh tế toàn diện, bao gồm dữ liệu giao dịch lịch sử, các yếu tố cơ bản của công ty và các chỉ số kinh tế vĩ mô thiết yếu cho nghiên cứu tài chính có thể tái tạo. Chúng ta sử dụng Datacore làm nguồn dữ liệu chính xuyên suốt cuốn sách này.

3.1 Các tùy chọn truy cập dữ liệu

Độc giả có thể truy cập dữ liệu được sử dụng trong cuốn sách này thông qua một số kênh sau:

Gói đăng ký dành cho tổ chức: Nhiều trường đại học và viện nghiên cứu đăng ký sử dụng Datacore. Hãy liên hệ với thư viện hoặc văn phòng nghiên cứu của bạn để nhận thông tin đăng nhập. Nếu tổ chức của bạn chưa có gói đăng ký, hãy cân nhắc yêu cầu một gói thông qua quy trình mua sắm của thư viện — Datacore cung cấp giá ưu đãi cho mục đích học thuật.

Bộ dữ liệu demo: Datacore cung cấp bộ dữ liệu demo cho phép bạn chạy các ví dụ mã trong sách này với dữ liệu mẫu.

3.2 Tổng quan chương

Chương này được tổ chức như sau. Trước tiên, chúng ta thiết lập kết nối với cơ sở hạ tầng lưu trữ đám mây của Datacore. Sau đó, chúng ta tải xuống và chuẩn bị dữ liệu cơ bản của công ty, bao gồm các khoản mục bảng cân đối kế toán, các biến số báo cáo kết quả kinh doanh và các chỉ số phái sinh cần thiết cho nghiên cứu định giá tài sản. Tiếp theo, chúng ta truy xuất và xử lý dữ liệu giá cổ phiếu, tính toán lợi nhuận, vốn hóa thị trường và lợi nhuận vượt trội. Cuối cùng, chúng ta kết hợp các tập dữ liệu này và cung cấp số liệu thống kê mô tả đặc trưng cho thị trường chứng khoán Việt Nam.

3.3 Thiết lập môi trường

Chúng ta bắt đầu bằng cách tải các gói Python được sử dụng xuyên suốt chương này. Các gói cốt lõi bao gồm pandas để thao tác dữ liệu, numpy cho các phép toán số học và sqlite3 để quản lý cơ sở dữ liệu cục bộ. Chúng ta cũng nhập các thư viện trực quan hóa để tạo ra các hình ảnh chất lượng cao phục vụ cho việc xuất bản.

Chúng ta thiết lập kết nối đến cơ sở dữ liệu SQLite cục bộ, đóng vai trò là kho lưu trữ trung tâm cho tất cả dữ liệu đã được xử lý. Cơ sở dữ liệu này đã được giới thiệu trong chương trước và sẽ lưu trữ các tập dữ liệu đã được làm sạch để sử dụng trong các phân tích tiếp theo.

tidy_finance = sqlite3.connect(database="data/tidy_finance_python.sqlite")Chúng ta xác định phạm vi ngày tháng cho việc thu thập dữ liệu. Thị trường chứng khoán Việt Nam bắt đầu hoạt động vào tháng 7 năm 2000 với sự thành lập của Sở Giao dịch Chứng khoán Thành phố Hồ Chí Minh (HOSE), vì vậy giai đoạn mẫu của chúng ta bắt đầu từ năm 2000 và kéo dài đến hết năm 2024.

start_date = "2000-01-01"

end_date = "2024-12-31"3.4 Kết nối với Datacore

Datacore cung cấp dữ liệu thông qua hệ thống lưu trữ đối tượng dựa trên đám mây được xây dựng trên MinIO, một cơ sở hạ tầng lưu trữ tương thích với S3. Kiến trúc này cho phép truy cập hiệu quả, lập trình được vào các tập dữ liệu lớn mà không bị hạn chế bởi các kết nối cơ sở dữ liệu truyền thống. Để truy cập dữ liệu, bạn cần thông tin xác thực do Datacore cung cấp khi đăng ký: URL điểm cuối, khóa truy cập và khóa bí mật.

Lớp sau đây thiết lập kết nối với hệ thống lưu trữ của Datacore. Thông tin đăng nhập được lưu trữ dưới dạng biến môi trường để đảm bảo an toàn, tuân theo các thực tiễn tốt nhất về quản lý thông tin đăng nhập trong môi trường điện toán nghiên cứu.

import os

import boto3

from botocore.client import Config

class DatacoreConnection:

"""

Connection handler for Datacore's MinIO-based storage system.

This class manages authentication and provides methods for

accessing financial datasets stored in Datacore's cloud infrastructure.

Attributes

----------

s3 : boto3.client

S3-compatible client for interacting with Datacore storage

"""

def __init__(self):

"""Initialize connection using environment variables."""

self.MINIO_ENDPOINT = os.environ["MINIO_ENDPOINT"]

self.MINIO_ACCESS_KEY = os.environ["MINIO_ACCESS_KEY"]

self.MINIO_SECRET_KEY = os.environ["MINIO_SECRET_KEY"]

self.REGION = os.getenv("MINIO_REGION", "us-east-1")

self.s3 = boto3.client(

"s3",

endpoint_url=self.MINIO_ENDPOINT,

aws_access_key_id=self.MINIO_ACCESS_KEY,

aws_secret_access_key=self.MINIO_SECRET_KEY,

region_name=self.REGION,

config=Config(signature_version="s3v4"),

)

def test_connection(self):

"""Verify connection by listing available buckets."""

response = self.s3.list_buckets()

print("Connected successfully. Available buckets:")

for bucket in response.get("Buckets", []):

print(f" - {bucket['Name']}")

def list_objects(self, bucket_name, prefix=""):

"""List objects in a bucket with optional prefix filter."""

response = self.s3.list_objects_v2(

Bucket=bucket_name,

Prefix=prefix

)

return [obj["Key"] for obj in response.get("Contents", [])]

def read_excel(self, bucket_name, key):

"""Read an Excel file from Datacore storage."""

obj = self.s3.get_object(Bucket=bucket_name, Key=key)

return pd.read_excel(BytesIO(obj["Body"].read()))

def read_csv(self, bucket_name, key, **kwargs):

"""Read a CSV file from Datacore storage."""

obj = self.s3.get_object(Bucket=bucket_name, Key=key)

return pd.read_csv(BytesIO(obj["Body"].read()), **kwargs)Sau khi định nghĩa lớp kết nối, chúng ta có thể thiết lập kết nối và xác minh quyền truy cập vào các kho dữ liệu của Datacore.

# Initialize connection

conn = DatacoreConnection()

conn.test_connection()

# Get bucket name from environment

bucket_name = os.environ["MINIO_BUCKET"]Connected successfully. Available buckets:

- dsteam-data

- rawbctc3.5 Dữ liệu cơ bản của công ty

Dữ liệu kế toán của các công ty là yếu tố thiết yếu cho việc phân tích danh mục đầu tư, xây dựng yếu tố và nghiên cứu định giá. Datacore cung cấp dữ liệu cơ bản toàn diện cho các công ty niêm yết của Việt Nam, bao gồm báo cáo tài chính hàng năm và hàng quý được lập theo Chuẩn mực Kế toán Việt Nam (VAS).

3.5.1 Hiểu về Báo cáo Tài chính Việt Nam

Trước khi xử lý dữ liệu, điều quan trọng là phải hiểu cấu trúc của báo cáo tài chính Việt Nam. Các công ty Việt Nam tuân theo Chuẩn mực kế toán Việt Nam (VAS), có nhiều điểm tương đồng với Chuẩn mực báo cáo tài chính quốc tế (IFRS) nhưng cũng có những khác biệt đáng chú ý:

Năm tài chính: Hầu hết các công ty Việt Nam sử dụng năm tài chính theo lịch dương, kết thúc vào ngày 31 tháng 12, mặc dù một số công ty (đặc biệt là trong lĩnh vực bán lẻ và nông nghiệp) sử dụng năm tài chính kết thúc vào ngày khác.

Tần suất báo cáo: Các công ty niêm yết phải công bố báo cáo tài chính hàng quý trong vòng 20 ngày kể từ ngày kết thúc quý và báo cáo kiểm toán hàng năm trong vòng 90 ngày kể từ ngày kết thúc năm tài chính.

Các định dạng đặc thù theo ngành: Các công ty trong lĩnh vực ngân hàng, bảo hiểm và chứng khoán tuân theo các định dạng báo cáo chuyên biệt, khác với định dạng tiêu chuẩn của ngành.

Tiền tệ: Tất cả các số liệu được báo cáo bằng Đồng Việt Nam (VND). Do giá trị danh nghĩa lớn (hàng triệu đến hàng nghìn tỷ VND), chúng ta thường quy đổi các số liệu thành hàng triệu hoặc hàng tỷ để dễ đọc hơn.

3.5.2 Tải xuống dữ liệu cơ bản

Datacore tổ chức dữ liệu cơ bản trong các tệp Excel được phân vùng theo khoảng thời gian để truy cập hiệu quả. Chúng ta tải xuống và ghép nối các tệp này để tạo ra một tập dữ liệu toàn diện bao gồm toàn bộ giai đoạn mẫu của chúng ta.

# Define paths to fundamentals data files

fundamentals_paths = [

"fundamental_annual_1767674486317/fundamental_annual_1.xlsx",

"fundamental_annual_1767674486317/fundamental_annual_2.xlsx",

"fundamental_annual_1767674486317/fundamental_annual_3.xlsx",

]

# Download and combine all files

fundamentals_list = []

for path in fundamentals_paths:

df_temp = conn.read_excel(bucket_name, path)

fundamentals_list.append(df_temp)

print(f"Downloaded: {path} ({len(df_temp):,} rows)")

df_fundamentals_raw = pd.concat(fundamentals_list, ignore_index=True)

print(f"\nTotal observations: {len(df_fundamentals_raw):,}")/home/mikenguyen/project/tidyfinance/.venv/lib/python3.13/site-packages/openpyxl/styles/stylesheet.py:237: UserWarning: Workbook contains no default style, apply openpyxl's defaultDownloaded: fundamental_annual_1767674486317/fundamental_annual_1.xlsx (10,000 rows)/home/mikenguyen/project/tidyfinance/.venv/lib/python3.13/site-packages/openpyxl/styles/stylesheet.py:237: UserWarning: Workbook contains no default style, apply openpyxl's defaultDownloaded: fundamental_annual_1767674486317/fundamental_annual_2.xlsx (10,000 rows)/home/mikenguyen/project/tidyfinance/.venv/lib/python3.13/site-packages/openpyxl/styles/stylesheet.py:237: UserWarning: Workbook contains no default style, apply openpyxl's defaultDownloaded: fundamental_annual_1767674486317/fundamental_annual_3.xlsx (2,821 rows)

Total observations: 22,8213.5.3 Nguyên tắc cơ bản về vệ sinh và tiêu chuẩn hóa

Dữ liệu cơ bản thô cần trải qua nhiều bước làm sạch để đảm bảo tính nhất quán và khả năng sử dụng. Chúng ta chuẩn hóa tên biến, xử lý các giá trị thiếu và tạo ra các biến dẫn xuất thường được sử dụng trong nghiên cứu định giá tài sản.

def clean_fundamentals(df):

"""

Clean and standardize company fundamentals data.

Parameters

----------

df : pd.DataFrame

Raw fundamentals data from Datacore

Returns

-------

pd.DataFrame

Cleaned fundamentals with standardized column names

"""

df = df.copy()

# Standardize identifiers

df["symbol"] = df["symbol"].astype(str).str.upper().str.strip()

df["year"] = pd.to_numeric(df["year"], errors="coerce").astype("Int64")

# Drop rows with missing identifiers

df = df.dropna(subset=["symbol", "year"])

# Define columns that should be numeric

numeric_columns = [

"total_asset", "total_equity", "total_liabilities",

"total_current_asset", "total_current_liabilities",

"is_net_revenue", "is_cogs", "is_manage_expense",

"is_interest_expense", "is_eat", "is_net_business_profit",

"na_tax_deferred", "nl_tax_deferred", "e_preferred_stock",

"capex", "total_cfo", "ca_cce", "ca_total_inventory",

"ca_acc_receiv", "cfo_interest_expense", "basic_eps",

"is_shareholders_eat", "cl_loan", "cl_finlease",

"cl_due_long_debt", "nl_loan", "nl_finlease",

"is_cos_of_sales", "e_equity"

]

for col in numeric_columns:

if col in df.columns:

df[col] = pd.to_numeric(df[col], errors="coerce")

# Handle duplicates: keep row with most non-missing values

df["_completeness"] = df.notna().sum(axis=1)

df = (df

.sort_values(["symbol", "year", "_completeness"])

.drop_duplicates(subset=["symbol", "year"], keep="last")

.drop(columns="_completeness")

.reset_index(drop=True)

)

return df

df_fundamentals = clean_fundamentals(df_fundamentals_raw)

print(f"After cleaning: {len(df_fundamentals):,} firm-year observations")

print(f"Unique firms: {df_fundamentals['symbol'].nunique():,}")After cleaning: 21,232 firm-year observations

Unique firms: 1,5543.5.4 Tạo các biến chuẩn hóa

Để tạo điều kiện so sánh với các nghiên cứu quốc tế và đảm bảo tính tương thích với các phương pháp định giá tài sản tiêu chuẩn, chúng ta tạo ra các biến số theo các quy ước đã được thiết lập trong tài liệu học thuật. Chúng ta đối chiếu các khoản mục báo cáo tài chính của Việt Nam với các giá trị tương đương trong Compustat khi có thể.

def create_standard_variables(df):

"""

Create standardized financial variables for asset pricing research.

This function maps Vietnamese financial statement items to standard

variable names used in the academic finance literature, following

conventions from Fama and French (1992, 1993, 2015).

Parameters

----------

df : pd.DataFrame

Cleaned fundamentals data

Returns

-------

pd.DataFrame

Fundamentals with standardized variables added

"""

df = df.copy()

# Fiscal date (assume December year-end)

df["datadate"] = pd.to_datetime(df["year"].astype(str) + "-12-31")

# === Balance Sheet Items ===

df["at"] = df["total_asset"] # Total assets

df["lt"] = df["total_liabilities"] # Total liabilities

df["seq"] = df["total_equity"] # Stockholders' equity

df["act"] = df["total_current_asset"] # Current assets

df["lct"] = df["total_current_liabilities"] # Current liabilities

# Common equity (fallback to total equity if not available)

df["ceq"] = df.get("e_equity", df["seq"])

# === Deferred Taxes ===

df["txditc"] = df.get("na_tax_deferred", 0).fillna(0) # Deferred tax assets

df["txdb"] = df.get("nl_tax_deferred", 0).fillna(0) # Deferred tax liab.

df["itcb"] = 0 # Investment tax credit (rare in Vietnam)

# === Preferred Stock ===

pref = df.get("e_preferred_stock", 0)

if isinstance(pref, pd.Series):

pref = pref.fillna(0)

df["pstk"] = pref

df["pstkrv"] = pref # Redemption value

df["pstkl"] = pref # Liquidating value

# === Income Statement Items ===

df["sale"] = df["is_net_revenue"] # Net sales/revenue

df["cogs"] = df.get("is_cogs", 0).fillna(0) # Cost of goods sold

df["xsga"] = df.get("is_manage_expense", 0).fillna(0) # SG&A expenses

df["xint"] = df.get("is_interest_expense", 0).fillna(0) # Interest expense

df["ni"] = df.get("is_eat", np.nan) # Net income

df["oibdp"] = df.get("is_net_business_profit", np.nan) # Operating income

# === Cash Flow Items ===

df["oancf"] = df.get("total_cfo", np.nan) # Operating cash flow

df["capx"] = df.get("capex", np.nan) # Capital expenditures

return df

df_fundamentals = create_standard_variables(df_fundamentals)3.5.5 Tính toán giá trị sổ sách và lợi nhuận

Giá trị sổ sách là một biến số quan trọng đối với các chiến lược đầu tư giá trị và việc xây dựng danh mục đầu tư theo yếu tố HML (Cao Trừ Thấp). Chúng ta tuân theo định nghĩa từ thư viện dữ liệu của Kenneth French, có tính đến thuế hoãn lại và cổ phiếu ưu đãi.

def compute_book_equity(df):

"""

Compute book equity following Fama-French conventions.

Book equity = Stockholders' equity

+ Deferred taxes and investment tax credit

- Preferred stock

Negative or zero book equity is set to missing, as book-to-market

ratios are undefined for such firms.

Parameters

----------

df : pd.DataFrame

Fundamentals with standardized variables

Returns

-------

pd.DataFrame

Fundamentals with book equity (be) added

"""

df = df.copy()

# Primary measure: stockholders' equity

# Fallback 1: common equity + preferred stock

# Fallback 2: total assets - total liabilities

seq_measure = (df["seq"]

.combine_first(df["ceq"] + df["pstk"])

.combine_first(df["at"] - df["lt"])

)

# Add deferred taxes

deferred_taxes = (df["txditc"]

.combine_first(df["txdb"] + df["itcb"])

.fillna(0)

)

# Subtract preferred stock (use redemption value as primary)

preferred = (df["pstkrv"]

.combine_first(df["pstkl"])

.combine_first(df["pstk"])

.fillna(0)

)

# Book equity calculation

df["be"] = seq_measure + deferred_taxes - preferred

# Set non-positive book equity to missing

df["be"] = df["be"].where(df["be"] > 0, np.nan)

return df

df_fundamentals = compute_book_equity(df_fundamentals)

# Summary statistics for book equity

print("Book Equity Summary Statistics (in million VND):")

print(df_fundamentals["be"].describe().round(2))Book Equity Summary Statistics (in million VND):

count 2.023500e+04

mean 1.031884e+12

std 4.705269e+12

min 4.404402e+07

25% 7.267610e+10

50% 1.803885e+11

75% 5.304653e+11

max 1.836314e+14

Name: be, dtype: float64Lợi nhuận hoạt động, được giới thiệu bởi Fama and French (2015), đo lường lợi nhuận của một công ty so với vốn chủ sở hữu trên sổ sách. Các công ty có lợi nhuận hoạt động cao hơn thường có tỷ suất sinh lời kỳ vọng cao hơn.

def compute_profitability(df):

"""

Compute operating profitability following Fama-French (2015).

Operating profitability = (Revenue - COGS - SG&A - Interest) / Book Equity

Parameters

----------

df : pd.DataFrame

Fundamentals with book equity computed

Returns

-------

pd.DataFrame

Fundamentals with operating profitability (op) added

"""

df = df.copy()

# Operating profit before taxes

operating_profit = (

df["sale"]

- df["cogs"].fillna(0)

- df["xsga"].fillna(0)

- df["xint"].fillna(0)

)

# Scale by book equity

df["op"] = operating_profit / df["be"]

# Winsorize extreme values (outside 1st and 99th percentiles)

lower = df["op"].quantile(0.01)

upper = df["op"].quantile(0.99)

df["op"] = df["op"].clip(lower=lower, upper=upper)

return df

df_fundamentals = compute_profitability(df_fundamentals)3.5.6 Tính toán Đầu tư

Đầu tư, được đo lường bằng sự tăng trưởng tài sản, nắm bắt hành vi đầu tư của các công ty. Fama and French (2015) ghi nhận rằng các công ty có tốc độ tăng trưởng tài sản cao (đầu tư tháo vát) thường có tỷ suất sinh lời trong tương lai thấp hơn.

def compute_investment(df):

"""

Compute investment (asset growth) following Fama-French (2015).

Investment = (Total Assets_t / Total Assets_{t-1}) - 1

Parameters

----------

df : pd.DataFrame

Fundamentals data

Returns

-------

pd.DataFrame

Fundamentals with investment (inv) added

"""

df = df.copy()

# Create lagged assets

df_lag = (df[["symbol", "year", "at"]]

.assign(year=lambda x: x["year"] + 1)

.rename(columns={"at": "at_lag"})

)

# Merge lagged values

df = df.merge(df_lag, on=["symbol", "year"], how="left")

# Compute investment (asset growth)

df["inv"] = df["at"] / df["at_lag"] - 1

# Set to missing if lagged assets non-positive

df["inv"] = df["inv"].where(df["at_lag"] > 0, np.nan)

return df

df_fundamentals = compute_investment(df_fundamentals)3.5.7 Tính toán tổng nợ

Trong báo cáo tài chính của Việt Nam, tổng nợ phải trả bao gồm các khoản mục không sinh lãi như khoản phải trả cho nhà cung cấp và thuế phải trả. Để phân tích đòn bẩy, chúng ta tính tổng nợ có lãi bằng cách cộng gộp các khoản vay và nghĩa vụ thuê.

def compute_total_debt(df):

"""

Compute total interest-bearing debt.

Total Debt = Short-term loans + Finance leases (current)

+ Current portion of long-term debt

+ Long-term loans + Finance leases (non-current)

Parameters

----------

df : pd.DataFrame

Fundamentals data

Returns

-------

pd.DataFrame

Fundamentals with total_debt added

"""

df = df.copy()

df["total_debt"] = (

df.get("cl_loan", 0).fillna(0) + # Short-term bank loans

df.get("cl_finlease", 0).fillna(0) + # Current finance leases

df.get("cl_due_long_debt", 0).fillna(0) + # Current portion LT debt

df.get("nl_loan", 0).fillna(0) + # Long-term bank loans

df.get("nl_finlease", 0).fillna(0) # Non-current finance leases

)

return df

df_fundamentals = compute_total_debt(df_fundamentals)3.5.8 Áp dụng bộ lọc

Chúng ta áp dụng các bộ lọc tiêu chuẩn để đảm bảo chất lượng dữ liệu: yêu cầu tài sản dương, doanh số bán hàng không âm và sự hiện diện của các biến cốt lõi cần thiết để xây dựng danh mục đầu tư.

# Keep only observations with required variables

required_vars = ["at", "lt", "seq", "sale"]

comp_vn = df_fundamentals.dropna(subset=required_vars)

# Apply quality filters

comp_vn = comp_vn.query("at > 0") # Positive assets

comp_vn = comp_vn.query("sale >= 0") # Non-negative sales

# Keep last observation per firm-year (in case of restatements)

comp_vn = (comp_vn

.sort_values("datadate")

.groupby(["symbol", "year"])

.tail(1)

.reset_index(drop=True)

)

# Diagnostic summary

print(f"Final sample: {len(comp_vn):,} firm-year observations")

print(f"Unique firms: {comp_vn['symbol'].nunique():,}")

print(f"Sample period: {comp_vn['year'].min()} - {comp_vn['year'].max()}")Final sample: 20,091 firm-year observations

Unique firms: 1,502

Sample period: 1998 - 20233.5.9 Lưu trữ dữ liệu

Chúng ta lưu trữ dữ liệu cơ bản đã chuẩn bị trong cơ sở dữ liệu SQLite cục bộ để sử dụng trong các chương tiếp theo.

comp_vn.to_sql(

name="comp_vn",

con=tidy_finance,

if_exists="replace",

index=False

)

print("Company fundamentals saved to database.")Company fundamentals saved to database.3.6 Dữ liệu giá cổ phiếu

Dữ liệu giá cổ phiếu là nền tảng của các phân tích dựa trên lợi nhuận trong tài chính thực nghiệm. Datacore cung cấp dữ liệu giá lịch sử toàn diện cho tất cả các chứng khoán được giao dịch trên HOSE, HNX và UPCoM, bao gồm cả giá điều chỉnh có tính đến các hành động của công ty.

3.6.1 Tải xuống dữ liệu giá

Chúng ta tải xuống dữ liệu giá lịch sử từ hệ thống lưu trữ của Datacore. Dữ liệu bao gồm các quan sát hàng ngày với giá mở cửa, giá cao nhất, giá thấp nhất, giá đóng cửa, khối lượng giao dịch và các yếu tố điều chỉnh.

# Download historical price data

prices_raw = conn.read_csv(

bucket_name,

"historycal_price/dataset_historical_price.csv",

low_memory=False

)

print(f"Downloaded {len(prices_raw):,} daily price observations")

print(f"Date range: {prices_raw['date'].min()} to {prices_raw['date'].max()}")Downloaded 4,307,791 daily price observations

Date range: 2010-01-04 to 2025-05-123.6.2 Xử lý dữ liệu giá

Chúng ta làm sạch dữ liệu giá và tính toán giá điều chỉnh có tính đến việc chia tách cổ phiếu, cổ tức bằng cổ phiếu và các hành động khác của công ty.

def process_price_data(df):

"""

Process raw price data from Datacore.

"""

df = df.copy()

# Parse dates

df["date"] = pd.to_datetime(df["date"])

# Standardize column names

df = df.rename(columns={

"open_price": "open",

"high_price": "high",

"low_price": "low",

"close_price": "close",

"vol_total": "volume"

})

# Compute adjusted close price

df["adjusted_close"] = df["close"] * df["adj_ratio"]

# Standardize symbol

df["symbol"] = df["symbol"].astype(str).str.upper().str.strip()

# Sort for return calculation

df = df.sort_values(["symbol", "date"])

# Add year and month

df["year"] = df["date"].dt.year

df["month"] = df["date"].dt.month

return df

prices = process_price_data(prices_raw)3.6.3 Tính toán Số lượng Cổ phiếu Hoạt động và Giá trị Thị trường

Giá trị thị trường được tính bằng sản phẩm của giá và số lượng cổ phiếu hoạt động. Vì Datacore cung cấp lợi nhuận trên mỗi cổ phiếu và lợi nhuận sau thuế, chúng ta có thể suy ra số lượng cổ phiếu hoạt động từ các biến số này.

def compute_shares_outstanding(fundamentals_df):

"""

Compute shares outstanding from fundamentals.

"""

shares = fundamentals_df.copy()

shares["shrout"] = shares["is_shareholders_eat"] / shares["basic_eps"]

shares = shares[["symbol", "year", "shrout"]].dropna()

return shares

shares_outstanding = compute_shares_outstanding(df_fundamentals)def add_market_cap(df, shares_df):

"""

Add market capitalization to price data.

"""

df = df.merge(shares_df, on=["symbol", "year"], how="left")

# Compute market cap (in million VND)

df["mktcap"] = (df["close"] * df["shrout"]) / 1_000_000

# Set zero or negative market cap to missing

df["mktcap"] = df["mktcap"].where(df["mktcap"] > 0, np.nan)

return df

prices = add_market_cap(prices, shares_outstanding)3.6.4 Tính Lợi Nhuận và Lợi Nhuận Kỳ Lượng

Chúng ta tính toán lợi nhuận sử dụng giá đóng cửa điều chỉnh để đảm bảo lợi nhuận phản ánh chính xác lợi nhuận tổng của cổ đông bao gồm cả cổ tức và các hành động của công ty.

3.6.4.1 Tạo Bộ Dữ Liệu Hàng Ngày

- Phiên bản tuần tự

def create_daily_dataset(df, annual_rf=0.04):

"""

Create daily price dataset with returns and excess returns.

"""

df = df.copy()

# Sort by symbol and date (critical for correct return calculation)

df = df.sort_values(["symbol", "date"]).reset_index(drop=True)

# Remove duplicate dates within each symbol (keep last observation)

df = df.drop_duplicates(subset=["symbol", "date"], keep="last")

# Compute daily returns

df["ret"] = df.groupby("symbol")["adjusted_close"].pct_change()

# Cap extreme negative returns

df["ret"] = df["ret"].clip(lower=-0.99)

# Daily risk-free rate (assuming 252 trading days)

df["risk_free"] = annual_rf / 252

# Excess returns

df["ret_excess"] = df["ret"] - df["risk_free"]

df["ret_excess"] = df["ret_excess"].clip(lower=-1.0)

# Lagged market cap

df["mktcap_lag"] = df.groupby("symbol")["mktcap"].shift(1)

return df

prices_daily = create_daily_dataset(prices)- Phiên bản song song

from joblib import Parallel, delayed

import os

def process_daily_symbol(symbol_df, annual_rf=0.04):

"""

Process a single symbol's daily data.

"""

df = symbol_df.copy()

# Sort by date (critical for correct return calculation)

df = df.sort_values("date").reset_index(drop=True)

# Remove duplicate dates (keep last observation if duplicates exist)

df = df.drop_duplicates(subset=["date"], keep="last")

# Compute daily returns

df["ret"] = df["adjusted_close"].pct_change()

# Replace infinite values with NaN

df["ret"] = df["ret"].replace([np.inf, -np.inf], np.nan)

# Cap extreme negative returns

df["ret"] = df["ret"].clip(lower=-0.99)

# Daily risk-free rate

df["risk_free"] = annual_rf / 252

# Excess returns

df["ret_excess"] = df["ret"] - df["risk_free"]

df["ret_excess"] = df["ret_excess"].clip(lower=-1.0)

# Lagged market cap

df["mktcap_lag"] = df["mktcap"].shift(1)

return df

def create_daily_dataset_parallel(df, annual_rf=0.04):

"""

Create daily price dataset using parallel processing.

"""

# Ensure data is sorted before splitting

df = df.sort_values(["symbol", "date"])

# Split by symbol

symbol_groups = [group for _, group in df.groupby("symbol")]

n_jobs = max(1, os.cpu_count() - 1)

print(f"Processing {len(symbol_groups):,} symbols using {n_jobs} cores...")

results = Parallel(n_jobs=n_jobs, verbose=1)(

delayed(process_daily_symbol)(group, annual_rf)

for group in symbol_groups

)

return pd.concat(results, ignore_index=True)

prices_daily = create_daily_dataset_parallel(prices)

# Quick validation

print("\nValidation checks:")

print(f"Any duplicate (symbol, date): {prices_daily.duplicated(subset=['symbol', 'date']).sum()}")

print(f"Sample of non-zero returns:")

print(prices_daily[prices_daily["ret"] != 0][["symbol", "date", "adjusted_close", "ret"]].head(10))

prices_daily.query("symbol == 'FPT'")[["symbol", "date", "adjusted_close", "ret"]].head(3)Processing 1,837 symbols using 87 cores...[Parallel(n_jobs=87)]: Using backend LokyBackend with 87 concurrent workers.

[Parallel(n_jobs=87)]: Done 26 tasks | elapsed: 7.8s

[Parallel(n_jobs=87)]: Done 276 tasks | elapsed: 10.5s

[Parallel(n_jobs=87)]: Done 626 tasks | elapsed: 11.7s

[Parallel(n_jobs=87)]: Done 1076 tasks | elapsed: 13.6s

[Parallel(n_jobs=87)]: Done 1626 tasks | elapsed: 16.0s

[Parallel(n_jobs=87)]: Done 1837 out of 1837 | elapsed: 16.6s finished

Validation checks:

Any duplicate (symbol, date): 0

Sample of non-zero returns:

symbol date adjusted_close ret

0 A32 2018-10-23 44.574418 NaN

27 A32 2018-11-29 55.072640 0.235521

30 A32 2018-12-04 48.188560 -0.125000

43 A32 2018-12-21 51.974804 0.078571

49 A32 2019-01-02 55.072640 0.059603

53 A32 2019-01-08 50.030370 -0.091557

74 A32 2019-02-13 44.289180 -0.114754

75 A32 2019-02-14 41.008500 -0.074074

78 A32 2019-02-19 36.087480 -0.120000

91 A32 2019-03-08 41.336568 0.145455| symbol | date | adjusted_close | ret | |

|---|---|---|---|---|

| 1146076 | FPT | 2010-01-04 | 1170.9885 | NaN |

| 1146077 | FPT | 2010-01-05 | 1170.9885 | 0.000000 |

| 1146078 | FPT | 2010-01-06 | 1149.6978 | -0.018182 |

# Select columns

daily_columns = [

"symbol", "date", "year", "month",

"open", "high", "low", "close", "volume",

"adjusted_close", "shrout", "mktcap", "mktcap_lag",

"ret", "risk_free", "ret_excess"

]

prices_daily = prices_daily[daily_columns]

# Remove observations with missing essential variables

prices_daily = prices_daily.dropna(subset=["ret_excess", "mktcap", "mktcap_lag"])

print("Daily Return Summary Statistics:")

print(prices_daily["ret"].describe().round(4))

print(f"\nFinal daily sample: {len(prices_daily):,} observations")Daily Return Summary Statistics:

count 3.462157e+06

mean 3.000000e-04

std 4.480000e-02

min -9.900000e-01

25% -4.900000e-03

50% 0.000000e+00

75% 4.000000e-03

max 3.250000e+01

Name: ret, dtype: float64

Final daily sample: 3,462,157 observations3.6.4.2 Tạo Dữ liệu Tháng

Đối với lợi nhuận hàng tháng, chúng ta tính toán lợi nhuận trực tiếp từ giá điều chỉnh cuối tháng thay vì lãi kép lợi nhuận hàng ngày. Điều này tránh được sai sót do lãi kép từ các ngày thiếu và là phương pháp tiêu chuẩn trong tài chính thực nghiệm.

- Phiên bản tuần tự

def create_monthly_dataset(df, annual_rf=0.04):

"""

Create monthly price dataset with returns computed from

month-end to month-end adjusted prices.

"""

df = df.copy()

# Sort by symbol and date (critical for correct return calculation)

df = df.sort_values(["symbol", "date"]).reset_index(drop=True)

# Remove duplicate dates within each symbol (keep last observation)

df = df.drop_duplicates(subset=["symbol", "date"], keep="last")

# Get month-end observations

monthly = (df

.groupby("symbol")

.resample("ME", on="date")

.agg({

"open": "first", # First day open

"high": "max", # Monthly high

"low": "min", # Monthly low

"close": "last", # Last day close

"volume": "sum", # Total monthly volume

"adjusted_close": "last", # Month-end adjusted price

"shrout": "last", # Month-end shares outstanding

"mktcap": "last", # Month-end market cap

"year": "last",

"month": "last"

})

.reset_index()

)

# Remove duplicate (symbol, date) after resampling (safety check)

monthly = monthly.drop_duplicates(subset=["symbol", "date"], keep="last")

# Sort again after resampling

monthly = monthly.sort_values(["symbol", "date"]).reset_index(drop=True)

# Compute monthly returns from month-end to month-end adjusted prices

monthly["ret"] = monthly.groupby("symbol")["adjusted_close"].pct_change()

# Cap extreme returns

monthly["ret"] = monthly["ret"].clip(lower=-0.99)

# Monthly risk-free rate

monthly["risk_free"] = annual_rf / 12

# Excess returns

monthly["ret_excess"] = monthly["ret"] - monthly["risk_free"]

monthly["ret_excess"] = monthly["ret_excess"].clip(lower=-1.0)

# Lagged market cap for portfolio weighting

monthly["mktcap_lag"] = monthly.groupby("symbol")["mktcap"].shift(1)

return monthly

prices_monthly = create_monthly_dataset(prices)- Phiên bản song song

from joblib import Parallel, delayed

import os

def process_monthly_symbol(symbol_df, annual_rf=0.04):

"""

Process a single symbol's data to monthly frequency.

"""

df = symbol_df.copy()

# Sort by date (critical for correct return calculation)

df = df.sort_values("date").reset_index(drop=True)

# Remove duplicate dates (keep last observation if duplicates exist)

df = df.drop_duplicates(subset=["date"], keep="last")

# Set date as index for resampling

df = df.set_index("date")

# Resample to monthly

monthly = df.resample("ME").agg({

"symbol": "last",

"open": "first",

"high": "max",

"low": "min",

"close": "last",

"volume": "sum",

"adjusted_close": "last",

"shrout": "last",

"mktcap": "last",

"year": "last",

"month": "last"

}).reset_index()

# Remove rows where symbol is NaN (months with no trading)

monthly = monthly.dropna(subset=["symbol"])

# Sort by date

monthly = monthly.sort_values("date").reset_index(drop=True)

# Compute monthly returns

monthly["ret"] = monthly["adjusted_close"].pct_change()

# Replace infinite values with NaN

monthly["ret"] = monthly["ret"].replace([np.inf, -np.inf], np.nan)

# Cap extreme returns

monthly["ret"] = monthly["ret"].clip(lower=-0.99)

# Monthly risk-free rate

monthly["risk_free"] = annual_rf / 12

# Excess returns

monthly["ret_excess"] = monthly["ret"] - monthly["risk_free"]

monthly["ret_excess"] = monthly["ret_excess"].clip(lower=-1.0)

# Lagged market cap

monthly["mktcap_lag"] = monthly["mktcap"].shift(1)

return monthly

def create_monthly_dataset_parallel(df, annual_rf=0.04):

"""

Create monthly price dataset using parallel processing.

"""

# Ensure data is sorted before splitting

df = df.sort_values(["symbol", "date"])

# Split by symbol

symbol_groups = [group for _, group in df.groupby("symbol")]

n_jobs = max(1, os.cpu_count() - 1)

print(f"Processing {len(symbol_groups):,} symbols using {n_jobs} cores...")

results = Parallel(n_jobs=n_jobs, verbose=1)(

delayed(process_monthly_symbol)(group, annual_rf)

for group in symbol_groups

)

return pd.concat(results, ignore_index=True)

prices_monthly = create_monthly_dataset_parallel(prices)

# Validation checks

print("\nValidation checks:")

print(f"Any duplicate (symbol, date): {prices_monthly.duplicated(subset=['symbol', 'date']).sum()}")

print(f"\nSample of non-zero returns:")

print(prices_monthly[prices_monthly["ret"] != 0][["symbol", "date", "adjusted_close", "ret"]].head(10))

prices_monthly.query("symbol == 'FPT'")[["symbol", "date", "adjusted_close", "ret"]].head(3)Processing 1,837 symbols using 87 cores...[Parallel(n_jobs=87)]: Using backend LokyBackend with 87 concurrent workers.

[Parallel(n_jobs=87)]: Done 26 tasks | elapsed: 0.2s

[Parallel(n_jobs=87)]: Done 378 tasks | elapsed: 1.8s

[Parallel(n_jobs=87)]: Done 1078 tasks | elapsed: 4.5s

[Parallel(n_jobs=87)]: Done 1664 out of 1837 | elapsed: 7.0s remaining: 0.7s

[Parallel(n_jobs=87)]: Done 1837 out of 1837 | elapsed: 7.7s finished

Validation checks:

Any duplicate (symbol, date): 0

Sample of non-zero returns:

symbol date adjusted_close ret

0 A32 2018-10-31 44.574418 NaN

1 A32 2018-11-30 55.072640 0.235521

2 A32 2018-12-31 51.974804 -0.056250

3 A32 2019-01-31 50.030370 -0.037411

4 A32 2019-02-28 36.087480 -0.278689

5 A32 2019-03-31 41.828670 0.159091

7 A32 2019-05-31 43.304976 0.035294

8 A32 2019-06-30 35.929125 -0.170323

9 A32 2019-07-31 37.525975 0.044444

10 A32 2019-08-31 38.324400 0.021277| symbol | date | adjusted_close | ret | |

|---|---|---|---|---|

| 55963 | FPT | 2010-01-31 | 1092.9226 | NaN |

| 55964 | FPT | 2010-02-28 | 1107.1164 | 0.012987 |

| 55965 | FPT | 2010-03-31 | 1185.1823 | 0.070513 |

# Select columns (same structure as daily)

monthly_columns = [

"symbol", "date", "year", "month",

"open", "high", "low", "close", "volume",

"adjusted_close", "shrout", "mktcap", "mktcap_lag",

"ret", "risk_free", "ret_excess"

]

prices_monthly = prices_monthly[monthly_columns]

# Remove observations with missing essential variables

prices_monthly = prices_monthly.dropna(subset=["ret_excess", "mktcap", "mktcap_lag"])

print("Monthly Return Summary Statistics:")

print(prices_monthly["ret"].describe().round(4))

print(f"\nFinal monthly sample: {len(prices_monthly):,} observations")Monthly Return Summary Statistics:

count 165499.0000

mean 0.0042

std 0.1862

min -0.9900

25% -0.0703

50% 0.0000

75% 0.0553

max 12.7500

Name: ret, dtype: float64

Final monthly sample: 165,499 observations3.6.5 Lưu trữ dữ liệu giá

prices_daily.to_sql(

name="prices_daily",

con=tidy_finance,

if_exists="replace",

index=False

)

print("Daily price data saved to database.")

prices_monthly.to_sql(

name="prices_monthly",

con=tidy_finance,

if_exists="replace",

index=False

)

print("Monthly price data saved to database.")3.7 Thống kê mô tả

Trước khi tiến hành phân tích giá tài sản, chúng ta xem xét các đặc điểm của mẫu để hiểu sự phát triển và thành phần của thị trường chứng khoán Việt Nam.

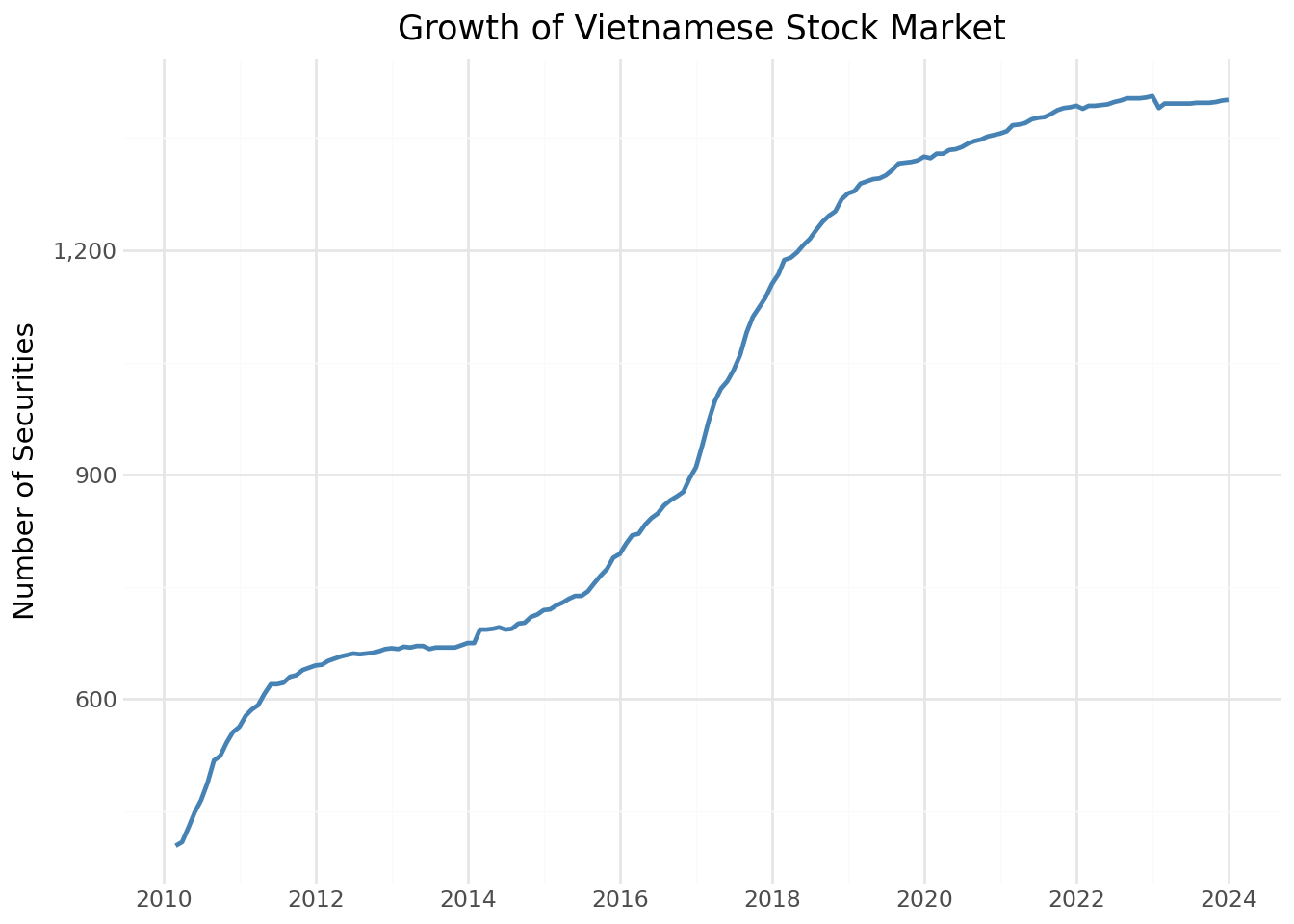

3.7.1 Sự phát triển của thị trường theo thời gian

Trước tiên, chúng ta kiểm tra số lượng chứng khoán niêm yết đã tăng lên như thế nào theo thời gian.

securities_over_time = (prices_monthly

.groupby("date")

.agg(

n_securities=("symbol", "nunique"),

total_mktcap=("mktcap", "sum")

)

.reset_index()

)securities_figure = (

ggplot(securities_over_time, aes(x="date", y="n_securities"))

+ geom_line(color="steelblue", size=1)

+ labs(

x="",

y="Number of Securities",

title="Growth of Vietnamese Stock Market"

)

+ scale_x_datetime(date_breaks="2 years", date_labels="%Y")

+ scale_y_continuous(labels=comma_format())

+ theme_minimal()

)

securities_figure.show()

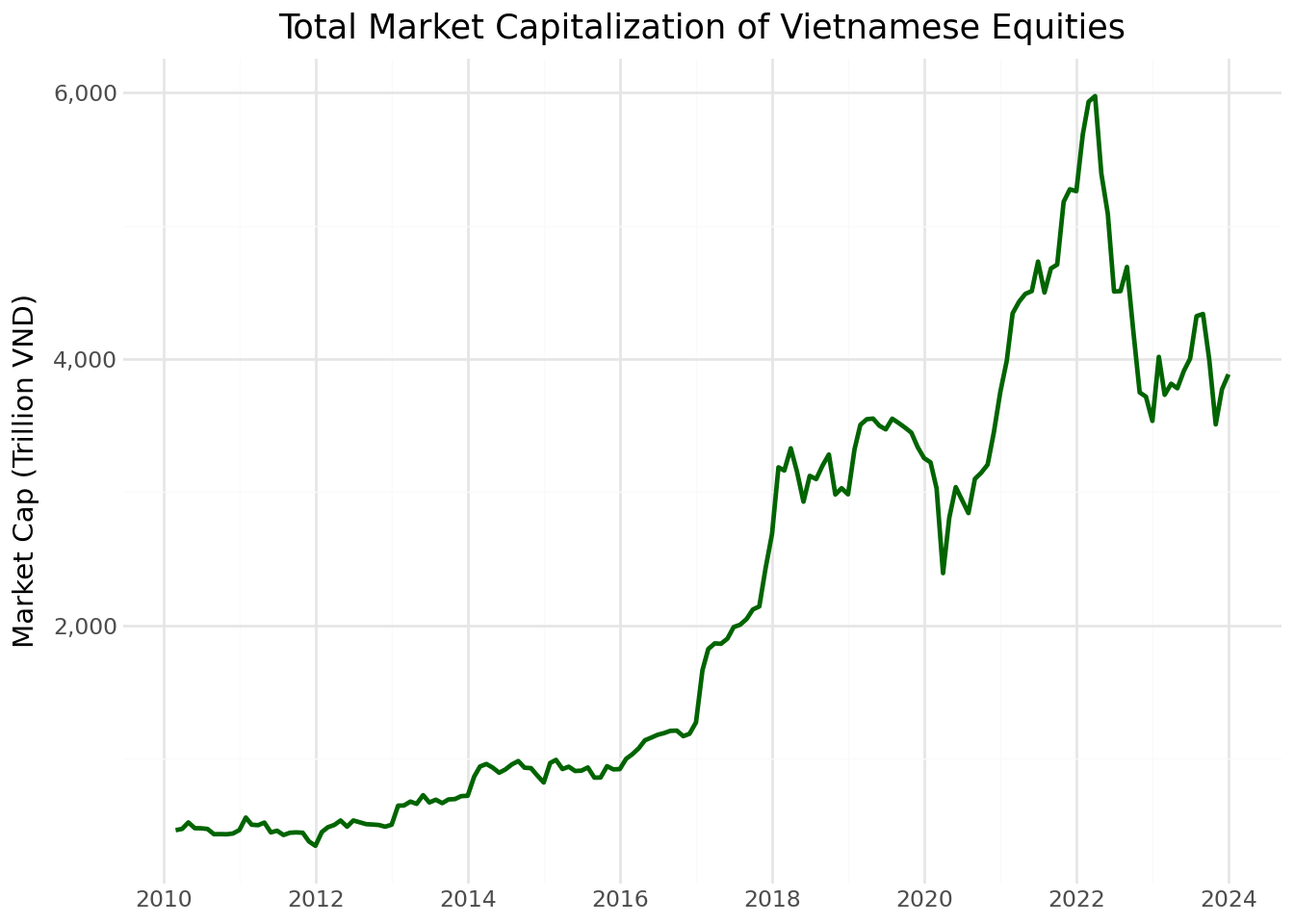

3.7.2 Sự phát triển của Tổng vốn hóa thị trường

Tổng vốn hóa thị trường phản ánh quy mô và sự phát triển chung của thị trường chứng khoán Việt Nam.

mktcap_figure = (

ggplot(securities_over_time, aes(x="date", y="total_mktcap / 1000"))

+ geom_line(color="darkgreen", size=1)

+ labs(

x="",

y="Market Cap (Trillion VND)",

title="Total Market Capitalization of Vietnamese Equities"

)

+ scale_x_datetime(date_breaks="2 years", date_labels="%Y")

+ scale_y_continuous(labels=comma_format())

+ theme_minimal()

)

mktcap_figure.show()

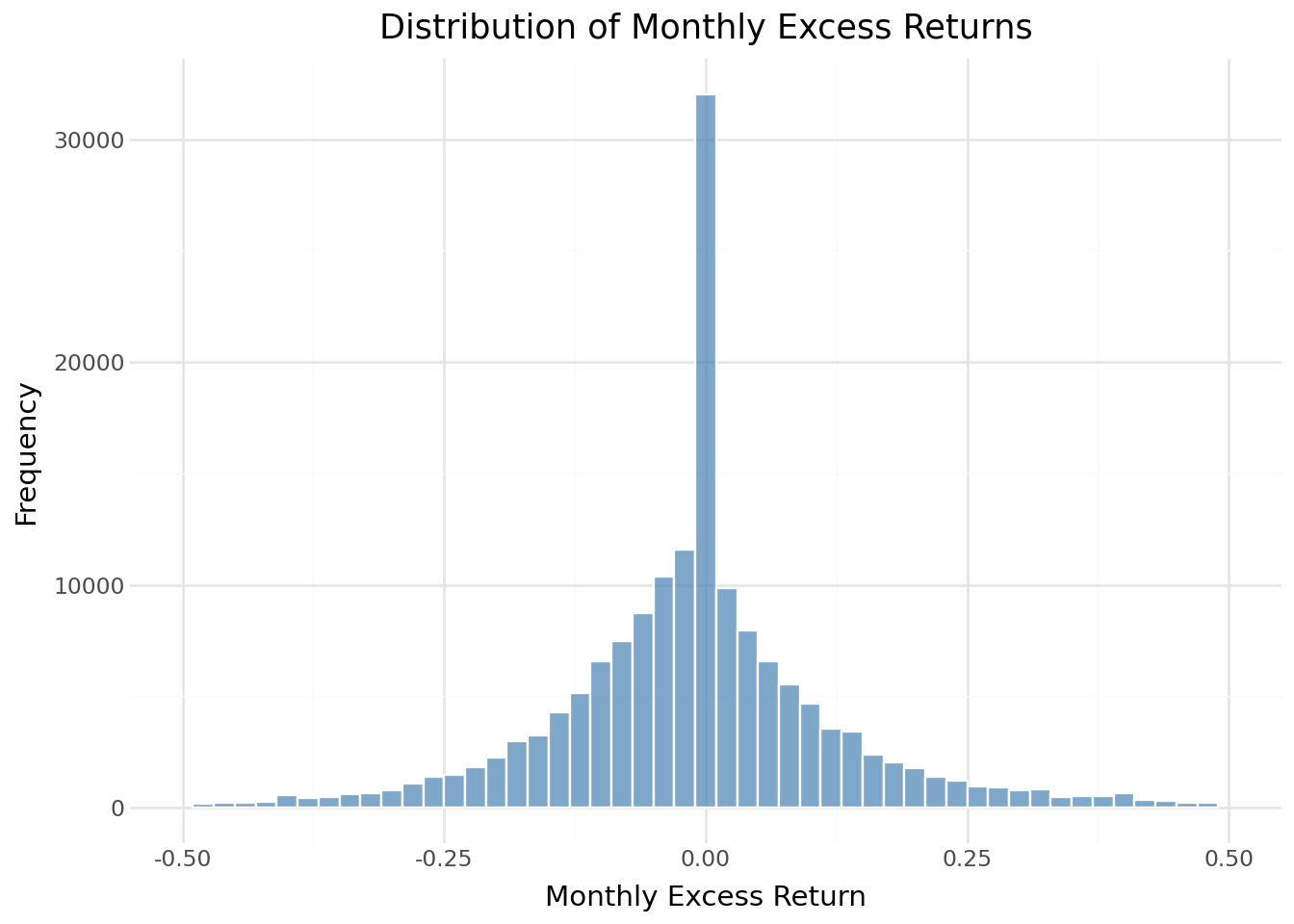

3.7.3 Phân phối lợi nhuận

Việc hiểu rõ sự phân bố lợi nhuận hàng tháng giúp xác định các vấn đề tiềm ẩn về chất lượng dữ liệu và đánh giá rủi ro thị trường.

return_distribution = (

ggplot(prices_monthly, aes(x="ret_excess"))

+ geom_histogram(

binwidth=0.02,

fill="steelblue",

color="white",

alpha=0.7

)

+ labs(

x="Monthly Excess Return",

y="Frequency",

title="Distribution of Monthly Excess Returns"

)

+ scale_x_continuous(limits=(-0.5, 0.5))

+ theme_minimal()

)

return_distribution.show()/home/mikenguyen/project/tidyfinance/.venv/lib/python3.13/site-packages/plotnine/layer.py:293: PlotnineWarning: stat_bin : Removed 3264 rows containing non-finite values.

/home/mikenguyen/project/tidyfinance/.venv/lib/python3.13/site-packages/plotnine/layer.py:374: PlotnineWarning: geom_histogram : Removed 2 rows containing missing values.

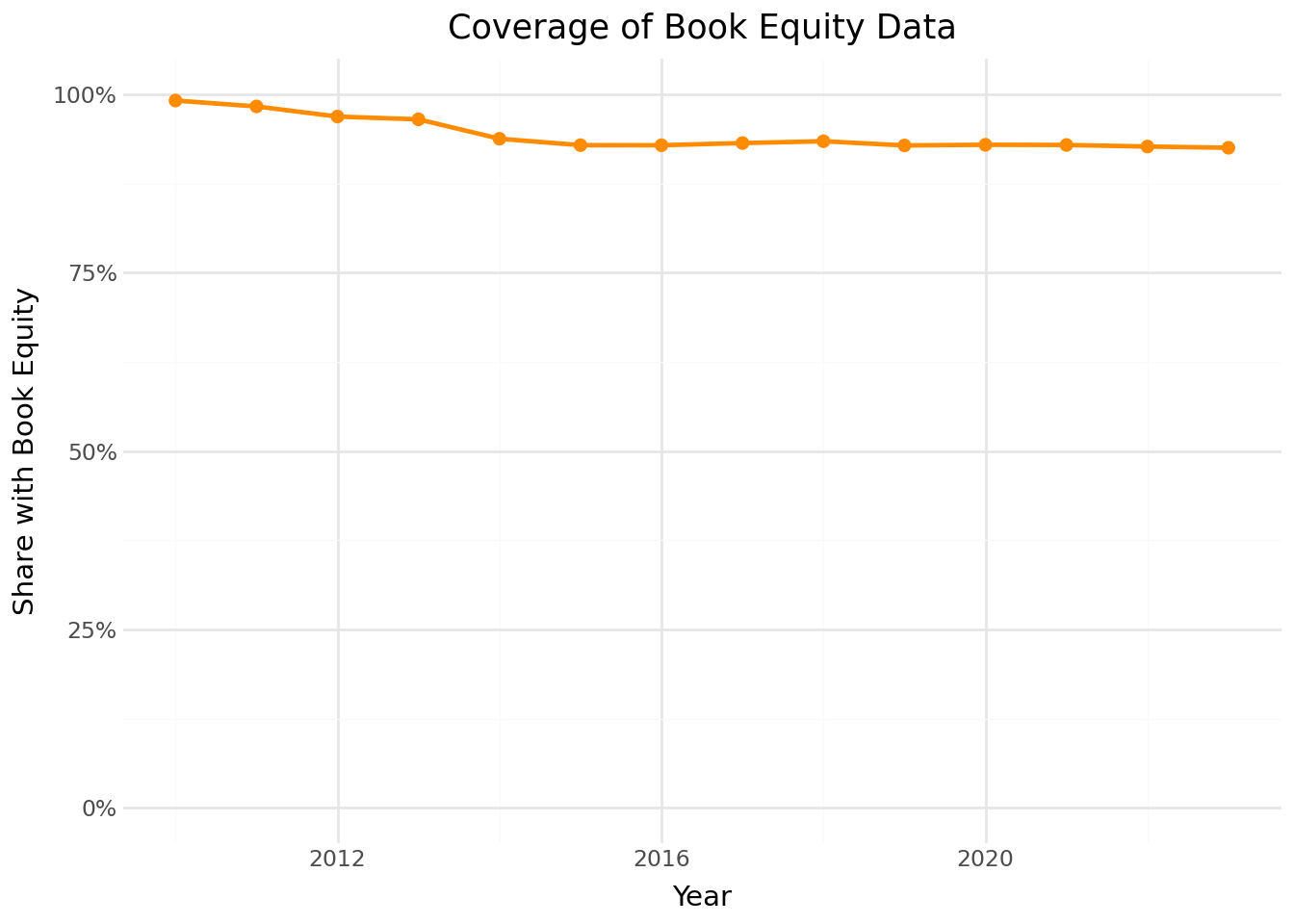

3.7.4 Phạm vi Giá Trị Sổ Sách của Vốn Chủ Sở Hữu

Vốn chủ sở hữu sổ sách là điều cần thiết để xây dựng danh mục đầu tư giá trị. Chúng ta kiểm tra phần nào trong mẫu của chúng ta có dữ liệu vốn chủ sở hữu sổ sách theo thời gian.

# Merge prices with fundamentals

coverage_data = (prices_monthly

.assign(year=lambda x: x["date"].dt.year)

.groupby(["symbol", "year"])

.tail(1)

.merge(comp_vn[["symbol", "year", "be"]],

on=["symbol", "year"],

how="left")

)

# Compute coverage by year

be_coverage = (coverage_data

.groupby("year")

.apply(lambda x: pd.Series({

"share_with_be": x["be"].notna().mean()

}))

.reset_index()

)

coverage_figure = (

ggplot(be_coverage, aes(x="year", y="share_with_be"))

+ geom_line(color="darkorange", size=1)

+ geom_point(color="darkorange", size=2)

+ labs(

x="Year",

y="Share with Book Equity",

title="Coverage of Book Equity Data"

)

+ scale_y_continuous(labels=percent_format(), limits=(0, 1))

+ theme_minimal()

)

coverage_figure.show()

3.8 Hợp nhất cổ phiếu và dữ liệu cơ bản

Bước cuối cùng liên kết dữ liệu giá với dữ liệu cơ bản bằng cách sử dụng biểu tượng chứng khoán làm mã định danh chung. Bộ dữ liệu hợp nhất này tạo cơ sở để xây dựng danh mục đầu tư được sắp xếp theo đặc điểm của công ty.

# Example: Create merged dataset for end-of-June each year

merged_data = (prices_monthly

.query("month == 6")

.merge(

comp_vn[["symbol", "year", "be", "op", "inv", "at"]],

on=["symbol", "year"],

how="left",

suffixes=("", "_fundamental")

)

)

# Convert BE from VND to BILLION VND

merged_data["be"] = merged_data["be"] / 1e9

# Compute book-to-market ratio

merged_data["bm"] = merged_data["be"] / merged_data["mktcap"]

merged_data.loc[

(merged_data["bm"] <= 0) |

(merged_data["bm"] > 20),

"bm"

] = pd.NA

merged_data["bm"].describe(percentiles=[.01, .1, .5, .9, .99])

print(f"Merged observations: {len(merged_data):,}")

print(f"With book-to-market: {merged_data['bm'].notna().sum():,}")

merged_data.head(3)

merged_data.describe()

merged_dataMerged observations: 13,756

With book-to-market: 12,859| symbol | date | year | month | open | high | low | close | volume | adjusted_close | ... | mktcap | mktcap_lag | ret | risk_free | ret_excess | be | op | inv | at | bm | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | A32 | 2019-06-30 | 2019.0 | 6.0 | 26.4 | 26.4 | 21.0 | 22.5 | 3700 | 35.929125 | ... | 153.000 | 179.52 | -0.170323 | 0.003333 | -0.173657 | 223.612748 | 0.232362 | -0.072329 | 4.349303e+11 | 1.461521 |

| 1 | A32 | 2020-06-30 | 2020.0 | 6.0 | 25.0 | 26.3 | 24.5 | 26.3 | 7500 | 38.811173 | ... | 178.840 | 187.00 | -0.067977 | 0.003333 | -0.071311 | 242.216943 | 0.195565 | 0.122698 | 4.882955e+11 | 1.354378 |

| 2 | A32 | 2021-06-30 | 2021.0 | 6.0 | 30.2 | 37.0 | 29.5 | 32.0 | 78400 | 45.363520 | ... | 217.600 | 214.20 | 0.015873 | 0.003333 | 0.012540 | 238.385190 | 0.157723 | 0.081581 | 5.281309e+11 | 1.095520 |

| 3 | A32 | 2022-06-30 | 2022.0 | 6.0 | 30.9 | 35.5 | 25.0 | 35.3 | 15200 | 47.503210 | ... | 240.040 | 210.12 | 0.142395 | 0.003333 | 0.139061 | 215.399735 | 0.172085 | 0.036584 | 5.474523e+11 | 0.897349 |

| 4 | A32 | 2023-06-30 | 2023.0 | 6.0 | 30.1 | 33.5 | 29.2 | 29.4 | 2400 | 35.064204 | ... | 199.920 | 204.68 | -0.023256 | 0.003333 | -0.026589 | 222.024135 | 0.174658 | -0.076752 | 5.054342e+11 | 1.110565 |

| ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... |

| 13751 | YTC | 2019-06-30 | 2019.0 | 6.0 | 70.0 | 79.9 | 70.0 | 79.9 | 38900 | 171.451817 | ... | 246.092 | 215.60 | 0.141429 | 0.003333 | 0.138095 | 59.901389 | 0.738190 | -0.021758 | 7.521980e+11 | 0.243411 |

| 13752 | YTC | 2020-06-30 | 2020.0 | 6.0 | 88.5 | 88.5 | 77.0 | 87.0 | 150640 | 180.966960 | ... | 267.960 | 272.58 | -0.016949 | 0.003333 | -0.020282 | 13.459082 | -0.458548 | 0.323501 | 9.955348e+11 | 0.050228 |

| 13753 | YTC | 2021-06-30 | 2021.0 | 6.0 | 76.0 | 115.5 | 61.0 | 61.0 | 34100 | 126.884880 | ... | 187.880 | 234.08 | -0.197368 | 0.003333 | -0.200702 | 21.746595 | 0.539521 | -0.215694 | 7.808035e+11 | 0.115747 |

| 13754 | YTC | 2022-06-30 | 2022.0 | 6.0 | 68.0 | 68.0 | 65.0 | 65.5 | 200 | 136.245240 | ... | 201.740 | 209.44 | -0.036765 | 0.003333 | -0.040098 | 32.403055 | 0.483088 | 0.182911 | 9.236206e+11 | 0.160618 |

| 13755 | YTC | 2023-06-30 | 2023.0 | 6.0 | 59.0 | 59.0 | 59.0 | 59.0 | 49545 | 122.724720 | ... | 181.720 | 181.72 | 0.000000 | 0.003333 | -0.003333 | 38.976624 | 0.450157 | 0.017930 | 9.401815e+11 | 0.214487 |

13756 rows × 21 columns

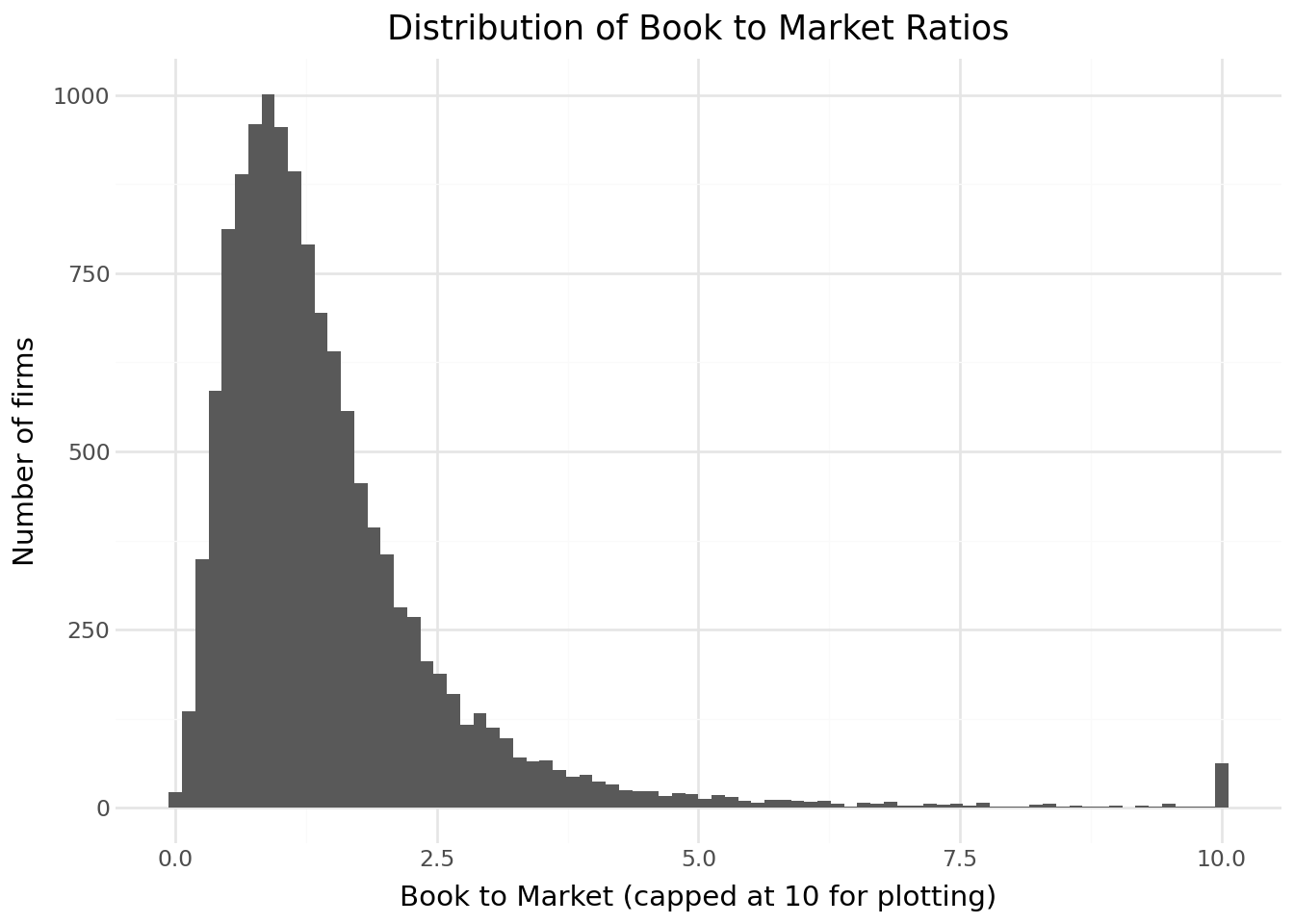

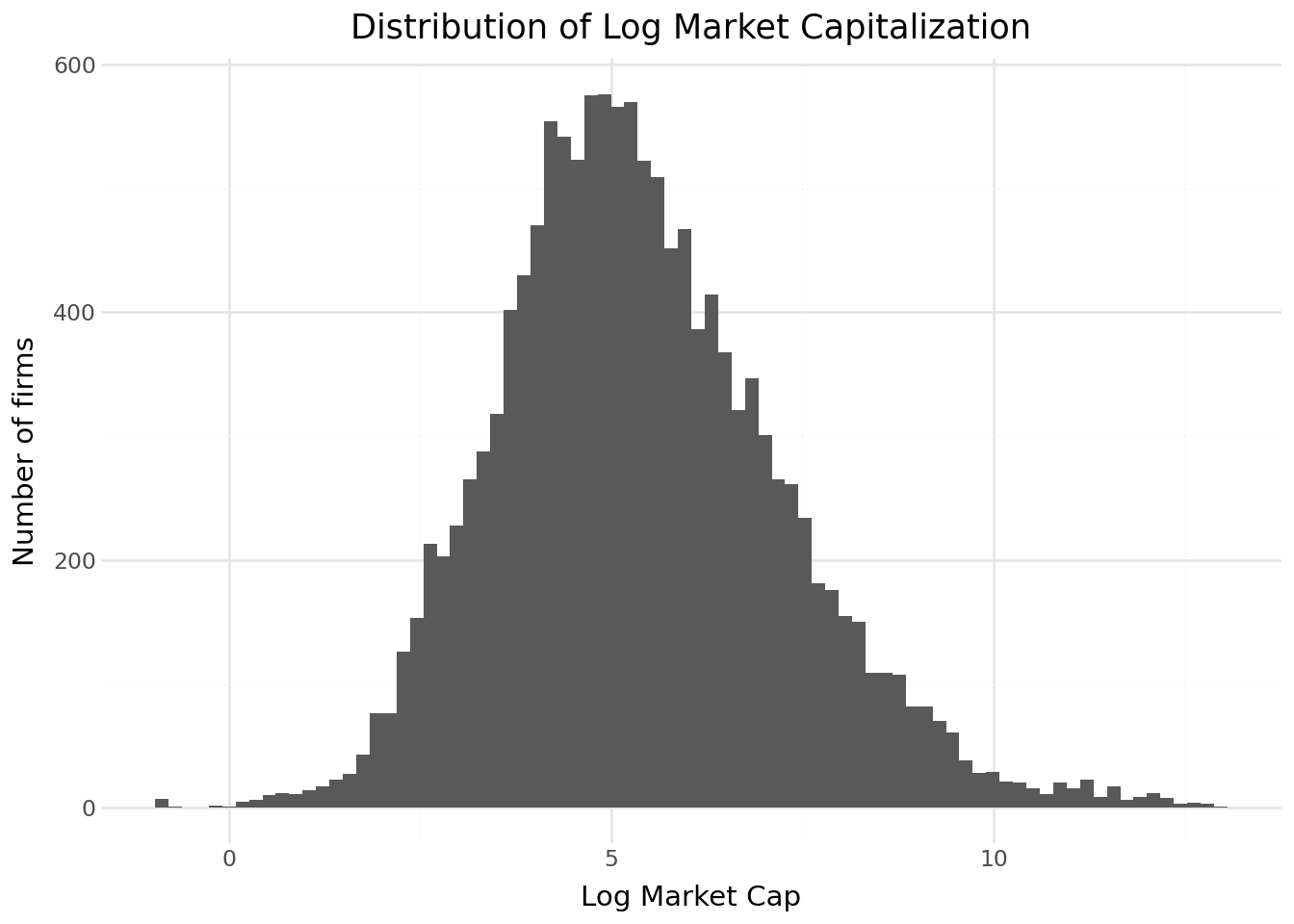

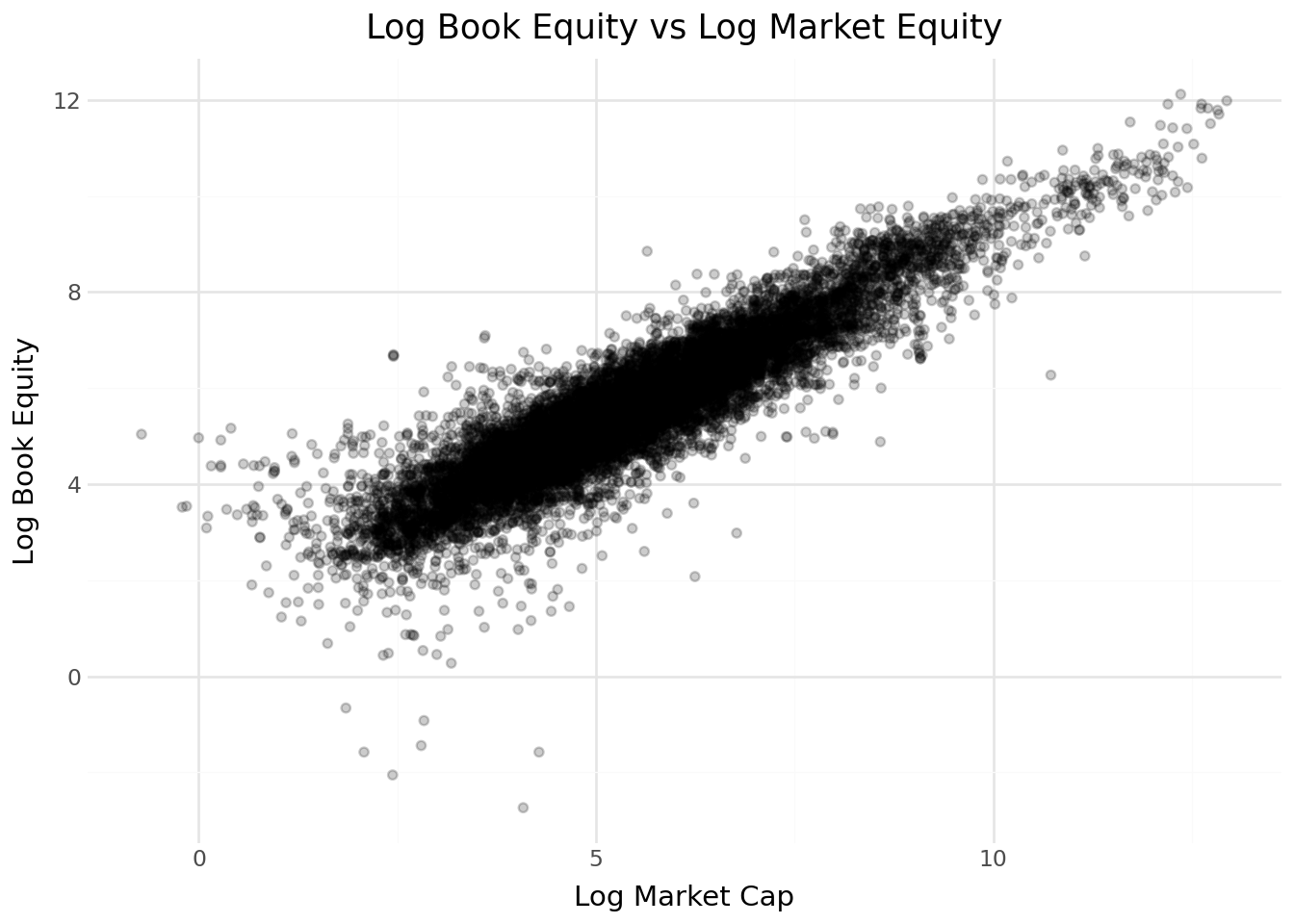

from plotnine import *

import numpy as np

bm_plot_data = (

merged_data[["bm"]]

.dropna()

.assign(bm_plot=lambda x: x["bm"].clip(upper=10))

)

(

ggplot(bm_plot_data, aes(x="bm_plot")) +

geom_histogram(bins=80) +

labs(

title="Distribution of Book to Market Ratios",

x="Book to Market (capped at 10 for plotting)",

y="Number of firms"

) +

theme_minimal()

)

size_plot_data = (

merged_data[["mktcap_lag"]]

.dropna()

.assign(log_size=lambda x: np.log(x["mktcap_lag"]))

)

(

ggplot(size_plot_data, aes(x="log_size")) +

geom_histogram(bins=80) +

labs(

title="Distribution of Log Market Capitalization",

x="Log Market Cap",

y="Number of firms"

) +

theme_minimal()

)

scatter_data = (

merged_data[["be", "mktcap_lag"]]

.dropna()

.assign(

log_be=lambda x: np.log(x["be"]),

log_me=lambda x: np.log(x["mktcap_lag"])

)

)

(

ggplot(scatter_data, aes(x="log_me", y="log_be")) +

geom_point(alpha=0.2) +

labs(

title="Log Book Equity vs Log Market Equity",

x="Log Market Cap",

y="Log Book Equity"

) +

theme_minimal()

)

3.9 Những điểm chính cần ghi nhớ

Datacore cung cấp quyền truy cập thống nhất vào dữ liệu tài chính Việt Nam thông qua cơ sở hạ tầng điện toán đám mây hiện đại, loại bỏ nhu cầu tổng hợp dữ liệu từ nhiều nguồn phân tán.

Các yếu tố cơ bản của công ty từ Datacore bao gồm bảng cân đối kế toán, báo cáo kết quả kinh doanh và dữ liệu lưu chuyển tiền tệ toàn diện được lập theo Chuẩn mực Kế toán Việt Nam, mà chúng ta đối chiếu với các biến số chuẩn được sử dụng trong nghiên cứu quốc tế.

Cách tính giá trị sổ sách tuân theo phương pháp Fama-French, có tính đến thuế hoãn lại và cổ phiếu ưu đãi để đảm bảo tính tương đồng với các nghiên cứu tại Hoa Kỳ.

Dữ liệu giá cổ phiếu bao gồm các yếu tố điều chỉnh cho các hoạt động của công ty, cho phép tính toán lợi nhuận chính xác trong thời gian dài.

Tần suất hàng tháng là tiêu chuẩn trong nghiên cứu định giá tài sản, giúp giảm nhiễu trong khi vẫn duy trì đủ số liệu quan sát để suy luận thống kê.

Phương pháp ước tính lãi suất phi rủi ro sử dụng lợi suất trái phiếu chính phủ Việt Nam làm thước đo thay thế, do không có chuỗi lãi suất ngắn hạn tiêu chuẩn tương đương với tín phiếu kho bạc Mỹ.

Kiểm định chất lượng dữ liệu thông qua thống kê mô tả và trực quan hóa giúp xác định các vấn đề tiềm ẩn trước khi tiến hành phân tích chính thức.

Xử lý theo lô cho phép xử lý hiệu quả các tập dữ liệu lớn hàng ngày mà nếu không sẽ vượt quá giới hạn bộ nhớ.